Global Transactional Video-On-Demand Market Size, Share, Trends, & Growth Forecast Report By Access (OTT Streaming, Desktops & Laptops, Smartphones & Tablets, Smart TVs, and Other devices); Content (Entertainment, Food, Travel & Fashion, Games & Sports, Kids and Others); Availability (Electronic Sell-Through and Download to Rent), and Regional - (2024 to 2033)

Global Transactional Video-On-Demand Market Size

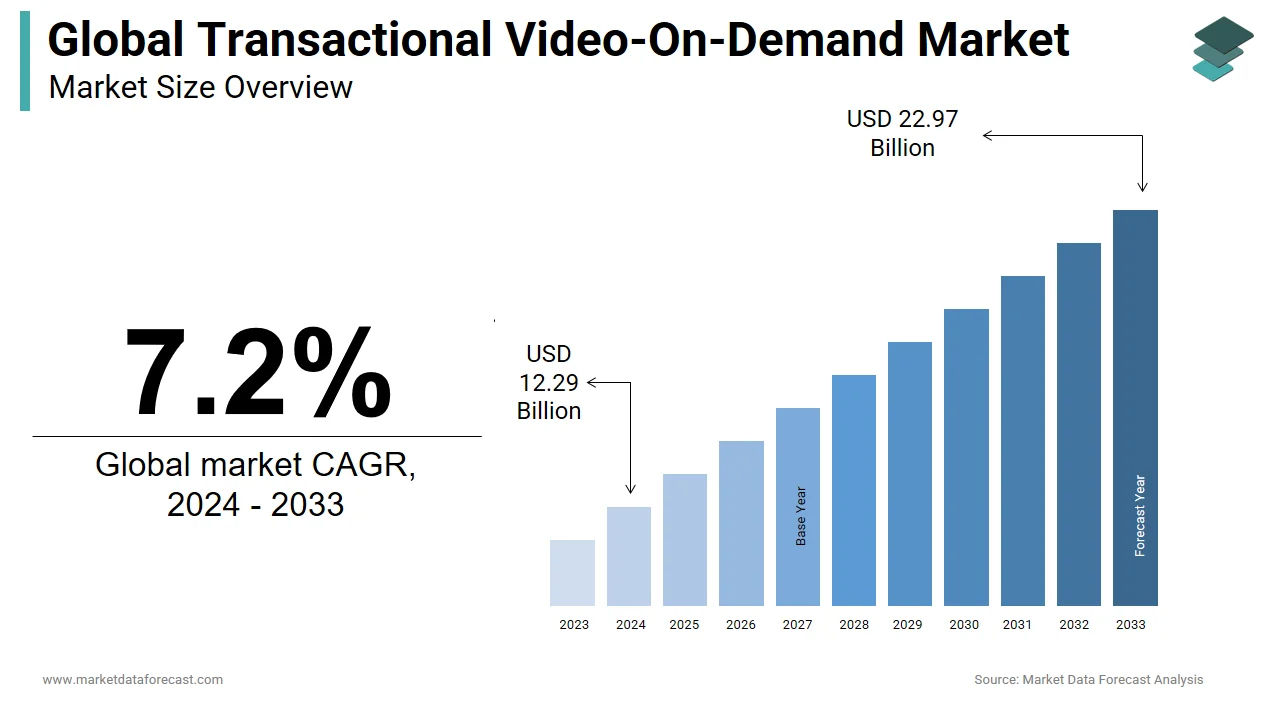

The global transactional video-on-demand market is projected to grow from USD 12.29 billion in 2024 to USD 22.97 billion by 2033, at a CAGR of 7.2%.

Transactional Video-On-Demand (TVOD) is a digital content consumption model where users pay for individual media items, such as movies or series, on a per-view basis rather than subscribing to a recurring service. This approach offers flexibility and caters to consumers who prefer occasional access without long-term financial commitment. TVOD includes both electronic sell-through (EST), where content is purchased permanently, and pay-per-view (PPV), where users rent content for a limited period. The market has evolved significantly with advancements in streaming technology, improved internet penetration, and shifting consumer preferences toward personalized entertainment. In recent years, the global TVOD market has demonstrated steady growth, driven by increasing demand for high-quality digital content and the expansion of online platforms. Moreover, emerging markets are witnessing gradual adoption, supported by growing smartphone usage and localized content offerings. This evolving landscape shows the relevance of TVOD as a critical component within the broader digital entertainment ecosystem.

MARKET DRIVERS

Increasing Demand for High-Quality Original Content

The rising consumer appetite for premium and exclusive original content is one of the primary drivers fueling the growth of the Transactional Video-On-Demand (TVOD) market. As viewers become more selective about what they watch, studios and digital platforms are investing heavily in producing high-budget films, documentaries, and short-form content tailored for on-demand purchase or rental. This trend has been further amplified by the success of independent filmmakers leveraging digital distribution channels to reach global audiences without relying on traditional theatrical releases. Moreover, the surge in home entertainment consumption post-pandemic has reinforced the viability of transactional models.

Rising Penetration of Smart Devices and Broadband Connectivity

The widespread adoption of smart devices has significantly contributed to the growth of the Transactional Video-On-Demand (TVOD) market. Such as smartphones, tablets, smart TVs, and streaming sticks. These devices offer seamless access to digital content, enabling users to rent or purchase videos anytime and anywhere. Simultaneously, the global expansion of high-speed broadband and mobile networks has enhanced streaming quality, reducing buffering times and improving overall user experience. In parallel, as per Ookla's Speedtest Global Index, median fixed broadband download speeds exceeded 85 Mbps globally in Q1 2024, marking a substantial improvement compared to previous years. These developments have made digital content delivery more efficient, encouraging greater participation in transactional viewing models. These technological enablers not only enhance accessibility but also expand the addressable audience base for TVOD platforms, making them pivotal to the market’s continued expansion.

MARKET RESTRAINTS

Intense Competition from Subscription-Based Streaming Services

The dominance and aggressive expansion of subscription-based video-on-demand (SVOD) platforms is one of the most significant restraints facing the Transactional Video-On-Demand (TVOD) market. Services such as Netflix, Amazon Prime Video, Disney+, and Hulu have gained massive global traction by offering unlimited content access at relatively low monthly fees. This pricing model often proves more cost-effective for frequent viewers, thereby diverting potential customers away from transactional models that require payment per title. Moreover, major studios have increasingly shifted their focus toward proprietary SVOD platforms, limiting the availability of premium content on third-party TVOD services. For example, Warner Bros. Discovery prioritizes HBO Max for new film releases, reducing the number of titles available for digital sale or rent immediately after theatrical runs. This strategic move restricts the diversity of content accessible via TVOD, diminishing its appeal among consumers seeking immediate access to new releases. Such competitive pressures hinder the organic growth trajectory of the TVOD market despite its inherent flexibility and on-demand nature.

Piracy and Unauthorized Distribution of Digital Content

Piracy remains a persistent challenge for the Transactional Video-On-Demand (TVOD) market, undermining legitimate revenue streams and deterring content creators from investing in digital-first distribution strategies. Despite efforts by governments and industry stakeholders to curb unauthorized access, illegal streaming sites and torrent platforms continue to proliferate, offering free access to premium content shortly after official releases. This undermines the value proposition of paying for individual titles and erodes consumer trust in legal platforms. Notably, high-profile releases such as Fast X and Spider-Man: Across the Spider-Verse were illegally downloaded millions of times within days of their launch, affecting potential sales on TVOD platforms. In regions like Southeast Asia and Latin America, where digital enforcement mechanisms are weaker, piracy rates remain particularly high. Furthermore, there is a significant share of internet users access unlicensed music content often using statistics around 30–40% of consumers being involved in music piracy. This widespread behavior reduces the incentive for consumers to engage with legitimate TVOD services, especially when similar content is available at no cost through illicit channels.

MARKET OPPORTUNITIES

Expansion into Emerging Markets with Growing Disposable Incomes

Expanding its presence in emerging economies where disposable incomes are steadily rising, and digital infrastructure is rapidly improving is providing a significant opportunity for the Transactional Video-On-Demand (TVOD) market. Countries in Southeast Asia, Latin America, and Sub-Saharan Africa are witnessing a growing middle class with increased purchasing power, creating a conducive environment for digital content consumption on a pay-per-view basis. According to the World Bank, per capita GDP in countries such as Indonesia, Vietnam, and India grew annually between 2020 and 2023. This economic upliftment has translated into higher consumer spending on entertainment, particularly digital formats. In addition, local content production in these regions is gaining momentum, attracting international distributors to partner with domestic studios. For instance, South Korea’s K-content boom has led to increased digital rentals and purchases beyond its borders, with platforms like Rakuten Viki capitalizing on this demand.

Integration with Gaming and Interactive Media Platforms

Integration with gaming and interactive media ecosystems is an emerging avenue for growth in the Transactional Video-On-Demand (TVOD) market as digital entertainment converges, and platforms that combine video content with immersive experiences are gaining traction among younger audiences. This opens new avenues for TVOD providers to monetize content through hybrid models that blend storytelling with interactivity, appealing to tech-savvy consumers who seek dynamic engagement. Within this ecosystem, platforms like Xbox, PlayStation, and Steam already host integrated video stores where users can rent or purchase films alongside games. Moreover, interactive streaming technologies such as those developed by Netflix with "Bandersnatch" and emerging AI-driven narrative platforms are pushing boundaries in how content is consumed.

MARKET CHALLENGES

Fragmentation of Distribution Channels and Licensing Complexities

The fragmentation of distribution channels and the complexities associated with content licensing across different territories is a significant challenge confronting the Transactional Video-On-Demand (TVOD) market. Unlike subscription-based models, which often operate under centralized agreements, TVOD platforms must navigate a highly dispersed ecosystem involving multiple regional players, including studios, broadcasters, and digital retailers. This fragmentation complicates content availability and pricing consistency, ultimately affecting consumer satisfaction and platform scalability. For instance, a film may be available for rental on Apple TV+ in the United States but inaccessible in parts of Europe or Asia due to exclusive distribution rights held by local partners. Also, the lack of standardization increases operational costs for content owners and diminishes consumer convenience, as users must subscribe to or transact on multiple platforms to access desired content.

Declining Average Revenue per User Due to Price Sensitivity

The declining average revenue per user (ARPU) caused by heightened price sensitivity among consumers is a pressing challenge for the Transactional Video-On-Demand (TVOD) market. While transactional models offer flexibility, many users perceive individual content purchases or rentals as expensive relative to alternative forms of entertainment. This perception limits repeat transactions and discourages impulse buying, constraining revenue growth for TVOD platforms. Furthermore, promotional strategies such as discounted rentals and time-limited offers, while effective in driving short-term engagement, contribute to lower ARPU over time. Apart from these, TVOD providers must innovate with tiered pricing models, bundling select titles, or introducing micro-transactions for short-form content. Without such adaptations, sustaining profitability in an increasingly cost-conscious market will remain a formidable challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Access, Content, Availability, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Eros International (India), Iflix (Malaysia), Tencent (China), LeEco (China), Rakuten (Japan), Disney (US), Amazon (US), Apple Inc (US), Comcast Corp (US), Vivendi (France), Filmdoo (UK), Icflix (UAE)Tving (South Korea) and Others. |

SEGMENTAL ANALYSIS

By Access Insights

The smartphones & tablets segment dominated the Transactional Video-On-Demand (TVOD) market by accounting for 42.4% of total revenue share in 2024. This dominance of the smartphones & tablets segment is primarily attributed to the widespread adoption of mobile devices and the increasing consumption of digital content on the go. The convenience of accessing transactional content anytime and anywhere has made smartphones and tablets the preferred medium for TVOD engagement. The improvement in mobile internet speeds, which enhances streaming quality and reduces buffering delays, also drives the growth of this segment. Additionally, platforms like Apple TV+ and Google Play Movies have optimized their mobile apps for ease of use, contributing to higher conversion rates. Another major factor is the rising number of mobile-first consumers, particularly in emerging markets.

The smart TVs segment is projected to grow at the fastest pace, registering a CAGR of 14.2% between 2025 and 20233. Increasing penetration of connected television sets and the integration of built-in streaming applications that facilitate direct access to TVOD content is majorly propelling the growth of the smart TVs segment. These devices come pre-installed with apps such as Amazon Prime Video, Apple TV+, and Roku Channel, enabling users to rent or purchase movies directly without external devices. A key growth driver is the rising preference for large-screen entertainment within households, especially post-pandemic. These devices come pre-installed with apps such as Amazon Prime Video, Apple TV+, and Roku Channel, enabling users to rent or purchase movies directly without external devices. Furthermore, the emergence of voice-controlled interfaces and AI-driven recommendation engines has enhanced user engagement on smart TVs, making them more interactive and personalized. Also, partnerships between TV manufacturers and streaming platforms such as Samsung’s collaboration with Universal+ and LG’s integration with Apple TV app are accelerating the adoption of transactional models on larger screens. These developments position smart TVs as a critical growth engine for the TVOD market in the coming years.

By Content Insights

The entertainment segment held the largest market share of 65.5% in the Transactional Video-On-Demand (TVOD) market. Sustained consumer demand for premium films, exclusive releases, and cinematic experiences is mainly driving the growth of the entertainment segment. This dominance is also supported by the continued appeal of blockbuster movies and independent films available for digital rental or purchase shortly after theatrical release. Platforms like Vudu, iTunes, and Google Play Movies have seen spikes in sales during premiere weekends, reflecting strong consumer interest in time-sensitive content. Moreover, the rise of hybrid release strategies where films debut simultaneously in theaters and digital stores has further bolstered the entertainment segment. In addition, international film markets, including Bollywood and K-content, are increasingly leveraging TVOD for monetization. These factors collectively reinforce entertainment as the dominant content category in the TVOD landscape.

The Games & Sports content segment is experiencing the fastest growth in the Transactional Video-On-Demand (TVOD) market and is expanding at a CAGR of 16.8% in the coming years. This surge is fueled by increasing consumer interest in niche sports events, esports tournaments, and game-related documentaries or behind-the-scenes content that are not typically included in subscription-based libraries. For instance, the 2023 League of Legends World Championship was a major global esports event with a record-breaking viewership of over 6.4 million peak concurrent viewers, indicating a growing willingness to spend on premium gaming content. Simultaneously, traditional sports leagues have embraced transactional models to monetize secondary events and highlight reels. Furthermore, platforms like the PlayStation Store and Xbox Video have integrated sports documentaries and game development stories into their TVOD offerings, attracting both casual viewers and dedicated enthusiasts.

By Availability Insights

The Electronic Sell-Through (EST) segment led the Transactional Video-On-Demand (TVOD) market by accounting for 58.6% of total revenue in 2024. Consumer preference for permanent ownership of digital content, particularly among families and collectors who seek long-term access to favorite films and series is one of the aspects propelling the growth of the EST segment. Unlike rentals, EST allows users to build personal digital libraries, enhancing perceived value despite higher upfront costs. Another key driver is the bundling of digital copies with physical media purchases. Moreover, cloud storage services like Disney Digital Plus and Warner Bros. Locker have enabled users to stream purchased content across multiple devices, improving accessibility and convenience. Also, parental control features and offline playback capabilities make EST appealing for household usage. These factors collectively sustain EST’s leadership in the TVOD availability segment.

The download-to-rent (DTR) segment is the fastest-growing availability mode in the Transactional Video-On-Demand (TVOD) market and is expanding at a CAGR of 13.5% between 2023 and 2029. Shifting consumer preferences toward flexible, short-term access to premium content without long-term commitment or high costs is majorly contributing to the rise of the DTR segment. An additional key factor is the strategic rollout of early digital rentals by studios to maximize revenue windows. This model allows studios to capture peak consumer demand while avoiding direct competition with SVOD exclusives. Besides, improved offline playback functionality has boosted DTR usage, particularly among travelers and users in low-connectivity areas. Platforms like Amazon Prime Video and FandangoNow now allow rented content to be downloaded and viewed later without requiring continuous streaming. These enhancements are strengthening DTR’s position as a high-growth segment in the TVOD market.

REGIONAL ANALYSIS

North America Transactional Video-On-Demand Market Insights

North America remained the largest regional contributor to the Transactional Video-On-Demand (TVOD) market by holding a share of 37.6% in 2024. The United States, in particular, drives this dominance due to high digital literacy, robust broadband infrastructure, and a mature ecosystem of digital storefronts such as Apple TV+, Google Play Movies, and Vudu. Consumer behavior in North America is heavily influenced by early digital releases of major Hollywood films. Additionally, the prevalence of bundled promotions, such as free digital codes with physical disc purchases, has further incentivized consumer participation. The region also benefits from advanced payment systems and a high level of trust in digital transactions, ensuring smooth user experiences. With ongoing investments from major studios in hybrid distribution models, North America is poised to maintain its leadership in the TVOD space for the foreseeable future.

Europe Transactional Video-On-Demand Market Insights

Europe steady growth in the Transactional Video-On-Demand (TVOD) market is supported by a combination of technological maturity and regulatory alignment with digital rights management. Countries such as the UK, Germany, and France lead the region in terms of transactional content spending. A primary driver of growth is the increasing availability of localized content. European studios and broadcasters have been actively digitizing their catalogs, making classic films and regional productions accessible through digital storefronts. Moreover, regulatory frameworks such as the EU Audiovisual Media Services Directive have encouraged legal content distribution while curbing piracy. The directive mandates that platforms provide fair compensation to content creators, fostering a sustainable environment for TVOD providers. Additionally, the proliferation of 5G networks across Western Europe has enhanced streaming quality, encouraging greater uptake of digital rentals and purchases. Despite challenges related to fragmented licensing agreements, Europe continues to present substantial opportunities for TVOD expansion, particularly through cross-border digital storefronts and localized marketing campaigns.

Asia Pacific Transactional Video-On-Demand Market Insights

Asia Pacific is an emerging hub in the Transactional Video-On-Demand (TVOD) market, but it is recognized as one of the most dynamic and rapidly expanding regions. Countries like India, South Korea, and Japan are leading this growth trajectory. A key growth enabler is the rising smartphone and broadband penetration across the region. Like, India saw significant growth in broadband subscribers between 2021 and 2023, facilitating greater access to digital content. Similarly, in South Korea, where internet speeds rank among the highest globally, TVOD platforms have introduced premium movie rentals alongside local dramas, capturing a diverse consumer base. Another important factor is the increasing production and digital distribution of regional content. In China, platforms such as Tencent Video and iQIYI have expanded their transactional models, allowing users to rent or buy Mandarin films and documentaries. With improving digital payment infrastructure and rising disposable incomes, Asia Pacific is expected to become a crucial growth engine for the TVOD market, particularly as platforms tailor pricing and content strategies to local preferences.

Latin America Transactional Video-On-Demand Market Insights

Latin America is another significant player in the Transactional Video-On-Demand (TVOD) market, with Brazil, Mexico, and Argentina emerging as key contributors to regional growth. A significant growth driver is the increasing availability of Spanish and Portuguese-language content tailored for local audiences. Regional studios and distributors have begun leveraging digital platforms to monetize telenovelas, comedies, and independent films outside traditional broadcast channels. Another contributing factor is the expansion of e-commerce and digital payment ecosystems. Mercado Pago, PayPal, and local fintech companies have simplified online transactions, reducing friction in content purchases. Also, improvements in internet infrastructure is supporting smoother streaming experiences. While regulatory hurdles and piracy remain challenges, the gradual shift toward digital consumption positions Latin America as a promising market for TVOD expansion in the coming years.

Middle East and Africa Transactional Video-On-Demand Market Insights

The Middle East and Africa collectively represent an emerging yet nascent market with untapped potential. While overall penetration remains low compared to other regions, countries like the UAE, Saudi Arabia, and South Africa are showing signs of growth, driven by increasing smartphone adoption and digital transformation initiatives. This expansion has facilitated broader access to digital content, particularly in urban centers where mobile-first users are more inclined to engage in micro-transactions. In the UAE, for instance, platforms like OSN and Shahid VIP have started incorporating TVOD elements, allowing users to rent premium content without full subscription commitments. A key growth catalyst is the localization of content. Arabic-language films and regional dramas are gaining traction on digital platforms, with studios exploring transactional models to reach wider audiences. Despite infrastructural limitations and payment gateway complexities, the region’s youthful demographic and increasing investment in digital infrastructure suggest a positive outlook for TVOD adoption in the long term.

KEY MARKET PARTICIPANTS

The major companies operating in the global transactional video-on-demand market include Eros International (India), Iflix (Malaysia), Tencent (China), LeEco (China), Rakuten (Japan), Disney (US), Amazon (US), Apple Inc. (US), Comcast Corp (US), Vivendi (France), Filmdoo (UK), iFlix (UAE), and Tving (South Korea).

TOP LEADING PLAYERS IN THE MARKET

Apple Inc.

One of the leading players in the Transactional Video-On-Demand (TVOD) market is Apple Inc., primarily through its Apple TV+ platform which includes a robust TVOD section. Apple has significantly contributed to the global market by offering high-quality digital rentals and purchases, integrating them seamlessly into its ecosystem of devices. The company’s strong brand loyalty, user-friendly interface, and exclusive film partnerships have enhanced consumer trust and engagement in transactional content. Its ability to bundle digital transactions with device purchases has further reinforced its position in the TVOD space.

Amazon.com, Inc.

Amazon.com, Inc. is another major player, operating through Amazon Prime Video, which offers both subscription-based and transactional content. While Prime Video is largely SVOD, it also provides an extensive TVOD library that allows users to rent or buy movies outside the subscription model. Amazon’s contribution lies in leveraging its vast customer base, cloud infrastructure, and personalized recommendation engine to drive transactional sales. Its integration with Alexa-enabled devices and Fire TV Stick enhances accessibility, making it a key enabler of digital content monetization on a per-title basis.

Google LLC

Google LLC, under its Google Play Movies service (now rebranded as Movies Anywhere in some regions), plays a pivotal role in the TVOD landscape. The platform enables users to purchase or rent films across Android devices and smart TVs, contributing to the expansion of digital storefronts globally. Google’s strength lies in its seamless integration with Android smartphones and YouTube, allowing for cross-promotion and wider reach. Its partnerships with major studios ensure a broad content catalog, while cloud-based storage allows consumers to access purchased content across multiple screens, enhancing convenience and retention.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Transactional Video-On-Demand (TVOD) market employ strategic content partnerships to secure exclusive titles and expand their digital catalogs. By collaborating with major studios and independent filmmakers, platforms enhance their appeal and attract a broader audience seeking premium content on a pay-per-view basis. These alliances not only improve content availability but also help in differentiating offerings in a competitive landscape.

Another critical strategy is the integration of TVOD services with existing digital ecosystems. Companies embed transactional content within their established platforms such as mobile app stores, gaming consoles, and smart TVs to streamline access and encourage spontaneous purchases. This approach leverages existing user bases and device ecosystems, improving conversion rates and reinforcing consumer engagement with transactional models.

Lastly, localization and personalization are widely adopted strategies. Market leaders tailor content libraries based on regional preferences, offer localized payment methods, and use AI-driven recommendation engines to enhance user experience. These tactics increase relevance and engagement, driving higher participation in transactional viewing across diverse markets.

COMPETITION OVERVIEW

The competition in the Transactional Video-On-Demand (TVOD) market is marked by a dynamic mix of traditional entertainment companies, tech giants, and emerging digital platforms striving to capture consumer interest and spending. As the demand for flexible, on-demand content continues to grow, players are intensifying their efforts to differentiate themselves through exclusive content, superior user experiences, and strategic partnerships. Established studios are increasingly shifting toward direct-to-consumer models, bypassing traditional distribution channels to maximize digital revenue. At the same time, streaming behemoths are integrating transactional options into their existing platforms, blurring the lines between subscription and pay-per-view models. The presence of regional players further adds complexity, as they cater to local tastes and leverage cost-effective pricing strategies. Innovation in delivery mechanisms, such as cloud-based purchases and offline rentals, is becoming a key battleground. Besides, advancements in artificial intelligence for content recommendations and personalized marketing are shaping how platforms engage users.

RECENT MARKET DEVELOPMENTS

- In January 2023, Apple Inc. expanded its TVOD content library by securing exclusive digital rental rights for several independent films, strengthening its position in the premium movie segment and attracting a more diverse audience.

- In June 2023, Amazon Studios announced a new partnership with a European film distributor to offer select theatrical releases directly on Amazon Prime Video for digital rental, shortening the window between cinema and home viewing.

- In November 2023, Google LLC integrated its TVOD platform with a leading South Korean content provider, enhancing its regional catalog and supporting growth in the Asia-Pacific market through localized content offerings.

- In March 2024, Disney launched a standalone digital store for electronic sell-through purchases in Latin America, aiming to boost transactional revenue in a region where subscription fatigue is limiting SVOD adoption.

- In August 2024, Warner Bros. Discovery introduced a tiered pricing model for digital rentals, offering short-term and extended viewing periods to cater to varying consumer preferences and enhance flexibility in the TVOD space.

MARKET SEGMENTATION

This research report on the global video-on-demand market has been segmented and sub-segmented based on access, content, availability, and region.

By Access

- OTT Streaming

- Desktops & Laptops

- Smartphones & Tablets

- Smart TVs

- Other Devices

By Content

- Entertainment

- Food

- Travel & Fashion

- Games & Sports

- Kids

- Others

By Availability

- Electronic Sell-Through

- Download to rent

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How is the Transactional Video-On-Demand market affected by the competition from subscription-based streaming services?

While subscription-based services are popular, TVOD caters to a different audience seeking one-time content access. TVOD remains competitive by offering a pay-per-view model, allowing users to rent or purchase specific content without committing to a subscription.

What role do mobile devices play in the Transactional Video-On-Demand market's growth?

The increasing prevalence of smartphones and tablets has significantly contributed to the growth of the TVOD market. Consumers prefer the convenience of accessing on-demand content on their mobile devices, driving the market's expansion.

How does the Transactional Video-On-Demand market address concerns related to digital piracy?

TVOD platforms employ digital rights management (DRM) technologies and encryption methods to protect content from piracy. Additionally, the convenience and affordability of legal TVOD options act as deterrents to piracy.

What technological advancements are influencing the evolution of the Transactional Video-On-Demand market?

Technologies such as artificial intelligence, virtual reality, and improved streaming capabilities are enhancing the user experience on TVOD platforms. Personalized recommendations and interactive features are becoming integral to the evolving landscape.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com