Global Bacterial and Viral Specimen Collection Market Size, Share, Trends & Growth Forecast Report By Type, Application, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2026 to 2034

Global Bacterial and Viral Specimen Collection Market Size

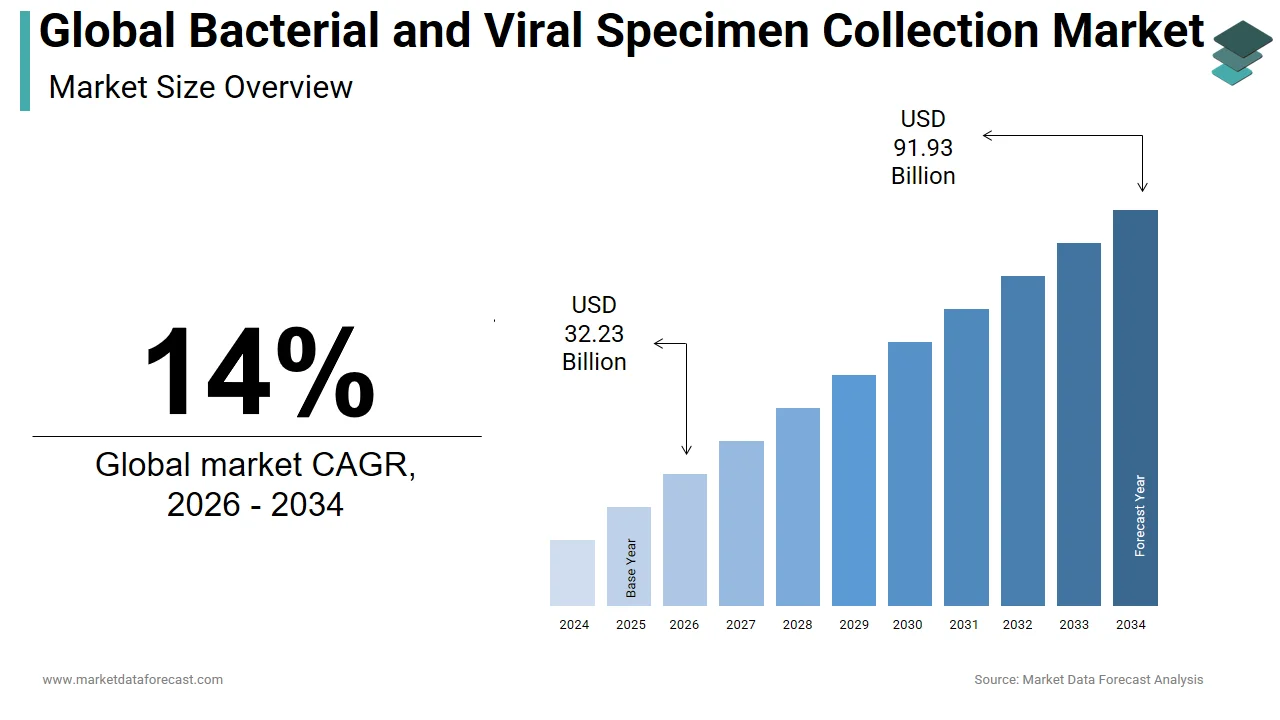

The global bacterial and viral specimen collection market was valued at USD 28.27 billion in 2025, is estimated to reach USD 32.23 billion in 2026, and is projected to reach USD 91.93 billion by 2034, growing at a CAGR of 14% from 2026 to 2034.

The bacterial and viral specimen collection is specialized devices and media designed to safely obtain, preserve, and transport biological samples, such as nasopharyngeal swabs, blood, sputum, urine, and stool for the accurate detection and identification of pathogenic microorganisms. These systems include sterile swabs, viral transport media, bacterial culture transport tubes, and nucleic acid stabilization kits engineered to maintain microbial viability or genetic integrity from the point of collection to laboratory analysis. The clinical and public health utility of these tools has been unequivocally demonstrated during global health emergencies, where timely diagnosis hinges on specimen quality. According to the World Health Organization, over 200 million cases of bacterial pneumonia occur annually worldwide, necessitating reliable sputum and blood collection for culture and sensitivity testing. Similarly, the Global Influenza Surveillance and Response System, coordinated by the same body, processes more than 1 million respiratory specimens each year to monitor viral evolution and inform vaccine composition.

MARKET DRIVERS

Escalating Global Burden of Infectious Diseases

The persistent and rising incidence of bacterial and viral infections worldwide, for standardized specimen collection systems, is escalating the growth of the bacterial and viral specimen collection market. According to the World Health Organization, lower respiratory infections remain the leading cause of death from infectious disease, with 2.5 million fatalities in 2023 alone, predominantly due to bacterial pneumonia and viral influenza. Tuberculosis continues to afflict over 10 million people annually, with accurate diagnosis requiring sputum collection in specialized transport media to preserve Mycobacterium tuberculosis viability for culture and drug susceptibility testing. In sub-Saharan Africa, the World Health Organization estimates that 233 million malaria cases occurred in 2023, necessitating blood collection for rapid diagnostic tests and molecular confirmation. Concurrently, viral threats such as dengue, chikungunya, and respiratory syncytial virus are expanding geographically due to climate change and urbanization. As per some studies, 2.3 million cases of sexually transmitted bacterial infections in 2023 required urethral, cervical, and urine specimens collected in nucleic acid amplification test-compatible media.

Strengthening of Global Pandemic Preparedness Frameworks

The national and international investments in pandemic readiness have institutionalized specimen collection as a core public health function, driving sustained procurement of standardized kits. The strengthening of global pandemic preparedness frameworks is additionally to propel the growth of the bacterial and viral specimen collection market. Following the lessons of the SARS-CoV-2 pandemic, the World Health Organization updated its International Health Regulations in 2023 to require all member states to maintain minimum stockpiles of viral collection supplies for rapid outbreak response. As per the United States Department of Health and Human Services, it allocated 1.8 billion US dollars in 2023 through the Administration for Strategic Preparedness and Response to pre-position viral transport media and swabs in state health departments. Similarly, the European Union’s HERA Incubator program established a strategic reserve of 50 million specimen collection kits for deployment during future health emergencies. In Africa, the Centers for Disease Control and Prevention launched the Pathogen Genomics Initiative in 2022, which has trained over 1,200 laboratory personnel in standardized specimen collection across 30 countries to support real-time sequencing of emerging threats. These structural commitments transform specimen collection from an episodic clinical activity into a permanent pillar of global health security infrastructure, ensuring continuous demand beyond immediate outbreak cycles.

MARKET RESTRAINTS

Inconsistent Regulatory Standards Across Jurisdictions

The absence of globally harmonized regulatory requirements for specimen collection devices creates significant barriers to market entry and clinical reliability. The inconsistent regulatory standards across jurisdictions are impeding the growth of the bacterial and viral specimen collection market. While the United States Food and Drug Administration classifies viral transport media as Class II medical devices requiring 510 k clearance, many low- and middle-income countries lack formal regulatory pathways, leading to widespread use of non-validated or counterfeit products. In Latin America, the Pan American Health Organization, only 12 of 35 member states have national standards for bacterial transport media, resulting in inter-country variability that compromises regional outbreak investigations.

Cold Chain and Logistics Constraints in Resource-Limited Settings

Maintaining specimen integrity during transport remains a critical challenge in regions with underdeveloped healthcare infrastructure, particularly where temperature-sensitive viral samples must reach distant laboratories. According to the World Health Organization, over 60% of health facilities in sub-Saharan Africa lack reliable refrigerated transport, and 45% experience electricity outages exceeding four hours daily. This compromises the stability of RNA viruses like influenza and SARS-CoV-2 CoV 2 which degrade rapidly at ambient temperatures. Although ambient temperature stabilization media exist, they are often cost-prohibitive for public health programs operating on tight budgets. The United Nations Children’s Fund estimates that only 28% of national immunization programs in low-income countries have access to validated ambient stable collection systems.

MARKET OPPORTUNITIES

Integration of Specimen Collection into Point of Care and Decentralized Testing Networks

The expansion of decentralized diagnostics for next-generation specimen collection systems designed for simplicity, stability, and compatibility with portable analyzers is greatly influencing the growth of the bacterial and viral specimen collection market. As per the World Health Organization, people in low-resource settings first seek care at community clinics or pharmacies that lack laboratory infrastructure, necessitating collection devices that enable immediate or near-patient testing. The United States President’s Emergency Plan for AIDS Relief has deployed over 15 million HIV self-collection kits in sub-Saharan Africa since 2020, allowing patients to collect oral fluid or dried blood spots at home for later testing. Similarly, the Foundation for Innovative New Diagnostics is piloting integrated collection and testing cartridges for tuberculosis that eliminate separate transport steps. In high-income countries, urgent care centers and retail clinics now perform over 40 million rapid strep and flu tests annually, as per the American Medical Association, requiring pre-packaged swab and reagent systems. This shift toward decentralized care demands collection formats that are user-friendly, ambient stable, and directly interfaced with analytical platforms, creating a fertile ground for innovation in integrated diagnostic ecosystems.

Rise of Multi-Pathogen Syndromic Testing Panels

The clinical adoption of syndromic testing, which simultaneously screens for dozens of bacterial and viral agents from a single specimen, is driving demand for universal collection media compatible with broad molecular platforms. According to the Centers for Disease Control and Prevention, hospital laboratories in the United States now use multiplex PCR panels for respiratory, gastrointestinal, and central nervous system infections. These assays require collection devices that preserve both DNA and RNA without inhibition across diverse pathogen types. BioFire’s FilmArray system, for example, tests for 22 respiratory pathogens from one nasopharyngeal swab, necessitating transport media validated for all targets. As insurance providers increasingly reimburse, these comprehensive panel manufacturers are developing next-generation universal transport media that support extended room temperature stability and compatibility with automated extraction systems.

MARKET CHALLENGES

Shortage of Trained Personnel for Proper Specimen Collection

The global deficit of healthcare workers skilled in aseptic and anatomically precise specimen collection directly compromises diagnostic yield and contributes to false negative results. The shortage of trained personnel for proper specimen collection is attributed to hampering the growth of the bacterial and viral specimen collection market. According to the World Health Organization, the world faces a shortage of 10 million health workers, with the most acute gaps in sub-Saharan Africa and South Asia, where nurse-to-patient ratios often exceed 1 to 1,000. Similarly, inadequate sputum induction or contamination during urine collection leads to culture misidentification and inappropriate antibiotic use. In low-resource settings, community health workers with minimal training often perform collections without supervision or quality assurance. The United States Centers for Disease Control and Prevention estimates that pre-analytical errors related to collection technique account for all microbiology testing inaccuracies.

Environmental and Disposal Concerns Related to Single-Use Plastics

The massive scale of single-use specimen collection is driven by infection control protocols that have intensified scrutiny over plastic waste and environmental sustainability. A single large hospital in the United States can generate over 200,000 swabs and transport tubes monthly, as per the Healthcare Environmental Resource Center. Globally, the World Health Organization estimates that the COVID-19 pandemic produced over 140,000 tons of plastic medical waste, including specimen collection kits, most of which ended up in landfills or incinerators. Many collection devices contain mixed materials such as plastic shafts, foam tips, and liquid media that are not recyclable under standard municipal systems. The European Environment Agency has flagged medical plastics as a priority waste stream under the Circular Economy Action Plan, prompting manufacturers to explore biodegradable swab materials and dry collection systems that eliminate liquid media. However, regulatory concerns about performance equivalence and higher costs have slowed adoption. Balancing infection safety with environmental responsibility remains a complex challenge requiring innovation in materials science, regulatory flexibility, and waste management infrastructure to ensure sustainable growth in specimen collection practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Puritan Medical Products, COPAN Diagnostics, Becton, Dickinson and Company, Thermo Fisher Scientific, Inc., Quidel Corporation, Longhorn Vaccines and Diagnostics, LLC, Pretium Packaging, Trinity Biotech, Medical Wire & Equipment, HiMedia Laboratories, Hardy Diagnostics, Nest Scientific, VIRCELL S.L., DiaSorin, Titan Biotech. |

SEGMENTAL ANALYSIS

By Type Insights

The viral specimen collection segment accounted in holding 46.5% of the bacterial and viral specimen collection market share in 2024. The infrastructure built for mass testing spans nasopharyngeal swabs, viral transport media, and RNA stabilization tubes that remain operational for monitoring influenza, respiratory syncytial virus, and emerging pathogens. National public health agencies continue to prioritize viral diagnostics as part of pandemic preparedness frameworks. The United States Centers for Disease Control and Prevention maintains year-round surveillance for over 20 viral agents through its National Respiratory and Enteric Virus Surveillance System. Additionally, the European Centre for Disease Prevention and Control mandates standardized viral collection protocols across all member states to enable cross-border outbreak response.

The bacterial specimen collection segment is expected to grow at the fastest CAGR of 13.2% during the forecast period, driven by the escalating threat of antimicrobial resistance and the urgent need for culture-based and molecular identification of pathogenic bacteria. According to the World Health Organization, antimicrobial resistance causes over 1.27 million deaths annually and is projected to surpass 10 million by 2050 without intervention. This crisis has intensified demand for sterile transport systems that maintain bacterial viability for accurate susceptibility testing. The United States National Action Plan for Combating Antibiotic-Resistant Bacteria mandates that all hospitals implement antimicrobial stewardship programs requiring timely and reliable specimen collection. Furthermore, the rise of hospital-acquired infections, such as those caused by methicillin-resistant Staphylococcus aureus and carbapenem-resistant Enterobacteriaceae, has compelled healthcare facilities to upgrade collection kits with selective media and anaerobic transport capabilities. These clinical and regulatory imperatives are accelerating innovation and adoption in bacterial specimen collection far beyond historical norms.

By Application Insights

The diagnostics segment held a significant share of the bacterial and viral specimen collection market in 2024. Every infectious disease diagnosis, from urinary tract infections to viral hepatitis, begins with proper specimen acquisition using validated collection devices. According to the College of American Pathologists pre pre-analytical errors, including improper collection, account for nearly 70% of laboratory inaccuracies, highlighting the critical role of standardized kits. In the United States, clinical microbiology tests are performed annually, as per the Centers for Medicare and Medicaid Services, with each requiring a dedicated collection system. The expansion of point-of-care testing in urgent care centers and pharmacies has further increased demand for ready-to-use viral swabs and bacterial transport tubes. Additionally, regulatory frameworks such as the Clinical Laboratory Improvement Amendments enforce strict requirements for specimen integrity, driving adoption of FDA-cleared collection devices. This diagnostic imperative ensures that clinical testing remains the primary engine of market demand.

The research application segment is anticipated to witness the fastest CAGR of 10.7% from 2026 to 2034, with the global investments in pathogen discovery, vaccine development, and microbiome studies. Academic and pharmaceutical researchers require specialized collection systems that preserve microbial DNA, RNA, and viability for next-generation sequencing and functional assays. According to the National Institutes of Health, over 3.1 billion US dollars were allocated to infectious disease research in 2023, including major initiatives like the Human Microbiome Project 2.0, which collects thousands of bacterial specimens monthly. The Coalition for Epidemic Preparedness Innovations has funded over 20 viral pathogen characterization studies since 2022, each requiring standardized global specimen collection protocols. Additionally, the rise of metagenomic sequencing has increased demand for nucleic acid stabilization tubes that prevent degradation during long-distance shipping from remote field sites.

By End User Insights

The diagnostic laboratories segment was the largest by holding 35.4% of the bacterial and viral specimen collection market share in 2024 due to their centralized role in processing high volumes of infectious disease specimens from hospitals, clinics, and public health programs. Reference labs such as Quest Diagnostics and Labcorp in the United States alone process over 500 million microbiology tests annually, requiring millions of standardized collection kits. According to the World Health Organization, accredited clinical laboratories in high-income countries perform an average of 250 diagnostic tests per capita per year, many involving bacterial or viral specimens. The consolidation of laboratory networks has further concentrated demand as regional hubs standardize on single vendor collection systems to ensure consistency and reduce inventory complexity. In Europe, the European Union’s In Vitro Diagnostic Regulation mandates stringent performance validation for specimen collection devices used in diagnostics, reinforcing reliance on certified suppliers.

The academic and research institutions segment is gaining huge traction with an expected CAGR of 11.2% from 2026 to 2034 by expanding global research funding, pathogen surveillance networks, and interdisciplinary microbiome studies. Universities and public health research centers increasingly conduct longitudinal cohort studies requiring repeated specimen collection from human and environmental sources. As per the Africa Centres for Disease Control and Prevention, a few regional biosafety level three laboratories since 2021 each equipped with standardized viral and bacterial collection protocols for emerging pathogen research.

REGIONAL ANALYSIS

North America Bacterial and Viral Specimen Collection Market Analysis

North America was the top performer of the global bacterial and viral specimen collection market by capturing 25.4% of the share in 2024, with its advanced healthcare infrastructure, robust public health surveillance, and high diagnostic testing volumes. The United States was the major contributor with a dense network of hospital laboratories, commercial reference labs, and urgent care centers. According to the Centers for Disease Control and Prevention, the National Notifiable Diseases Surveillance System collects bacterial and viral specimens annually from state health departments. Canada complements this ecosystem through the National Microbiology Laboratory, which coordinates standardized collection protocols across provinces. Stringent regulatory oversight by the Food and Drug Administration and high reimbursement rates for molecular diagnostics further sustain demand for premium collection devices, ensuring North America’s market growth.

Europe Bacterial and Viral Specimen Collection Market Analysis

The Europe bacterial and viral specimen collection market was ranked second by holding 23.2% of the share in 2024 due to harmonized public health policies, centralized laboratory networks, and proactive antimicrobial resistance monitoring. As per the European Centre for Disease Prevention and Control, coordinates specimen collection for over 50 communicable diseases across 31 countries using standardized kits compliant with the EU In Vitro Diagnostic Regulation. Additionally, the European Union’s 100 Million Genomes Initiative includes pathogen sequencing components that require high-integrity viral and bacterial samples. National programs like the United Kingdom’s Targeted Antimicrobial Stewardship Initiative further drive the adoption of advanced transport media. This integrated regulatory and surveillance framework ensures consistent and high-quality specimen collection across the region.

Asia Pacific Bacterial and Viral Specimen Collection Market Analysis

Asia Pacific bacterial and viral specimen collection market growth is driven by large populations, expanding healthcare access, and intensified pandemic preparedness efforts. China’s National Health Commission established over 5,000 fever clinics post-pandemic, each equipped with viral specimen collection stations processing millions of tests monthly. According to the World Health Organization, South East Asia is seeing a surge in global tuberculosis cases necessitating massive bacterial sputum collection programs. India’s National Centre for Disease Control operates a network of 20 viral research and diagnostic laboratories that collected many specimens in 2023 for influenza and dengue surveillance. Japan and South Korea lead in advanced diagnostics with universal insurance coverage for molecular testing, driving demand for premium collection kits.

Latin America Bacterial and Viral Specimen Collection Market Analysis

Latin America bacterial and viral specimen collection market growth is likely to grow with the increasing infectious disease burden and gradual strengthening of laboratory systems. Brazil’s Oswaldo Cruz Foundation operates the largest public health laboratory network in the region, processing over 20 million bacterial and viral specimens annually for diseases like dengue, Zika, and tuberculosis.

Middle East and Africa Bacterial and Viral Specimen Collection Market Analysis

The Middle East and Africa bacterial and viral specimen collection market growth is likely to grow with the concentration in national reference laboratories and disease hotspot zones. Saudi Arabia’s Ministry of Health established 300 designated specimen collection centers during the Hajj season to monitor for Middle East Respiratory Syndrome and other viral threats. The African Union’s Partnership for African Vaccine Manufacturing includes specimen collection as a critical upstream component.

COMPETITIVE LANDSCAPE

The bacterial and viral specimen collection market features intense competition among established diagnostics giants, specialized specimen collection innovators, and regional manufacturers. Global leaders such as Becton Dickinson and Thermo Fisher Scientific leverage their scale, regulatory expertise, and integrated diagnostic ecosystems to dominate hospital and reference laboratory channels. Niche players like Copan Diagnostics differentiate through proprietary swab and media technologies that offer superior analytical performance, particularly for molecular testing. The market is further fragmented by numerous local suppliers in emerging economies offering low-cost alternatives, though often lacking validation and quality control. Competition is increasingly shaped by the shift toward syndromic testing and decentralized diagnostics, which demand universal collection systems compatible with multiplex platforms. Regulatory harmonization efforts and environmental sustainability requirements are raising barriers to entry while creating opportunities for companies that combine performance reliability with eco-conscious design. Intellectual property around swab architecture and media formulation remains a key battleground as firms race to establish technical standards in a post-pandemic world.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global bacterial and viral specimen collection market include

- Puritan Medical Products

- COPAN Diagnostics

- Becton Dickinson and Company

- Thermo Fisher Scientific, Inc.

- Quidel Corporation

- Longhorn Vaccines and Diagnostics, LLC

- Pretium Packaging

- Trinity Biotech

- Medical Wire & Equipment

- HiMedia Laboratories

- Hardy Diagnostics

- Nest Scientific

- VIRCELL S.L.

- DiaSorin

- Titan Biotech

TOP PLAYERS IN THE MARKET

- Becton Dickinson and Company is a global leader in bacterial and viral specimen collection through its extensive portfolio of sterile swabs, transport media, and integrated collection systems. The company supplies standardized kits for respiratory, gastrointestinal, and sexually transmitted infection testing to hospitals, laboratories, and public health agencies worldwide. BD has strengthened its position by launching the BD Universal Viral Transport System, which maintains the stability of a broad range of viruses, including influenza, SARS-CoV-2, and respiratory syncytial virus, at ambient temperatures for up to 30 days. The company also collaborates with the World Health Organization and national health ministries to support pandemic preparedness stockpiling and training programs, ensuring its solutions remain central to global diagnostic infrastructure.

- Thermo Fisher Scientific Inc. plays a pivotal role in the bacterial and viral specimen collection market by providing advanced transport media, sample stabilization technologies, and molecular collection kits compatible with next-generation sequencing and PCR platforms. Its Applied Biosystems and Norgen Biotek brands offer RNA and DNA stabilization tubes that preserve nucleic acid integrity without cold chain requirements. Thermo Fisher has recently expanded its impact by integrating specimen collection solutions with its KingFisher automated extraction systems, enabling end-to-end workflows for high-throughput diagnostic laboratories. The company also partners with global research consortia to validate collection protocols for emerging pathogens, reinforcing its position as a critical enabler of both clinical diagnostics and infectious disease research.

- Copan Diagnostics Inc. is renowned for its innovative flocked swab technology and universal transport media designed to maximize pathogen recovery and compatibility with molecular assays. The company’s ESwab system has become a global standard for bacterial culture and PCR testing due to its ability to release over 90% of collected specimens compared to traditional fiber swabs. Copan has reinforced its leadership by developing the UTM 3mL and 5mL viral transport media formulations validated for over 100 viral targets, including SARS-CoV-2, influenza, and enteroviruses. Recent initiatives include expanding manufacturing capacity in the United States and Europe and collaborating with public health agencies to deploy collection kits for antimicrobial resistance surveillance and syndromic testing programs worldwide.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the bacterial and viral specimen collection market employ several strategic approaches to maintain a competitive advantage. They prioritize product innovation by developing ambient temperature stable transport media and flocked swabs that enhance pathogen recovery and compatibility with molecular diagnostics. Strategic partnerships with public health agencies, academic institutions, and diagnostic platform manufacturers ensure integration into standardized testing workflows and pandemic response frameworks. Companies also invest in regulatory compliance by securing United States Food and Drug Administration clearance and European Conformity certification for new collection systems. Geographic expansion is achieved through localized manufacturing and distribution networks, particularly in high-growth regions like Asia and Africa. Additionally, firms focus on sustainability by exploring biodegradable materials and dry collection technologies to address environmental concerns associated with single-use plastics.

MARKET SEGMENTATION

This research report on the global bacterial and viral specimen collection Market has been segmented and sub-segmented based on Type, Material, Application, and Region.

By Type

- Bacterial Specimen Collection

- Viral Specimen Collection

By Application

- Diagnostics

- Research

By End-User

- Hospitals

- Diagnostic Laboratories

- Academic and Research Institution

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What drives growth in the global bacterial and viral specimen collection market?

Growth is driven by rising infectious diseases, awareness of specimen collection methods, advanced healthcare infrastructure, and demand for accurate diagnostics in the global bacterial and viral specimen collection market.

2. Who are the key companies in the global bacterial and viral specimen collection market?

Key players include Thermo Fisher Scientific, Becton Dickinson, and Copan Diagnostics, focusing on innovative collection kits for the global bacterial and viral specimen collection market.

3. What products dominate the global bacterial and viral specimen collection market?

The dominant products are bacterial specimen collection kits, viral swabs, specimen transport containers, and molecular diagnostic collection tools in the global bacterial and viral specimen collection market.

4. Which regions lead the global bacterial and viral specimen collection market?

North America leads with over 25.4% revenue share, followed by fast-growing Asia Pacific, reflecting high healthcare investments in the global bacterial and viral specimen collection market.

5. How does infectious disease prevalence affect the global bacterial and viral specimen collection market?

Increasing infectious diseases worldwide significantly propel the global bacterial and viral specimen collection market by increasing demand for reliable diagnostic specimens.

6. What role does technology innovation play in the global bacterial and viral specimen collection market?

Innovation in specimen collection devices, transport media, and molecular testing enhances accuracy and speeds diagnosis, boosting the global bacterial and viral specimen collection market

7. How is the hospital segment influencing the global bacterial and viral specimen collection market?

Hospitals and clinics contribute the largest end-user segment revenue due to heightened specimen collection needs, driving growth in the global bacterial and viral specimen collection market.

8. What challenges exist for the global bacterial and viral specimen collection market?

Challenges include high costs, supply chain disruptions, contamination risks, and infrastructure limitations, affecting the global bacterial and viral specimen collection market.

9. How is Asia Pacific contributing to the global bacterial and viral specimen collection market?

Asia Pacific is the fastest-growing region in the global bacterial and viral specimen collection market due to expanding telemedicine and healthcare infrastructure investments.

10. What are the applications driving the global bacterial and viral specimen collection market?

Diagnostic testing dominates applications in the global bacterial and viral specimen collection market, essential for early infectious disease detection.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com