- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

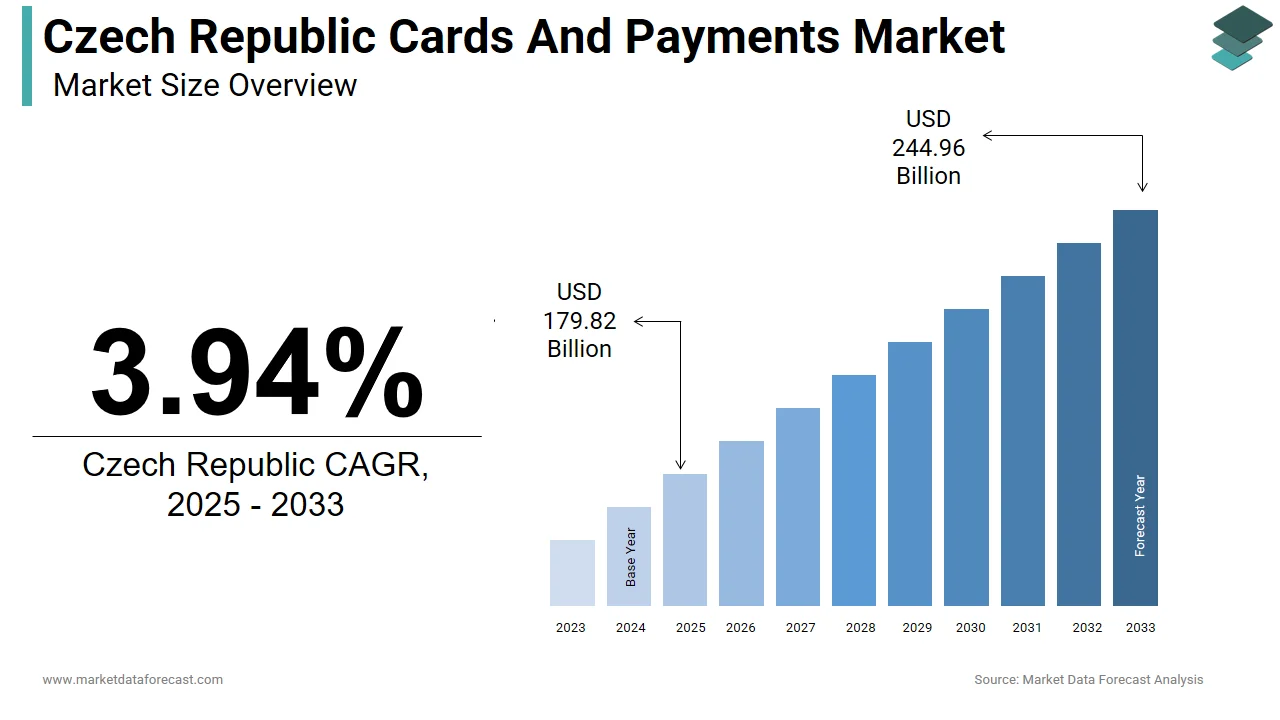

Czech Republic Cards and Payments Market Size

The Czech Republic cards and payments market was valued at USD 173 billion in 2024, is estimated to reach USD 179.82 billion in 2025, and is projected to reach USD 244.96 billion by 2033, growing at a CAGR of 3.94% from 2025 to 2033.

Czech Republic Cards And Payments Market report offers a distinct range of possibilities in the market of payment cards, along with the accurately validated statistics of operational cards in the market and their total transactional values. It suggests profitable marketing strategies considering the competitive landscape in the market, purchase trends, payment options in online trade, and significant government frameworks impacting the overall payment card market of the Czech Republic.

MARKET DRIVERS

Rapid Growth in Digital Payment Adoption Driven by E-Commerce Expansion

One of the primary drivers of the Czech Republic's cards and payments market is the surge in digital payment adoption, largely fueled by the expansion of e-commerce. According to Statista, Czech online retail sales reached approximately CZK 254 billion (around €9.7 billion) in 2023, representing a year-on-year growth of 8.6%. This increasing shift toward online shopping has significantly raised demand for secure and convenient card-based transactions. Additionally, data from the Czech National Bank reveals that in 2023, over 86% of the population aged 15–74 had used a debit or credit card for online purchases at least once, up from 72% in 2019. The rise in contactless card usage further supports this trend, with contactless payments accounting for more than 60% of all point-of-sale transactions under CZK 1,500, as reported by Mastercard Central & Eastern Europe in Q4 2023. With government support for digital infrastructure and financial literacy programs, consumers are increasingly moving away from cash, reinforcing the long-term growth trajectory of the cards and payments sector.

Increasing Penetration of Contactless and Mobile Payments

Another significant driver of the Czech Republic’s cards and payments market is the rising adoption of contactless and mobile payment technologies. As per a 2023 report by McKinsey on European payment trends, the Czech Republic saw a 22% increase in contactless transaction volumes compared to the previous year. Furthermore, nearly 40% of smartphone users in the country have adopted mobile wallet solutions such as Apple Pay, Google Pay, or Samsung Pay, according to data released by the Czech Statistical Office in late 2023. Banks and fintech companies are aggressively rolling out NFC-enabled cards and integrating mobile wallets into their services to meet growing consumer demand for convenience and speed. Komerční Banka reported that in 2023, one-third of all card transactions were conducted via mobile devices. This technological shift not only enhances user experience but also aligns with broader global trends toward seamless digital payments, positioning the Czech Republic as a progressive market within Central and Eastern Europe.

MARKET RESTRAINTS

Persistent Preference for Cash Transactions Among Older Demographics

Despite the overall growth in digital payments, a major restraint on the Czech Republic's cards and payments market is the persistent preference for cash among older demographics. According to the Czech National Bank’s 2023 financial behavior survey, nearly 45% of individuals over the age of 65 still prefer using cash for daily transactions, citing concerns about security, lack of trust in digital systems, and limited familiarity with new technologies. This behavioral inertia slows down the transition to a fully digitized payment ecosystem. Additionally, Eurostat data from 2023 indicates that cash remains the most frequently used payment method in over 40% of retail transactions across the country, particularly in smaller towns and rural areas where digital infrastructure lags behind urban centers. While younger generations are rapidly embracing card and mobile payments, the slower adaptation rate among seniors creates a fragmented payment landscape. Financial institutions must invest in targeted education and awareness campaigns to bridge this generational gap, which currently limits the full potential of digital payment growth in the Czech Republic.

Regulatory Complexity and Compliance Costs for New Payment Technologies

The regulatory environment in the Czech Republic, while generally supportive of financial innovation, poses challenges due to its complexity and compliance costs for emerging payment technologies. The implementation of the EU’s revised Payment Services Directive (PSD2) and other local regulations has increased the operational burden on fintech startups and digital banks entering the market. According to a 2023 report by Deloitte, compliance costs can account for up to 20% of total operating expenses for small-scale payment service providers in the Czech Republic. Moreover, the Czech National Bank maintains strict licensing requirements for electronic money institutions and payment service providers, leading to longer time-to-market for innovative products. A study by the European Banking Authority (EBA) in Q3 2023 found that the Czech Republic ranked among the top five EU countries with the highest regulatory barriers to entry for fintech firms. These constraints deter smaller players from entering the market, limiting competition and slowing the pace of technological advancement in the cards and payments sector.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services in the Retail Sector

A significant opportunity in the Czech Republic’s cards and payments market lies in the rapid growth of Buy Now, Pay Later (BNPL) services, especially among younger consumers and online retailers. According to a 2023 report by NielsenIQ, approximately 22% of Czech consumers had used BNPL services at least once, with millennials and Gen Z showing the highest adoption rates. The BNPL model is gaining traction due to its flexibility, low upfront cost, and appeal to budget-conscious shoppers. Local banks and international fintech firms such as Klarna and Twisto have been expanding their presence in the Czech market, partnering with major e-commerce platforms like Mall.cz and Zootopia. Data from the Czech Statistical Office shows that BNPL transactions accounted for nearly 7% of total online payment volume in 2023, up from 2% in 2021.

Integration of Open Banking and API-Based Financial Services

The introduction and gradual integration of open banking in the Czech Republic present a transformative opportunity for the cards and payments industry. Facilitated by the EU’s PSD2 regulation, open banking allows third-party providers to access financial data securely through APIs, enabling personalized financial products and streamlined payment experiences. According to a 2023 analysis by PwC, nearly 60% of Czech banks have initiated open banking implementations, with several launching API marketplaces to foster collaboration with fintech firms. The Czech Banking Association reported that in 2023, the number of registered third-party providers increased by 34% compared to the previous year. Consumers are beginning to benefit from enhanced services such as real-time account aggregation, instant loan approvals, and integrated budgeting tools. As awareness and trust in these services grow, open banking could catalyze a wave of innovation, allowing new entrants to disrupt traditional payment models and offer competitive, customer-centric solutions in the Czech Republic.

MARKET CHALLENGES

Cybersecurity Threats and Fraud Risks in Digital Payment Channels

A pressing challenge facing the Czech Republic’s cards and payments market is the growing threat of cyberattacks and fraud in digital payment channels. As the use of online and mobile payments increases, so does the exposure to sophisticated financial fraud schemes. According to the Czech National Security Authority (NÚKIB), there was a 28% rise in reported cyber incidents targeting financial institutions in 2023 compared to the previous year. Phishing attacks, card-not-present (CNP) fraud, and malware-based payment interception remain prevalent. The Czech Police’s 2023 annual report noted that CNP fraud alone accounted for nearly 65% of all payment-related crimes, with losses exceeding CZK 1.2 billion. To combat these threats, banks and payment service providers must continuously invest in advanced fraud detection systems, biometric authentication, and encryption technologies. However, the high cost of implementing robust cybersecurity measures poses a particular burden on smaller financial institutions and fintech startups, potentially slowing down their ability to scale and innovate in the fast-evolving digital payments space.

Fragmented Merchant Acceptance Infrastructure Across Small Businesses

Another key challenge in the Czech Republic’s cards and payments market is the uneven merchant acceptance infrastructure, particularly among small and micro businesses. Despite widespread card ownership and usage, many small retailers in rural and semi-urban areas still do not accept card payments due to high equipment costs and lack of technical know-how. Additionally, the Czech Statistical Office reported that in 2023, nearly 30% of all retail establishments accepted cash exclusively. This fragmentation limits the overall growth of non-cash transactions and hampers efforts to build a fully inclusive digital economy. While initiatives such as subsidized POS terminal programs and digitalization grants have been introduced by the Ministry of Industry and Trade, adoption remains slow.

MARKET KEY HIGHLIGHTS

The plan of the Czech National Bank (the country’s central bank) to introduce a nationwide instant fund transfer system by the end of 2018 allowing customers to transfer up to CZK400,000 ($18,792.09) instantly during any point of time in the year, and around one-third of banks in the country accepted this proposal.

The advent of several alternative payments like Google's Android Pay, compatible with Visa and MasterCard payment cards offered by J&T Banka, mBank, KomerAní Banka, and MONETA Money Bank, the NaNakupy mobile wallet by Aeskoslovenská obchodní Banka (AESOB) in partnership with electronic payments provider SIA, allowing NFC payments, and MasterCard’s Masterpass QR code feature in collaboration with the Shell Czech Republic to be used at Shell fuel stations.

The earlier stages of the growth of digital-only banks in the nation promote electronic payments. For example, Hello bank, the mobile-only bank launched by Cetelem (a BNP Paribas Personal Finance brand), provides a MasterCard debit card offering all the banking services.

KEY MARKET PLAYERS

Top players in the Czech Republic cards and payments market include

- Ceska spořitelna

- Erste Bank

- CSOB

- KBC Bank

- Komerční banka

- Societe Generale Group

- MONETA Money Bank

- Raiffeisen Bank

MARKET SEGMENTATION

This research report on the Czech Republic cards and payments market is segmented and sub-segmented into the following categories.

By Instruments

- Cards

- Credit Transfers

- Direct Credits

- Cash

By Payment

- Card-based payments

- E-commerce payments

- Alternative Payments