Denmark Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), By Payment Terminals (POS And ATM's), By Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards) - Transaction Value, Volumes, Historical Trends, Industry Analysis From 2025 to 2033

Denmark Cards and Payments Market Size

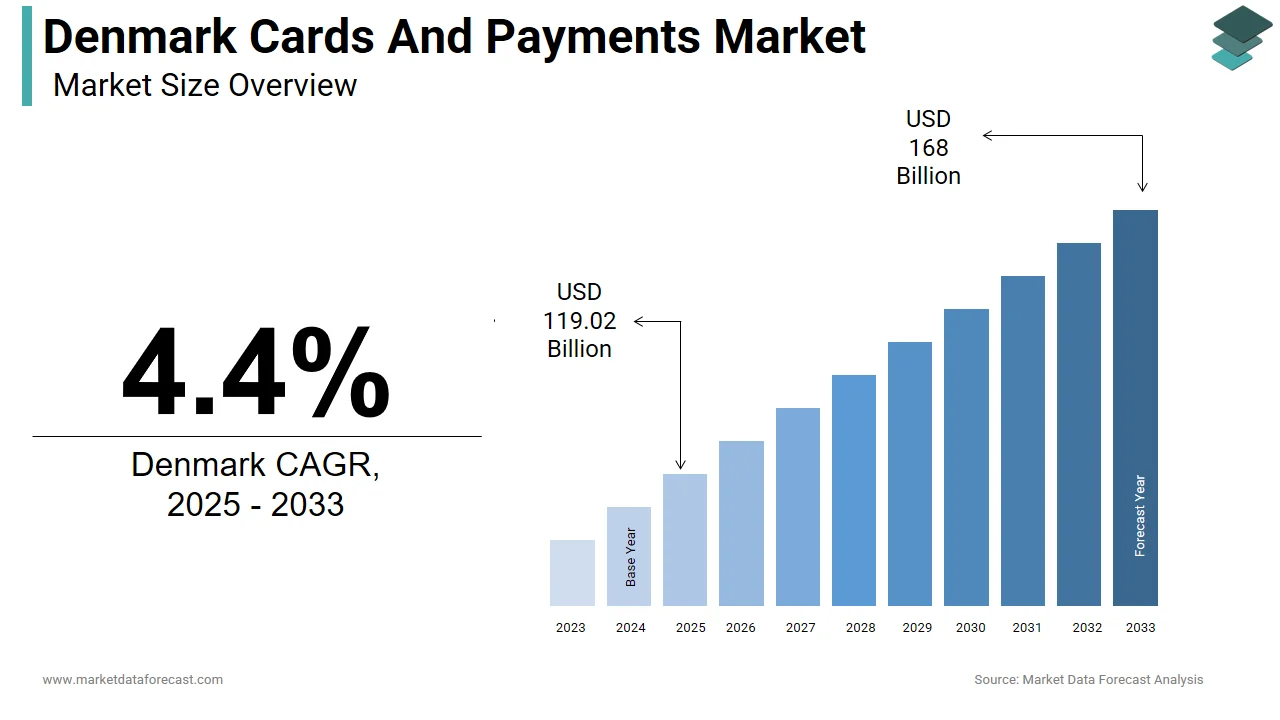

The Denmark cards and payments market size was valued at USD 114 billion in 2024. This market is expected to grow at a CAGR of 4.4% from 2025 to 2033 and be worth USD 168 billion by 2033 from USD 119.02 billion in 2025.

MARKET DRIVERS

High Digital Adoption and Shift toward Cashless Transactions

Denmark continues to be a global leader in digital payments, driven by a strong cultural shift toward cashless transactions and high consumer trust in electronic payment systems. According to Statistics Denmark (Danish Agency for Labour Market and Recruitment), as of 2023, only 6% of Danes used cash for daily purchases, down from over 40% in 2010. This transition is supported by widespread digital infrastructure, with nearly 98% of the population having access to internet banking and 95% owning smartphones, based on data from the Danish Business Authority. Furthermore, contactless card usage has expanded significantly by accounting for 78% of all in-person card transactions under DKK 1,000, according to Mastercard’s Nordic Payment Report. These trends reflect a broader societal move toward convenience and efficiency, reinforcing the growth trajectory of the cards and payments market in Denmark.

Strong Regulatory Support for Fintech Innovation and Open Banking

Another key driver of Denmark's cards and payments market is the supportive regulatory environment that encourages fintech innovation and open banking. As an early adopter of the EU’s revised Payment Services Directive (PSD2), Denmark has facilitated seamless integration between traditional banks and third-party providers, enhancing competition and service diversity. The Danish Financial Supervisory Authority (FSA) reported that by the end of 2023, over 20 licensed fintech firms were actively offering payment initiation or account information services. Additionally, Danske Bank and Jyske Bank have launched open API platforms to support financial startups in developing new digital products. A 2023 report by Deloitte Denmark found that open banking contributed to a 15% increase in digital banking engagement among consumers under 40.

MARKET RESTRAINTS

Decline in Physical Cash Infrastructure and Inclusivity Gaps

A significant restraint on Denmark’s cards and payments market is the rapid decline in physical cash infrastructure, which has led to growing inclusivity gaps among certain demographic groups. According to the Danish Bankers Association, the number of ATMs in Denmark fell by 18% between 2020 and 2023, with rural areas being disproportionately affected. Moreover, only 25% of small businesses in remote regions like Bornholm and Western Jutland consistently accepted card payments, per the Confederation of Danish Industry (DI). While Denmark moves closer to becoming a fully cashless society, this divide highlights the need for inclusive policies that ensure equitable access to financial services across all segments of the population.

Rising Cybersecurity Threats Targeting Digital Payment Platforms

As digital payment adoption accelerates in Denmark, the sector faces increasing cybersecurity threats that pose risks to both consumers and financial institutions. According to the Danish Cyber Defence Centre (part of the Danish Defence), cyber incidents targeting financial organizations rose by 24% in 2023 compared to the previous year, with phishing, ransomware, and payment fraud being the most common attack vectors. Although major banks like Nordea and Saxo Bank have invested heavily in AI-based fraud detection systems, many smaller fintech players struggle to match these capabilities. A 2023 consumer study by YouGov revealed that 36% of Danes expressed concerns about the safety of their financial data during online transactions. Addressing these vulnerabilities will require continuous investment in secure infrastructure and public education to maintain trust in the digital payment ecosystem.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services in E-Commerce

A growing opportunity in Denmark’s cards and payments market is the expansion of Buy Now, Pay Later (BNPL) services, particularly within the e-commerce sector. Data from the Danish Financial Supervisory Authority indicates that BNPL transaction value reached DKK 18 billion (€2.4 billion) in 2023, reflecting a 22% annual increase. These services appeal to younger consumers seeking flexible payment options without long-term debt commitments. As regulatory frameworks evolve to accommodate BNPL while ensuring consumer protection, this segment is poised to become a mainstream alternative to traditional credit cards, which offer substantial revenue opportunities for payment providers and boost overall digital transaction volumes.

Integration of Embedded Finance across Non-Financial Platforms

The rise of embedded finance presents a transformative opportunity for Denmark’s cards and payments market, which is allowing non-financial platforms from ride-hailing apps to real estate portals to integrate payment and financial services directly into their ecosystems. For example, MobilePay has integrated its payment gateway into food delivery and transport apps like Wolt and Movia, while Lunar Way enables SMEs to embed invoicing and expense management tools directly into business software. The Confederation of Danish Industry (DI) reported that in 2023, over 50% of mid-sized Danish companies adopted at least one form of embedded financial service to streamline operations and enhance customer experience.

MARKET CHALLENGES

Increasing Sophistication of Financial Fraud and Identity Theft

Despite Denmark’s advanced digital payment infrastructure, the sector faces a growing challenge from increasingly sophisticated financial fraud and identity theft schemes. Phishing attacks, fake merchant sites, and synthetic identity fraud have become more prevalent, exploiting weaknesses in multi-factor authentication and consumer awareness. Although major banks like Danske Bank and Jyske Bank have implemented advanced fraud detection systems, many consumers, especially seniors, are still vulnerable to social engineering tactics. Tackling this growing threat requires coordinated efforts between regulators, financial institutions, and technology providers to strengthen verification protocols, enhance consumer education, and invest in next-generation fraud prevention technologies.

Regulatory Complexity and Compliance Burden for Fintech Startups

While Denmark maintains a progressive regulatory framework for digital finance, emerging fintech startups face challenges related to regulatory complexity and compliance costs. The implementation of PSD2, along with stringent anti-money laundering (AML) and know-your-customer (KYC) requirements, has increased operational burdens for new entrants. While regulation ensures financial stability and consumer protection, streamlining oversight and improving dialogue between regulators and innovators could help accelerate the development of next-generation payment solutions in Denmark.

MARKET KEY HIGHLIGHTS

The launch of the digital wallet by Bokis (a group of 62 Danish banks), including local banks, savings banks, and co-operative banks in Denmark, along with four national banks: Sydbank, Spar Nord Bank, Arbejdernes Landsbank, and Nykredit, supports Visa and MasterCard international credit and debit card payments. Android and iPhone compatible NFC mobile wallet that uses Nets’ host card emulation technology and tokenization to ensure secure contactless mobile transactions. Apple also launched Apple Pay, which is supported by Jyske Bank (Visa debit cards only) and Nordea.

The gaining significance of Contactless payments led banks like Danske Bank and Jyske Bank to offer contactless Dankort cards. Nets agreed with JCB to allow merchants to accept Dankort debit card payments via smartphones using J/Speedy, JCB's contactless technology. J/Speedy can be used to make contactless payments of up to DKK200 ($28.30), with a security code required for transactions beyond that.

The mandate provision of the Payment Accounts Act, based on EU Directive 2014/92/EU (PAD) enabled all Danish consumers to have access to payments using payment cards, including online payments.

KEY MARKET PLAYERS

Top players in the Denmark cards and payments market include Danske Bank, Nordea, Jyske Bank, Sydbank, Arbejdernes Landsbank, Nykredit, SEB, Alm. Brand Bank, BankNordik, Basisbank, The Jutland Sparekasse, Djurslands Bank, Spar Nord Bank, and Vestjysk Bank.

MARKET SEGMENTATION

This research report on the Denmark cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Denmark cards and payments market?

The Denmark cards and payments market is valued at around USD 119.02 billion in 2025, growing via digital shifts and e-commerce, with cards dominating transactions.

2. What drives growth in the Denmark cards and payments market?

Smartphone penetration and MobilePay usage propel the Denmark cards and payments market, alongside e-commerce and contactless preferences.

3. What are key trends in the Denmark cards and payments market?

Contactless and mobile wallets lead trends in the Denmark cards and payments market, reducing cash to under 5% of payments.

4. How dominant are debit cards in the Denmark cards and payments market?

Debit cards hold over 70% share in the Denmark cards and payments market, favored for daily use and bank-linked security.

5. What is MobilePay's role in the Denmark cards and payments market?

MobilePay drives P2P and retail in the Denmark cards and payments market, integrating seamlessly with cards and apps.

6. Which card technologies prevail in the Denmark cards and payments market?

Contactless EMV chips dominate the Denmark cards and payments market, enabling fast taps in transit and stores.

7. How does e-commerce influence the Denmark cards and payments market?

E-commerce boosts secure card and wallet use in the Denmark cards and payments market, with high online shopping rates.

8. What opportunities exist in the Denmark cards and payments market?

BNPL and open banking offer growth in the Denmark cards and payments market for issuers and fintech partnerships.

9. Who leads the Denmark cards and payments market?

Danske Bank, Nordea, and MobilePay shape the Denmark cards and payments market through apps and networks.

10. What regulations affect the Denmark cards and payments market?

PSD2 and instant payments rules enhance competition in the Denmark cards and payments market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com