Europe Second Hand Clothing Market Size, Share, Trends, & Growth Forecast Report By Deployment Mode (Dresses and Tops, Shirts and T-shirts, Sweaters, Coats, and Jackets, Jeans and Pants, Others), Organization Size, Software Function, End-User Industry and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2026 to 2034

Europe Second Hand Clothing Market Report Summary

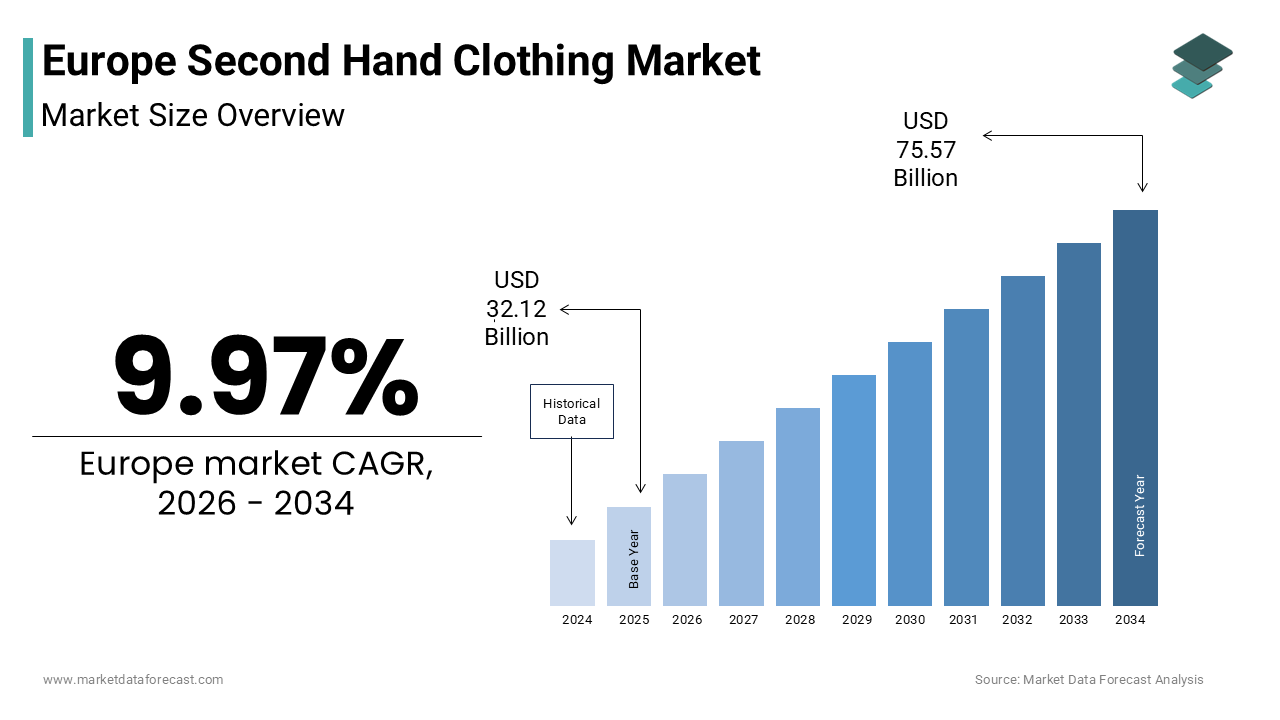

The Europe Second Hand clothing market was valued at USD 32.12 billion in 2025, is estimated to reach USD 35.33 billion in 2026, and is projected to reach USD 75.57 billion by 2034, growing at a CAGR of 9.97% during the forecast period from 2026 to 2034. The growth of the Europe Second Hand clothing market is driven by mainstream cultural acceptance of pre-owned fashion, strong regulatory backing for circular textiles, and increasing digital platform penetration. Rising environmental awareness, EU mandates on textile waste collection, and the expansion of AI-powered resale platforms are transforming Second Hand clothing from a niche alternative into a core pillar of Europe’s circular fashion economy.

Key Market Trends

-

Rapid normalization of pre-owned fashion among Gen Z and millennials across Europe.

-

Expansion of digital resale platforms with integrated logistics and authentication tools.

-

Strong regulatory push through the EU Strategy for Sustainable and Circular Textiles.

-

Growing adoption of brand-led take-back and certified pre-owned programs.

-

Increasing integration of AI-driven personalization and counterfeit detection technologies.

Segmental Insights

-

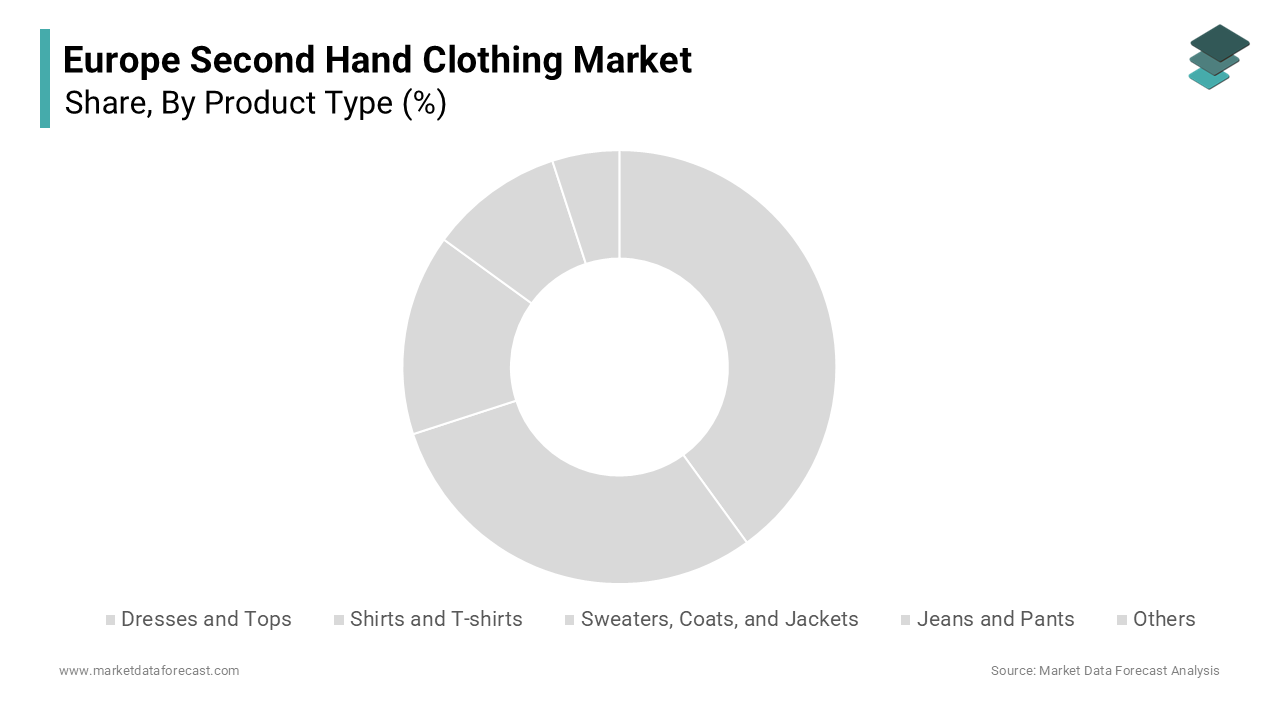

Based on product type, the dresses and tops segment led the market by holding 30.3% of the European market share in 2025, driven by high fashion turnover and strong resale suitability.

-

The coats and jackets segment is projected to witness the fastest CAGR of 15.5% during the forecast period due to durability, premium value retention, and rising demand for high-quality outerwear.

-

Based on sector, the resale segment dominated the market with 61.9% share in 2025, supported by digitized peer-to-peer platforms and structured online marketplaces.

-

Based on sales channel, the online retailers segment accounted for 56.5% of the market share in 2025, driven by convenience, personalization algorithms, and integrated payment and logistics systems.

Regional Insights

The Europe Second Hand clothing market shows strong regional diversity shaped by digital maturity, sustainability awareness, and regulatory alignment.

-

The United Kingdom led the market with 20.2% share in 2025, supported by strong digital resale adoption and a well-established charity retail ecosystem.

-

Germany held the second-largest share in 2025, driven by environmental consciousness, structured textile collection systems, and policy leadership in circular economy frameworks.

-

France is emerging as a premium circular fashion hub supported by the Anti-Waste Law and a strong luxury resale culture.

-

Sweden is projected to register a prominent CAGR due to high household participation in Second Hand exchange and progressive garment tax incentives.

-

The Netherlands continues to expand through digital literacy, urban circular initiatives, and logistical strength across Northwest Europe.

Competitive Landscape

The Europe Second Hand clothing market is highly dynamic and digitally driven, characterized by global resale platforms, regional specialists, and independent vintage retailers. Market leaders focus on authentication technologies, AI-powered personalization, logistics integration, and partnerships with primary fashion brands. The competitive environment is intensifying as traditional retailers embed resale into their core strategies to align with EU circular economy mandates. Major players operating in the Europe Second Hand clothing market include ThredUp Inc., The RealReal Inc., Vestiaire Collective SA, Vinted UAB, Zalando SE, eBay Inc., Depop Ltd., Beyond Retro Ltd., Oxfam GB, and Humana People to People.

Europe Second Hand Clothing Market Size

The Europe second hand clothing market size was valued at USD 32.12 billion in 2025 and is anticipated to reach USD 35.33 billion in 2026 from USD 75.57 billion by 2034, growing at a CAGR of 9.97% during the forecast period from 2026 to 2034.

Second hand clothing refers to the commercial ecosystem facilitating the resale, exchange and redistribution of pre-owned garments and accessories through physical stores, online platforms, and peer-to-peer channels. This market has evolved from a niche segment associated with necessity into a mainstream retail category driven by shifting consumer values and environmental awareness. According to a 2025 Eurobarometer survey on sustainable consumption, European consumers are increasingly embracing second-hand clothing, which is reflecting a cultural shift toward normalization across demographics. As per the European Environment Agency, Europeans discard textiles annually, with only a small portion being reused or recycled, which is indicating the untapped potential for circular fashion models. The European Commission’s Strategy for Sustainable and Circular Textiles mandates that all textile waste be separately collected by 2025, creating structural support for organized resale and reuse infrastructure. This convergence of behavioral change, environmental necessity, and regulatory momentum positions the second-hand clothing market as an integral component of Europe’s future fashion economy.

MARKET DRIVERS

Mainstream Cultural Acceptance and De-stigmatization of Pre-Owned Fashion

The transformation in social perception, where wearing used garments has shifted from a symbol of economic constraint to one of conscious style and environmental responsibility is one of the key factors driving the Europe second-hand clothing market growth. This de-stigmatization is particularly pronounced among younger generations. According to a 2025 YouGov survey, Europeans aged 18 to 34 increasingly view buying second-hand as a positive and fashionable choice. Digital media amplifies this cultural shift, with influencers and celebrities showcasing curated vintage and thrifted outfits, normalizing the practice for millions. The rise of curated online platforms like Vinted and Vestiaire Collective has further elevated the experience, offering authentication, quality grading, and seamless logistics that mimic traditional retail. As per the European Consumer Organisation, trust in the quality of second-hand clothing has increased since 2020, directly correlating with higher purchase frequency. This new social license allows consumers to express individuality while aligning with their values, turning second-hand shopping into a lifestyle statement that transcends class and geography across the continent.

Stringent EU Policy Frameworks Promoting Circular Textile Economies

The European Union’s regulatory agenda aimed at curbing textile waste and enforcing circularity that directly incentivizes the growth of organized second-hand markets is further fuelling the regional market expansion. The EU Strategy for Sustainable and Circular Textiles require all member states to implement separate collection of textile waste by January 2025. This policy creates a formalized supply chain for reusable garments, diverting them from landfills and incinerators toward sorting, refurbishment, and resale channels. Complementing this, the Ecodesign for Sustainable Products Regulation mandates that by 2030, all textiles placed on the EU market must be durable, repairable, and recyclable, implicitly valuing garments with extended lifespans. According to the European Environment Agency, the EU generates textile waste annually, with only a small portion currently recycled into new fibers. By establishing Extended Producer Responsibility schemes, the EU is compelling brands to finance the collection and processing of their end-of-life products, thereby subsidizing the infrastructure that feeds the second-hand market and ensuring its long-term viability as a core pillar of the bloc’s green transition.

MARKET RESTRAINTS

Persistent Quality Inconsistency and Lack of Standardized Grading

The absence of a universal standard for assessing and communicating garment condition that is leading to inconsistent customer experiences and eroded trust is hampering the second-hand clothing market growth in Europe. Unlike new retail, where quality is guaranteed, second-hand items vary dramatically in wear, damage, and cleanliness, creating uncertainty for buyers. According to the European Consumer Organisation, many respondents in a 2025 study cited inaccurate or vague condition descriptions as a primary reason for returning second-hand purchases or avoiding the channel altogether. This problem is exacerbated in peer-to-peer models where sellers lack professional training in textile evaluation. While some platforms have introduced grading systems, these are proprietary and non-interoperable, confusing consumers who shop across multiple sites. The lack of harmonization prevents the market from achieving the reliability expected in modern e-commerce, limiting its appeal to risk-averse shoppers and hindering its ability to scale into the broader mass market.

Logistical and Sanitary Complexities in Cross-Border Resale

The Europe second-hand clothing market faces operational restraints due to logistical and sanitary regulations governing the movement of used textiles across national borders within the EU. Although the EU is a single market, second-hand clothing is often classified under waste or hygiene-sensitive categories, subjecting it to varying national rules on import, disinfection, and labeling. For instance, France requires all imported second-hand garments to undergo certified sanitization, while Germany enforces strict traceability for items sourced outside the EU. According to the European Apparel and Textile Confederation, compliance with divergent national sanitary protocols can increase operational costs for multi-country retailers. These fragmented requirements increase costs and administrative burdens, fragmenting the market and discouraging efficient cross-border inventory pooling. This regulatory patchwork undermines the economies of scale essential for profitability and innovation, effectively trapping many players in local or national silos despite the theoretical freedom of movement within the single market.

MARKET OPPORTUNITIES

Integration of AI-Driven Personalization and Authentication Technologies

A major opportunity for the Europe second-hand clothing market lies in the deployment of artificial intelligence to solve its core challenges of trust and relevance. Advanced computer vision and machine learning algorithms can automate garment authentication, condition grading, and style categorization at scale, directly addressing consumer concerns about quality and fraud. Platforms such as Vestiaire Collective have already implemented AI tools capable of detecting counterfeit luxury items with high accuracy, as verified by internal audits shared with regulators in 2025. Beyond authentication, AI enables hyper-personalized discovery by analyzing user behavior and preferences, algorithms can surface relevant vintage or pre-owned items from vast inventories, replicating the curated feel of a boutique. According to McKinsey, personalized recommendation engines can significantly increase conversion rates in second-hand fashion. As these technologies mature and become more accessible, they will lower barriers to entry for smaller players and elevate the sector’s professionalism, transforming second-hand shopping from a treasure hunt into a predictable, high-fidelity experience.

Expansion of Brand-Led Take Back and Resale Programs

The rapid adoption of official brand-operated resale and take-back schemes that lend institutional credibility and seamless integration to the second-hand ecosystem, which is another major opportunity in the Europe second-hand clothing market. Major European fashion houses and retailers are launching certified pre-owned platforms, such as Zalando’s “Pre-Owned” and H&M’s garment collecting initiative, which has gathered tens of thousands of tonnes of used clothing across Europe since 2013. These programs create a closed loop where customers can return items for store credit and later repurchase authenticated, refurbished pieces from the same brand. This model enhances brand loyalty, provides a controlled channel for managing end-of-life products, and educates consumers on circularity. As per a 2025 survey by Boston Consulting Group, a majority of European shoppers are more likely to buy from a brand that offers a take-back program. As more companies embed resale into their core business strategy, they legitimize the second-hand market while capturing value from extended product lifecycles, which is creating a powerful synergy between primary and secondary retail.

MARKET CHALLENGES

Counterfeit Infiltration in High-Value Second-Hand Segments

A primary challenge confronting the Europe second-hand clothing market is the growing infiltration of counterfeit goods, particularly within the luxury and designer resale segment. The anonymity and scale of online platforms make them attractive vectors for fake merchandise, which erodes consumer trust and exposes legitimate sellers to reputational and legal risk. The European Union Intellectual Property Office estimates that counterfeit apparel and accessories cost the EU economy billions in lost sales in 2023, with a significant portion flowing through informal and online second-hand channels. Authenticating every item is resource-intensive, and many smaller platforms lack the expertise or technology to reliably distinguish fakes. This problem is especially acute for iconic items like handbags and sneakers, where a single counterfeit can trigger negative reviews and chargebacks. The burden of verification falls disproportionately on sellers, discouraging participation from both genuine consumers and professional resellers, ultimately stifling growth in the high-margin luxury segment that is crucial for market profitability.

Environmental Paradox of Digital Second-Hand Logistics

The Europe second-hand clothing market faces a complex sustainability challenge stemming from the carbon footprint of its own success, particularly in e-commerce logistics. While resale extends garment lifespans and reduces the need for new production, the model relies heavily on individual parcel shipping for peer-to-peer transactions and returns. A 2025 study by the Öko-Institut in Germany calculated that the average second-hand online order generates measurable CO₂ emissions, primarily from last-mile delivery and reverse logistics. With return rates in online fashion exceeding 50% in some segments, the environmental benefit of reusing a single garment can be negated by emissions from multiple shipments. This paradox is intensified by consumer expectations of fast and free shipping, which discourage consolidated or low-emission delivery options. Without systemic changes in packaging, routing, and consumer behavior, the digital second-hand boom risks becoming a net contributor to urban congestion and greenhouse gas emissions, undermining its environmental value proposition and inviting scrutiny from regulators focused on genuine circularity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.97% |

| Segments Covered | By Product Type, Sector, Target Population, Sales Channel and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | ThredUp Inc., The RealReal Inc., Vestiaire Collective SA, Vinted UAB, Zalando SE, eBay Inc., Depop Ltd., Beyond Retro Ltd., Oxfam GB, and Humana People to People. |

SEGMENTAL ANALYSIS

By Product Type Insights

The dresses and tops segment led the market by holding 30.3% of the European market share in 2025. The growth of the dresses and tops segment in the European market is driven by high fashion turnover, seasonal versatility, and strong appeal in both casual and formal contexts. Consumers frequently refresh their wardrobes with these items due to rapidly changing trends, making them prime candidates for resale after limited use. According to the European Apparel and Textile Confederation, a majority of European women reported purchasing second-hand dresses or tops in the past year, citing style variety and affordability as key motivators. The segment also benefits from visibility on social platforms like Instagram and Pinterest, where curated vintage blouses or statement dresses drive discovery and demand. Additionally, their relatively low bulk and ease of shipping make them logistically efficient for e-commerce platforms, which is further boosting availability and transaction volume across digital marketplaces.

The coats and jackets segment is a promising segment and is estimated to witness the fastest CAGR of 15.5% over the forecast period owing to the rising consumer preference for high-quality outerwear with extended lifespans, particularly in premium categories such as wool coats, down jackets, and heritage workwear. These items retain significant value and durability long after purchase, making them ideal for circular consumption. A study by the Öko-Institut in Germany found that a majority of European consumers view outerwear as a “long-term investment” and are increasingly willing to buy pre-owned versions to avoid the high cost of new equivalents. The growing popularity of outdoor and functional fashion has elevated demand for second-hand performance jackets. Platforms like Vinted report sharp increases in listings for branded winter coats, reflecting heightened supply and consumer interest. This convergence of durability, brand prestige, and climate-conscious layering needs positions outerwear as the vanguard of premium second-hand adoption.

By Sector Insights

The resale segment dominated the market in 2025 by commanding for 61.9% of the regional market share in 2025. The dominance of re-sale segment in the Europe second-hand clothing market can be credited to the digitization of peer-to-peer and platform-mediated exchanges, which have transformed second-hand shopping into a convenient, scalable, and socially validated activity. Unlike traditional thrift models, resale platforms offer curated inventories, secure payment systems, and user reviews, creating a retail-like experience that appeals to mainstream consumers. According to the data of Eurostat, tens of millions of Europeans used dedicated second-hand fashion apps in 2024, with platforms like Vinted and Vestiaire Collective facilitating billions in annual gross merchandise value. Generational shifts amplify this trend as younger Europeans overwhelmingly prefer resale platforms over charity shops for their selection, speed, and perceived quality control. This digital-first model has repositioned second-hand shopping as a dynamic, choice-driven marketplace rather than a necessity.

The traditional thrift stores & donations segment is experiencing the fastest growth with a CAGR of 13.5% over the forecast period owing to the regulatory support, community engagement, and evolving consumer sentiment toward hyperlocal and socially impactful consumption. The EU’s mandate for separate textile waste collection by 2025 has revitalized donation infrastructure, with organizations like Emmaüs in France and Humana in Sweden expanding their sorting and retail operations. The European Environment Agency reports rising donations to registered charitable organizations, partly due to tax incentives introduced in countries like Germany and Italy. Moreover, consumer surveys show that many now associate thrift stores with “community benefit” and “authentic vintage,” distinguishing them from commercial resale. This moral and nostalgic appeal, combined with policy tailwinds, is transforming traditional thrift into a purpose-driven retail channel with renewed relevance.

By Sales Channel Insights

The online retailers segment dominated the market by accounting for 56.5% of the regional market share in 2025. The growth of the online retailers segment in the European market is driven by convenience, scale, and personalization offered by digital platforms, which have democratized access to second-hand fashion across geographies and demographics. Apps like Vinted, Depop, and Vestiaire Collective provide millions of listings, real-time notifications, and integrated logistics, enabling seamless buying and selling from mobile devices. According to the European Commission, a majority of second-hand clothing transactions in the EU now occur online, up significantly from 2020. Algorithmic recommendations and social features mimic entertainment platforms, turning browsing into a habitual activity. Crucially, online retailers have solved historical pain points of physical second-hand shopping by aggregating supply and offering return policies, converting casual browsers into repeat buyers at scale.

The independent small stores segment the fastest-growing sales channel and is estimated to exhibit a CAGR of 15.8% over the forecast period due to the grassroots movement toward localism, craftsmanship, and experiential retail, where curated vintage boutiques offer tactile and narrative-rich alternatives to algorithm-driven e-commerce. These stores thrive in urban creative districts from Berlin to Lisbon, sourcing unique pieces, restoring garments, and building community through events and styling services. As per a Eurofound survey, many European consumers prefer shopping at independent second-hand stores for their “authenticity” and “personal connection.” Municipal support has also played a role, with cities like Amsterdam and Copenhagen introducing grants for small circular fashion businesses as part of climate action plans. This blend of cultural cachet, sustainability storytelling, and local economic policy is transforming micro-retailers into influential nodes in Europe’s circular fashion ecosystem.

REGIONAL ANALYSIS

United Kingdom Second Hand Clothing Market Analysis

The United Kingdom led the second-hand clothing market in Europe in 2025 by holding 20.2% of the regional market share. The dominance of the UK in the European market is driven by its early adoption of digital resale culture and vibrant vintage scene. London’s status as a global fashion capital has fostered a sophisticated consumer base that values individuality and sustainability, driving demand across both online and physical channels. According to the UK’s Office for National Statistics, millions of adults purchased second-hand clothing in 2024, with platforms like Vinted reporting the UK as its highest user base in Europe. The country’s strong charity retail sector, led by organizations such as Oxfam and the British Heart Foundation, further bolsters the market by providing accessible entry points for first-time buyers. Recent government initiatives, including the Extended Producer Responsibility consultation for textiles, signal continued policy support. This combination of cultural openness, digital maturity, and institutional infrastructure ensures the UK remains the region’s most dynamic and mature second-hand fashion market.

Germany Second Hand Clothing Market Analysis

Germany held the second largest share of the European market in 2025. The growth of Germany in the Europe second-hand clothing market is attributed to the strong environmental consciousness and a robust regulatory framework. German consumers consistently rank among the most sustainability-oriented in Europe; a 2025 Federal Environment Agency survey found that a majority actively seek to extend the life of their clothing through reuse or resale. The country’s well-established network of municipal textile collection bins and charitable organizations like Caritas provides a steady supply stream, while platforms such as Kleiderkreisel (now part of Vinted) have normalized peer-to-peer trading. Germany’s leadership in the EU’s circular economy agenda, including its pioneering role in drafting the Ecodesign for Sustainable Products Regulation, creates a favorable policy climate. Additionally, grassroots initiatives like “repair cafés” and local vintage markets in Berlin and Hamburg reflect a cultural commitment to textile longevity, making Germany a model of systemic integration between policy, infrastructure, and consumer behavior.

France Second Hand Clothing Market Analysis

France is estimated to command for a promising share of the Europe second-hand clothing market over the forecast period due to its blend of luxury heritage and progressive environmental legislation. The French government has shaped the circular fashion landscape through measures such as the Anti-Waste for a Circular Economy Law, which bans the destruction of unsold non-food goods, which is a policy that has redirected thousands of tonnes of apparel into second-hand channels. According to France’s Ministry of Ecological Transition, textile reuse activities grew significantly between 2021 and 2024, supported by state-backed initiatives like the “Recyclerie” network. Paris remains a global hub for vintage fashion, with iconic boutiques in Le Marais attracting international buyers. A 2025 IFOP survey revealed that many French consumers view second-hand shopping as “chic and responsible,” reflecting a cultural shift where sustainability enhances style. This synergy of regulatory ambition and aesthetic sensibility positions France as a trendsetter in premium circular fashion.

Sweden Second Hand Clothing Market Analysis

Sweden is anticipated to register a prominent CAGR in the European second-hand clothing market over the forecast period. Sweden is serving as a Nordic leader in sustainable consumption and innovation. The country’s high penetration of digital platforms is matched by a deeply ingrained culture of reuse, exemplified by the popularity of “loppis” (flea markets) and community swap events. According to Statistics Sweden, a majority of households participated in some form of second-hand clothing exchange in 2024, the highest rate in the EU. Sweden’s garment tax reduction policy, which lowered VAT on repaired and reused clothing in 2022, has boosted affordability and demand. Companies like Sellpy have scaled nationally by integrating collection, sorting, and resale into a seamless circular loop. Furthermore, municipalities actively support textile recycling infrastructure, with most urban areas offering dedicated collection points. This holistic ecosystem makes Sweden a benchmark for systemic circularity in fashion.

Netherlands Second Hand Clothing Market Analysis

The Netherlands is projected to hold a noteworthy share of the European second-hand clothing market over the forecast period owing to its logistical prowess and progressive urban policies to become a hub for circular fashion innovation. Amsterdam and Rotterdam host a dense concentration of vintage stores, repair studios, and platform headquarters, benefiting from the country’s high digital literacy and international connectivity. According to the Dutch Central Bureau of Statistics, a majority of Dutch consumers aged 18 to 40 purchased second-hand clothing in the past year, driven by environmental awareness and pragmatic frugality. The national government’s “Circular Economy 2050” roadmap includes specific targets for textile reuse, while cities like Utrecht offer subsidies for circular fashion startups. The Netherlands’ strategic location and advanced port infrastructure also facilitate the import and redistribution of second-hand garments across Northwest Europe. This combination of consumer readiness, policy foresight, and logistical advantage enables the Netherlands to exert influence far beyond its production volume.

COMPETITIVE LANDSCAPE

The competition in the Europe second hand clothing market is highly dynamic, characterized by a three-tiered structure comprising global digital platforms regional specialists and local independent operators. At the top, companies like Vinted and Vestiaire Collective dominate through scale technology and brand recognition, competing on user experience trust and logistics efficiency. Mid-tier players include national platforms such as Sellpy in Sweden and Rebelle in Germany, which focus on niche segments or localized services. Meanwhile thousands of small vintage boutiques charity shops and flea markets form a fragmented but culturally significant grassroots layer. Intense rivalry is driving rapid innovation in areas like AI powered authentication carbon footprint tracking and seamless returns. The entry of traditional fashion brands into resale through partnerships or proprietary platforms is further intensifying competition, blurring the lines between primary and secondary retail and pushing the entire ecosystem toward greater professionalism and integration.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe second hand clothing market include

- ThredUp Inc.

- The RealReal Inc.

- Vestiaire Collective SA

- Vinted UAB

- Zalando SE

- eBay Inc.

- Depop Ltd.

- Beyond Retro Ltd.

- Oxfam GB

- Humana People to People

Top Players in the Europe Second Hand Clothing Market

Vinted

Vinted is a leading force in the Europe second hand clothing market, operating as a peer-to-peer marketplace that empowers individuals to buy and sell pre owned garments with minimal friction. Headquartered in Vilnius but deeply embedded in Western European markets like Germany France and the UK, Vinted has redefined user experience through its no listing fee model integrated logistics and robust trust and safety protocols. The company contributes significantly to the global circular fashion movement by enabling millions of transactions annually while promoting sustainable consumption. To strengthen its position, Vinted launched its “Green Checkout” feature in early 2025, which offsets carbon emissions from every shipment and provides transparency on environmental impact, reinforcing its brand as a responsible platform aligned with European sustainability values.

Vestiaire Collective

Vestiaire Collective is a premium player in the Europe second hand clothing market, specializing in authenticated luxury and designer pre owned fashion. Based in Paris, it has established itself as a global benchmark for trust and quality in high end resale, serving discerning clients across Europe North America and Asia. The platform’s rigorous verification process conducted in its authentication centers ensures product integrity, addressing a key barrier in luxury second hand adoption. In 2025, Vestiaire Collective expanded its physical presence by opening a flagship store in Milan and enhanced its AI powered authentication tools to detect counterfeits with greater accuracy. These moves reinforce its dual strategy of blending digital scale with tangible retail experiences while solidifying its role in shaping the future of responsible luxury consumption worldwide.

ThredUp

ThredUp, though US headquartered, maintains a strategic and growing footprint in the Europe second hand clothing market through its Clean Out service and B2B partnerships with European retailers. It operates one of the world’s largest automated sorting and processing facilities, enabling scalable resale operations for both consumers and brands. ThredUp contributes globally by providing technology infrastructure that powers circularity programs for major fashion companies. In Europe, it has deepened collaborations with retailers like M&S and Galeria Karstadt Kaufhof to manage their recommerce initiatives. In January 2025, ThredUp launched its Resale as a Service platform in Germany, allowing European brands to embed second hand offerings directly into their e-commerce sites, thereby accelerating mainstream adoption of circular business models across the region.

Top Strategies Used by the Key Market Participants

Key players in the Europe second hand clothing market are deploying several core strategies to secure competitive advantage. First, they are investing heavily in authentication and quality control technologies to build consumer trust, especially in luxury segments. Second, they are expanding physical touchpoints such as pop-up stores and permanent boutiques to complement online platforms and enhance brand experience. Third, they are forming strategic partnerships with traditional fashion retailers to offer integrated resale services under white label models. Fourth, they are leveraging artificial intelligence for personalized recommendations dynamic pricing and automated garment categorization to improve efficiency and user engagement. Finally, they are embedding environmental impact metrics into the shopping journey to align with European consumers’ strong sustainability values and comply with emerging regulatory expectations around circularity.

MARKET SEGMENTATION

This research report on the Europe second hand clothing market has been segmented and sub-segmented based on the following categories.

By Product Type

- Dresses and Tops

- Shirts and T-shirts

- Sweaters, Coats, and Jackets

- Jeans and Pants

- Others

By Sector

- Resale

- Traditional Thrift Stores & Donations

By Target Population

- Men

- Women

- Kids

By Sales Channel

- Wholesalers or Distributors

- Hypermarkets or Supermarkets

- Multi-brand Stores

- Independent Small Stores

- Departmental Stores

- Online Retailers

- Other Sales Channel

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Second Hand Clothing Market?

It refers to the buying, selling, and redistribution of pre-owned apparel across European countries through online platforms, thrift stores, charity shops, and resale marketplaces.

What factors are driving growth in the Europe second-hand clothing market?

Rising sustainability awareness, affordability concerns, circular economy initiatives, and digital resale platforms are major growth drivers.

How does sustainability influence market expansion?

Consumers increasingly prefer eco-friendly fashion alternatives to reduce textile waste and carbon footprint, supporting resale and reuse trends.

Which sales channels dominate the market?

Online resale platforms and mobile apps are growing rapidly, while thrift stores and charity retail outlets continue to hold steady demand.

Which product categories are most popular in second-hand clothing?

Casual wear, vintage fashion, luxury resale, children’s clothing, and branded apparel are leading categories.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com