Finland Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATMs), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Transaction Value, Volumes, Historical Trends, Industry Analysis From 2025 to 2033

Finland Cards and Payments Market Size

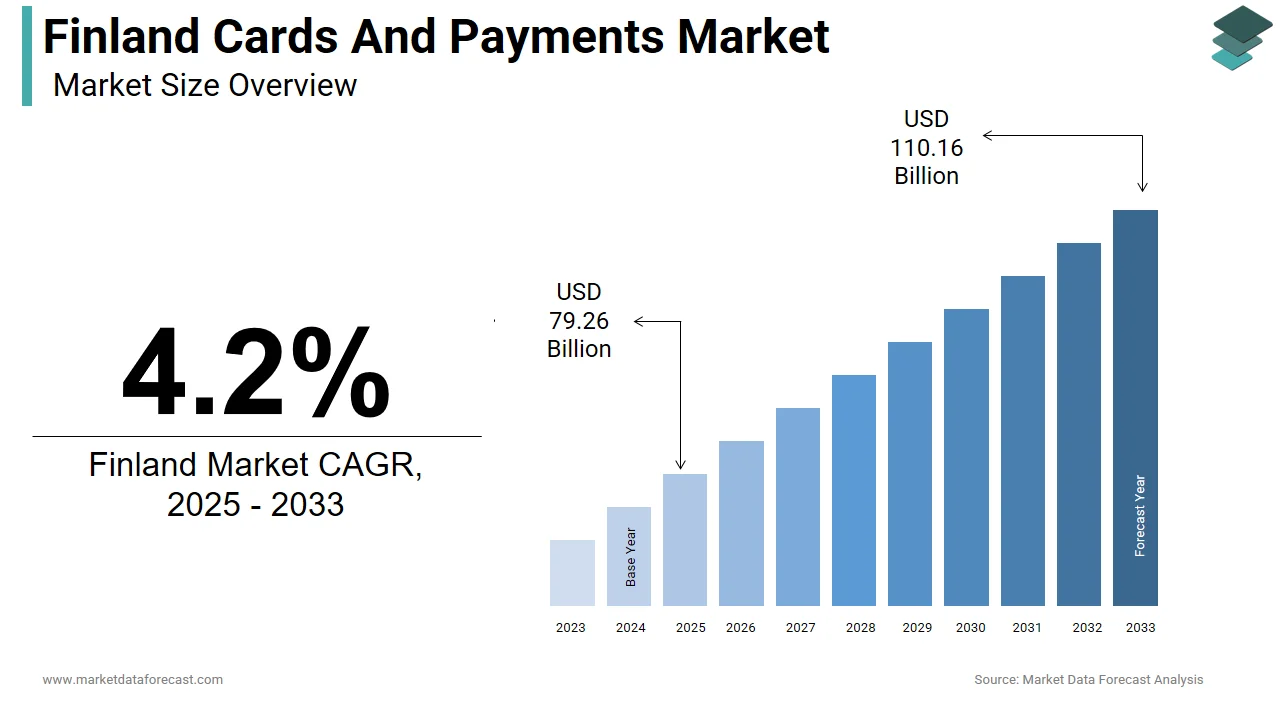

The Finland cards and payments market size was valued at USD 76.07 billion in 2024. This market is expected to grow at a CAGR of 4.2% from 2025 to 2033 and be worth USD 110.16 billion by 2033 from USD 79.26 billion in 2025.

MARKET DRIVERS

High Digital Readiness and Rapid Adoption of Contactless Payments

Finland is among the most digitally advanced countries in the world, and this digital maturity has significantly driven the growth of its cards and payments market. According to Statistics Finland (Tilastokeskus), as of 2023, a large majority of Finns used the internet daily, and smartphone ownership was very high. This widespread digital adoption has enabled a swift transition toward contactless card and mobile payment usage. The Bank of Finland reported that in 2023, contactless transactions accounted for approximately 85% of all domestic card payments under €20, with an average of 150 contactless transactions per person annually. Mobile wallets such as Apple Pay, Google Pay, and local solutions like Nordea’s Mobile Mastercard have seen strong uptake, particularly among urban populations. As cash usage continues to decline—making Finland one of the most cashless societies globally, the cards and payments sector remains on a robust growth trajectory.

Strong Government Support for Financial Innovation and Open Banking

Another key driver of Finland's cards and payments market is the proactive regulatory environment that encourages fintech innovation and open banking. As an early adopter of the EU’s revised Payment Services Directive (PSD2), Finland has facilitated seamless integration between traditional banks and third-party providers, enhancing competition and service diversity. The Finnish Financial Supervisory Authority (FIN-FSA) reported that by the end of 2023, more than 40 licensed fintech firms were actively offering payment initiation or account information services. Leading banks such as OP Financial Group and Handelsbanken have launched open API platforms to support financial startups in developing new digital products.

MARKET RESTRAINTS

Declining Number of Physical ATMs and Cash Acceptance Points

A significant restraint on Finland’s cards and payments market is the rapid decline in physical ATMs and cash acceptance points, which poses challenges for certain segments of the population who still rely on cash. While Finland moves closer to becoming a fully cashless society, this growing divide highlights the need for inclusive policies that ensure equitable access to financial services across all demographics.

Rising Concerns Over Data Privacy and Cybersecurity in Digital Payments

Despite Finland’s advanced digital payment infrastructure, rising concerns over data privacy and cybersecurity are acting as restraints on further expansion of the cards and payments market. A 2023 report by the Finnish Transport and Communications Agency (Traficom) revealed that cyberattacks targeting financial institutions increased by 21% compared to the previous year, with phishing, ransomware, and payment fraud being the most common threats. Meanwhile, the FIN-FSA recorded substantial payment-related fraud losses in 2023. As digital payment channels expand, maintaining consumer trust will require continuous investment in robust encryption technologies, real-time fraud detection systems, and comprehensive consumer education programs.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services in E-Commerce

A growing opportunity in Finland’s cards and payments market is the expansion of Buy Now, Pay Later (BNPL) services, particularly within the e-commerce sector. International players like Klarna and (local operators) such as Lainarahasto and Afterpay (before its acquisition) have been expanding their presence in the Finnish market, partnering with major retailers including Stockmann, Elisa, and Verkkokauppa.com. Data from the Financial Supervisory Authority of Finland indicates that BNPL transaction value reached €1.8 billion in 2023, reflecting a 25% annual increase. These services appeal to younger consumers seeking flexible payment options without long-term debt commitments. As regulatory frameworks evolve to accommodate BNPL while ensuring consumer protection, this segment is poised to become a mainstream alternative to traditional credit cards, offering substantial revenue opportunities for payment providers and boosting overall digital transaction volumes.

Integration of Embedded Finance across Non-Financial Platforms

The rise of embedded finance presents a transformative opportunity for Finland’s cards and payments market, allowing non-financial platforms—from ride-hailing apps to real estate portals—to integrate payment and financial services directly into their ecosystems. According to a report by EY Finland, the embedded finance landscape is expected to grow significantly at an annual rate of 15% through 2027, driven by partnerships between fintechs and traditional banks. As demand for seamless, frictionless transactions rises, embedded finance is set to become a key growth driver in Finland’s evolving digital payments landscape.

MARKET CHALLENGES

Increasing Sophistication of Financial Fraud and Identity Theft

Despite Finland’s advanced digital payment infrastructure, the sector faces a growing challenge from increasingly sophisticated financial fraud and identity theft schemes. Phishing attacks, fake merchant sites, and synthetic identity fraud have become more prevalent, exploiting weaknesses in multi-factor authentication and consumer awareness. The FIN-FSA highlighted in its 2023 annual report that card-not-present (CNP) fraud accounted for over 73% of all digital payment fraud cases. Although major banks like OP Financial Group and Danske Bank Finland have implemented AI-based fraud detection systems, many consumers, especially seniors, are still vulnerable to social engineering tactics.

Regulatory Complexity and Compliance Burden for Fintech Startups

While Finland maintains a progressive regulatory framework for digital finance, emerging fintech startups face challenges related to regulatory complexity and compliance costs. According to a 2023 report by PwC Finland, the average time to obtain a full payment institution license was between 9 to 13 months, with initial setup costs often exceeding €500,000. Startups also face ongoing reporting obligations and capital adequacy rules that can hinder agility and speed to market. While regulation ensures financial stability and consumer protection, streamlining oversight and improving dialogue between regulators and innovators could help accelerate the development of next-generation payment solutions in Finland.

MARKET KEY HIGHLIGHTS

The shift of banking industry towards digitalization is providing all the services over the internet or smartphone, like German-based mobile-only bank Number26, and Holvi, which offers services to small SMEs and entrepreneurs through its digital solutions and launcheda Business MasterCard debit card only for customers in business.

The decline in the number of ATMs and branches of the banks displays a growing society of cashless transactions and customers' preference for digital payments, as per the Nordic regional trends.

The instant money transfer solution Siirto, introduced by ATM operator Automia and developed by Tieto Finnish IT services, allows transactions using the recipient's mobile number and is currently available for customers of Nordea Bank, OP Bank, and S-Bank, alongside its e-commerce payments option.

KEY MARKET PLAYERS

Top players in the Finland cards and payments market include

- OP Bank

- Nordea

- Danske Bank

- Aktia Bank

- SSaastopankki

- SEB

MARKET SEGMENTATION

This research report on the Finland cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Finland cards and payments market?

The Finland cards and payments market is about USD 79.26 billion in 2025 and is projected to reach roughly USD 110.16 billion by 2033 as digital and contactless usage expands.

2. What is the growth rate of the Finland cards and payments market?

The Finland cards and payments market is expected to grow near 4.2% CAGR to 2033, driven by high card penetration, digital wallets, and strong POS infrastructure nationwide.

3. What drives the Finland cards and payments market?

Key drivers of the Finland cards and payments market include near‑cashless consumer behavior, mobile and virtual terminals, and rapid e‑commerce and digital wallet adoption.

4. How important are debit cards in the Finland cards and payments market?

Debit cards remain the main everyday instrument in the Finland cards and payments market, reflecting universal bank accounts and strong acceptance in retail and online channels.

5. What role do credit cards play in the Finland cards and payments market?

Credit cards in the Finland cards and payments market support travel, e‑commerce, and higher‑value purchases, while facing competition from BNPL and account‑to‑account options.

6. How is contactless adoption shaping the Finland cards and payments market?

Contactless now accounts for the vast majority of card taps in the Finland cards and payments market, with over four in five low‑value payments made via tap at POS terminals.

7. How do digital wallets affect the Finland cards and payments market?

Digital wallets like Apple Pay and Google Pay are expanding in the Finland cards and payments market, linking cards to convenient, tokenised in‑store and online transactions.

8. What is the impact of e‑commerce on the Finland cards and payments market?

Growing online retail pushes the Finland cards and payments market toward card, wallet, and A2A checkouts, as merchants seek lower fees and seamless consumer experiences.

9. How are virtual terminals influencing the Finland cards and payments market?

Virtual terminals already handle a rising share of value in the Finland cards and payments market, as more card payments start inside apps and browser‑based online flows.

10. What opportunities exist in the Finland cards and payments market?

Opportunities in the Finland cards and payments market include embedded finance, BNPL, contactless transit pilots, and SME‑focused SoftPOS and remote card acceptance tools.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com