Hong Kong Cards And Payments Market Size, Share, Trends & Growth Forecast Report By Cards (Debit Cards, Credit Cards & Prepaid Cards), Payment Terminals (POS and ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques and Payment Cards), Transaction Value, Volumes, Historical Trends, Analysis And Forecasts 2026 to 2034

Hong Kong Cards and Payments Market Report Summary

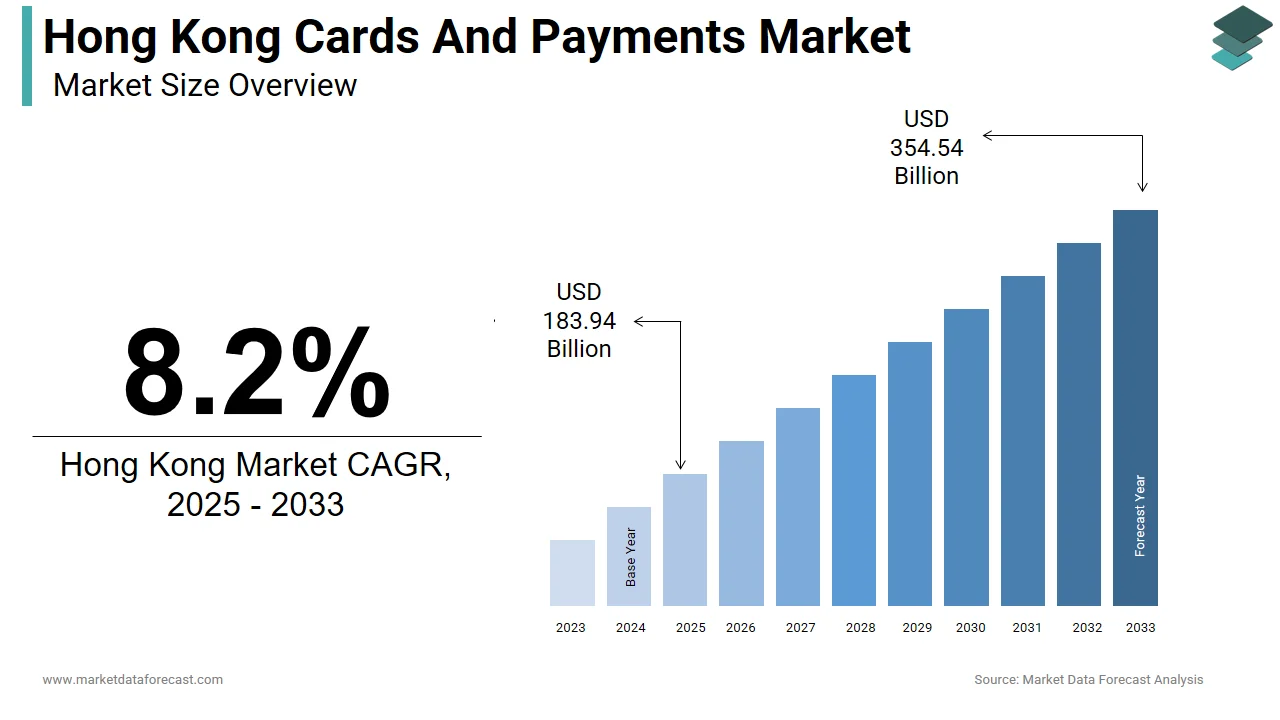

The Hong Kong cards and payments market was valued at USD 183.94 billion in 2025 and is projected to grow from USD 199.02 billion in 2026 to USD 373.87 billion by 2034, registering a CAGR of 8.2% from 2026 to 2034. Market growth is driven by the increasing adoption of cashless payment methods, widespread use of payment cards, and the rapid expansion of digital commerce across the region. Hong Kong's advanced financial infrastructure, high banking penetration, and strong regulatory framework continue to support the evolution of secure and convenient payment solutions. The growing popularity of contactless payments, mobile wallets, and e-commerce transactions is further accelerating market expansion.

Key Market Trends

- Increasing adoption of contactless card payments across retail and service sectors.

- Rising growth of e-commerce and digital payment ecosystems.

- Growing integration of mobile wallets and omnichannel payment solutions.

- Continuous investments in payment security, tokenization, and fraud prevention technologies.

- Expansion of cross-border digital payment services supported by Hong Kong's position as an international financial hub.

Segmental Insights

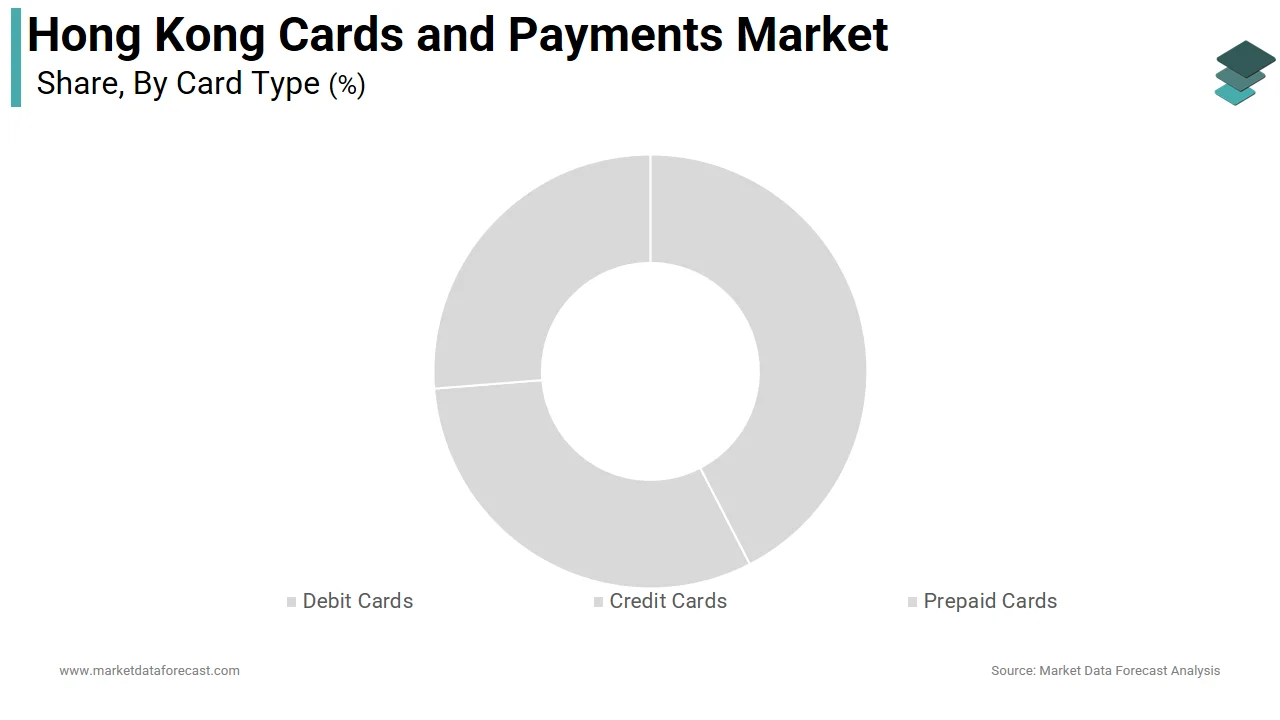

- Based on card type, the credit card segment dominated the Hong Kong cards and payments market in 2025 by accounting for 55.6% market share, driven by high consumer spending, widespread merchant acceptance, attractive rewards programs, and strong adoption of contactless payment technologies.

Competitive Landscape

The Hong Kong cards and payments market is highly competitive, with leading banks, global card networks, and financial institutions focusing on digital innovation, customer experience, and payment security. Market participants are investing in contactless payment technologies, digital banking services, loyalty programs, and cross-border payment capabilities to strengthen their market presence. Strategic collaborations between banks, fintech companies, and payment networks continue to drive innovation across the market.

Prominent companies operating in the Hong Kong cards and payments market include HSBC, Bank of China, Mastercard, Visa, Standard Chartered, Bank of East Asia, and Citibank.

Hong Kong Cards and Payments Market Size

The Hong Kong cards and payments market size was valued at USD 183.94 billion in 2025. This market is expected to grow at a CAGR of 8.2% from 2026 to 2034 and be worth USD 373.87 billion by 2034 from USD 199.02 billion in 2026.

The Hong Kong cards and payments market is expected to experience steady growth and technological advancement over the next few years, as digital platforms continue to expand. This digital financial infrastructure is deeply integrated into the daily lives of residents and visitors alike, supporting everything from public transportation to high-end retail purchases. The region boasts one of the highest smartphone penetration rates globally, which acts as the foundational bedrock for mobile payment adoption. According to the Census and Statistics Department, the total retail sales value in the region reached approximately 376.8 billion Hong Kong dollars in 2024. Furthermore, the recovery of the tourism sector has significantly amplified transaction volumes. As per the Hong Kong Tourism Board, the region welcomed over 44.5 million visitor arrivals in 2024. The Monetary Authority actively regulates this space, ensuring systemic stability while fostering innovation through various fintech supervisory frameworks.

MARKET DRIVERS

The return of international and mainland travelers has fundamentally revitalized the local retail and hospitality sectors, creating an urgent demand for diverse and universally accepted payment solutions. Visitors often arrive with specific digital payment habits, necessitating that local merchants upgrade their terminal infrastructure to accommodate foreign mobile wallets and international credit cards. According to the Hong Kong Tourism Board, the region recorded approximately 44.5 million visitor arrivals in 2024. To capture these lucrative demographic, merchants must integrate quick response code systems and near-field communication terminals that support multiple global payment networks. Furthermore, according to the Census and Statistics Department, the retail sales value reached approximately 376.8 billion Hong Kong dollars recently. Financial institutions are aggressively partnering with international payment networks to offer multi-currency settlement and dynamic currency conversion services, ensuring that tourists can transact seamlessly without incurring excessive foreign exchange fees.

Consumers in the region increasingly prefer the convenience of scanning a digital code or tapping a mobile device over carrying physical wallets, driving massive adoption of stored-value facilities. The integration of these digital applications into everyday lifestyle services, such as public transit, utility bill payments, and peer-to-peer transfers, creates a highly sticky ecosystem. According to the Hong Kong Monetary Authority, there are currently over 20 licensed stored-value facility operators. Furthermore, the government has actively promoted the use of digital payments through various consumption voucher schemes. As per the Financial Services and the Treasury Bureau, the disbursement of digital consumption vouchers injected over 30 billion Hong Kong dollars directly into the electronic payment ecosystem.

MARKET RESTRAINTS

Small retail shops and independent restaurants often operate on extremely thin profit margins, making them highly sensitive to the transaction fees levied by payment processors and acquiring banks. When a customer pays using a credit card or a specific digital wallet, the merchant is typically charged a percentage of the total transaction value, which can significantly erode their net profitability. According to the Federation of Hong Kong Industries, approximately 45% of small enterprises cite high payment processing costs as a primary barrier to upgrading their point-of-sale systems. Many micro-merchants still prefer cash transactions to avoid these recurring financial deductions, despite the overwhelming consumer preference for cashless payments. Furthermore, according to the Hong Kong Small and Medium Enterprises Association, the initial capital expenditure required to purchase smart terminals and the ongoing monthly connectivity fees present an insurmountable hurdle for newly established businesses. Payment networks and banks have been slow to reduce these fees due to the complex interchange fee structures and the high costs of maintaining secure processing infrastructure.

Financial institutions and fintech companies must navigate a complex web of regulatory mandates designed to protect consumer data and ensure the absolute integrity of the financial system. The Personal Data Privacy Ordinance and the strict cybersecurity guidelines issued by the Monetary Authority require continuous investment in advanced encryption technologies, real-time fraud monitoring systems, and regular third-party security audits. According to the Office of the Privacy Commissioner for Personal Data, the number of suspected data privacy breaches in the financial sector has risen significantly. To maintain their operating licenses, payment providers must allocate a substantial portion of their technology budgets purely toward regulatory compliance rather than developing new consumer-facing features. Furthermore, according to the Hong Kong Computer Society, the average cost of implementing enterprise-grade security infrastructure has increased by over 30% in recent years due to the escalating sophistication of cyber threats. This heavy financial burden disproportionately affects smaller fintech startups that lack the economies of scale enjoyed by major banks.

MARKET OPPORTUNITIES

By securely sharing customer data with authorized third-party providers, banks can unlock entirely new revenue streams and deliver highly personalized financial services directly within non-banking applications. The Monetary Authority has actively championed the open application programming interface initiative, allowing fintech companies to integrate payment initiation and account information services directly into electronic commerce platforms and lifestyle applications. According to the Hong Kong Monetary Authority, over 300 open application programming interfaces have been successfully launched across various business domains. This structural evolution allows consumers to initiate payments or check their balances without ever leaving their favorite retail or social media applications, creating a highly frictionless user experience. Furthermore, according to the Asian Development Bank, the broader regional adoption of open finance models could increase digital payment transaction volumes by over 25% within the next five years. By leveraging these secure data-sharing protocols, payment providers can develop contextual financial products, such as instant point-of-sale financing or automated micro-savings tools.

Consumers and merchants alike are increasingly demanding payment experiences that require zero physical interaction with terminals or mobile devices, drastically reducing queue times and improving operational efficiency. Technologies such as facial recognition, palm scanning, and advanced behavioral biometrics allow users to authorize transactions simply by looking at a camera or hovering their hand over a sensor. According to the International Biometric Industry Association, the global deployment of biometric payment terminals in the retail sector is expanding at an accelerated pace, with adoption rates in advanced Asian economies leading the world. In the local market, major supermarket chains and convenience stores are actively piloting these systems to process thousands of customers per hour without the need for physical cards or mobile phones. Furthermore, according to the World Economic Forum, biometric authentication can reduce checkout times by up to 40%. Payment networks are heavily investing in the underlying tokenization infrastructure required to make these biometric transactions completely secure and compliant with global privacy standards.

MARKET CHALLENGES

The Hong Kong market is currently saturated with numerous competing mobile wallet applications, each offering slightly different loyalty programs, merchant acceptance networks, and user interfaces. This overwhelming abundance of choices forces consumers to manage multiple applications simultaneously, leading to frustration and a degraded overall user experience. According to the Hong Kong Monetary Authority, there are more than 20 distinct stored-value facility operators actively competing in the region. When a consumer attempts to make a purchase, they frequently discover that their preferred wallet is not accepted at a specific merchant, forcing them to revert to cash or physical cards. Furthermore, according to the Federation of Hong Kong Industries, small merchants are forced to maintain multiple quick-response code stands and separate settlement accounts just to accommodate the diverse preferences of their customers. This operational complexity increases the administrative burden on retail staff and complicates daily financial reconciliation.

Cybercriminals are continuously developing highly deceptive methods to steal sensitive payment credentials and manipulate consumers into authorizing fraudulent transactions. The use of deepfake technology, artificial intelligence voice cloning, and highly personalized spoofed messages makes it increasingly difficult for even vigilant users to distinguish between legitimate communications from their banks and malicious fraud attempts. According to the Hong Kong Police Force, the number of reported deception cases involving electronic payment platforms and online banking has surged dramatically, resulting in over 5 billion Hong Kong dollars in total financial losses over the recent period. When consumers fall victim to these sophisticated scams, they often lose confidence in the security of digital payment methods, leading to a temporary reversion to cash usage. Financial institutions are forced to invest heavily in advanced behavioral analytics and real-time transaction blocking systems to intercept fraudulent activities before the funds are permanently lost. Furthermore, according to the Hong Kong Association of Banks, the cost of reimbursing victims and upgrading fraud detection infrastructure places immense financial pressure on the banking sector.

SEGMENT ANALYSIS

By Card Type Insights

The credit card segment commanded an overwhelming share of 55.6% of the Hong Kong cards and payments market in 2025. The aggressive deployment of lucrative reward programs and cashback incentives acts as the primary catalyst for credit card dominance. Financial institutions in the region continuously compete for consumer mindshare by offering highly attractive points-accumulation systems that can be redeemed for air travel, luxury goods, and exclusive lifestyle experiences. According to the Hong Kong Monetary Authority, the total outstanding credit card lending consistently exceeds 100 billion Hong Kong dollars. Retailers actively partner with major banks to launch co-branded cards that provide instant discounts at the point of sale, further embedding these plastic instruments into the daily purchasing habits of the population. Furthermore, according to the Census and Statistics Department, retail sales heavily concentrate in high-value categories such as electronics and jewelry, where the ability to earn substantial reward points significantly influences the choice of payment method.

On the other side, the prepaid card segment is experiencing the fastest expansion and is expected to expand at a CAGR of 15.5% during the forecast period. The seamless integration of prepaid cards with mobile wallet applications and the robust recovery of the tourism sector drive rapid expansion. Modern consumers and international visitors heavily prefer the convenience of loading funds onto digital stored-value facilities that can be instantly accessed via smartphones for transit and retail purchases. According to the Hong Kong Monetary Authority, the total value stored in licensed stored-value facilities has surpassed 25 billion Hong Kong dollars. As per the Hong Kong Tourism Board, the region welcomed over 44.5 million visitor arrivals recently, with many tourists utilizing cross-border mobile payment solutions linked to prepaid instruments to navigate the local cashless economy. This digital convergence allows users to enjoy the security of prepaid limits while benefiting from the frictionless experience of mobile transactions. Furthermore, the integration of these cards with public transportation networks and government consumption voucher schemes has fundamentally normalized their usage across all demographic segments.

COMPETITIVE LANDSCAPE

The competition within the Hong Kong cards and payments sector is characterized by intense rivalry among traditional banking institutions and agile financial technology companies. Major global card networks leverage their extensive international acceptance to attract premium consumers seeking seamless cross-border transaction capabilities. Meanwhile, local banks aggressively compete by offering highly lucrative reward programs and zero annual fee credit cards to capture the affluent demographic. The emergence of digital wallet providers has further fragmented the landscape, forcing legacy institutions to accelerate their digital transformation initiatives. These traditional players are heavily investing in proprietary mobile applications and open banking frameworks to retain customer loyalty and prevent capital flight to non-bank entities. Furthermore, strategic partnerships between retail merchants and payment processors have become a critical differentiator, enabling exclusive discount ecosystems that lock consumers into specific payment loops. The regulatory environment also shapes competitive dynamics as the monetary authority encourages interoperability and fair competition among stored value facility operators. Ultimately, the market demands continuous innovation in biometric security and instant settlement technologies, ensuring that only the most technologically advanced and consumer centric organizations maintain their profitability and relevance in this highly sophisticated financial ecosystem, right now, today, and tomorrow across the region.

KEY MARKET PLAYERS

Top players in the Hong Kong cards and payments market include

- HSBC

- Bank of China

- Mastercard

- Visa

- Standard Chartered

- Bank of East Asia

- Citibank

TOP PLAYERS IN THE MARKET

- HSBC operates as a premier global financial institution providing comprehensive payment solutions and credit card products to millions of customers worldwide. The corporation leverages its extensive international network to facilitate seamless cross-border transactions and premium wealth management services. Recently, the enterprise launched an advanced artificial intelligence-driven fraud detection system to enhance transaction security and protect consumer assets. This strategic innovation significantly reduces false declines and improves the overall checkout experience for cardholders. By prioritizing digital transformation and customer-centric security measures, the organization successfully reinforces its industry leadership and drives substantial technological advancement across international markets right now.

- Visa functions as a monumental global payments technology company connecting consumers, merchants, and financial institutions across the entire planet. The corporation utilizes its massive processing network to enable billions of secure electronic transactions every single year with unmatched reliability. In a recent strategic move, the enterprise unveiled a new tokenization framework designed to protect sensitive card data during online purchases. This technological breakthrough enables merchants to accept digital payments safely while eliminating the risk of data breaches. Through continuous investment in cybersecurity and global interoperability, the company maintains its formidable presence and accelerates enterprise adoption worldwide right now.

- Mastercard stands as a premier international technology company operating a highly efficient global payment network that facilitates commerce for everyone. The organization focuses heavily on creating innovative digital payment experiences that integrate seamlessly with modern electronic commerce platforms and mobile applications. Recently, the corporation completed the integration of advanced biometric authentication protocols into its core processing systems to verify user identity instantly. This massive operational upgrade significantly enhances transaction security and reduces friction during the checkout process for millions of global consumers. By prioritizing technological excellence and seamless connectivity, the enterprise successfully attracts major clients and maintains a competitive edge.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the market employ several strategic approaches to reinforce their competitive standing and capture evolving consumer preferences. Product innovation remains central as companies develop advanced mobile applications and biometric authentication tools tailored for frictionless checkout experiences. Strategic partnerships are another common tactic, with major financial institutions collaborating directly with retail merchants and transit authorities to embed payment interfaces into everyday lifestyle applications. Investment in open banking frameworks allows providers to securely share data with third-party developers, creating highly personalized financial ecosystems. Geographic expansion, particularly into cross-border payment corridors, enables access to international tourists and global commerce. Lastly, continuous investment in artificial intelligence ensures that fraud detection systems remain perfectly synchronized with emerging cyber threats, ensuring long-term commercial viability and sustained consumer trust across all digital transaction environments today.

MARKET SEGMENTATION

This research report on the Hong Kong cards and payments market has been segmented and sub-segmented based on the following categories.

By Card Type

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What defines the Norway cards and payments market?

The Norway cards and payments market includes debit, credit, and prepaid cards plus digital options, driven by strong non-cash preferences.

2. How does the Norway cards and payments market evolve?

The Norway cards and payments market progresses via contactless tech and mobile solutions amid digital infrastructure advances.

3. What drives changes in the Norway cards and payments market?

Tech innovation and e-commerce growth push the Norway cards and payments market toward seamless payment ecosystems.

4. Who leads the Norway cards and payments market?

Major banks and card networks shape the Norway cards and payments market through competitive digital services.

5. What role do debit cards have in the Norway cards and payments market?

Debit cards anchor everyday use in the Norway cards and payments market, valued for simplicity and security.

6. How prominent are contactless payments in the Norway cards and payments market?

Contactless methods thrive in the Norway cards and payments market, boosting transaction efficiency everywhere.

7. What impact do mobile wallets have on the Norway cards and payments market?

Mobile wallets enhance convenience within the Norway cards and payments market for instant, secure payments.

8. How does e-commerce influence the Norway cards and payments market?

E-commerce expands card reliance in the Norway cards and payments market for reliable online transactions.

9. What is BNPL's place in the Norway cards and payments market?

Buy Now Pay Later integrates into the Norway cards and payments market, suiting installment-based purchases.

10. Are QR payments growing in the Norway cards and payments market?

QR codes emerge in the Norway cards and payments market for versatile retail and peer-to-peer applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com