Italy Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards) - Transaction Value, Volumes, Historical Trends, Industry Analysis From 2025 to 2033

Italy Cards And Payments Market Size

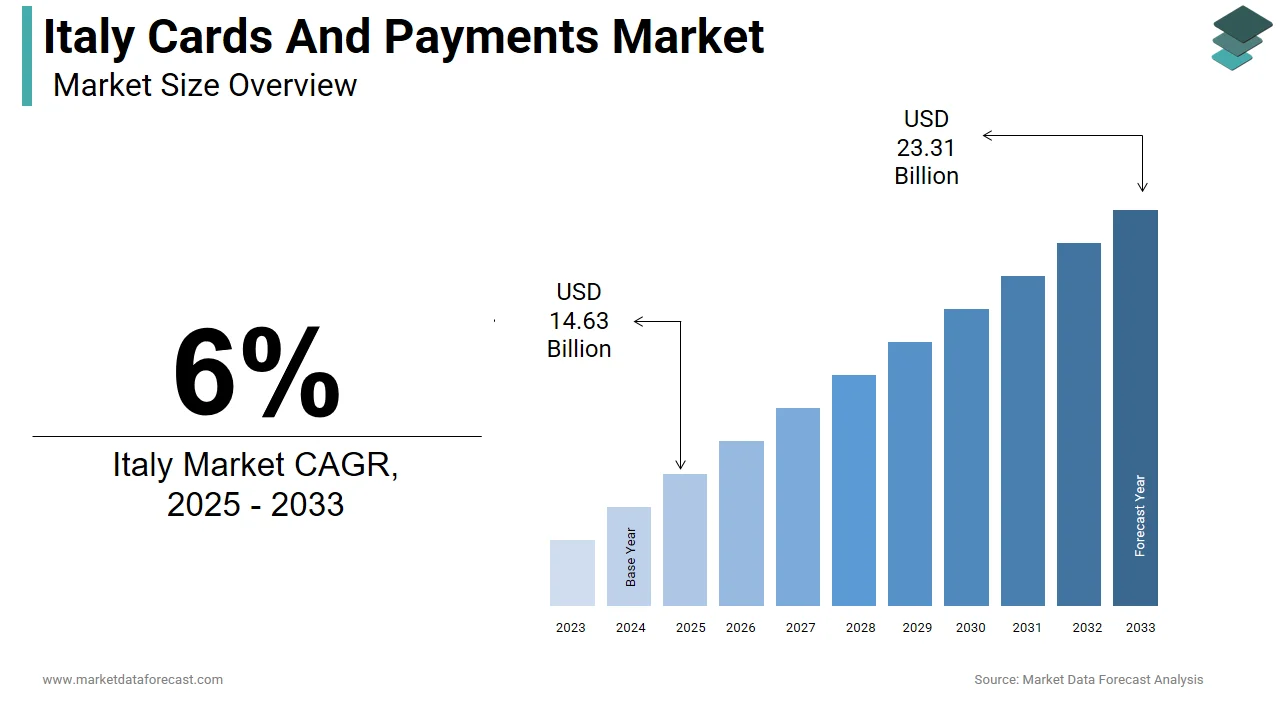

The Italy cards and payments market size was valued at USD 13.80 billion in 2024. This market is expected to grow at a CAGR of 6% from 2025 to 2033 and be worth USD 23.31 billion by 2033 from USD 14.63 billion in 2025.

MARKET DRIVERS

Accelerated Shift toward Digital Payments in the Post-Pandemic Era

One of the primary drivers of Italy’s cards and payments market is the accelerated shift toward digital payment methods following the pandemic, as consumer behavior evolved toward contactless and online transactions. According to Banca d'Italia (Bank of Italy), in 2023, card-based transactions increased significantly compared to the previous year, reaching a total value of approximately €1.6 trillion. Contactless card usage surged, with a notable share of point-of-sale (POS) transactions under €50 conducted via contactless methods, up from just 35% in 2019. Apart from these, mobile wallet adoption through platforms such as Apple Pay, Google Pay, and local solutions like Satispay grew significantly. These trends reflect a broader cultural shift toward convenience-driven financial behavior, supported by strong telecom infrastructure and government incentives encouraging digital transactions.

Government-Led Initiatives to Promote Financial Inclusion and Cashless Transactions

Another key driver of Italy's cards and payments market is the government’s proactive push for financial inclusion and digital transformation through targeted policies and incentives. The Italian Ministry of Economy and Finance introduced the "Cashback Italia" program in 2021, which rewarded consumers for making digital transactions, leading to a significant spike in card usage. Although the initiative was phased out in 2023, it had already contributed to a structural change in consumer habits, increasing digital payment adoption. Also, the introduction of PagoPA, the national digital payment system for public services, has expanded access to secure electronic payments across all regions.

MARKET RESTRAINTS

Persistent Preference for Cash among Older Generations and SMEs

A major restraint on Italy’s cards and payments market is the continued dominance of cash-based transactions among older generations and small-to-medium enterprises (SMEs). According to a 2023 survey by SWG Research Institute, a significant portion of individuals aged 65 and above used cash for a notable share of their daily purchases, citing concerns about security, lack of trust in digital systems, and ease of budgeting. Similarly, Confcommercio reported that only a limited percentage of SMEs accepted non-cash payments regularly, largely due to high transaction fees and limited technical know-how. Banca d'Italia noted that in 2023, cash-in-circulation still accounted for approximately 48% of total retail transactions by volume. This behavioral inertia slows down the transition to a fully digitized payment ecosystem and requires targeted education campaigns and cost-reduction strategies to encourage broader adoption.

Fragmentation and Limited Interoperability across Payment Platforms

Another key constraint in Italy's cards and payments market is the fragmentation of payment platforms, which limits interoperability and creates inefficiencies in the digital payment landscape. Unlike unified systems seen in countries like Sweden or Singapore, Italy hosts a wide array of competing mobile and QR code-based payment solutions, including Satispay, Nexi, PayPal, and various bank-specific apps. According to a 2023 report by McKinsey & Company, there were over 25 active digital payment providers operating in Italy, leading to duplication of infrastructure and reduced economies of scale. Without greater collaboration between providers or regulatory intervention to standardize payment protocols, this fragmentation may continue to hinder the seamless expansion of Italy’s digital payment ecosystem.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services in E-Commerce and Retail

A growing opportunity in Italy’s cards and payments market is the rapid expansion of Buy Now, Pay Later (BNPL) services, particularly within the e-commerce and retail sectors. Data from the Italian Banking Association (ABI) indicates that BNPL transaction value reached €6.8 billion in 2023, reflecting a 35% annual increase. As regulatory frameworks evolve to accommodate BNPL while ensuring consumer protection, this segment is poised to become a mainstream alternative to traditional credit cards, offering substantial revenue opportunities for payment providers.

Rise of Super App Ecosystems Integrating Financial and Payment Services

The emergence of super app ecosystems presents a transformative opportunity for Italy’s cards and payments market, allowing non-financial platforms from ride-hailing apps to entertainment services to integrate payment and credit services directly into their interfaces. Satispay, Nexi, and Revolut have been leading this trend, offering comprehensive financial ecosystems that serve millions of users daily. Satispay reported processing over €8 billion in transaction value in 2023, reflecting a 40% annual increase. These super apps are not only enhancing financial inclusion but also driving card-linked payments, QR code transactions, and peer-to-peer transfers.

MARKET CHALLENGES

Increasing Sophistication of Financial Fraud and Identity Theft

Despite Italy’s advanced digital payment infrastructure, the sector faces a growing challenge from increasingly sophisticated financial fraud and identity theft schemes. According to the Italian Postal Police Department, reports of online payment fraud increased by 32% in 2023 compared to the previous year, with total losses surpassing €1.1 billion. Phishing attacks, fake merchant sites, and synthetic identity fraud have become more prevalent, exploiting weaknesses in multi-factor authentication and consumer awareness. Banca d'Italia highlighted in its 2023 annual report that card-not-present (CNP) fraud accounted for over 63% of all digital payment fraud cases. Although major banks like Intesa Sanpaolo and UniCredit have implemented AI-based fraud detection systems, many consumers, especially seniors, are still vulnerable to social engineering tactics.

Regulatory Complexity and Compliance Burden for Fintech Startups

While Italy maintains a progressive regulatory framework for digital finance, emerging fintech startups face challenges related to regulatory complexity and compliance costs. The implementation of PSD2, along with stringent anti-money laundering (AML) and know-your-customer (KYC) requirements, has increased operational burdens for new entrants. Startups also face ongoing reporting obligations and capital adequacy rules that can hinder agility and speed to market. While regulation ensures financial stability and consumer protection, streamlining oversight and improving dialogue between regulators and innovators could help accelerate the development of next-generation payment solutions in Italy.

MARKET KEY HIGHLIGHTS

The emergence of digital-only banks in Italy, like the German-based mobile-only bank N26, allows consumers to do complete banking transactions on their mobile phones. Hello Bank! by Banca Nazionale del Lavoro (BNL), and UniCredit Bank's mobile-only buddybank with services like current accounts, credit and debit cards, personal loans, and 24/7 personal assistance.

The advent of foreign payment service providers in alternative payments such as Apple Pay, Seqr mobile payment app by Sweden's Seamless, US's Boku acquisition of mobile view Italia, and the partnership of Vodafone and PayPal allowing contactless payments for the customers by linking their accounts to Vodafone wallet is pushing the local payments markets.

Government initiatives to promote cashless and electronic transactions, like the No Cash Day Project and National project in association with Maestro, Mastercard, Visa, UBI Banca, Bancomat Consortium, and Banco Popolare. The daily and monthly coupons offered on the transactions resulted in making Bergamo a cashless city by adopting electronic payments.

KEY MARKET PLAYERS

Top players in the Norway cards and payments market include

- BancoPosta

- Poste Italiane

- Banca Nazionale del Lavoro

- Intesa Sanpaolo

- UniCredit Bank

MARKET SEGMENTATION

This research report on the Italy cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Italy cards and payments market?

The Italy cards and payments market exceeds USD 14.63 billion, with debit cards leading amid rising digital adoption.

2. What drives growth in the Italy cards and payments market?

E-commerce surge and contactless mandates propel the Italy cards and payments market toward cashless retail.

3. What are key trends in the Italy cards and payments market?

Contactless hits 70% of transactions in the Italy cards and payments market, boosting debit and wallet use.

4. How dominant are debit cards in the Italy cards and payments market?

Debit via Bancomat leads the Italy cards and payments market at 80% volume for everyday spending.

5. What role do credit cards play in the Italy cards and payments market?

Credit cards grow in travel and online buys within the Italy cards and payments market via rewards.

6. How common are contactless payments in the Italy cards and payments market?

Contactless dominates low-value payments in the Italy cards and payments market at NFC-enabled POS.

7. How does e-commerce impact the Italy cards and payments market?

Online retail drives secure card use in the Italy cards and payments market with 3D Secure.

8. What opportunities exist in the Italy cards and payments market?

Satispay and BNPL expand reach in the Italy cards and payments market for SMEs.

9. Who leads the Italy cards and payments market?

Unicredit, Intesa Sanpaolo dominate the Italy cards and payments market issuer shares.

10. What regulations shape the Italy cards and payments market?

PSD2 and cash caps accelerate digitization in the Italy cards and payments market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com