Japan Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Transaction Value, Volumes, Historical Trends, Industry Analysis From 2025 to 2033

Japan Cards and Payments Market Size

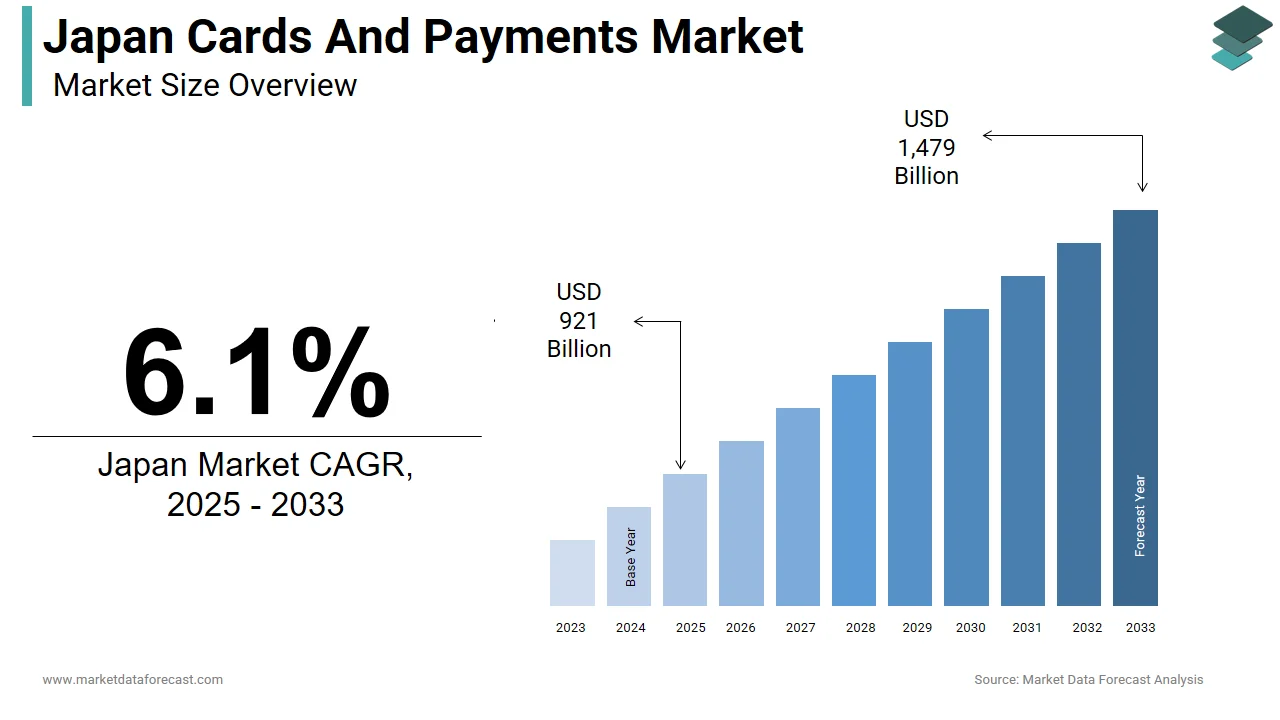

The Japan cards and payments market size was valued at USD 868 billion in 2024. This market is expected to grow at a CAGR of 6.1% from 2025 to 2033 and be worth USD 1,479 billion by 2033 from USD 921 billion in 2025.

MARKET DRIVERS

Rise in Contactless and Digital Payment Adoption

The adoption of contactless payments has surged in Japan, especially post-pandemic, driven by consumer preference for safer, faster, and more convenient payment methods. In 2023, contactless card transactions accounted for over 55% of all face-to-face card payments in Japan, according to the Bank of Japan. A major catalyst for this shift was the government's push through initiatives like "Goto Campaigns" and subsidies for cashless transactions, which encouraged both merchants and consumers to adopt digital tools. Furthermore, the number of contactless POS terminals increased by 40% between 2021 and 2023, which is reaching approximately 6.8 million units nationwide, as reported by Japan’s Ministry of Economy, Trade and Industry (METI). This trend is further reinforced by younger generations who are more tech-savvy and prefer frictionless payment experiences. Financial institutions are also launching innovative credit and debit card products with embedded rewards and loyalty programs, which is boosting market growth.

Regulatory Support and Financial Inclusion Initiatives

Japan’s regulatory environment has become increasingly supportive of electronic payments, aiming to reduce reliance on cash and promote financial inclusion. The Financial Services Agency (FSA) has introduced several reforms, including easing regulations around fintech startups and encouraging collaboration between banks and non-bank players. These policies have led to the rise of neobanks and alternative payment platforms that serve underbanked populations in rural areas where traditional banking penetration is low. Moreover, the FSA has mandated enhanced cybersecurity frameworks and data protection laws, increasing consumer trust in digital transactions. These measures have significantly contributed to the rising demand for card-based payment systems by improving the safety net for users.

MARKET RESTRAINTS

Persistent Preference for Cash Transactions

Despite significant advancements in the card and payments ecosystem, Japan remains one of the most cash-reliant societies globally. This deeply ingrained cultural habit is a major restraint on the growth of card and digital payment systems. Multiple factors contribute to this behavior, including an aging population that prefers physical currency, concerns about fraud and privacy, and a lack of awareness about digital alternatives among older demographics. Additionally, small businesses remain hesitant to adopt digital payment infrastructure due to perceived high costs and complexity. Efforts to change this behavior require sustained public education campaigns and incentives, but progress remains gradual, which is posing a continued challenge.

Fragmentation in Payment Systems and Lack of Interoperability

The Japanese payments landscape is highly fragmented, with multiple proprietary systems operating independently, ranging from Suica and Pasmo cards to PayPay, LINE Pay, and Rakuten Pay. As of 2023, there were over 150 different mobile and card-based payment services active in Japan, many operated by regional banks, telecom companies, or e-commerce firms. However, only 12% of these platforms support cross-service compatibility, according to a McKinsey report. Consumers often maintain multiple apps and cards to cover different spending needs, by reduces convenience and discourages deeper engagement with digital finance.

Interoperability challenges are further exacerbated by technical standards disparities and limited data-sharing agreements between service providers. For instance, QR code-based payment systems used by different banks do not always work across platforms, which is creating confusion for users and merchants alike.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

The BNPL sector is emerging as a transformative opportunity in Japan, tapping into a growing appetite for flexible financing solutions among younger and digitally savvy consumers. This growth is fueled by partnerships between fintechs and major retailers to offer interest-free installment plans. Younger consumers, particularly those aged 20–35, account for nearly 60% of BNPL users, as they seek alternatives to traditional credit cards due to lower credit limits or aversion to debt. Additionally, BNPL allows unbanked or underbanked individuals to build a credit profile via responsible repayment behavior.

Integration of AI and Blockchain in Payment Fraud Detection

Japan’s financial institutions are investing heavily in AI and blockchain technologies to secure payment systems and enhance trust as cyberattacks and digital fraud become increasingly sophisticated. Blockchain technology is being tested by several banks and fintech firms for real-time transaction verification and identity management. These innovations are attracting global attention. Japan is poised to strengthen its digital payments infrastructure by unlocking new growth potential in both domestic and international markets.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

As digital payments expand, so too does the risk of cybercrime, making cybersecurity a critical challenge for Japan’s cards and payments market. In particular, phishing attacks and malware targeting mobile payment apps saw a significant uptick, affecting over 1.2 million users. One notable breach in early 2023 compromised data belonging to 400,000 users of a major mobile wallet provider, leading to temporary service suspensions and reputational damage. Consumer trust remains fragile, where a 2023 survey by the Nomura Research Institute found that 43% of respondents were concerned about data theft when using digital payment methods, and 31% had stopped using certain services due to privacy fears. The challenge lies in balancing innovation with robust security to maintain user confidence and ensure sustainable market growth.

High Entry Barriers for Foreign Fintech Companies

Foreign fintech firms face significant entry barriers when attempting to operate in Japan’s cards and payments market, which is limiting international competition and innovation. Japan’s regulatory framework, while modernizing, remains complex and requires extensive localization, including adherence to strict licensing requirements set by the Financial Services Agency (FSA). Moreover, Japan’s language barrier, conservative business culture, and entrenched domestic players make market penetration difficult. Even global giants like Stripe and Adyen have faced slow adoption due to reluctance from Japanese merchants accustomed to domestic payment processors.

Banks also dominate customer relationships by leaving little room for neobanks or alternative payment providers to scale quickly. These structural and regulatory hurdles create a challenging environment for foreign entrants, which is potentially stifling the pace of digital transformation in the sector.

MARKET KEY HIGHLIGHTS

The idea of the use of advanced technologies like visible light palm authentication biometric process by companies like JCB in partnership with Universal Robot and the National Institute of Advanced Industrial Science and Technology with the help of a smartphone to capture the patterns of palm and store in the server to match during the transactions and return the results.

The increasing prominence of alternative payments in the Japanese market, like QuickPass, launched by UnionPay and Sumitomo Mitsui Card company, allows customers to pay at almost 100 merchants in Tokyu Plaza Ginza by tapping. Other alternative methods include Android Pay of Google, introduced in partnership with Japan's Rakuten Edy, and Apple Pay, providing contactless payment solutions with cards stored in their wallet.

New products by payment solution providers with more security features, like replacing PIN with fingerprint authentication in the F-Code Payment card developed by JCB and France-based IDEMIA, and the upcoming Sumitomo Mitsui and US-based Dynamics company's partnered credit card with locking ability, along with touch-activated buttons, LCD, and LED lights.

KEY MARKET PLAYERS

Top players in the Norway cards and payments market include

- Japan Post Bank

- Sumitomo Mitsui Financial Group

- Mizuho Financial Group

- Mitsubishi UFJ Financial Group

- Resona Holdings

- Rakuten

- Credit Saison

- Aeon Credit Service

- JCB

MARKET SEGMENTATION

This research report on the Japan cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Japan cards and payments market?

The Japan cards and payments market reached USD 921 billion in 2025, with cards holding a 90% share amid a steady digital shift.

2. What drives growth in the Japan cards and payments market?

Declining cash use and contactless adoption propel the Japan cards and payments market, boosted by government subsidies.

3. What are key trends in the Japan cards and payments market?

Contactless transactions exceed 55% in the Japan cards and payments market, alongside QR codes reducing cash reliance.

4. What role do contact smart cards play in the Japan cards and payments market?

Contact smart cards lead at 54% in the Japanese cards and payments market, favored for secure retail and transit use.

5. How is e-commerce impacting the Japan cards and payments market?

E-commerce surges demand for cards and wallets in the Japan cards and payments market, enhancing cross-border options.

6. What is the outlook for the Japan cards and payments market?

The Japan cards and payments market projects a 6.1% CAGR to USD 1,479 billion by 2033 via digital modernization.

7. Who are main players in the Japan cards and payments market?

Credit Saison, Rakuten Card, and Sumitomo Mitsui lead the Japan cards and payments market with 50% top-5 share.

8. What opportunities exist in the Japan cards and payments market?

QR codes and biometric auth offer growth in the Japan cards and payments market for merchants and fintechs.

9. How does regulation affect the Japan cards and payments market?

Cashless campaigns and new banknotes drive the Japan cards and payments market toward infrastructure upgrades.

10. What is debit card usage like in the Japan cards and payments market?

Debit cards aid spending control in the Japan cards and payments market, growing with contactless integration.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com