Netherlands Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Transaction Value, Volumes, Historical Trends, Industry Analysis From 2025 to 2033

Netherlands Cards And Payments Market Size

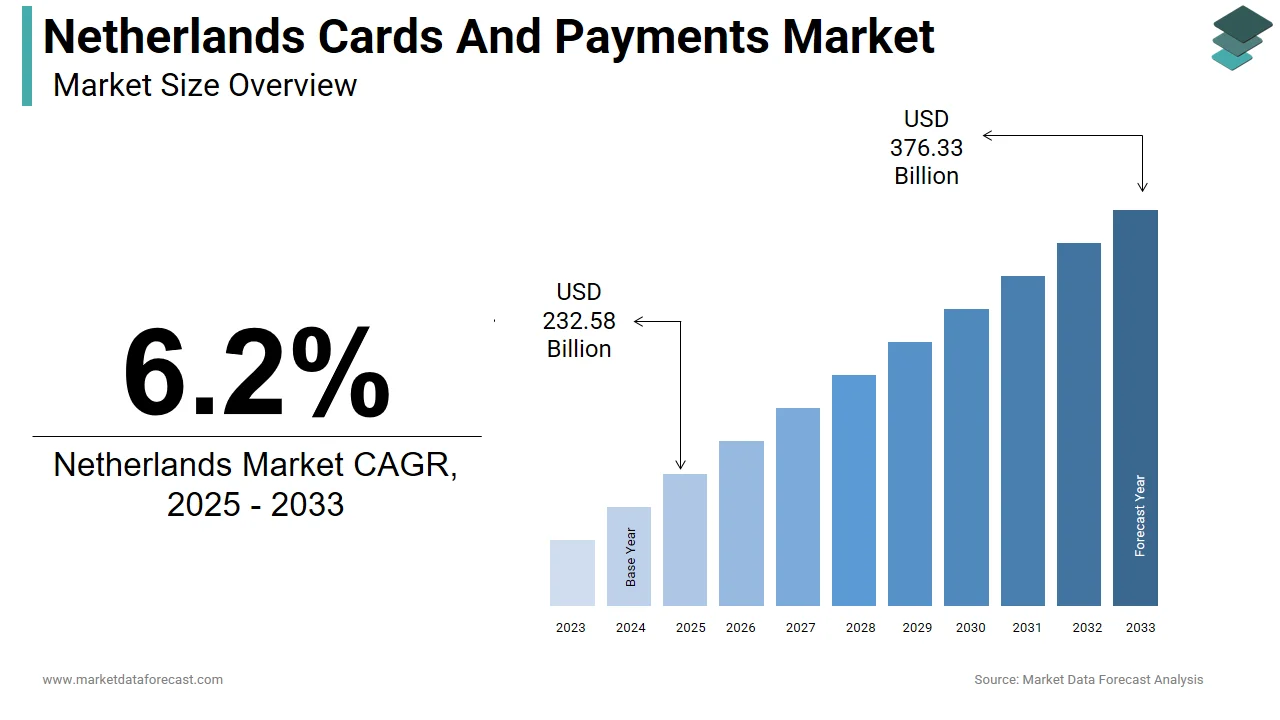

The Netherlands cards and payments market size was valued at USD 219 billion in 2024. This market is expected to grow at a CAGR of 6.2% from 2025 to 2033 and be worth USD 376.33 billion by 2033 from USD 232.58 billion in 2025.

MARKET DRIVERS

High Digital Penetration and Mobile Payment Adoption

The Netherlands has one of the most digitally advanced economies in Europe, with widespread internet access and high smartphone adoption driving a shift toward digital payments. According to a study, 98% of households had internet access, and over 94% of adults owned a smartphone, creating an ideal environment for contactless and mobile wallet transactions. Data from De Nederlandsche Bank (DNB) shows that in 2023, contactless card payments accounted for 67% of all face-to-face card transactions, with a total value exceeding EUR 95 billion, marking a year-on-year growth of 14%. The popularity of mobile wallets such as Apple Pay, Google Pay, and iDEAL-linked cards has further accelerated this trend. In addition, the country's robust financial infrastructure and early adoption of PSD2 and Open Banking standards have enabled fintechs like Bunq, N26, and ING to offer innovative card-linked services, including real-time spending analytics and instant virtual card issuance.

Expansion of E-commerce and Online Spending Growth

E-commerce is a key driver fueling demand for card-based and digital payment solutions in the Netherlands. In the Netherlands, online retail sales reached EUR 42.6 billion in 2023, accounting for over 18% of total retail sales, up from 12% in 2019, indicating a structural shift toward digital commerce. This surge in online shopping has directly boosted the usage of debit and credit cards, which remain the most preferred payment method for digital purchases. In the Netherlands, card payments accounted for a significant portion of all online transactions, with credit card usage rising notably each year. Major platforms like Bol.com, Coolblue, Zalando, and Amazon Netherlands have integrated multiple card payment gateways, enhancing user experience and driving transaction volumes. Also, Visa Europe’s 2023 Payment Insights Report highlighted that contactless online card payments grew by 28% in the Netherlands, reflecting growing consumer preference for convenience and speed. As cross-border e-commerce expands, particularly within the EU, the demand for multi-currency and secure card acceptance continues to rise, reinforcing the momentum of the Netherlands’ evolving payments landscape.

MARKET RESTRAINTS

Declining Use of Physical Cards Due to Embedded Finance and Super Apps

Despite high digital payment adoption, the traditional card issuance model in the Netherlands is facing a decline due to the rise of embedded finance and super apps that integrate payment functionalities directly into non-financial platforms. Consumers are increasingly opting for seamless in-app payment experiences rather than carrying or using physical cards. According to a report, the Netherlands experienced a drop in new card issuance in 2023 compared to the previous year, primarily attributed to the growing popularity of tokenized and app-based payment methods. Major platforms such as Uber, Spotify, and PayPal now offer direct payment integrations without requiring users to input card details repeatedly. Various reports and studies revealed that a significant portion of millennials and Gen Z consumers rarely use their physical debit cards, preferring to transact via mobile wallets or embedded financial tools. Banks are also reporting lower card activation rates. For instance, ING Netherlands noted in Q4 2023 that only 77% of newly issued cards were activated within the first month, down from 90% in 2021. This shift poses a challenge for traditional card networks and issuing banks, which may see reduced interchange fee revenues and declining customer engagement unless they adapt to this evolving payment behavior.

Regulatory Complexity and Compliance Burden for Fintechs and New Entrants

The Netherlands' financial sector operates under a stringent regulatory framework shaped by both national policies and EU-wide directives such as PSD2 (Revised Payment Services Directive) and GDPR (General Data Protection Regulation). While these regulations aim to enhance transparency and consumer protection, they also impose significant compliance burdens on fintech firms and new entrants. In addition, the implementation of Open Banking regulations has increased liability for fraud and required additional layers of authentication, sometimes slowing transaction speeds and affecting user experience. A report by the Dutch Banking Association (NVB) found that smaller payment service providers faced an average compliance cost increase of 14% post-PSD2, limiting their ability to compete with larger players.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

The Netherlands presents a growing opportunity for Buy Now, Pay Later (BNPL) services, driven by increasing consumer demand for flexible payment options and a young, digitally engaged population. BNPL allows shoppers to split purchases into interest-free installments, aligning with the financial preferences of millennials and Gen Z. Major international players such as Klarna, Afterpay, and Scalapay, along with domestic fintechs like Mollie and Bunq have expanded rapidly, integrating seamlessly into major e-commerce platforms including Bol.com, Zalando, and Coolblue. According to Mastercard’s 2023 Benelux Fintech Outlook, more than 45% of Dutch retailers now offer BNPL as a payment option, reflecting increasing merchant acceptance. Banks and card issuers can leverage this trend by embedding installment features into existing card products, thereby enhancing customer engagement and boosting transaction volumes while meeting evolving consumer finance demands.

Rise of Real-Time Payments and Interoperable Card Solutions

The Netherlands’ real-time payments infrastructure, powered by the iDEAL system, has created a fertile ground for innovation in card-based and hybrid payment solutions. According to Payments Association Netherlands (PIN), iDEAL is the most popular payment method for online purchases in the Netherlands, and its transaction volume is significant. While iDEAL dominates peer-to-peer (P2P) and merchant transfers, banks and fintechs are leveraging its infrastructure to develop iDEAL-linked virtual cards, QR-based contactless cards, and interoperable card solutions that work seamlessly across both online and offline environments. Major banks such as Rabobank, ING, and ABN AMRO have launched real-time card issuance and instant activation features, enabling users to generate virtual cards via mobile apps for immediate use. Moreover, EMVCo and international card networks like Visa and Mastercard are collaborating with Dutch payment processors to introduce tokenized card transactions and QR interoperability, allowing greater flexibility and convenience for consumers and merchants alike.

MARKET CHALLENGES

Rising Cybersecurity Threats and Payment Fraud Incidents

As the Netherlands accelerates its transition toward a fully digital payments ecosystem, it faces growing cybersecurity threats and fraud incidents that undermine consumer trust and operational efficiency. According to the National Cyber Security Centre of the Netherlands (NCSC-NL), in 2023, there were significant cybercrime incidents, with online payment fraud accounting for a notable share of these cases. Card-not-present (CNP) fraud remains a critical concern, particularly with the rise in e-commerce transactions. The Dutch Central Bank (DNB) reported that in 2023, CNP fraud losses totaled EUR 210 million, representing a year-on-year increase of 17%. Phishing scams, malware attacks, and data breaches have contributed to declining consumer confidence in digital payments, especially among older users. Furthermore, Europol’s Internet Organised Crime Threat Assessment (IOCTA) identified the Netherlands as a key node in transnational cybercrime, often exploited due to its high-value financial infrastructure and dense digital economy.

To mitigate risks, financial institutions must invest in advanced fraud detection technologies such as AI-driven analytics, biometric verification, and end-to-end encryption, which could increase operational costs and impact transaction speed. Balancing robust security with seamless user experience remains a key challenge as the Netherlands continues to evolve its digital payments landscape.

Uneven Adoption across Generational and Demographic Segments

Despite the Netherlands' reputation as a technologically advanced financial hub, there remains a notable disparity in digital payment adoption across different age groups, posing a structural challenge to the cards and payments market. While younger generations embrace mobile payments and card usage, older demographics continue to rely on cash and traditional banking methods. According to a study by Statistics Netherlands (CBS), nearly 91% of users aged 18–34 used digital payment apps weekly, compared to only 35% of those aged 65 and above. Similarly, almost 48% of seniors in the Netherlands still preferred using cash for daily transactions, citing concerns about security and unfamiliarity with digital tools. This generational gap affects both consumers and merchants. Many small businesses serving older customers continue to accept only cash. Addressing this divide requires targeted financial literacy campaigns, improved accessibility in digital interfaces, and incentives for merchants to adopt inclusive payment systems.

MARKET KEY HIGHLIGHTS

The development of infrastructure for real-time instant payments by the Dutch Payment Association to provide instant fund transfers within five seconds with no amount limit by integrating with all major banks in the Netherlands, which is scheduled to be ready by May 2018.

The demand growth for alternative payment solutions forced the banking and payment service providers to launch new products like the mobile wallet by de Volksbank offering NFC-based mobile payments at POS terminals, the wallet by G+D Mobile Security, supporting payments of both Visa and Mastercard debit cards of the bank, ABN Amro's digital ABN wallet, Seqr by Swedish m-payment solution provider Seamless, and the ING mobile wallet by ING Bank.

The growing adoption of contactless payments, which increased by five times from 2015 to 2016, with almost two-thirds of all the payment terminals of the Netherlands accepting these payments, and is expected to gain full hold by 2020. Banks like Rabobank have partnered with mobile operator KPN to launch an NFC-based mobile payment option to benefit from this migration.

KEY MARKET PLAYERS

Top players in the Norway cards and payments market include

- ING Bank

- Rabobank

- ABN AMRO

- Deutsche Volksbank

MARKET SEGMENTATION

This research report on the Netherlands cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What drives growth in the Netherlands cards and payments market?

Contactless mandates and iDEAL e-commerce propel the Netherlands cards and payments market toward full digitization.

2. What are key trends in the Netherlands cards and payments market?

iDEAL and contactless dominate the Netherlands cards and payments market, with cash under 10% of transactions.

3. How dominant are debit cards in the Netherlands cards and payments market?

Debit cards via PIN lead the Netherlands cards and payments market for secure everyday retail payments.

4. What role do credit cards play in the Netherlands cards and payments market?

Credit cards support travel/e-commerce in the Netherlands cards and payments market despite debit preference.

5. How common are contactless payments in the Netherlands cards and payments market?

Contactless exceeds 85% of card txns in the Netherlands cards and payments market at NFC POS.

6. How does e-commerce impact the Netherlands cards and payments market?

iDEAL handles 70% online payments in the Netherlands cards and payments market securely.

7. What opportunities exist in the Netherlands cards and payments market?

Neobanks and BNPL expand in the Netherlands cards and payments market for fintech growth.

8. Who leads the Netherlands cards and payments market?

ING, Rabobank, ABN AMRO dominate the Netherlands cards and payments market issuer shares.

9. What regulations shape the Netherlands cards and payments market?

PSD2 accelerates open banking in the Netherlands cards and payments market innovations.

10. How does mobile adoption affect the Netherlands cards and payments market?

Smartphones boost Apple Pay in the Netherlands cards and payments market POS use.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com