Poland Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Transaction Value, Volumes, Historical Trends, Industry Analysis From 2025 to 2033

Poland Cards And Payments Market Size

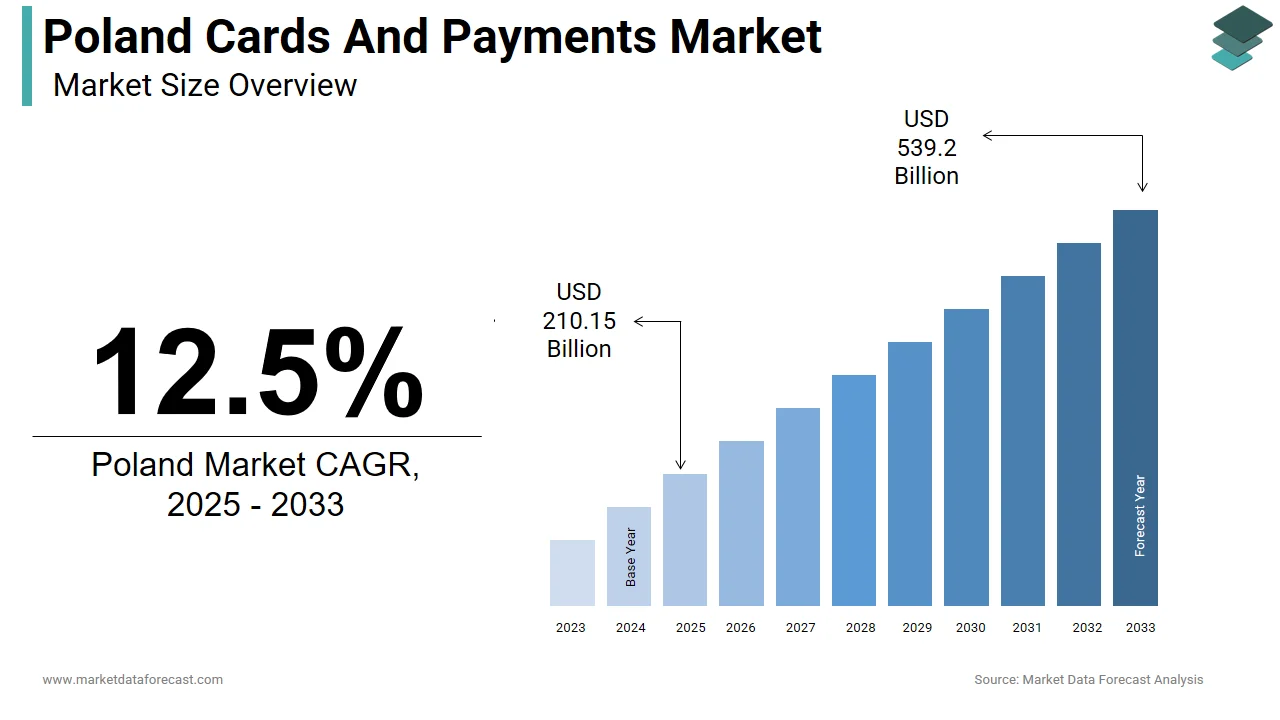

The Poland cards and payments market size was valued at USD 186.8 billion in 2024. This market is expected to grow at a CAGR of 12.5% from 2025 to 2033 and be worth USD 539.2 billion by 2033 from USD 210.15 billion in 2025.

MARKET DRIVERS

Rise in Digital Wallet Adoption and Contactless Payments

Digital wallet usage in Poland has surged, reflecting a shift toward more convenient and secure payment options. Mobile wallets such as Apple Pay, Google Pay, and local platforms like BLIK have gained significant traction among younger consumers. Additionally, the pandemic accelerated consumer preference for touch-free transactions, reinforcing behavioral shifts that continue today. This trend is further reinforced by banks launching co-branded digital wallets and integrating loyalty programs directly into mobile apps by encouraging repeat usage and deeper engagement with electronic payment ecosystems.

Expansion of E-commerce and Online Retail Platforms

E-commerce has become a critical driver for the Poland cards and payments market, fueled by increased internet penetration, improved logistics, and rising consumer confidence in online shopping. This expansion has led to a corresponding rise in card-based and digital payment adoption, particularly among urban consumers. Major international players like PayPal and Stripe have expanded their operations in Poland, offering localized payment gateways that cater to regional preferences. Furthermore, cross-border e-commerce has grown rapidly, with Poles increasingly purchasing goods from global platforms such as Amazon and AliExpress. As consumer trust in online transactions continues to grow, so does reliance on electronic payment instruments, which is making e-commerce a cornerstone of the cards and payments market in Poland.

MARKET RESTRAINTS

Persistent Preference for Cash Among Older Demographics

Despite advancements in digital payments, cash remains dominant in certain segments of the Polish population, especially among older generations. This preference is largely influenced by generational habits and skepticism toward digital security. Around 34% of respondents above the age of 55 expressed concerns about fraud, data breaches, and the complexity of using digital payment tools, as per a study by the Institute for Market Economics (IME) in 2023. Additionally, small businesses and micro-enterprises remain hesitant to adopt digital payment infrastructure due to perceived high costs and limited awareness of available benefits. Efforts to change this behavior require sustained public education campaigns and incentives, but progress remains gradual by posing a continued challenge for the modernization of the Polish payments ecosystem.

Fragmentation in Payment Systems and Limited Interoperability

The Polish payments landscape features multiple competing systems, leading to interoperability challenges that hinder seamless user experiences. While BLIK dominates domestic instant payments, other platforms such as traditional card networks and mobile wallets often operate in silos by creating confusion for both merchants and consumers. According to the Polish Chamber of Electronic Communications (KIE), there are currently eight major digital payment service providers active in Poland, yet only two of them offer full interoperability with external banking systems. This lack of integration limits scalability and discourages wider adoption beyond specific ecosystems. Moreover, QR code-based payment systems used by different banks do not always work across platforms by forcing users to maintain multiple apps for different use cases.

MARKET OPPORTUNITIES

Growth of Buy Now, Pay Later (BNPL) Services

The BNPL sector is emerging as a transformative opportunity in Poland, tapping into a growing appetite for flexible financing solutions among younger and digitally savvy consumers. This growth is driven by partnerships between fintechs and major retailers to offer interest-free installment plans. Companies like Klarna, Afterpay, and local players such as PayPo and Monedo are expanding rapidly, with PayPo alone processing over PLN 8 billion in annual gross merchandise volume by Q4 2023. Younger consumers, particularly those aged 18–35, which account for nearly 70% of BNPL users, as they seek alternatives to traditional credit cards due to high interest rates or lack of access to formal credit. Financial regulators are working closely with industry stakeholders to develop a balanced regulatory framework that encourages innovation while protecting consumers, which is suggesting a favorable policy climate ahead.

Integration of AI and Blockchain in Fraud Detection and Security

The cybersecurity has become a pressing concern is prompting Polish financial institutions to invest heavily in AI-driven analytics and blockchain-based verification systems. Blockchain technology is being tested by several banks and fintech firms for identity verification and transaction traceability. For example, PKO Bank Polski partnered with ConsenSys to pilot a blockchain-based KYC system in 2023, streamlining customer onboarding and reducing fraud risks. These innovations are attracting international attention.

MARKET CHALLENGES

Cybersecurity Threats and Rising Fraud Incidents

As digital payments gain traction in Poland, the risk of cyberattacks and payment fraud has risen sharply. Phishing attacks targeting mobile banking apps affected over 900,000 users during the same period, per a report by Kaspersky Lab. Fintech startups and smaller banks face particular challenges in implementing robust cybersecurity measures due to limited resources and expertise. Many rely on third-party vendors for fraud detection, which can lead to vulnerabilities if not properly managed. To combat this, the KNF issued updated cybersecurity guidelines in late 2023, mandating stronger authentication protocols and real-time fraud monitoring systems. However, enforcement remains inconsistent, and awareness among end-users remains low, which is posing ongoing threats to the market’s integrity.

Regulatory Complexity and Compliance Burdens

The Polish payments market operates within a complex regulatory environment, which poses challenges for fintechs and traditional financial institutions alike. Although Poland has adopted EU directives on payment services (PSD2), implementation at the national level has introduced additional layers of oversight and compliance requirements. The Polish Financial Supervision Authority (KNF) oversees banking institutions, while the Ministry of Digitization regulates non-bank payment service providers, creating overlapping jurisdictions. Furthermore, licensing timelines for fintech firms remain lengthy, averaging 10–14 months, which is deterring foreign investment and slowing product launches. Interoperability issues also persist QR code-based payment systems such as BLIK and those offered by private banks often do not work seamlessly across platforms by causing confusion for users and merchants alike.

MARKET KEY HIGHLIGHTS

The extensive spread of contactless technologies in the country with the support from all major banks like PKO Bank Polski, mBank, Bank Zachodni WBK, and Bank Pekao favored the rapid adoption of contactless POS terminals at retailer outlets.

The adoption of new technologies by payment solution providers led to the introduction of m-payment services like Blik, formed by the Polish Payment Standard, a company set up by six Polish banks: Alior Bank, Millennium Bank, Bank Zachodni WBK, mBank, ING Bank ÅšlÄ…ski, and PKO Bank Polski allows mobile payments for in-store and online, and peer-to-peer (P2P) transfers, and Android Pay by Google supported by Alior Bank, Bank Zachodni WBK, and T-Mobile Banking Services.

The benefits of several alternative payments like Visa Checkout, which stores users’ payment and shipping details and provides faster checkout, One Touch instant checkout by PayPal allowing customers to skip login in eligible websites, and MasterCard's Masterpass, allowing customers to shop online using pre-registered credit or debit cards.

KEY PARTICIPANTS IN THE MARKET

The major players in the Poland cards and payments market include

- PKO Bank Polski

- mBank

- Bank Pekao

- Santander

- ING Bank

- Credit Agricole

MARKET SEGMENTATION

This research report on the Poland cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Poland cards and payments market?

The Poland cards and payments market reached USD 210.15 billion in 2025, projected to hit USD 539.2 billion by 2033.

2. What drives growth in the Poland cards and payments market?

BLIK expansion and e-commerce propel the Poland cards and payments market at a 12.5% CAGR. Non-card payments grow 50% faster than cards.

3. Who are key players in the Poland cards and payments market?

Leaders in the Poland cards and payments market include PKO Bank Polski, Santander, Visa, Mastercard, and BLIK operators.

4. What is the CAGR of the Poland cards and payments market?

The Poland cards and payments market forecasts a 12.5% CAGR through 2033, fueled by digital wallets and contactless adoption.

5. Which payment types dominate the Poland cards and payments market?

Payment cards lead at 65% of transactions in the Poland cards and payments market, with 10 billion POS/online volumes.

6. What is BLIK in the Poland cards and payments market?

BLIK mobile wallet drives growth in the Poland cards and payments market, contributing most to non-card expansion.

7. How does e-commerce impact the Poland cards and payments market?

E-commerce boosts digital payments in the Poland cards and payments market via BLIK and card gateways.

8. What trends shape the Poland cards and payments market?

Contactless and biometric like HandGo trend in the Poland cards and payments market for seamless transactions.

9. Are debit cards key in the Poland cards and payments market?

Debit dominates volume in the Poland cards and payments market amid high per capita transactions at 420.

10. What opportunities exist in the Poland cards and payments market?

BNPL and biometric payments offer opportunities in the Poland cards and payments market expansion.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com