- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

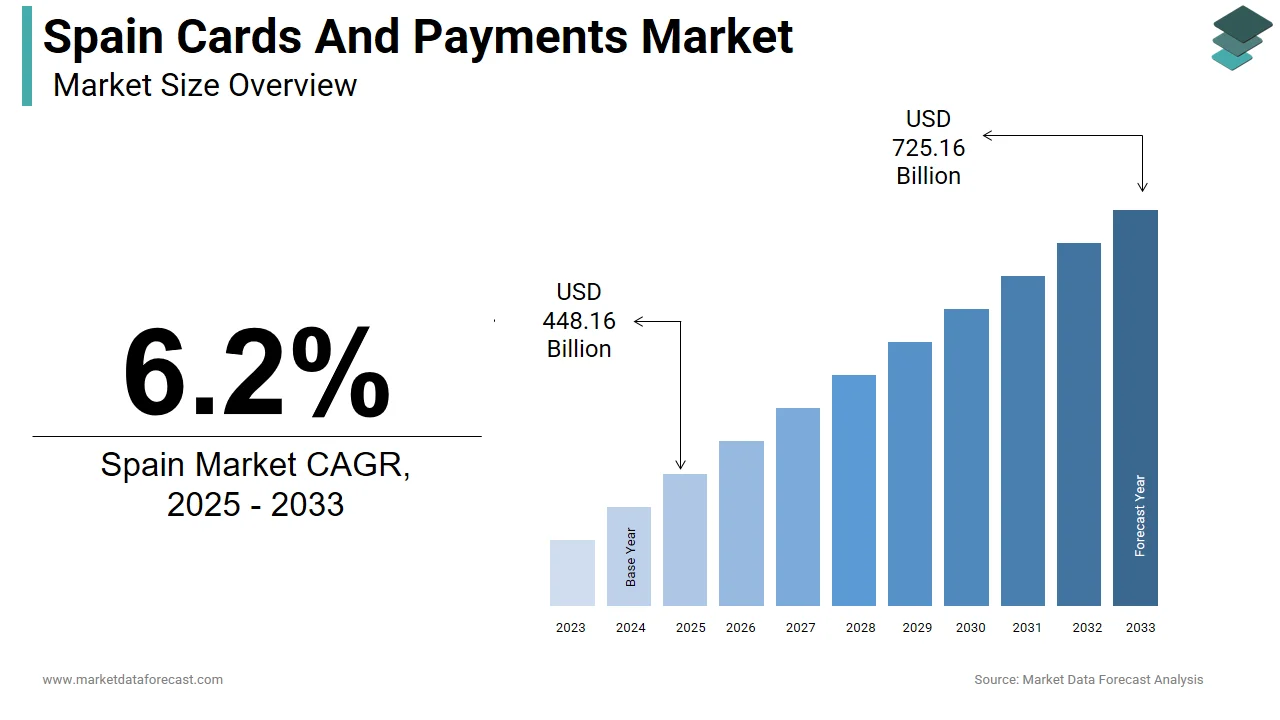

Spain Cards And Payments Market Size

The Spain cards and payments market size was valued at USD 422 billion in 2024. This market is expected to grow at a CAGR of 6.2% from 2025 to 2033 and be worth USD 725.16 billion by 2033 from USD 448.16 billion in 2025.

MARKET DRIVERS

Rapid Growth in E-commerce and Digital Transactions

Spain’s cards and payments market is being significantly driven by the rapid expansion of its e-commerce sector, which has intensified demand for secure and convenient digital payment methods. This surge in online shopping has directly increased the use of debit and credit cards as the preferred mode of payment. Data from Redsys, Spain’s leading payment gateway provider, indicates that in 2023, card payments accounted for a significant portion of all online transactions, with international card networks like Visa and Mastercard dominating the space. Additionally, the Bank of Spain reported that contactless card payments grew by 16% year-on-year, with over EUR 28 billion processed via NFC-enabled cards. The rise in mobile commerce (m-commerce) has further boosted this trend. A report by Comscore found that mobile devices accounted for a significant portion of all digital transactions in Spain, reinforcing the need for seamless card integration across platforms.

Government Support for Financial Inclusion and Digital Transformation

The Spanish government has actively promoted financial inclusion and digital transformation through policy reforms and public-private partnerships, contributing to the expansion of the cards and payments market. According to the European Commission’s Digital Economy and Society Index (DESI) 2023, Spain ranked 12th out of 27 EU countries, showing strong progress in digital connectivity and internet usage. The Bank of Spain also reported that over 98% of adults had access to a bank account in 2023, up from 94% in 2018, largely due to targeted financial inclusion programs. Apart from these, the widespread deployment of Point of Sale (POS) terminals which exceeded 2.4 million units nationwide in 2023, according to report has enabled greater acceptance of card-based transactions across small businesses and rural areas.

MARKET RESTRAINTS

High Preference for Cash among Older Generations

Despite Spain's progress toward digitization, a significant portion of the population, particularly older generations, continues to rely on cash for daily transactions, posing a restraint on the cards and payments market. This preference is rooted in familiarity, trust, and concerns about cybersecurity, especially among elderly users who are less comfortable with digital tools. Moreover, small merchants in rural areas often continue to accept only cash, citing high fees or lack of infrastructure for card payments. This ongoing reliance on cash limits the penetration of electronic payment systems and hampers transaction volume growth for traditional card providers, creating a structural challenge in achieving full digital payment adoption across the country.

Regulatory Complexity and Compliance Costs

Spain’s financial sector operates within a complex regulatory framework influenced by both national legislation and EU-wide directives, such as PSD2 (Revised Payment Services Directive) and GDPR (General Data Protection Regulation). While these regulations aim to enhance consumer protection and security, they also impose significant compliance burdens on banks and fintech firms, slowing down innovation and increasing operational costs. According to a Deloitte 2023 FinTech Report, 41% of Spanish fintech startups identified regulatory compliance as a major barrier to scaling their payment solutions, with many facing delays in product launches due to extensive approval processes. Besides, the Bank of Spain reported in 2023 that compliance-related costs for smaller payment institutions had risen notably since the implementation of stricter anti-money laundering (AML) requirements, reducing profit margins and limiting investment in new payment technologies.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

Spain presents a growing opportunity for Buy Now, Pay Later (BNPL) services, driven by shifting consumer preferences and a young, digitally engaged population. BNPL offers flexible payment options that align with the spending habits of millennials and Gen Z, who prioritize convenience and affordability over traditional credit. A survey found that a considerable portion of online shoppers in Spain had used BNPL services at least once, signaling increasing mainstream adoption. International players, along with local fintechs, have expanded their operations in Spain, integrating seamlessly with major e-commerce platforms including Amazon Spain, El Corte Inglés, and Zalando. According to Visa’s 2023 European Fintech Outlook, more than 35% of Spanish retailers now offer BNPL as a payment option, reflecting growing merchant acceptance. Banks and card issuers can leverage this trend by partnering with BNPL providers to embed installment features into existing card products, thereby enhancing customer engagement and boosting transaction volumes while meeting evolving consumer finance demands.

Rise of Embedded Finance and Super App Integration

Embedded finance—where financial services like payments, lending, and insurance are integrated into non-financial platforms—is gaining traction in Spain, offering a transformative opportunity for the cards and payments market. With increasing smartphone adoption and digital service consumption, super apps and platforms are incorporating payment solutions to streamline user experiences. A 2023 report by McKinsey & Company highlighted that Spain was among the fastest-growing markets in Europe for embedded finance, with transaction values surpassing EUR 3.4 billion in 2023. Platforms have introduced in-app payment capabilities, allowing users to transact without switching between banking apps or using physical cards. Also, BBVA and Banco Santander have launched open banking APIs to enable third-party developers to integrate financial services into their applications, accelerating the adoption of card-based payments across ecosystems. According to Openbank’s 2023 Digital Payments Survey, 46% of Spanish consumers prefer making payments through integrated platforms rather than standalone banking apps, emphasizing the shift in user behavior.

MARKET CHALLENGES

Cybersecurity Threats and Rising Fraud Incidents

As Spain accelerates its transition toward a digital-first payments ecosystem, the frequency and sophistication of cyberattacks targeting financial transactions have surged, posing a major challenge to the cards and payments industry. According to Spain’s National Cryptologic Center (CCN), cybercrime incidents increased in recent years, with online payment fraud accounting for a notable portion of all reported cases. Card-not-present (CNP) fraud remains a critical concern, particularly with the rise in e-commerce transactions. Phishing scams, malware attacks, and data breaches have contributed to declining consumer confidence in digital payments, especially among older users. Moreover, Europol’s 2023 Internet Organised Crime Threat Assessment (IOCTA) identified Spain as one of the top five EU countries affected by online payment fraud, with criminals exploiting weak authentication mechanisms and stolen card credentials. To avoid risks, financial institutions must invest in advanced fraud detection technologies such as AI-driven analytics, biometric verification, and tokenization, which could increase operational costs and slow transaction processing speeds.

Uneven Digital Infrastructure across Regions

While urban centers in Spain, such as Madrid and Barcelona, enjoy robust digital infrastructure and high card payment adoption, disparities persist in rural and remote regions, hindering the uniform growth of the cards and payments market. According to Red.es, Spain’s public agency for digital advancement, only 62% of rural municipalities had reliable broadband access in 2023, compared to 98% in major cities. This digital divide affects both consumers and merchants. Many small businesses in rural areas still rely on cash due to limited access to POS terminals or unstable internet connections required for card transactions. A 2023 report by CEPYME (Confederation of Small and Medium Enterprises) found that a significant percentage of micro-enterprises in rural Spain lacked the necessary infrastructure to process card payments, constraining transaction opportunities. On the consumer side, INE (National Institute of Statistics) data shows that digital payment adoption among residents in rural provinces was 21% lower than in metropolitan areas, primarily due to low digital literacy and lack of access to mobile banking services.

MARKET KEY INSIGHTS

The growing alternative payments in the country, like Android Pay, accepted by BBVA, Visa/MasterCard debit or credit card at contactless POS terminals, Alipay offering services in collaboration with BBVA, and Apple Pay and Samsung Pay accepted by Caixa Bank and Banco Santander.

The adoption of Bizum, a real-time common mobile payment platform that offers instant transfers, was launched by 27 Spanish banks that include Bankia, Sabadell, Santander, CaixaBank, BBVA, Popular, CajaSur, Kutxabank, Laboral Kutxa, Bankinter, Evo, BMN, Abanca, BCC, Caja Almendralejo, Ibercaja, Caja Rural Castilla La Mancha, Cajamar Group, Unicaja, Spain Duero, Castilla la Mancha Bank, and Openbank, which facilitates customers with P2P, in-store, and online transactions instantly through their mobile phones.

The physical branches of digital-only banks shift, promoting the electronic payments system in Spain. One such milestone is imaginBank, a mobile-only bank launched by Caixa Bank, providing services like current accounts, credit cards, and consumer loans, managing personal finances and person-to-person (P2P) payments through the mobile app, and the option to view bank balances and recent transactions on Facebook.

KEY MARKET PLAYERS

Top players in the Spain cards and payments market include

- CaixaBank

- BBVA

- Santander

- Bankia

- Banco Sabadell

MARKET SEGMENTATION

This research report on the Spain cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards