Africa Diamond Market Size, Share, Trends, Forecast, Research Report Segmented By Type, Application, and Region (Sudan, Egypt, Kenya, Ethiopia, South Africa, and the rest of Africa) – Regional Industry 2026 to 2034

Africa Diamond Market Size

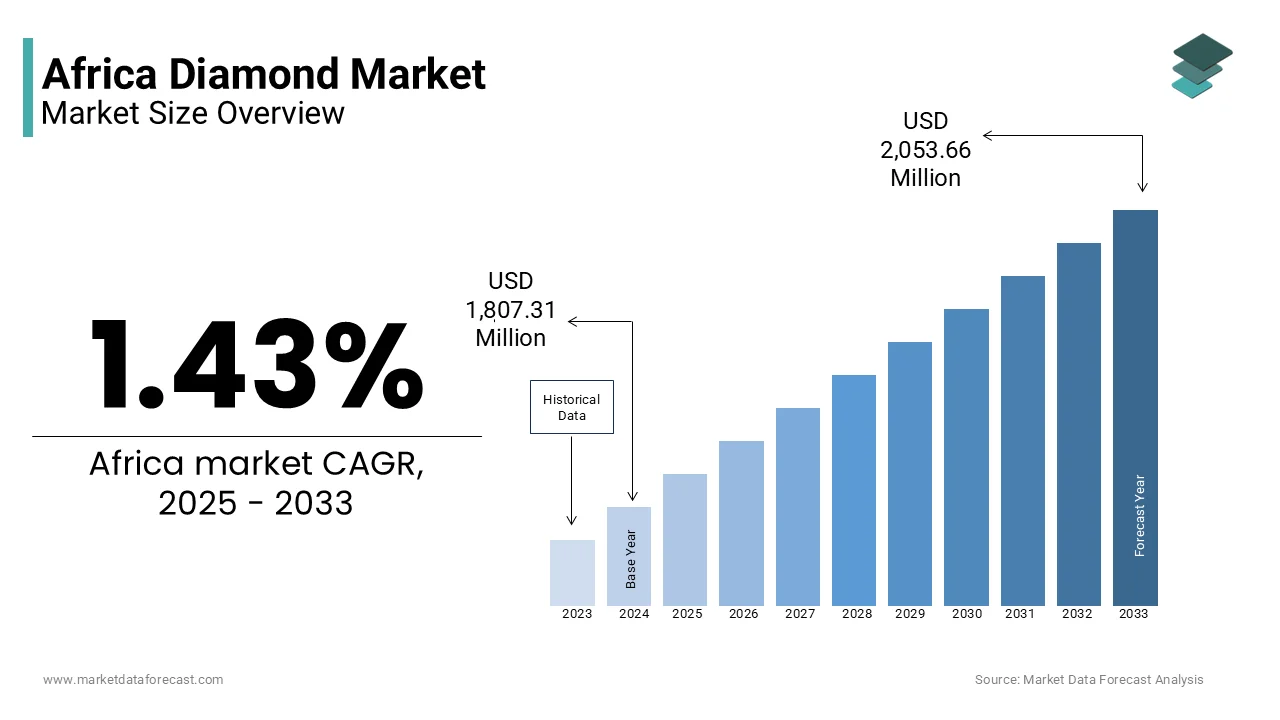

The Africa diamond market size was calculated to be USD 1.83 billion in 2025 and is anticipated to be worth USD 2.08 billion by 2034, from USD 1.86 billion in 2026, growing at a CAGR of 1.43% during the forecast period.

Diamond is one of the most historically significant and economically impactful segments of the global gemstone industry. The region is home to some of the world’s richest diamond reserves, with major production centers in countries such as Botswana, South Africa, Angola, Namibia, and the Democratic Republic of the Congo. These diamonds are primarily extracted through both large-scale industrial operations and smaller artisanal mining activities.

Africa contributes significantly to global diamond supply, with Botswana alone accounting for over a quarter of the world's total diamond production by value. According to the Kimberley Process Certification Scheme, the continent supplied more than 50% of the world’s rough diamonds by volume in recent years. Despite this abundance, the industry has faced persistent challenges related to transparency, ethical sourcing, and economic equity distribution.

As per the African Union, the diamond sector supports millions of livelihoods across the continent, either directly through mining or indirectly via downstream industries such as cutting, polishing, and jewelry manufacturing. In addition, government revenues from diamond exports play a crucial role in national budgets, particularly for resource-dependent economies like Sierra Leone and Angola.

The market has also seen a shift toward traceability and sustainability, driven by increasing consumer awareness and international regulatory pressure. Initiatives like the Kimberley Process have been instrumental in curbing the trade in conflict diamonds, although gaps remain.

MARKET DRIVERS

Global Demand for Ethical and Traceable Diamonds

The growing global preference for ethically sourced and traceable diamonds is one of the key drivers of the Africa diamond market. Consumers, particularly in Western markets, are increasingly demanding transparency regarding the origin of their gemstones. As per the Responsible Jewellery Council, a strong preference among luxury jewelry consumers in North America and Europe prefer diamonds that are certified conflict-free and responsibly mined.

This trend has benefited African producers who adhere to international standards such as the Kimberley Process and the Extractive Industries Transparency Initiative (EITI). Countries like Botswana and Namibia have strengthened their reputations as responsible suppliers, attracting premium pricing and long-term contracts from major diamond buyers including De Beers and Alrosa.

Furthermore, advancements in blockchain technology have enabled greater traceability throughout the supply chain. Initiatives like De Beers' Tracr platform allow for digital tracking of diamonds from mine to retail, reinforcing consumer confidence. This heightened emphasis on ethics and transparency is reshaping the Africa diamond market.

Expansion of Domestic Jewelry Manufacturing and Retail Sectors

The growth of domestic jewelry manufacturing and retail industries, which are creating new avenues for diamond consumption within the continent, is an emerging driver of the Africa diamond market. Traditionally an exporter of raw diamonds, several African countries are now investing in downstream processing to add value before export. Local jewelers in Nigeria, Kenya, and Ghana are capitalizing on rising disposable incomes and a growing middle class that seeks luxury products reflecting cultural identity. This shift is supported by government policies promoting beneficiation—where raw materials are processed domestically rather than exported. Moreover, fashion and entertainment industries across Africa are influencing jewelry trends, integrating traditional motifs with contemporary designs.

MARKET RESTRAINTS

Political Instability and Regulatory Challenges

Political instability remains a critical restraint on the Africa diamond market, particularly in regions where governance structures are weak or prone to disruption. Several diamond-rich nations, including the Central African Republic, the Democratic Republic of the Congo, and parts of Angola, have experienced recurrent civil unrest, corruption, and weak enforcement of mining laws. According to Transparency International’s Corruption Perceptions Index 2023, six out of the ten lowest-ranked countries globally were located in Sub-Saharan Africa.

These conditions create an environment conducive to illegal mining, smuggling, and exploitation, undermining formal market operations. As per the World Bank, informal diamond extraction accounts for up to 20% of total production in certain African countries, depriving governments of tax revenues and distorting official trade data. Apart from these, inconsistent regulatory frameworks and frequent policy shifts deter foreign investment in the sector.

For example, in 2023, Zimbabwe faced renewed sanctions from the European Union due to concerns over human rights violations linked to diamond mining activities. Such geopolitical tensions limit access to international markets and erode consumer confidence in African-sourced diamonds.

Declining Global Rough Diamond Prices

is the sustained decline in global rough diamond prices, which has impacted profitability for producers across the continent, is a significant challenge facing the Africa diamond market. This drop has been attributed to weakened demand from key manufacturing hubs in India and China, coupled with increased supply from alternative sources such as Canada and Russia.

For African diamond exporters, this price erosion translates into reduced revenues and tighter margins. Countries like Botswana and Namibia, which rely heavily on diamond royalties to fund public services, have experienced budgetary shortfalls. As per the International Monetary Fund, Botswana’s diamond-related revenue declined by USD 350 million in fiscal year 2022–2023 due to falling prices and lower sales volumes.

Besides, the rise of lab-grown diamonds has intensified competition, offering synthetic alternatives at significantly lower costs. This dual pressure from declining natural diamond prices and expanding synthetic substitutes presents a formidable challenge to the financial viability of African diamond mining operations.

MARKET OPPORTUNITIES

Growth of Blockchain-Based Diamond Traceability Systems

The adoption of blockchain-based traceability systems that enhance transparency and consumer trust presents one of the most promising opportunities for the Africa diamond market. As global demand for ethically sourced diamonds rises, African producers are leveraging digital innovations to authenticate the provenance of their stones. According to McKinsey & Company, blockchain technology enables real-time tracking of diamonds from extraction to retail, ensuring compliance with international certification standards.

Several African nations have already begun implementing such solutions. For instance, De Beers’ Tracr platform has been deployed in Botswana, allowing for secure digital registration of individual diamonds. Similarly, Namibia has introduced a pilot program using distributed ledger technology to monitor artisanal diamond transactions and prevent illicit trading.

These initiatives not only help combat the trade in conflict diamonds but also improve market access for African producers seeking premium buyers.

Expansion of Artisanal Mining Cooperatives and Community Beneficiation Programs

The expansion of structured artisanal mining cooperatives and community-led beneficiation programs is another significant opportunity for the Africa diamond market. A large portion of diamond production in countries like Sierra Leone, Tanzania, and the Democratic Republic of the Congo occurs through small-scale miners who often operate outside formal regulatory frameworks. According to the International Labour Organization, artisanal diamond mining employs over two million people across Sub-Saharan Africa, yet much of this labour remains informal and undercapitalized.

To address this gap, several governments and NGOs have launched initiatives aimed at formalizing artisanal operations and integrating them into legal supply chains. For example, the Diamond Development Initiative reports that cooperative models in Liberia and Guinea have improved income stability for miners. These groups receive training in safe mining practices, environmental stewardship, and business management, enhancing both productivity and sustainability.

Moreover, beneficiation programs encourage local cutting, polishing, and jewelry manufacturing, allowing African countries to capture greater economic value from their diamond resources. As per the African Union, such initiatives could potentially increase regional value addition by USD 1 billion annually if scaled effectively.

MARKET CHALLENGES

Competition from Lab-Grown Diamonds

The Africa diamond market faces mounting pressure from the rapid proliferation of lab-grown diamonds, which offer a cost-effective and ethically neutral alternative to natural stones. Unlike traditional mining, lab-grown diamonds require no excavation, resulting in lower environmental impact and consistent quality control.

This technological shift has disrupted pricing dynamics and altered consumer preferences, particularly among younger, environmentally conscious buyers. Like, a significant portion of millennials consumers expressed openness to purchasing lab-created diamonds over natural ones, citing affordability and ethical considerations. This shift threatens the competitiveness of African diamond producers, many of whom lack the infrastructure to adapt quickly to changing market demands.

Moreover, synthetic diamond producers in China and India have ramped up output, flooding international markets with affordable options. According to the Rapaport Group, wholesale prices for lab-grown diamonds dropped by 10–15% in 2023, further eroding the price advantage traditionally held by African mines.

Environmental and Social Impact Concerns

Environmental degradation and social displacement linked to diamond mining present significant challenges to the Africa diamond market. Traditional open-pit and alluvial mining methods often result in deforestation, soil erosion, water contamination, and habitat destruction. Also, diamond mining in West and Central Africa has contributed to the loss of over 50,000 hectares of forest land in the past decade, raising concerns among conservationists and regulators.

In addition to ecological damage, mining activities have frequently led to community displacement and labor disputes. These issues have prompted increased scrutiny from international watchdogs and consumers, leading to reputational risks for African diamond producers.

Regulatory bodies and industry stakeholders are responding by enforcing stricter environmental compliance measures. However, compliance costs can be prohibitive for smaller operators, limiting their ability to compete with larger firms that have the resources to implement sustainable practices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 1.43% |

| Segments Covered | By Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, and the rest of Africa |

| Market Leaders Profiled | De Beers Group, Petra Diamonds Limited, Trans Hex, Lucara Diamond, and Gem Diamonds |

SEGMENTAL ANALYSIS

By Type Insights

The natural diamond segment dominated the Africa diamond market by accounting for a substantial portion of total value in 2025. The enduring consumer preference for naturally formed diamonds, particularly in high-end luxury sectors is one of the key drivers of natural diamond segment. This overwhelming dominance is primarily attributed to the continent's vast natural diamond reserves and its historical significance as a leading global supplier of mined gemstones. The sentiment significantly influences global demand for African-sourced stones, which are often associated with heritage and authenticity.

Further, major mining companies such as De Beers and Alrosa maintain strong partnerships with African governments, ensuring long-term extraction rights and stable production cycles. According to the Kimberley Process Certification Scheme, African countries supplied more than 50% of the world’s rough diamonds by volume in 2023, strengthening the region’s reliance on natural diamond exports as a critical source of national income and foreign exchange earnings.

The synthetic diamond segment is the fastest growing within the Africa diamond market, expanding at a CAGR of 8.6% from 2025 to 2034. The rising acceptance of lab-grown diamonds among younger, environmentally conscious consumers is a primary factor propelling the rise of synthetic diamond segment. As per McKinsey & Company, millennials and Gen Z buyers accounted for over 40% of all diamond jewelry purchases in 2023, with a growing proportion opting for synthetic alternatives due to their lower cost and perceived ethical advantages. This shift has prompted several African jewelers to introduce hybrid collections featuring both natural and lab-created stones. The expansion of local diamond processing facilities equipped with chemical vapor deposition (CVD) technology is another influencial driver of this segment.

By Application Insights

The jewelry & ornaments application segment led the Africa diamond market by contributing a significant share of total revenue in 2025. The deep-rooted cultural significance of diamonds in African societies is among the primary factors fueling the dominance of jewelry & ornaments application segment. African-origin diamonds continue to be highly sought after in international luxury markets, where they are marketed as symbols of prestige and craftsmanship. Apart from these, the rise of locally owned luxury brands such as Thandiwe Jewels (South Africa) and House of Kirei (Kenya) has strengthened regional demand for artisanal and bespoke diamond pieces. The sustained interest from global jewelry retailers sourcing ethically certified African diamonds is also a key driver of this segment. These forces ensure that jewelry remains the dominant application for diamonds across the continent.

The industrial application segment is emerging as the fastest-growing within the Africa diamond market, projected to expand at a CAGR of 7.2%. The main driver of this growth is the expansion of manufacturing industries in countries like South Africa and Egypt, where diamond-tipped tools are essential for precision engineering and materials processing. Besides, advancements in synthetic diamond production have made industrial-grade diamonds more affordable and widely available. With Africa’s industrial base expected to grow over the next decade, the demand for industrial diamonds is set to rise correspondingly, offering new opportunities for market expansion beyond traditional jewelry applications.

REGIONAL ANALYSIS

Botswana

Botswana led the Africa diamond market by holding 25.6% of total share in 2025. Botswana’s strong partnership with De Beers through the joint venture Debswana Diamond Company ensures efficient exploration, extraction, and marketing of its diamond resources. A key factor underpinning Botswana’s market leadership is its commitment to responsible mining and economic reinvestment. Moreover, Botswana has been actively investing in downstream beneficiation by establishing diamond cutting and polishing centers in Gaborone and Francistown. Moreover, the government’s focus on transparency and governance has earned Botswana a reputation as a reliable and ethical supplier in the global diamond trade. As per the Extractive Industries Transparency Initiative, Botswana ranks among the top African nations in terms of compliance and reporting standards. These policies have helped attract premium buyers and sustain long-term investor confidence in the country’s diamond sector.

South Africa

South Africa occupies a significant position in the Africa diamond market. The country’s well-established mining infrastructure and regulatory framework support both large-scale and small-scale diamond operations. A key driver of South Africa’s market strength is the presence of renowned diamond fields such as the Cullinan Mine, which continues to yield some of the world’s most valuable gemstones. Such discoveries reinforce South Africa’s reputation for high-quality diamonds. Further, the country has been developing its downstream capabilities to enhance value addition. This strategy aims to capture more economic benefits before export and strengthen the country’s competitive edge in the global market.

Angola

Angola is also a notable player in the Africa diamond market, holding approximately 14% of total market share in 2023. According to the Angola Ministry of Geology and Mines, the country produced over 9 million carats of rough diamonds in that year, primarily from the Lunda Norte and Lunda Sul provinces. Despite political challenges in the past, Angola has made significant progress in formalizing its diamond sector and improving export transparency. One of the key factors supporting Angola’s market position is the dominance of Catoca Mine, the fourth-largest diamond mine in the world and the largest in Africa. As per Catoca Mining Company, the joint venture produced approximately 6.5 million carats in 2023, supplying both gem-quality and industrial-grade diamonds to global markets. This mine contributes significantly to the country’s export earnings and employment generation. Furthermore, Angola has been strengthening its participation in the Kimberley Process and implementing stricter controls to curb illegal trading. These reforms have enhanced Angola’s credibility as a responsible diamond producer, attracting renewed interest from international investors.

Democratic Republic of the Congo (DRC)

Democratic Republic of the Congo (DRC) a considerable share of the Africa diamond market. According to the DRC Ministry of Mines, the country produced around 15 million carats of rough diamonds in that year, though a significant portion comes from informal and artisanal sources. The Mbuji-Mayi region remains the epicenter of diamond extraction, with both large-scale and small-scale miners operating in the area. A major factor influencing the DRC’s market dynamics is the prevalence of artisanal and small-scale mining (ASM), which accounts for nearly 70% of total diamond output. According to the International Labour Organization, over 800,000 people in the DRC rely on ASM for livelihoods, highlighting the sector’s socio-economic importance despite regulatory challenges. Efforts to formalize the sector have intensified in recent years.

Namibia

Namibia remains an important region in the Africa diamond market. According to the Namibia Diamond Trading Company, the country produced over 1.3 million carats of diamonds in that year, predominantly from marine and alluvial sources along the Atlantic coast. Namibia’s unique geological conditions allow for the extraction of high-value diamonds through offshore dredging and coastal mining operations. One of the key strengths of Namibia’s diamond industry is its strict regulatory oversight and emphasis on environmental sustainability. As per the Namibian Geological Survey, marine diamond mining activities are conducted under stringent ecological guidelines to minimize disruption to marine ecosystems. This responsible approach enhances Namibia’s appeal to ethical buyers and premium markets in Europe and North America. Apart from these, the country benefits from a strategic partnership with De Beers through the Namdeb Holdings joint venture, which manages the majority of commercial diamond extraction. With continued investments in technology and beneficiation, Namibia is positioning itself as a model for sustainable diamond production in Africa.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the African diamond market are De Beers Group and its various partnerships (e.g., Debswana in Botswana, Namdeb in Namibia), Petra Diamonds Limited, Trans Hex, Lucara Diamond, and Gem Diamonds.

The Africa diamond market is highly competitive, shaped by a mix of multinational corporations, state-backed enterprises, and artisanal miners vying for market share and investment opportunities. Large-scale mining companies like De Beers, Alrosa, and Petra Diamonds dominate production and export channels, leveraging their technological capabilities, global distribution networks, and long-standing partnerships with African governments. However, they face increasing pressure from emerging private equity-backed operators and regional firms seeking to capitalize on underdeveloped diamond fields.

Competition is further intensified by growing emphasis on ethical sourcing, sustainability, and transparency, compelling firms to adopt more responsible mining practices and community engagement strategies. Besides, the informal sector remains influential, especially in countries where artisanal mining contributes significantly to total output. These small-scale miners often operate outside formal structures, creating challenges for regulation and fair market access.

At the same time, rising interest in lab-grown diamonds poses a new form of competition, prompting traditional players to reposition natural African diamonds as symbols of heritage, rarity, and authenticity. In this evolving landscape, differentiation through branding, innovation, and ethical storytelling has become crucial for maintaining relevance and securing long-term growth.

TOP PLAYERS IN THE MARKET

De Beers Group

De Beers Group is a dominant force in the Africa diamond market, with extensive operations across Botswana, Namibia, South Africa, and Canada. Known for its leadership in exploration, mining, and marketing, De Beers plays a critical role in shaping global diamond supply chains. The company's joint ventures, particularly with the government of Botswana through Debswana, have set industry benchmarks in responsible sourcing and community development.

Alrosa

Alrosa is one of the world’s largest diamond producers by volume and holds a strong presence in African diamond-rich regions. While headquartered in Russia, Alrosa has strategic partnerships and investments across several African countries, enabling it to influence regional production and pricing dynamics. Its focus on high-quality rough diamonds supports both luxury jewelry and industrial applications globally.

Petra Diamonds

Petra Diamonds specializes in diamond mining in southern Africa, particularly in South Africa and Tanzania. The company operates some of the most historically renowned mines, such as Cullinan and Finsch. Petra emphasizes sustainable mining practices, contributing to local economic development while supplying premium gemstones to international markets. Its operational expertise enhances Africa’s reputation as a source of high-value diamonds.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One major strategy employed by key players in the Africa diamond market is strengthening ethical sourcing and traceability initiatives , ensuring that mined diamonds meet international standards such as the Kimberley Process and EITI. This enhances consumer trust and secures access to premium markets in Europe and North America.

Another key approach is investing in local beneficiation , including cutting, polishing, and jewelry manufacturing within African countries. By adding value before export, companies support local economies and increase profitability from domestic processing rather than relying solely on raw diamond sales.

Lastly, leading firms are expanding digital transparency and blockchain integration , using innovative technologies to track diamonds from mine to retail. This not only improves supply chain efficiency but also strengthens brand credibility among environmentally and ethically conscious consumers.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, De Beers launched a blockchain-based certification pilot in partnership with the Botswana government to enhance diamond traceability and reinforce consumer confidence in African-origin stones.

- In July 2023, Petra Diamonds announced a strategic restructuring plan aimed at optimizing mine operations in South Africa, focusing on cost efficiency and environmental compliance to ensure long-term viability.

- In November 2023, Alrosa expanded its collaboration with Namdeb Holdings to explore new marine diamond extraction zones off the coast of Namibia, strengthening its regional footprint and resource base.

- In March 2025, Lucara Diamond Corporation entered into a joint venture with a South African technology firm to deploy AI-driven sorting systems at its Karowe mine, improving recovery rates of high-value diamonds.

- In September 2023, the Government of Botswana and De Beers renewed their long-term partnership agreement, reaffirming commitments to sustainable mining and shared economic benefits through the Debswana joint venture.

MARKET SEGMENTATION

This research report on the Africa diamond market is segmented and sub-segmented into the following categories.

By Type

- Natural

- Synthetic

By Application

- Jewelry & Ornaments

- Industrial

By Region

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa

Frequently Asked Questions

1. What factors are driving the growth of the Africa diamond market?

Growth drivers include rising global demand for luxury jewelry, investment in mining infrastructure, and favorable government policies.

2. Which African countries are the major producers in the diamond market?

Key producers include Botswana, South Africa, Angola, Namibia, and the Democratic Republic of Congo.

3. What types of diamonds are most in demand in Africa?

Rough diamonds for export and high-quality polished diamonds for luxury jewelry are in high demand.

4. Who are the major players in the Africa diamond market?

Leading players include De Beers, Petra Diamonds, Lucara Diamond Corp, ALROSA, and Endiama.

5. What role does Africa play in the global diamond supply chain?

Africa is a major supplier of rough diamonds, contributing significantly to global diamond production.

6. How is technology influencing diamond mining in Africa?

Technologies such as automated sorting, drone mapping, and AI-driven exploration are improving efficiency and yield.

7. What challenges affect the Africa diamond market?

Challenges include political instability, illegal mining, environmental concerns, and fluctuating global prices.

8. How is the demand for lab-grown diamonds affecting the Africa diamond market?

While still emerging, the rising global preference for lab-grown diamonds poses long-term competition for natural diamond producers.

9. How are lab-grown diamonds affecting the market?

They are creating competition by offering lower-cost alternatives.

10. What is the future outlook of the Africa diamond market?

The market is expected to grow steadily with increasing focus on sustainability and global demand.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com