Africa Diesel Genset Market Size, Share, Trends, COVID-19 Impact & Growth Analysis Report – Segmented By Ratings (0–75 kVA, 75–375 kVA, 375–750 kVA, Above 750 kVA), Application & Country (South Africa, Nigeria, Rest of Africa) - Industry Analysis From 2026 to 2034

Africa Diesel Genset Market Size

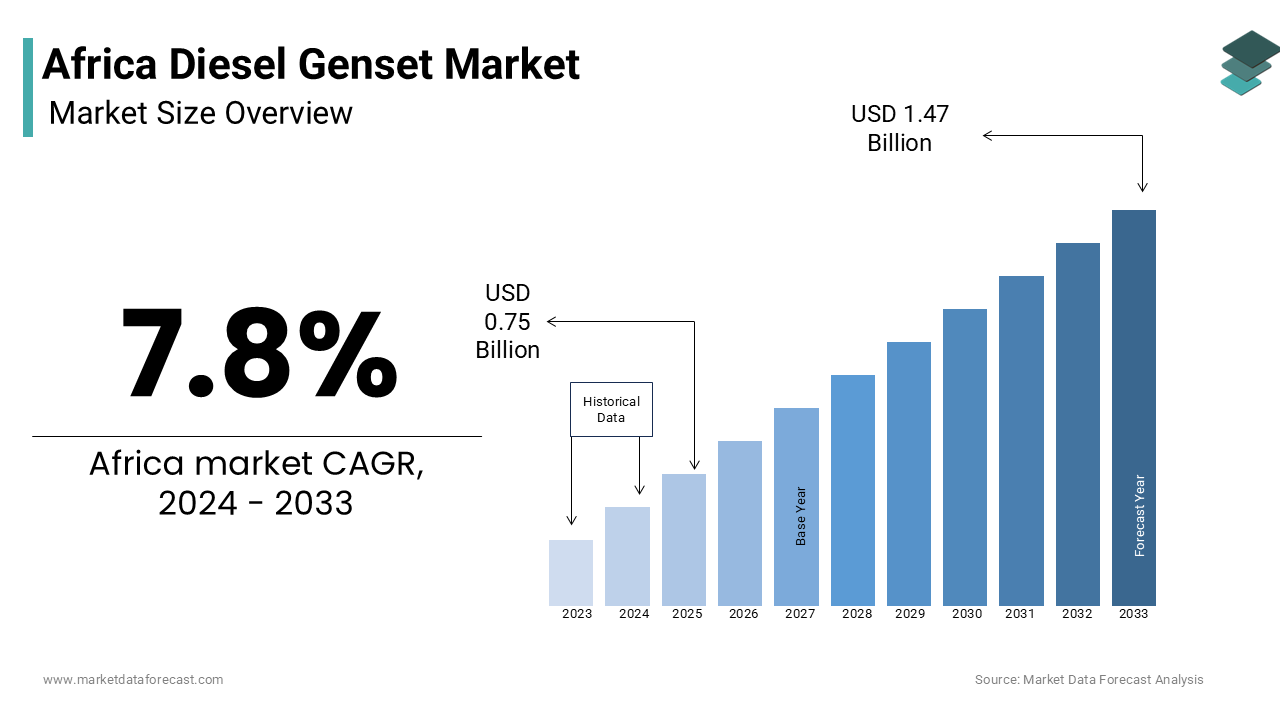

The Africa diesel genset market size was valued at USD 0.81 billion in 2025 and is anticipated to reach USD 0.87 billion in 2026 from USD 1.59 billion by 2034, growing at a CAGR of 7.8% during the forecast period from 2026 to 2034.

Diesel genset refers to the diesel-powered generator sets across residential, commercial, industrial, and institutional sectors, primarily as a response to inconsistent grid infrastructure and recurrent power outages. These gensets serve as critical backup or primary power sources across the continent, where energy access remains a persistent challenge. The operational resilience of diesel gensets in harsh climatic and logistical conditions further entrenches their adoption, particularly in remote and off-grid regions. Unlike centralized energy expansion, which progresses slowly due to capital intensity and regulatory bottlenecks, diesel gensets offer immediate scalability. Their integration into mining operations, healthcare facilities, and telecommunications networks underscores their strategic importance in sustaining economic activity across Africa’s diverse geographies.

MARKET DRIVERS

The continent’s acute and persistent electricity deficit, which compels both public and private entities to adopt off-grid power solutions, is one pivotal driver of the Africa diesel genset market. Industries such as mining and manufacturing, which require uninterrupted energy, deploy large-scale diesel gensets to maintain operations. Similarly, telecom towers across region operate on diesel backup for significant hours annually. This structural power gap, coupled with sluggish grid expansion, ensures sustained demand for diesel gensets across urban and rural Africa.

The rapid expansion of Africa’s construction and real estate sectors, which necessitates reliable on-site power for project continuity, is another significant driver. The continent’s construction industry grew notably between 2018 and 2023, fueled by urbanization and infrastructure development. Projects ranging from housing estates to commercial complexes in cities like Lagos, Nairobi, and Abidjan frequently operate in areas with unreliable grid access, requiring diesel gensets for both primary and auxiliary power. In Nigeria alone, developers installed diesel generator capacities for ongoing construction activities. Moreover, large-scale infrastructure initiatives such as the Dongo Kundu Special Economic Zone in Kenya and the Lekki Free Trade Zone in Nigeria rely extensively on diesel power during development phases. This construction boom, deeply intertwined with energy insecurity, sustains robust demand for diesel gensets across the continent.

MARKET RESTRAINTS

The escalating cost and volatility of diesel fuel, which significantly impacts operational expenditures, is a major restraint in the Africa diesel genset market. Also, the average retail price of diesel in Nigeria rose significantly in 2023, reflecting broader continental trends driven by global oil fluctuations and domestic subsidy reforms. For commercial users, fuel constitutes a major part of total genset lifecycle costs. In countries, where inflation and currency devaluation exacerbate fuel pricing, businesses are forced to limit generator runtime, undermining productivity. This economic burden discourages long-term reliance on diesel gensets, especially among small and medium enterprises, thereby constraining market growth despite high energy demand.

The tightening environmental regulation and growing policy shift toward cleaner energy alternatives, which threaten the long-term viability of diesel gensets, is another critical restraint. As per the United Nations Environment Programme, many African countries have updated their Nationally Determined Contributions (NDCs) under the Paris Agreement to include explicit targets for reducing fossil fuel dependency in power generation. Additionally, the African Development Bank is heavily investing in renewable energy investments were committed across the continent, signaling a strategic pivot away from diesel-based power. Urban centers are incentivizing solar-hybrid systems for commercial buildings, reducing diesel genset uptake. These regulatory and financial shifts create a disincentive for new diesel installations, particularly in environmentally conscious sectors and donor-funded projects.

MARKET OPPORTUNITIES

The integration of hybrid power systems, where diesel gensets are paired with renewable energy sources to enhance efficiency and reduce fuel dependency, is one transformative opportunity. As per the International Renewable Energy Agency, hybrid mini-grids combining solar PV and diesel gensets can reduce fuel consumption by 40% to 70%, a critical advantage in remote mining and rural telecom applications. In Namibia, mines implemented a solar-diesel hybrid system, cutting diesel use. This trend is supported by advancements in smart controllers and energy management systems that optimize genset operation. For manufacturers, this presents a lucrative avenue to reposition diesel gensets as transitional assets within cleaner energy ecosystems, extending their relevance amid decarbonization pressures.

The digitization and remote monitoring of diesel gensets, enabling predictive maintenance and operational efficiency in dispersed African markets, is another emerging opportunity. Companies have deployed cloud-based platforms across Nigeria and Ghana to manage fleets of rental gensets, reducing downtime. Nigerian telecom towers use remote monitoring to optimize genset usage, minimizing theft and inefficiency. With mobile network penetration exceeding 84% in sub-Saharan Africa as per the GSM Association, the infrastructure exists to scale these digital solutions. This technological evolution not only enhances genset reliability but also opens revenue streams in data analytics, service contracts, and managed power solutions, reshaping the market beyond mere equipment sales.

MARKET CHALLENGES

The prevalence of substandard and counterfeit equipment, which undermines performance, safety, and consumer trust, is a pressing challenge in the Africa diesel genset market. As per the Standards Organization of Nigeria, high percentage of diesel generators imported into the country in 2022 failed to meet minimum efficiency and emissions standards, often originating from unregulated supply chains in Asia. These non-compliant units, frequently rebranded or assembled from used components, exhibit higher fuel consumption and shorter lifespans, increasing long-term costs for end users. The Kenya Bureau of Standards frequently seized illicit gensets, many lacking proper certification. In healthcare settings, such unreliable units pose critical risks. This proliferation of inferior products erodes confidence in the market and impedes investment in legitimate, high-performance genset solutions.

The shortage of skilled technicians for installation, maintenance, and repair of diesel gensets across rural and underserved regions is another formidable challenge. Like, fewer share of technical and vocational training programs in member states include specialized courses on modern diesel generator systems. The lack of trained manpower delays response times and escalates operational risks, particularly in critical sectors like healthcare and water supply. This technical skills gap hampers the efficient utilization of existing genset capacity and limits the scalability of power solutions, even when equipment is available.

SEGMENTAL ANALYSIS

By Ratings Insights

The 75–375 kVA segment commanded the largest share of the Africa diesel genset market at 47.3% of total installed capacity in 2024. This dominance of segment is due to its alignment with the operational scale of medium-sized enterprises and critical infrastructure. The proliferation of commercial and industrial facilities, such as shopping malls, mid-tier manufacturing units, and private hospitals, that require uninterrupted power but operate below the threshold of utility-scale demand is a primary driver. According to the International Finance Corporation, formal SMEs in East and West Africa rely on gensets in this rating range due to their balance between output and cost-efficiency. Additionally, the segment supports telecom tower clusters; most of mobile network sites across region use 100–300 kVA diesel gensets, reinforcing their centrality in digital infrastructure resilience.

The 0–75 kVA segment is expanding at the fastest rate and is registering a CAGR of 7.9% between 2025 and 203. This acceleration is fueled by rising adoption among small businesses and residential users in rapidly urbanizing centers. The surge in off-grid housing developments, particularly in peri-urban regions of countries like Ethiopia and Tanzania, where grid access remains erratic, is a key factor. Like, millions of households in sub-Saharan Africa purchased small-scale power solutions between 2020 and 2023, with diesel gensets below 75 kVA being the most prevalent due to affordability and ease of installation. Furthermore, micro-enterprises such as bakeries, refrigerated kiosks, and roadside clinics increasingly deploy compact gensets, underscoring grassroots-level electrification dependency.

By Application Insights

The backup power segment constitutes the prominent application by capturing an estimated 62.4% of the Africa diesel genset market by usage volume in 2024. This preeminence is rooted in the continent’s chronic grid instability, which compels institutions and businesses to maintain standby power as a risk mitigation strategy. The vulnerability of critical infrastructure to outages is a pivotal driver. As per the World Health Organization, most of hospitals in sub-Saharan Africa operate diesel gensets as backup due to unreliable public electricity, with average blackout durations exceeding long hours per week. Similarly, financial institutions rely on backup systems to protect data centers and ATMs. This institutional dependency on fail-safe power ensures sustained demand, particularly in urban centers where downtime translates into severe economic and social consequences.

The prime power segment is emerging as the fastest-growing application and is projected to grow at a CAGR of 8.3% during the forecast period. Unlike backup usage, prime power denotes gensets operating as the primary electricity source, reflecting deepening energy poverty and the slow pace of grid extension. This growth is particularly pronounced in off-grid and peri-urban zones where electrification remains nominal. As per the United Nations Development Programme, millions of people in rural Africa lack grid connectivity, compelling reliance on diesel gensets for daily operations. Additionally, mining concessions in Burkina Faso and the Democratic Republic of Congo operate entirely on prime diesel power. This shift from supplementary to primary reliance underscores a structural energy deficit that continues to drive market expansion.

REGIONAL ANALYSIS

South Africa held a commanding position in the Middle East and Africa diesel genset market by representing a 22.7% of regional demand in 2024. Despite having the most developed grid on the continent, the country faces unprecedented load-shedding, with Eskom implementing over 200 days of rolling blackouts in 2023 alone, according to the Council for Scientific and Industrial Research. This systemic grid failure has triggered a surge in both commercial and residential genset adoption. Moreover, industrial zones like Coega and Dube TradePort operate on hybrid diesel setups to ensure continuity. The country’s high concentration of formal economic activity, coupled with deteriorating public power supply, sustains its leadership in genset demand across MEA.

Egypt is another key player in the MEA market which is propelled by aggressive industrialization and population growth that outpaces grid capacity expansion. The Ministry of Electricity and Renewable Energy reported that peak electricity demand reached 33 GW in 2023, while available generation capacity stood at 30.5 GW, resulting in persistent shortfalls. Additionally, the government’s push for new urban centers, such as the New Administrative Capital, has led to temporary but extensive diesel power deployment, with contractors installing genset capacity. The combination of infrastructural transition, energy deficit, and foreign investment in manufacturing solidifies Egypt’s position as a major market for medium and large diesel generators.

Nigeria follows closely in the market and is shaped by one of the most severe electricity access gaps in the world. As per the Nigerian Electricity Regulatory Commission, the national grid supplies less than 5 GW to a population of over 220 million, forcing over 80% of businesses to operate their own power systems. Also, diesel gensets generate more GWs of private power annually, exceeding grid output. The construction boom, telecom expansion, and rise of private healthcare facilities have institutionalized diesel dependency. Furthermore, as per the Central Bank of Nigeria, businesses spend up to 40% of operational costs on fuel for power, highlighting the embedded nature of diesel gensets in the country’s economic fabric.

Kenya holds a notable share of the MEA diesel genset market and is distinguished by its paradoxical energy landscape: a leader in geothermal and wind energy, yet heavily reliant on diesel for grid balancing and backup. The Kenya Power and Lighting Company experienced 137 planned outages in 2023, prompting businesses in Nairobi and Mombasa to invest in standby systems, as documented in the Energy and Petroleum Regulatory Authority’s annual performance review. The ICT sector is a major consumer. Additionally, the ongoing Standard Gauge Railway project and Lamu Port-South Sudan-Ethiopia Transport (LAPSSET) corridor have driven temporary but substantial diesel power demand. Though Kenya promotes renewables, intermittent supply forces continued reliance on diesel, particularly in high-value economic nodes.

Ethiopia accounts for key share of the regional market and is driven by industrial park development and persistent urban power shortages. The Ethiopian Investment Commission reports that all nine of the country’s major industrial parks, including Hawassa and Bole Lemi, operate on diesel gensets due to inconsistent grid supply. The government’s industrialization drive, which aims to create 1 million jobs in export-oriented manufacturing, depends heavily on self-generated power. This institutionalized off-grid power model positions Ethiopia as a growing and strategically significant market within the MEA region.

COMPETITIVE LANDSCAPE

Competition in the Africa diesel genset market is intensifying as global manufacturers, regional distributors, and specialized power providers vie for dominance across fragmented national markets. The landscape features a mix of established multinational corporations and agile local assemblers, each leveraging distinct advantages. Multinationals such as Cummins and Caterpillar compete on technology, durability, and service networks, while regional players offer cost-effective alternatives with faster turnaround. The rise of hybrid and digitalized gensets has shifted competitive dynamics, favoring companies investing in smart energy solutions. Rental models led by Aggreko add another dimension, catering to temporary and scalable needs. Price sensitivity, fuel efficiency, and after-sales reliability are key differentiators. Regulatory pressures and environmental concerns are prompting innovation, with competitors differentiating through emission-reducing technologies and training programs. The absence of standardized regulations across countries allows varied market entry strategies, but also fosters competition based on adaptability, localization, and responsiveness to Africa’s complex energy realities.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the Africa diesel genset market include

- Caterpillar Inc.

- Cummins Inc.

- Kohler-SDMO

- MTU Onsite Energy

- FG Wilson

- HIMOINSA

- Atlas Copco AB

- AKSA Power Generation

- Kirloskar Oil Engines Ltd.

- Mitsubishi Heavy Industries

- Perkins

- Volvo Penta

- Jubaili Bros

- Aggreko

- Teksan

- Baudouin

- Mikano International Limited

- Briggs & Stratton

- MAN Diesel & Turbo SE

- Yanmar Holdings Co.

- Honda Siel Power Products

Top Players in the Africa Diesel Genset Market

Cummins Inc. has established a deep-rooted presence across Africa through localized manufacturing, service networks, and energy solutions tailored to the continent’s infrastructure challenges. The company operates assembly facilities in South Africa and Nigeria, enabling faster deployment and reduced logistics costs. In 2023, Cummins launched a new digital monitoring platform for gensets in Kenya and Ghana, integrating IoT sensors to enable remote diagnostics and predictive maintenance. It also partnered with local distributors to expand rural reach and introduced fuel-efficient models designed for high ambient temperatures. Cummins has increasingly focused on hybrid-ready gensets, supporting mining and telecom clients in reducing diesel consumption. Its investment in technician training programs across East Africa, in collaboration with vocational institutions, has strengthened after-sales reliability, reinforcing customer loyalty and operational efficiency in remote deployments.

Caterpillar Inc. maintains a strategic footprint in Africa by targeting heavy-duty industrial and infrastructure sectors that demand high-capacity power solutions. The company supplies diesel gensets through its authorized dealer network, including Bramcor in South Africa and Obasanjo Group in Nigeria, ensuring localized support and maintenance. In 2022, Caterpillar deployed containerized power plants in Angola and Mozambique to support LNG projects, emphasizing rapid deployment and durability in extreme environments. It introduced Cat Connect technology to monitor genset performance in real time across mining operations in the Democratic Republic of Congo. Additionally, Caterpillar has expanded its remanufacturing programs in Africa, offering refurbished gensets with full warranties to reduce costs for mid-tier clients. These initiatives reflect its focus on lifecycle value, operational resilience, and alignment with large-scale energy-deficient industrial projects.

Aggreko plc distinguishes itself through a rental and temporary power model, making it a critical player in Africa’s short-to-medium-term energy supply landscape. The company provides scalable diesel genset solutions for events, construction sites, and emergency infrastructure, with operations spanning over 20 African countries. In 2023, Aggreko deployed 180 MW of temporary power across Nigeria and South Africa to support grid stabilization during peak outages. It launched hybrid power stations combining diesel and battery storage in Namibia and Rwanda, reducing fuel use by up to 40%. The company also expanded its service hubs in Accra and Kampala to enhance response times. Aggreko’s flexibility, rapid deployment capability, and shift toward low-emission configurations have solidified its role in bridging Africa’s power gaps during transitions to permanent grid solutions.

Top Strategies Used by Key Market Participants

Key players in the Africa diesel genset market are deploying multifaceted strategies to consolidate their presence amid evolving energy dynamics. A dominant approach is the expansion of localized service and distribution networks to improve response times and customer retention, particularly in remote regions. Companies are increasingly investing in digital integration, embedding IoT-enabled monitoring systems to offer predictive maintenance and remote diagnostics. Strategic partnerships with local distributors and energy firms are enhancing market penetration while reducing logistical barriers. Another critical strategy is product adaptation, with manufacturers redesigning gensets for high-temperature resilience, fuel efficiency, and compatibility with hybrid systems. Rental and pay-per-use models are gaining traction, especially among SMEs and temporary projects. Additionally, firms are launching technician training programs to address the skills gap and ensure reliable after-sales support. Sustainability-linked innovation, such as retrofitting gensets for lower emissions or hybrid operation, is also being prioritized to align with regulatory trends and environmental expectations.

RECENT MARKET DEVELOPMENTS

- In June 2023, Cummins Inc. launched an IoT-enabled remote monitoring system for diesel gensets in Kenya and Ghana, enhancing predictive maintenance and operational efficiency for telecom and industrial clients.

- In September 2022, Caterpillar Inc. deployed a 100 MW containerized diesel power plant in Mozambique to support LNG infrastructure, reinforcing its presence in large-scale energy projects.

- In January 2024, Aggreko plc commissioned a hybrid diesel-battery microgrid in Namibia, reducing fuel consumption by 38% and positioning itself as a transitional energy solutions provider.

- In November 2023, Generac Holdings expanded its distribution partnership with Lagos-based PowerGen Solutions to increase market reach across West Africa’s commercial sector.

- In March 2023, Kirloskar Electric established a new assembly and service center in Addis Ababa, Ethiopia, to improve delivery timelines and after-sales support for industrial clients.

MARKET SEGMENTATION

This research report on the Africa Diesel Genset Market is segmented and sub-segmented into the following categories.

By Ratings

- 0–75 kVA

- 75–375 kVA

- 375–750 kVA

- Above 750 kVA

By Application

- Backup Power

- Prime Power

By Country

- South Africa

- Nigeria

- Rest of Africa

Frequently Asked Questions

What is driving the growth of the Africa diesel genset market?

The market is primarily driven by unreliable grid power supply, rapid urbanization, industrialization, and the need for backup and prime power solutions across the continent.

Which rating segment holds the largest market share in Africa?

The 75–375 kVA segment holds the largest share, supported by demand from SMEs, hospitals, malls, and telecom towers.

What are the major challenges facing the Africa diesel genset market?

Challenges include high fuel costs, environmental concerns, competition from renewable energy, and maintenance expenses.

What is the future outlook for the Africa diesel genset market?

The market will continue to grow steadily, driven by grid unreliability, urban expansion, and industrial growth, though it will face increasing competition from renewable and hybrid systems.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com