Africa Freight logistic Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Function, End-User And Country (Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa), Industry Analysis From (2026 to 2034)

Market Size, 2025

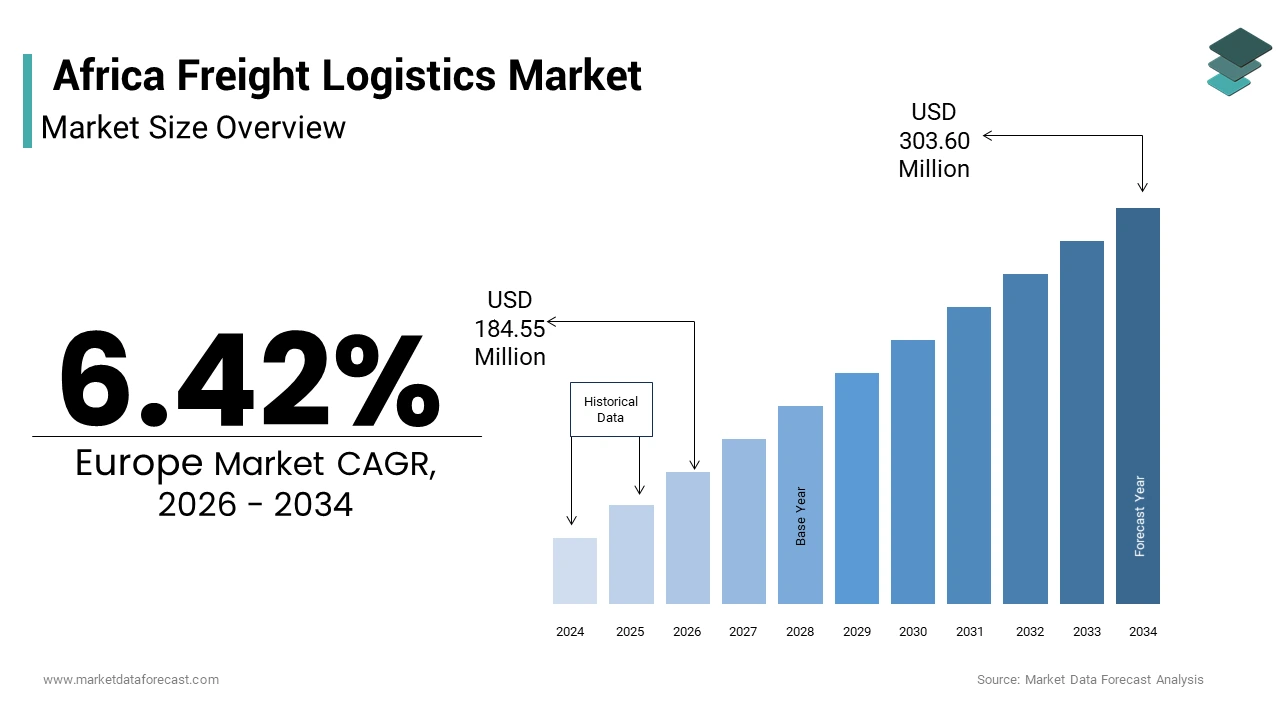

$173.42 MnMarket Estimate, 2026

$184.55 MnMarket Forecast, 2034

$303.60 MnCAGR, 2026–2034

6.42%Africa Freight Logistics Market Report Summary

The African freight logistics market was valued at USD 184.55 million in 2025 and is expected to reach USD 303.60 million by 2034 at a CAGR of 6.42%. Growth is driven by AfCFTA-led intra-regional trade expansion, rapid urbanization and e-commerce growth, and investments in regional corridors and dry ports. Key barriers include weak multimodal infrastructure, cross-border regulatory fragmentation, energy and fuel volatility, and a shortage of logistics skills. Opportunities exist in digital freight platforms, cold-chain expansion, corridor development, and value-added logistics services.

What is the Africana freight logistics market?

The African freight logistics market covers the movement, storage, and distribution of goods across the continent using road, rail, maritime, and air transport, plus warehouse and value-added services that support domestic and cross-border trade.

Key Trends of Africa Freight Logistics

- AfCFTA is shifting trade patterns, increasing demand for cross-border freight solutions and bonded logistics.

- Digital freight platforms and mobile load-matching are scaling, improving truck utilization, and reducing empty runs.

- Cold-chain and perishable logistics are expanding as agribusiness and horticulture exporters move to higher-value markets.

- Public-private corridor upgrades (ports, rail, dry ports) are unlocking capacity on major trade routes.

- Last-mile urban logistics is being professionalized and driven by e-commerce in major cities.

- Green and resilient logistics investments (electric last-mile vehicles, solar at warehouses) are emerging among large providers.

Segmental Insights

- Freight transport dominated the market due to heavy reliance on road haulage for inland movement.

- Value-added services are the fastest-growing function, driven by e-commerce, customs compliance, and cold-chain needs.

- Manufacturing & automotive is the largest end-user, supplying a steady corridor demand for components and finished goods.

- Agriculture, fishing & forestry are the fastest-growing end-users, increasing demand for refrigerated and specialty logistics.

- Road remains the primary mode, while rail and maritime are expanding where corridor investment occurs.

Regional Highlights

- East Africa corridors (Mombasa–Nairobi–Kampala) continue to strengthen as gateways for inland trade and perishables.

- Southern Africa relies on port hubs (Durban, Maputo, Ngqura) and regional rail projects to connect mining and agricultural exports.

- North Africa, led by Egypt, benefits from Suez connectivity and transshipment flows to Europe and Asia.

- West and Central Africa face acute corridor and customs challenges, but digital customs pilots and dry ports are improving flows.

- Landlocked countries show the largest logistical uplift potential from corridor and dry-port investments.

Africa Freight Logistics Market Size

The Africa Freight logistics market size was valued at USD 173.42 million in 2025 and is anticipated to reach USD 184.55 million in 2026 to USD 303.60 million by 2034, growing at a CAGR of 6.42% during the forecast period from 2026 to 2034.

Freight logistics covers the integrated movement, storage, and distribution of goods across the continent through multimodal transport networks, including road, rail, maritime, and air. Characterized by fragmented infrastructure and evolving regulatory frameworks, the sector plays a pivotal role in enabling intra-African trade, which, as of 2022, accounted for only 17% of total African commerce despite the launch of the African Continental Free Trade Area (AfCFTA). According to the World Bank, nearly 60% of Africa’s population resides in rural areas with limited or no all-weather road access, significantly impeding last-mile delivery efficiency. Furthermore, the United Nations Economic Commission for Africa indicates that logistics costs in Africa consume up to 30% of the value of shipments, more than double the global average, due to inefficiencies in border clearance and transport coordination. These structural realities define the operational landscape of freight logistics across diverse regional markets.

MARKET DRIVERS

Expansion of Intra-African Trade Under AfCFTA

The operationalization of the African Continental Free Trade Area has catalyzed a structural shift in regional trade dynamics, directly stimulating demand for cross-border freight logistics. As of 2023, the United Nations Economic Commission for Africa reported that the AfCFTA has the potential to increase intra-African trade by over 50% once fully implemented, creating a unified market of more than 1.3 billion people. This surge in regional commerce necessitates robust logistics frameworks to handle rising volumes of manufactured goods, agricultural produce, and industrial inputs across previously isolated markets. For instance, trade between East African Community member states grew by 12% year-on-year in 2022, as per the East African Shippers' Council, reflecting increased movement of cargo through corridors linking Mombasa, Dar es Salaam, and Kigali. Consequently, logistics providers are investing in transnational warehousing and bonded transport systems to meet the demand for seamless customs transit, reinforcing the strategic importance of integrated freight networks.

Rapid Urbanization and E-commerce Penetration

Africa’s accelerating urban population growth is reshaping consumption patterns and amplifying demand for efficient freight distribution systems. The United Nations projects that Africa will be home to 1.3 billion urban dwellers by 2050, with cities such as Lagos, Nairobi, and Addis Ababa experiencing some of the fastest urban expansion rates globally. This demographic shift has coincided with a surge in digital adoption. As consumer expectations for next-day or same-day delivery rise, logistics firms are compelled to enhance last-mile capabilities, cold chain solutions, and real-time tracking infrastructure to sustain service reliability.

MARKET RESTRAINTS

Underdeveloped Multimodal Transport Infrastructure

A critical impediment to the efficiency of Africa’s freight logistics sector is the continent’s inadequate and poorly integrated transport infrastructure. According to the African Development Bank, only 34% of rural Africans live within two kilometers of an all-season road, severely limiting access to major ports and distribution hubs. Rail networks, where they exist, often operate below capacity due to outdated signaling systems and a lack of standardization. Nearly 85% of Africa’s rail lines are single-track, as per the International Union of Railways. This fragmentation forces overreliance on road transport, which accounts for over 80% of freight movement in regions like West and East Africa, leading to congestion, higher fuel consumption, and vehicle wear.

Regulatory Fragmentation and Border Delays

Cross-border freight movement in Africa is significantly hindered by inconsistent customs procedures, non-harmonized trade regulations, and prolonged clearance times. Like, cargo moving between African countries faces many border control checks, with trucks spending a notable share of transit time waiting at borders rather than in motion. Additionally, the absence of universal electronic cargo tracking systems across regional economic communities exacerbates delays. The East African Community has made progress with the Electronic Cargo Tracking System, reducing transit time by 30%, but such initiatives remain unevenly adopted. These inefficiencies inflate operational costs and deter investment in scalable logistics solutions.

MARKET OPPORTUNITY

Digitalization and Logistics Technology Adoption

The integration of digital technologies presents a transformative opportunity for modernizing Africa’s freight logistics ecosystem. Mobile-based freight matching platforms, GPS-enabled fleet management systems, and blockchain-powered customs documentation are gaining traction across key corridors. Companies like Lori Systems and Kobo360 utilize real-time data analytics to optimize truck utilization, reportedly increasing load efficiency on routes between Nigeria and Niger. Furthermore, the African Development Bank estimates that widespread adoption of digital logistics platforms could reduce freight costs by 15–20% across the continent. Governments are also advancing digital trade facilitation; Rwanda’s paperless trade system, implemented in 2021, cut import clearance time from five days to under 24 hours, as per the United Nations Conference on Trade and Development.

Development of Regional Trade Corridors and Special Economic Zones

Strategic investments in regional transport corridors and industrial zones are unlocking new freight logistics demand across Africa. The African Union’s Program for Infrastructure Development in Africa (PIDA) prioritizes 16 regional multimodal corridors designed to link landlocked nations with seaports and economic hubs. One such initiative, the Lobito Atlantic Railway Corridor, launched in 2023 with support from the U.S. and European investors, aims to connect mineral-rich regions of the Democratic Republic of Congo and Zambia to the Angolan port of Lobito, reducing transit time by nearly 50%. These corridors are catalyzing the development of intermodal terminals, dry ports, and bonded logistics centers, creating scalable infrastructure for efficient cargo handling and value-added services.

MARKET CHALLENGE

Energy Insecurity and Fuel Supply Volatility

The reliability of freight operations across Africa is increasingly threatened by chronic energy shortages and fluctuating fuel availability. Diesel, the primary fuel for freight trucks and backup generators at logistics hubs, is subject to frequent supply disruptions due to underinvestment in refining capacity and import dependency. Nigeria, Africa’s largest economy, operates at less than 20% of its installed refinery capacity, resulting in over 90% of petroleum products being imported, as per the Nigerian National Petroleum Company in 2023. This dependence exposes the logistics sector to global price shocks and local distribution bottlenecks. Persistent power outages further impair warehouse operations, cold storage, and digital logistics platforms, undermining service consistency and increasing operational risk.

Skilled Labor Shortage in Logistics Management

The African freight logistics market faces a critical deficit in professionally trained personnel capable of managing complex supply chain operations. In South Africa, only some accredited institutions offer logistics and supply chain management programs at the tertiary level. This gap is exacerbated in landlocked countries such as Chad and Malawi, where technical education in transport planning and customs compliance is underfunded. The shortage affects critical functions, including fleet maintenance, warehouse automation, and regulatory compliance, leading to suboptimal asset utilization and increased error rates in cargo handling. Without targeted investment in vocational training and public-private partnerships, the human capital deficit will continue to constrain sectoral modernization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.42% |

| Segments Covered | By Function, End-User, Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Sudan, Egypt, Kenya, Ethiopia, South Africa, Rest of Africa |

| Market Leaders Profiled | DHL, Aramex, Kuehne + Nagel, United Parcel Service Inc., RAK Logistics, Al-Futtaim Logistics, Agility Logistics, Saudi Transport & Investment Co. (Mubarrad), Almajdouie Group, Ceva Logistics, Gulf Agency, Company (GAC). |

SEGMENT ANALYSIS

By Function Insights

The Freight Transport segment held the largest market share of 57.4% in 2024. This dominance of the element is credited to the continent’s heavy reliance on the physical movement of goods across vast distances, often under conditions of limited infrastructure integration. The segment encompasses road, rail, maritime, and air freight, with road transport alone contributing between 75-90% of inland freight volume across Sub-Saharan Africa, according to the African Development Bank. Long-haul trucking remains indispensable despite inefficiencies because only a portion of Africa’s roads are paved. Moreover, the absence of seamless intermodal connectivity forces shippers to depend on point-to-point road haulage, further entrenching freight transport as the backbone of logistics operations. The persistent underdevelopment of alternative logistics infrastructure, which compels continued dependence on road-based freight, is a primary driver of this segment’s preeminence. Also, landlocked countries in Africa rely exclusively on neighboring coastal nations’ road networks to access seaports, making overland trucking a non-negotiable component of trade. Additionally, rail freight contributes less than 10% of total inland cargo in most regions due to deteriorated tracks and a lack of standardization, as highlighted by the International Union of Railways. This infrastructure asymmetry ensures that freight transport remains the dominant function, absorbing the bulk of logistics expenditure.

The Value-added Services segment is the fastest-growing segment within the functional classification and is projected to expand at a CAGR of 11.3% between 2025 and 2033. This acceleration is fueled by rising demand for integrated logistics solutions that go beyond basic transportation and storage. As African supply chains become more complex, businesses increasingly seek services such as inventory tracking, kitting, labeling, quality inspection, and customs brokerage—functions that enhance supply chain visibility and compliance. The proliferation of e-commerce has been particularly instrumental in driving this trend. The digital transformation of logistics operations, enabling providers to offer scalable, tech-enabled value-added solutions, is a notable factor behind this rapid growth. Companies like DHL and Agility have introduced smart warehousing platforms across Nairobi and Lagos that integrate IoT sensors and automated sorting systems, increasing service efficiency. Furthermore, the African Continental Free Trade Area mandates standardized rules of origin and digital documentation, prompting freight forwarders to embed compliance and packaging services into their offerings. This shift toward service bundling is redefining competitive advantage in the sector, propelling value-added services into a high-growth trajectory.

By End User Insights

The Manufacturing and Automotive sector was the prevailing end-user in the African freight logistics market by commanding an estimated 32.4% share of total logistics demand in 2024. This lead position is associated with the sector’s extensive supply chain requirements, which span raw material importation, component distribution, and finished vehicle or machinery dispatch. Industrial zones across South Africa, Morocco, and Egypt have become hubs for automotive assembly, with the continent producing a substantial number of vehicles annually. These operations generate consistent freight flows, particularly along corridors connecting ports like Durban and Casablanca to inland manufacturing plants. Additionally, the expansion of local content policies in countries such as Nigeria and Kenya has spurred the establishment of component suppliers, further intensifying intra-regional logistics activity. The strategic localization of automotive production, supported by government incentives and regional trade agreements, is a critical driver of this segment’s dominance. South Africa is Africa’s largest vehicle production, exporting a significant volume of units annually to other African markets. This export-oriented model necessitates reliable multimodal freight networks capable of handling just-in-time delivery schedules and roll-on/roll-off (Ro-Ro) shipping. Moreover, the Moroccan Ministry of Industry indicates that the Tanger Med industrial zone, home to Renault and Stellantis plants, handles vehicles in exports, requiring dedicated rail and road links to the port. Such integrated industrial-logistics clusters have increased freight demand annually in host regions, reinforcing the sector’s outsized influence on logistics infrastructure development.

The Agriculture, Fishing, and Forestry segment is the fastest-growing end-user and is projected to register a CAGR of 10.7% in freight logistics demand from 2025 to 2033. This surge is driven by rising investment in agro-value chains and the need to reduce post-harvest losses, which currently stand at 30–40% across Sub-Saharan Africa due to inadequate cold chain and transport access. The African Union’s Comprehensive Africa Agriculture Development Programme (CAADP) has set targets to double agricultural productivity by 2030, catalyzing infrastructure upgrades and logistics modernization. Exports of perishable goods such as flowers, fruits, and seafood have expanded rapidly; Kenya’s horticulture sector ships notable metric tons of fresh produce via Jomo Kenyatta International Airport, making it the leading air cargo exporter in Africa. The expansion of perishable export corridors and cold chain investments is a major factor fueling this growth. Also, cold storage facilities in Ghana and Senegal have increased export readiness for mango and shrimp producers, reducing spoilage and extending market access. Additionally, the World Bank’s Ethiopia Logistics Program has facilitated the construction of refrigerated truck terminals along the Addis Ababa–Djibouti corridor, enabling year-round export of coffee and pulses. Airlines such as Ethiopian Cargo and RwandAir have dedicated perishable freighters, while logistics firms like Twiga Foods in Kenya are deploying AI-driven routing to optimize fresh produce distribution, signaling a structural shift toward high-efficiency agri-logistics.

COUNTRY-LEVEL ANALYSIS

South Africa Logistics Market Analysis

South Africa remained the most advanced logistics hub in sub-Saharan Africa by commanding an estimated 22.5% share of the MEA freight logistics market in 2024. Its strategic location, coupled with the most developed transport infrastructure on the continent, positions it as a gateway for landlocked neighbors, including Botswana, Zimbabwe, and Zambia. The Port of Durban, Africa’s busiest container terminal, handles over 3 million TEUs annually, as per the Transnet National Ports Authority. However, operational inefficiencies persist, with container dwell times averaging an increase in 2023. Despite these challenges, South Africa remains a magnet for logistics FDI, with companies like DSV and DB Schenker establishing regional distribution centers. The country’s integrated rail-road-port network, though under strain, is reinforcing its centrality in regional trade flows.

Egypt Logistics Market Analysis

Egypt has emerged as a pivotal logistics node in North Africa and the Eastern Mediterranean. Its geographic advantage, bridging Africa, Europe, and Asia via the Suez Canal, enables Egypt to serve as a global transshipment hub. The Suez Canal handles a large number of vessels, generating a substantial amount of revenue, while the adjacent East Port Said Industrial Zone hosts manufacturing and logistics firms. The government’s Vision 2030 includes investment in logistics infrastructure, including the expansion of dry ports and digital customs systems. With rising industrial output and a population of over 110 million, domestic freight demand is expanding at 7% annually, further solidifying Egypt’s logistical significance.

Kenya Logistics Market Analysis

Kenya holds a dominant position in East Africa’s freight logistics landscape. As a maritime gateway for the region, Kenya’s port of Mombasa handles over 25 million tons of cargo annually, serving Uganda, Rwanda, South Sudan, and eastern DRC. The Standard Gauge Railway (SGR), linking Mombasa to Nairobi and Naivasha, has increased freight capacity per year. Despite delays in full implementation, the corridor has reduced transit time to Kampala. Nairobi’s emergence as a regional air cargo hub underscores Kenya’s role in high-value and perishable freight movement.

Ethiopia Logistics Market Analysis

Ethiopia has rapidly ascended as a logistics powerhouse in the Horn of Africa. Despite being landlocked, Ethiopia’s state-led industrialization strategy has prioritized logistics infrastructure to support export-oriented manufacturing. The Addis Ababa–Djibouti Railway, inaugurated in 2018, now transports over 5 million tons of freight annually, reducing cargo transit time from 3 days to 12 hours, according to Ethiopian Railways Corporation. With over 20 industrial parks operational, including Hawassa and Bole Lemi, freight demand for raw materials and finished goods has surged. Ethiopian Airlines Cargo, Africa’s largest air freight carrier, is reinforcing the country’s multimodal logistics ambition.

Nigeria Logistics Market Analysis

Nigeria commands a substantial share of the MEA freight logistics market, which is driven by its status as Africa’s most populous nation and largest economy. With over 210 million people and a GDP exceeding $470 billion in 2023, domestic freight demand is immense, particularly for consumer goods, construction materials, and petroleum products. The Lagos port complex handles millions of tons of cargo annually, though congestion remains a challenge, with vessels waiting multiple days. The Federal Government’s concession of port operations to private operators like Lekki Deep Sea Port aims to increase capacity and efficiency. The rise of e-commerce is reshaping last-mile delivery dynamics, positioning Nigeria as a high-potential, albeit complex, logistics frontier.

COMPETITIVE LANDSCAPE

The competition in the Africana freight logistics market is intensifying as global and regional players navigate a complex landscape of infrastructure disparities, regulatory fragmentation, and rising trade demand. Multinational firms like DHL and Bolloré leverage scale and technology to dominate high-value corridors, while regional operators such as Transnet and Savannah Logistics exploit local expertise and cost efficiency. The market is characterized by strategic differentiation, with companies investing in digital platforms, green logistics, and specialized services like cold chain and hazardous cargo handling. Public-private partnerships are increasingly shaping competitive advantage, particularly in port and rail modernization. Although entry barriers remain high due to capital intensity, niche players are emerging with agile, tech-driven models. As AfCFTA accelerates intra-African trade, competitive dynamics are shifting toward integrated, compliant, and resilient supply chain solutions.

KEY MARKET PLAYERS

These are the market players that are dominating the African freight logistics market

- DHL

- Aramex

- Kuehne + Nagel

- United Parcel Service Inc.

- RAK Logistics

- Al-Futtaim Logistics

- Agility Logistics

- Saudi Transport & Investment Co. (Mubarrad)

- Almajdouie Group

- Ceva Logistics

- Gulf Agency,

- Company (GAC)

Top Players In The Market

- DHL Supply Chain & Global Forwarding operates as a dominant force in Africa’s freight logistics landscape, delivering end-to-end solutions across air, sea, road, and contract logistics. The company has intensified its footprint through localized infrastructure investments. DHL has also expanded cold chain capabilities in Kenya and Ghana to support pharmaceutical and agricultural exports, aligning with AfCFTA trade facilitation goals. In 2024, it deployed AI-driven route optimization tools across Nigeria and Egypt, enhancing delivery precision. Its integration of digital freight platforms and strategic partnerships with African customs authorities has strengthened compliance efficiency. By investing in green logistics, including electric delivery vehicles in Cape Town and Nairobi, DHL is positioning itself at the forefront of sustainable supply chain innovation across the continent.

- Bolloré Africa Logistics maintains a deeply entrenched presence across Sub-Saharan Africa, managing multimodal transport, port operations, and inland logistics through an extensive regional network. The company operates in over 45 African countries, leveraging its ownership of rail and port assets in West and Central Africa to streamline cargo movement. In 2023, Bolloré launched a digital customs clearance platform in Cameroon, reducing processing time by 40%, as verified by the Central African Economic and Monetary Community. It has also upgraded its dry port facilities in Abidjan and Douala to handle growing containerized trade. Despite divesting some port concessions, the company continues to invest in intermodal connectivity, including a new rail-linked terminal in Niamey in 2024. Its focus on integrated logistics—combining shipping, warehousing, and regulatory compliance—enables seamless cross-border operations, particularly in landlocked regions dependent on corridor efficiency.

- Grindrod Limited is a South Africa-based logistics and freight management company with a specialized focus on southern and eastern African trade corridors. It provides freight forwarding, port operations, rail haulage, and warehousing services, with a strong emphasis on bulk and break-bulk cargo. In 2023, Grindrod expanded its fleet of locomotives on the Maputo Corridor, enhancing capacity for coal and container transport between South Africa and Mozambique. The company also launched a digital freight exchange platform in 2024 to improve truck utilization and reduce empty return trips. Its investment in the Port of Ngqura aims to decongest Durban and offer an alternative gateway for regional trade. Grindrod’s deep integration with mining and energy sectors, combined with its push toward digitalization and operational transparency, strengthens its role in supporting resource-driven freight movements across the SADC region.

Top Strategies Used By Key Market Participants

Key players in the African freight logistics market are deploying multimodal integration, digital transformation, strategic partnerships, corridor optimization, and sustainability initiatives to consolidate their positions. Companies are investing in intermodal networks that link ports, railways, and inland depots to reduce transit times and dependency on road transport. Digitalization is a core focus, with firms adopting AI-powered logistics platforms, blockchain for customs documentation, and IoT-enabled tracking to enhance visibility. Strategic alliances with governments and regional economic communities facilitate access to trade corridors and regulatory reforms. Expansion into high-growth sectors such as e-commerce and pharmaceuticals is driving last-mile innovation. Additionally, green logistics strategies—including electric fleets and energy-efficient warehouses—are being implemented to meet ESG goals and reduce operational costs, ensuring long-term competitiveness in a fragmented yet rapidly evolving market.

RECENT MARKET NEWS

- In March 2023, DHL launched a $100 million logistics hub in Johannesburg, enhancing warehousing and distribution capabilities for Southern Africa and integrating AI-driven inventory management to improve supply chain responsiveness and support expanding e-commerce and healthcare logistics demand.

- In July 2023, Bolloré Africa Logistics introduced a digital customs clearance platform in Cameroon, reducing cargo processing time by 40% and improving cross-border freight efficiency across the Central African region, thereby strengthening compliance and transit reliability.

- In November 2023, Grindrod Limited expanded its locomotive fleet on the Maputo Corridor, increasing rail capacity for bulk cargo between South Africa and Mozambique and improving supply chain resilience for mining and energy sector clients.

- In January 2024, Maersk inaugurated a new inland container depot in Kigali, Rwanda, linked to the Mombasa port via digital freight corridors, enabling faster cargo clearance and reducing transit time for landlocked East African markets.

- In May 2024, Ethiopian Airlines Cargo launched three dedicated freighters for intra-African routes connecting Addis Ababa to Accra, Lagos, and Dar es Salaam, significantly boosting air cargo capacity for perishable and high-value goods across the continent.

MARKET SEGMENTATION

This research report on the African freight logistics market is segmented and sub-segmented into the following categories.

By Function Type

- Freight Transport

- Road

- Water

- Air

- Rail

- Freight Forwarding

- Warehousing

- Value-added Services and Other Functions

By End-User Insights

- Manufacturing and Automotive

- Oil and Gas, Mining, and Quarrying

- Agriculture, Fishing, and Forestry

- Construction

- Distributive Trade (Wholesale and Retail Segments - FMCG Included)

- Other End Users (Telecommunications and Pharmaceuticals)

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- South Africa

- Rest of Africa

Frequently Asked Questions

What is the current state of the Africa freight logistics market?

The African freight logistics sector is rapidly evolving, driven by regional trade integration and infrastructure upgrades. Challenges like border delays persist, but digital solutions are improving efficiency.

Which countries lead in logistics performance in Africa?

South Africa, Kenya, and Morocco rank highest due to better port infrastructure and regulatory clarity. These hubs serve as gateways for regional distribution and international trade.

How is the African Continental Free Trade Area (AfCFTA) impacting freight?

AfCFTA is boosting cross-border cargo movement by reducing tariffs and standardizing trade rules. Logistics providers are expanding networks to meet rising intra-African demand.

What are the main transport modes in African freight?

Road transport dominates due to flexibility, while rail and inland waterways are underutilized but seeing renewed investment. Air freight is limited but vital for high-value, time-sensitive goods.

What challenges do logistics companies face in Africa?

Fragmented regulations, poor road conditions, and port congestion increase costs and delays. Limited cold chain infrastructure also hampers perishable goods transport.

How is technology transforming African freight logistics?

Mobile tracking, digital freight platforms, and GPS-enabled fleets are enhancing visibility and coordination. Startups are introducing on-demand trucking and automated customs clearance tools.

What role do ports play in Africa’s freight network?

Major ports like Durban, Mombasa, and Lagos are critical import-export nodes, though inefficiencies remain. Modernization projects aim to reduce turnaround times and boost capacity.

How important is last-mile delivery in African logistics?

Last-mile delivery is a growing focus, especially with e-commerce rising in urban centers. Companies are using local agents and motorbike fleets to navigate congested city routes.

Are sustainable logistics practices emerging in Africa?

Yes—some firms are piloting electric delivery vehicles and solar-powered warehouses. Fuel efficiency and reduced emissions are becoming priorities in fleet management.

What’s the growth outlook for Africa’s freight logistics market?

The market is projected to grow at over 7% annually, fueled by urbanization, industrialization, and stronger regional trade. Investors are increasingly eyeing logistics as a strategic sector.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com