Africa Zero Liquid Discharge System Market Size, Share, Trends, COVID-19 Impact & Growth Analysis Report – Segmented By Type (Conventional Zero Liquid Discharge Systems, Hybrid Zero Liquid Discharge Systems), End-User Industry & Country (South Africa, Nigeria, Rest of Africa) - Industry Analysis From 2026 to 2034

Market Size, 2025

$0.24 BnMarket Estimate, 2026

$0.26 BnMarket Forecast, 2034

$0.46 BnCAGR, 2026–2034

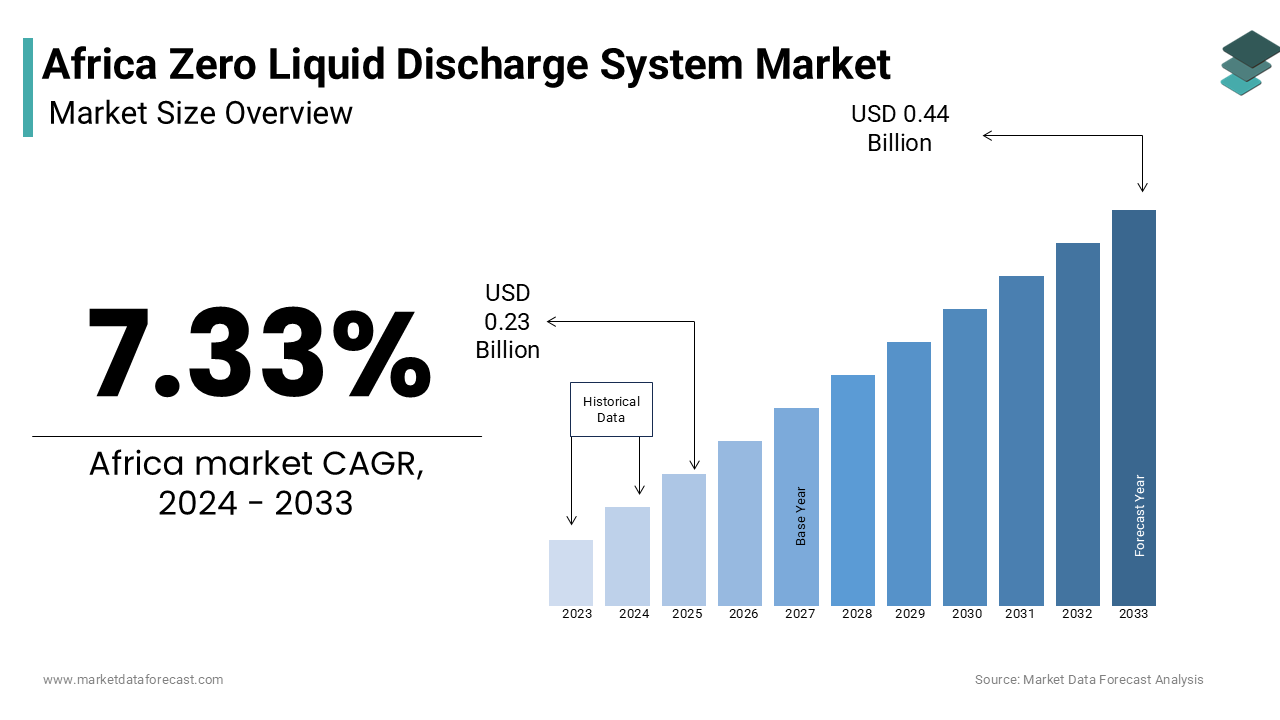

7.33%Africa Zero Liquid Discharge System Market Size

The Africa zero liquid discharge system market size was valued at USD 0.24 billion in 2025 and is anticipated to reach USD 0.26 billion in 2026 from USD 0.46 billion by 2034, growing at a CAGR of 7.33% during the forecast period from 2026 to 2034.

Zero liquid discharge (ZLD) system refers to the deployment of advanced wastewater treatment technologies designed to completely eliminate liquid effluent discharge by recovering and recycling water while concentrating dissolved solids into solid waste. These systems integrate processes such as reverse osmosis, evaporation, crystallization, and electrodialysis to enable industrial facilities to comply with environmental regulations and optimize water use in water-scarce regions. As of 2023, over 300 million people in sub-Saharan Africa live under high or extreme water stress, according to the World Resources Institute, making water recovery technologies increasingly critical. The mining, power generation, and chemical manufacturing sectors, particularly in South Africa, Namibia, and Botswana, are leading adopters due to stringent environmental mandates. According to the African Development Bank, only 12% of industrial wastewater in Africa undergoes proper treatment, underscoring the urgency for closed-loop water systems. ZLD is emerging not merely as a compliance tool but as a strategic asset in sustainable industrial development across the continent.

MARKET DRIVERS

Escalating Water Scarcity in Industrial Zones Driving Water Reuse Imperatives

Chronic water scarcity in key industrial corridors is compelling heavy industries to adopt zero liquid discharge systems as a means of securing operational continuity. Southern Africa, home to major mining and energy projects, experiences some of the lowest per capita water availability on the continent. According to the United Nations Environment Programme, South Africa’s annual water availability has declined to 470 cubic meters per person, well below the 500 cubic meter threshold for absolute scarcity. In the Waterberg Coalfield and Vaal River Industrial Basin, where power plants and coal-to-liquids facilities operate, freshwater access is increasingly contested. These cases illustrate how hydrological constraints are transforming ZLD from an environmental option into an operational necessity.

Strengthening Environmental Regulations and Industrial Effluent Standards

Governments across Africa are tightening industrial wastewater discharge regulations in response to deteriorating water quality and ecosystem degradation. These regulatory shifts are institutionalizing ZLD as a prerequisite for industrial licensing, particularly in mining, textiles, and petrochemicals.

MARKET RESTRAINTS

High Capital and Operational Costs Limiting Adoption in Developing Economies

The deployment of zero liquid discharge systems remains constrained by their substantial financial requirements, which many African industrial operators cannot sustain. In countries like Zambia, where industrial electricity tariffs exceed $0.18 per kWh, nearly double the global average, energy consumption becomes a prohibitive factor. Like, a portion of medium-sized manufacturers in East Africa cited high utility costs as a primary barrier to adopting advanced water treatment technologies. Additionally, the scarcity of local engineering expertise increases reliance on foreign contractors, further inflating lifecycle expenses. As per the African Development Bank, only limited share of industrial water treatment projects in sub-Saharan Africa include ZLD components due to cost concerns, despite regulatory pressure, indicating that economic viability remains a critical bottleneck.

Limited Availability of Skilled Personnel for System Operation and Maintenance

The technical complexity of ZLD systems necessitates specialized engineering and chemical management expertise, which is in acute shortage across much of Africa. Operators must manage multi-stage processes including brine concentrators, crystallizers, and membrane systems, requiring continuous monitoring to prevent scaling, fouling, and equipment failure. According to the International Labour Organization, Africa has only 80 engineers per million people, compared to 1,000 per million in high-income nations, severely limiting technical workforce capacity. In Ethiopia, where ZLD adoption is nascent, there are fewer professionals are certified in advanced wastewater management. This skills gap leads to suboptimal system performance, increased maintenance costs, and reluctance among investors to commit to long-term ZLD projects. Without institutionalized training programs and knowledge transfer, technological adoption will remain fragmented and inefficient.

MARKET OPPORTUNITIES

Integration of Renewable Energy to Reduce ZLD Operational Costs

The convergence of ZLD systems with renewable energy presents a transformative opportunity to overcome energy cost barriers. Solar and wind power can offset the high electricity demand of evaporation and reverse osmosis units, particularly in sun-rich regions like the Kalahari and Sahel. According to the International Renewable Energy Agency, solar photovoltaic costs in Africa have declined, making hybrid systems increasingly viable. As per the African Union’s Renewable Energy Cooperation Framework, many industrial zones across the continent are slated for renewable-powered water treatment infrastructure, positioning hybrid ZLD as a scalable model for sustainable industrialization.

Expansion of ZLD in Emerging Mining and Desalination Hubs

The rapid development of mineral extraction and seawater desalination projects across Africa is creating new demand centers for zero liquid discharge technology. With the global energy transition driving demand for cobalt, lithium, and manganese, new mining ventures in the Democratic Republic of Congo, Zimbabwe, and Namibia are being designed with closed-loop water systems from inception. Like, coastal nations are investing in desalination, which generates concentrated brine requiring ZLD treatment.

MARKET CHALLENGES

Disposal and Management of Solid Residual Waste from ZLD Systems

While ZLD eliminates liquid discharge, it generates solid waste streams such as crystallized salts and sludge, whose safe disposal remains a critical environmental challenge. In Namibia, the Rössing Uranium Mine stores crystallized waste in lined evaporation ponds, but long-term stability remains uncertain due to seismic and climatic risks. Without standardized protocols for reuse, such as salt recovery for industrial input or construction materials, ZLD risks merely shifting pollution from water to land, undermining its sustainability claims.

Intermittent Energy Supply Undermining System Efficiency

The reliability of ZLD operations is heavily dependent on uninterrupted power, a condition often unmet in African industrial zones. Frequent grid outages disrupt evaporation and membrane processes, leading to scaling, fouling, and system failure. According to the International Energy Agency, only 45% of sub-Saharan Africa’s industrial facilities have access to reliable electricity, making energy resilience a prerequisite for ZLD viability. Until energy infrastructure improves, hybrid systems with on-site generation will be essential, adding complexity and cost to deployment.

SEGMENTAL ANALYSIS

By Type Insights

The conventional zero liquid discharge systems segment held a dominant 68.3% share of the Africa ZLD market in 2024. This dominance is primarily sustained by their established engineering frameworks and familiarity among industrial operators, particularly in long-standing sectors such as power generation and mining. These systems typically employ multi-stage processes including brine concentrators, thermal evaporators, and crystallizers, technologies that have been in use for decades in South Africa’s coal-fired power plants and mineral processing facilities. The predictability of performance and availability of technical documentation make conventional systems the default choice for regulatory compliance in high-risk industrial zones. A further key factor reinforcing the dominance of conventional systems is the limited availability of modular, plug-and-play alternatives in African supply chains. Local engineering firms are more experienced in constructing and maintaining thermal-based evaporation units than in deploying advanced membrane hybrids. Furthermore, financing institutions such as the Development Bank of Southern Africa prefer conventional technologies due to their proven track record, making them more likely to approve capital for such projects.

The hybrid zero liquid discharge systems segment is emerging as the fastest-growing and is projected to expand at a CAGR of 14.6% from 2025 to 2033. This acceleration is driven by the urgent need to reduce the energy intensity of traditional ZLD operations. Hybrid systems integrate membrane-based technologies such as reverse osmosis, forward osmosis, and electrodialysis with thermal processes, significantly lowering evaporation loads and cutting energy consumption. A different driver is the increasing deployment of hybrid systems in greenfield industrial parks where sustainability benchmarks are embedded from inception. Their modular design also allows phased deployment, making them more accessible to mid-sized enterprises with constrained capital budgets.

By End-Use Industry Insights

The energy and power sector led the market by securing 54.2% of the Africa ZLD market in 2024. This lead position is due to the sector’s high water consumption and concentrated presence in arid regions where effluent regulations are most stringent. Coal-fired power plants, in particular, generate large volumes of flue gas desulfurization (FGD) wastewater containing sulfates, chlorides, and heavy metals, necessitating advanced treatment. Regulatory mandates further reinforce adoption. Additionally, the push for mine-mouth power plants, built near coal reserves in dry regions, has made water recycling an operational necessity, ensuring the energy sector remains the primary driver of ZLD demand across the continent.

The chemicals and petrochemicals sector is the fastest-growing end-user of ZLD systems in Africa and is expanding at a CAGR of 13.9% from 2025 to 2033. This growth is fueled by the expansion of industrial zones dedicated to specialty chemicals, fertilizers, and polymer manufacturing, particularly in Egypt, Nigeria, and Algeria. These processes generate highly saline and toxic effluents containing ammonia, nitrates, and organic solvents, which cannot be discharged under new environmental codes. A further catalyst is the rise of gas-to-chemicals projects that require closed-loop water systems.

REGIONAL ANALYSIS

South Africa Zero Liquid Discharge System Market Analysis

South Africa spearheaded the MEA ZLD market at 31.2% and is distinguished by its mature regulatory framework and concentration of water-intensive industries. As the continent’s most industrialized economy, it hosts major coal-fired power plants, platinum mines, and chemical facilities, all operating under strict water discharge laws. However, aging infrastructure and energy instability challenge consistent operation, requiring upgrades and hybrid retrofits to maintain compliance in an era of escalating water stress.

Egypt Zero Liquid Discharge System Market Analysis

Egypt commands a significant share of the MEA ZLD market, leveraging its strategic location and expanding industrial base to drive demand for closed-loop water systems. The country’s rapid development of petrochemical complexes along the Suez Canal Economic Zone has necessitated advanced wastewater treatment, with the Tahrir and Dabaa projects incorporating ZLD from inception. Thus, the country is positioning itself as a model for integrated water stewardship in arid economies.

Algeria Liquid Discharge System Market Analysis

Algeria holds a notable share of the MEA ZLD market which is emerging as a key player due to its vast hydrocarbon reserves and growing downstream chemical manufacturing. The country’s Sonatrach-led industrial expansion includes new gas-to-chemicals and urea fertilizer plants in Hassi Messaoud and Skikda, all of which generate high-salinity wastewater unsuitable for discharge. Despite bureaucratic delays, the country’s state-led industrial model ensures centralized investment in water sustainability, positioning it as a rising ZLD market in North Africa.

Nigeria Liquid Discharge System Market Analysis

Nigeria IS representing a high-growth opportunity constrained by infrastructure and enforcement challenges. The Dangote Refinery, Africa’s largest, has commissioned a full-scale ZLD system capable of recycling 98% of its process water, setting a precedent for future industrial projects. However, implementation remains inconsistent. The country’s unreliable power supply and lack of skilled operators further hinder adoption.

Morocco Liquid Discharge System Market Analysis

Morocco is distinguished by its proactive environmental policies and integration of water reuse into industrial planning. The country’s Green Growth Strategy mandates that all new industrial zones achieve 50% water recycling by 2030, with hybrid ZLD systems favored for energy efficiency. Solar-powered ZLD pilots in Boujdour and Laâyoune have reduced energy costs, aligning with Morocco’s renewable energy leadership.

MARKET SEGMENTATION

This research report on the Africa Zero Liquid Discharge System Market is segmented and sub-segmented into the following categories.

By Type

- Conventional Zero Liquid Discharge Systems

- Hybrid Zero Liquid Discharge Systems

By End-Use Industry

- Energy & Power

- Chemicals & Petrochemicals

By Country

- South Africa

- Nigeria

- Rest of Africa

Frequently Asked Questions

What is driving the growth of the Africa Zero Liquid Discharge (ZLD) system market?

The growth is driven by stringent wastewater discharge regulations, water scarcity in arid regions, and the need for sustainable water management in industries such as power, mining, and chemicals.

What are the key challenges for the ZLD market in Africa?

High capital costs, energy-intensive processes, limited local expertise in hybrid systems, and financing barriers remain major challenges.

What is the outlook for the Africa ZLD market?

The market is expected to grow significantly as industries shift from conventional to hybrid systems, with rising investments in sustainable industrial parks and stricter regulatory frameworks.

How does water scarcity influence ZLD adoption in Africa?

With many African regions facing acute water stress, industries are compelled to recycle and reuse wastewater through ZLD to sustain operations.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com