Global Aircraft Electrification Market Size, Share, Trends, & Growth Forecast Report, Segmented by Platform (Commercial Aircraft, Military Aircraft, and General Aviation), Technology (More Electric, Hybrid Electric, and Fully Electric), Application (Power Generation, Power Distribution, Power Conversion, and Energy Storage), System (Propulsion Systems, Aircraft Systems), Component (Batteries, Fuel Cells, Solar Cells, Electric Actuators, Electric Pumps, Generators, Motors, Power Electronics, and Distribution Devices), & Region (North America, Latin America, Asia Pacific, Europe, Middle East and Africa), Industry Forecast From 2026 to 2034

Global Aircraft Electrification Market Size

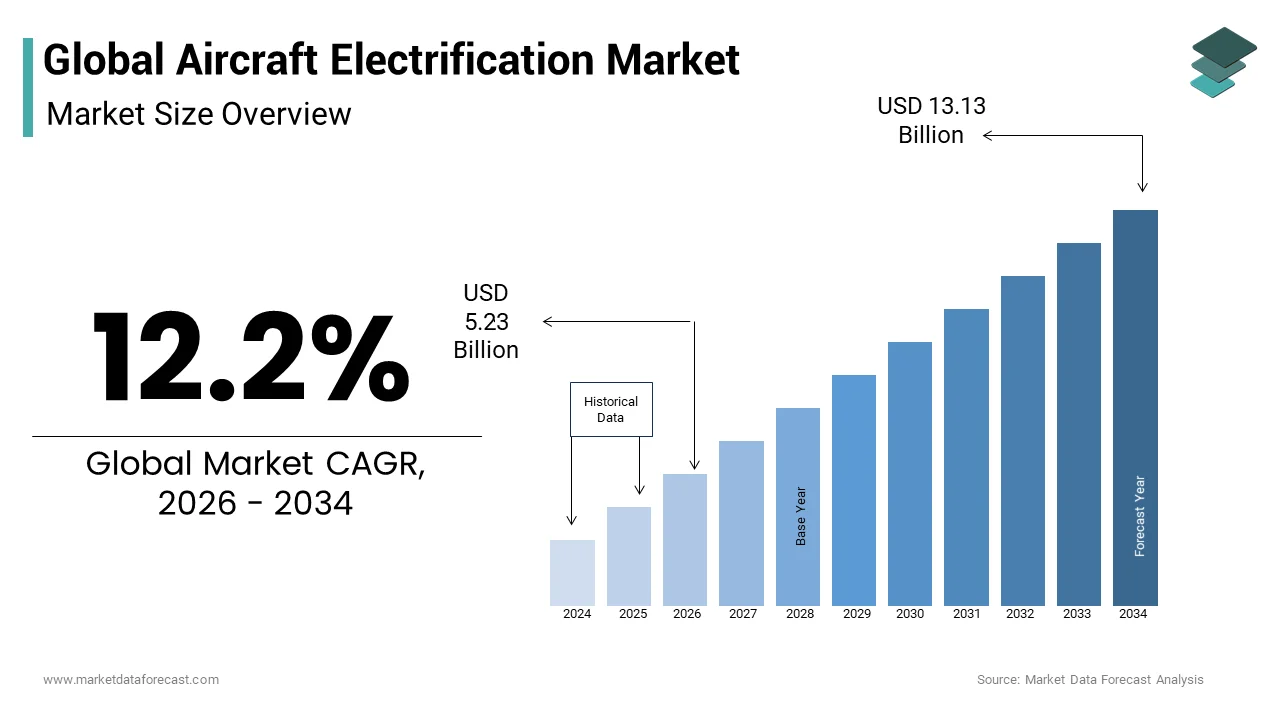

The global aircraft electrification market size was valued at USD 4.66 billion in 2025 and is anticipated to reach USD 5.23 billion in 2026 to reach USD 13.13 billion by 2034, growing with a compound annual growth rate of 12.2% during the forecast period from 2026 to 2034.

Aircraft electrification refers to a sector focused on the integration of electric power systems into aviation for propulsion, auxiliary power units, and onboard energy management. This technological shift encompasses a spectrum from hybrid-electric propulsion systems to fully electric aircraft, aiming to reduce emissions, improve fuel efficiency, and lower operational costs. Also, the global push toward sustainable aviation has positioned aircraft electrification at the forefront of aerospace innovation.

According to the International Air Transport Association (IATA), the aviation sector contributes nearly 2.5% of global CO₂ emissions, prompting regulators, airlines, and manufacturers to explore cleaner alternatives. In response, the European Union’s Clean Aviation Joint Undertaking and NASA’s X-57 Maxwell project are spearheading research initiatives aimed at advancing electric flight technologies.

Additionally, with urban air mobility (UAM) and regional commuter aircraft emerging as early adopters, the aircraft electrification market is undergoing rapid transformation. However, while progress is evident, the path to widespread adoption remains complex, requiring breakthroughs in battery technology, regulatory alignment, and infrastructure development.

MARKET DRIVERS

Growing Demand for Sustainable Aviation Solutions

A major factor contributing to the aircraft electrification market is the increasing demand for sustainable aviation solutions amid mounting environmental concerns.

As per the International Council on Clean Transportation (ICCT), commercial aviation accounts for a significant portion of greenhouse gas emissions, prompting governments and regulatory bodies worldwide to implement stringent emission reduction targets. In response, airlines and aircraft manufacturers are actively exploring electric and hybrid-electric propulsion systems as viable alternatives to conventional jet engines.

According to the European Union Aviation Safety Agency (EASA), over 200 electric aircraft development programs were underway globally in 2023, with a majority focused on short-haul and urban air mobility applications.

Apart from that, industry leaders such as Airbus and Rolls-Royce have committed to achieving net-zero carbon emissions by 2050, further reinforcing the shift toward electrified propulsion. The growing consumer preference for eco-friendly travel options and corporate sustainability mandates are also influencing fleet modernization strategies, accelerating the adoption of electric aircraft technologies across key markets.

Advancements in Battery and Energy Storage Technologies

Rapid advancements in battery and energy storage technologies represent another critical driver of the aircraft electrification market.

As per the U.S. Department of Energy (DOE), lithium-ion battery energy density has improved by more than 50% over the past decade, enhancing the feasibility of electric propulsion for smaller aircraft. Solid-state batteries, which promise higher energy densities, faster charging capabilities, and improved safety profiles, are also gaining traction among aerospace firms.

According to a report by the Fraunhofer Institute for Material and Beam Technology, several European startups and research institutions are developing lightweight, high-capacity battery packs specifically designed for aviation use.

Moreover, companies like Siemens and Magnix are integrating these advanced energy storage solutions into prototype electric aircraft, demonstrating promising performance metrics in test flights. As government agencies and private investors continue to fund battery innovation programs, the pathway to scalable, high-efficiency aircraft electrification becomes increasingly viable, driving sustained market growth.

MARKET RESTRAINTS

Limitations in Current Battery Performance and Range Capabilities

Current limitations in energy density and range remain significant restraints for the aircraft electrification market.

According to the National Aeronautics and Space Administration (NASA), existing lithium-ion batteries offer only about one-fiftieth of the energy content per unit weight compared to conventional jet fuel, severely restricting payload capacity and flight duration. Also, most all-electric aircraft currently under development are limited to short-range flights of less than 150 kilometers, making them unsuitable for long-haul commercial operations.

Furthermore, solid-state battery technology, though promising, is still in its infancy and faces challenges related to cost, scalability, and thermal management in extreme flight conditions. These technical constraints hinder widespread adoption and necessitate continued investment in next-generation energy storage solutions.

High Development and Certification Costs

The high costs associated with research, development, and certification of electric aircraft systems pose a major barrier to market expansion.

According to the Aerospace Technology Institute (ATI), developing a new electric propulsion system can require investments exceeding $1 billion, including extensive testing and compliance with evolving airworthiness standards. Unlike traditional aviation components, electric propulsion systems must undergo rigorous validation for electromagnetic interference, thermal stability, and fault tolerance, adding complexity and time to certification processes.

As per the Federal Aviation Administration (FAA), certifying an all-electric or hybrid-electric aircraft involves unprecedented regulatory scrutiny due to the novelty of integrated powertrain architectures and software controls. Also, start-ups and small manufacturers often struggle to secure funding for these extensive requirements, limiting their ability to compete with established aerospace giants. Consequently, despite strong interest and innovation potential, financial and regulatory hurdles continue to slow down the pace of commercialization in the aircraft electrification market.

MARKET OPPORTUNITIES

Expansion of Urban Air Mobility (UAM) and Regional Electric Flights

Urban Air Mobility (UAM) and regional electric flights present one of the most promising opportunities for the aircraft electrification market.

As per the World Economic Forum (WEF), cities worldwide are exploring vertical takeoff and landing (VTOL) electric aircraft as a solution to urban congestion and last-mile transportation inefficiencies. Companies like Joby Aviation, Lilium, and Vertical Aerospace have unveiled prototypes for air taxis capable of operating within metropolitan areas, supported by growing investor confidence and regulatory discussions around airspace integration.

In addition, regional airlines are piloting all-electric commuter aircraft for routes under 1,000 kilometers, offering a cost-effective alternative to conventional turboprops. With airports and municipalities planning dedicated vertiports and charging infrastructure, this segment is expected to drive substantial demand for electric propulsion systems, power electronics, and battery management solutions.

Increasing Government Funding and Policy Support for Green Aviation Initiatives

An additional significant opportunity lies in the growing government support for green aviation through policy incentives and funding programs.

As per the European Commission’s Clean Aviation initiative, over €1.7 billion has been allocated to accelerate the development of hybrid-electric and hydrogen-powered aircraft technologies. Similarly, the U.S. Department of Energy (DOE) and NASA have launched collaborative projects to advance battery performance and lightweight materials tailored for aviation use. According to the UK Aerospace Technology Strategy, national grants are being provided to SMEs and academic institutions involved in electric propulsion research, fostering innovation ecosystems. Additionally, countries like Norway and Sweden have set ambitious targets for zero-emission domestic flights by 2030 and 2045, respectively, creating a conducive environment for electric aircraft adoption. As regulatory frameworks evolve and subsidies become more accessible, public-private partnerships are expected to play a pivotal role in shaping the future of aircraft electrification.

MARKET CHALLENGES

Regulatory Uncertainty and Lack of Standardized Certification Protocols

A critical challenge confronting the aircraft electrification market is the absence of standardized certification protocols and evolving regulatory frameworks.

According to the International Civil Aviation Organization (ICAO), current airworthiness regulations are largely based on legacy propulsion systems, leaving gaps in how to assess the safety and reliability of electric powertrains. As noted by the Federal Aviation Administration (FAA), certifying novel components such as distributed propulsion systems, high-voltage wiring, and autonomous flight controls introduces complexities that traditional certification models do not account for.

This lack of harmonization increases development timelines and costs for manufacturers, particularly smaller players seeking to enter the market. Without clear, globally aligned standards, the deployment of electric aircraft at scale may face prolonged delays and inconsistent regulatory interpretations.

Integration Challenges with Existing Aviation Infrastructure and Operations

Integrating electric aircraft into existing aviation infrastructure and operational workflows presents another formidable challenge.

According to the International Air Transport Association (IATA), current airport facilities are primarily designed around fossil fuel-based logistics, lacking the necessary charging stations, maintenance bays, and battery swap capabilities required for electric fleets. As per the Airport Operators Association (AOA), retrofitting existing terminals and runways to accommodate electric aircraft entails significant capital expenditure, which many regional airports may find unfeasible.

Also, the need for specialized technician training, grid upgrades, and battery recycling facilities further complicates large-scale adoption. Until these infrastructure and logistical barriers are systematically addressed, the transition to electrified aviation will remain constrained to niche applications rather than mainstream commercial fleets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.2% |

| Segments Covered | By Application, System, Platform, Technology, Component, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | GE Aviation (US), Raytheon Company (US), AMETEK (US), Meggitt PLC (UK), BAE Systems (UK), Honeywell International Inc. (US), Safran (France), Thales Group (France), United Technologies Corporation (US), Radiant Power Corporation (US) |

SEGMENTAL ANALYSIS

By Platform Insights

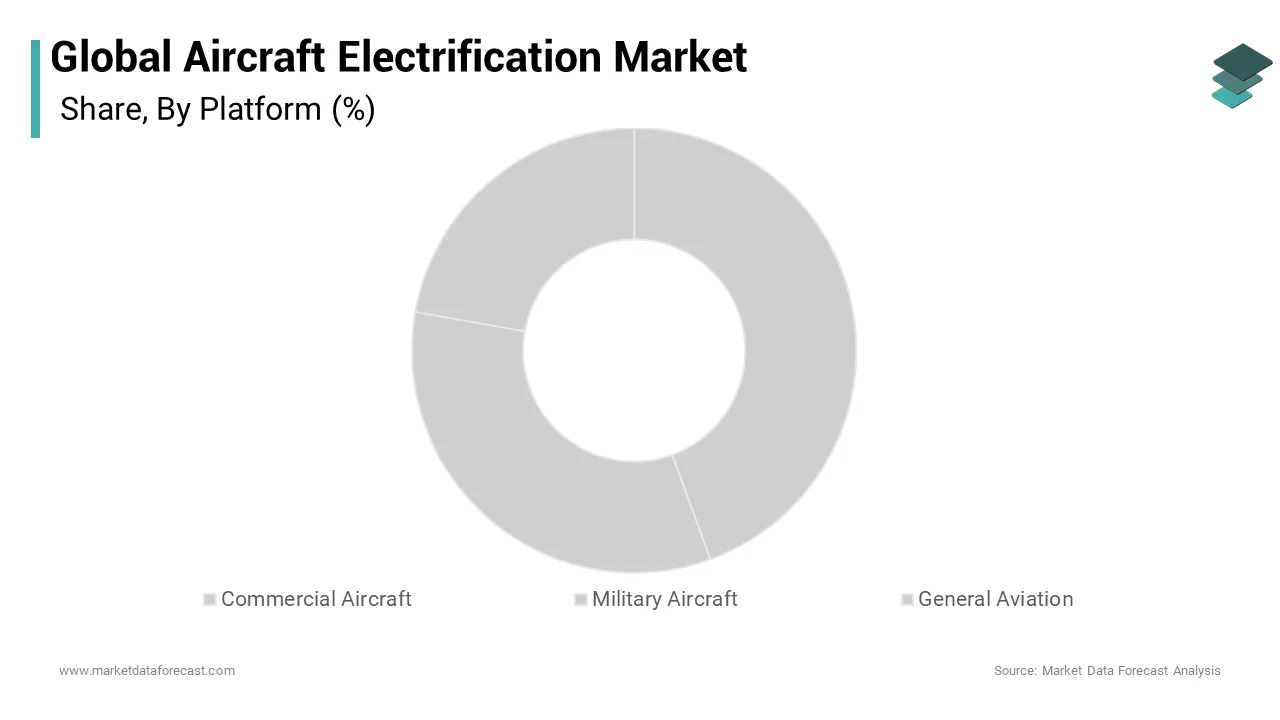

Commercial Aircraft

The commercial aircraft segment was at the forefront with a 50.7% share in the global aircraft electrification market in 2024. This dominance is primarily driven by the urgent need for sustainable aviation solutions in response to stringent environmental regulations and rising fuel costs.

As per the International Air Transport Association (IATA), commercial airlines are responsible for nearly 2.5% of global CO₂ emissions, prompting industry leaders to adopt more electric and hybrid-electric propulsion systems as part of their decarbonization strategies. Major manufacturers like Airbus, Boeing, and Rolls-Royce are investing heavily in electrified flight technologies, with programs such as E-Fan X and VoltAir leading the way. Moreover, the increasing development of urban air mobility (UAM) vehicles—many of which fall under the commercial aircraft umbrella—is further reinforcing this segment’s leadership.

General Aviation

General aviation is projected to grow at the fastest CAGR, exceeding 12% in the coming years, due to its early adoption of all-electric propulsion systems and favorable regulatory flexibility compared to larger commercial aircraft.

As per the European Business Aviation Association (EBAA), the general aviation sector includes small private planes, training aircraft, and experimental electric flight demonstrators, many of which are well-suited for electrification due to their lower power requirements and shorter mission profiles. Companies like Pipistrel, Bye Aerospace, and Eviation are already delivering or testing all-electric aircraft models that are gaining traction among flight schools and eco-conscious private owners. The ability to rapidly prototype and deploy new technologies in this segment makes it a key testing ground for future advancements in electric propulsion, contributing to its accelerated growth trajectory.

By Technology Insights

More Electric Aircraft (MEA)

The more electric aircraft (MEA) segment grabbed the majority of the aircraft electrification market, capturing 60.5% of total revenue in 2024. This technology focuses on replacing traditional hydraulic and pneumatic systems with electrically powered alternatives, improving efficiency while maintaining compatibility with existing gas turbine engines.

As per the U.S. Air Force Research Laboratory (AFRL), MEA architectures are being integrated into next-generation fighter jets and transport aircraft to reduce weight, enhance reliability, and improve fuel efficiency. In commercial aviation, major OEMs like Boeing and Airbus have incorporated more electric systems into flagship models, where electric actuators, compressors, and braking systems are now standard features.

With ongoing upgrades in onboard power generation and distribution, this segment remains the most widely adopted form of aircraft electrification globally.

Fully Electric Aircraft

Fully electric aircraft are witnessing the highest growth rate, rising at a CAGR of nearly 14%. This rapid expansion is fueled by advancements in lightweight battery technology, government incentives, and growing interest from regional carriers and urban air mobility (UAM) operators.

According to McKinsey & Company, the fully electric propulsion system is particularly viable for short-range flights under 500 km, where zero-emission operation and reduced operating costs offer compelling advantages. As per the European Union Aviation Safety Agency (EASA), multiple all-electric aircraft prototypes have entered certification trials, including Eviation’s Alice and Heart Aerospace’s ES-19.

In addition, startups and research institutions across North America and Europe are pushing the boundaries of electric motor efficiency and energy storage density. With airports beginning to invest in charging infrastructure and regulatory bodies streamlining certification pathways, the fully electric aircraft segment is poised for substantial growth over the coming decade.

By Application Insights

Energy Storage

Energy storage constituted the biggest application segment in the aircraft electrification market in 2024, representing 40.8% of the total value. This superiority is because of the critical role batteries play in both hybrid-electric and fully electric aircraft configurations.

As per the Massachusetts Institute of Technology (MIT) Battery Lab, current lithium-ion battery packs used in aviation applications must meet rigorous safety and performance standards due to the high-vibration, low-pressure environment of flight. According to the U.S. Department of Energy (DOE), significant investments are being made in solid-state and lithium-sulfur battery technologies, which promise higher energy densities and improved thermal stability for aerospace use.

In addition to electric propulsion, energy storage supports auxiliary power units, avionics, and emergency backup systems, ensuring continuous functionality even during engine shutdown. According to Rolls-Royce’s Electrical Systems Division, the integration of modular battery packs into aircraft designs enables scalable electrification across different platform types.

Power Conversion

Power conversion is emerging as the booming application segment, expanding at a CAGR of around 11%. This growth is driven by the increasing complexity of onboard electrical systems, requiring efficient conversion between AC and DC power sources to support motors, actuators, and avionics.

As per the Fraunhofer Institute for Integrated Systems and Device Technology, modern aircraft electrification strategies rely heavily on advanced semiconductor-based converters that minimize energy losses and improve overall system efficiency. In hybrid-electric aircraft, power conversion units manage energy flow between generators, batteries, and propulsion motors, ensuring optimal performance across varying flight conditions. Also, the adoption of wide-bandgap semiconductors like silicon carbide (SiC) is enabling lighter, more compact power electronics capable of handling high voltages without compromising reliability. As aircraft manufacturers integrate more digital and autonomous systems, demand for robust and intelligent power conversion solutions continues to rise, positioning this segment for sustained expansion.

By Component Insights

Batteries

Batteries represented the largest component segment in the aircraft electrification market, accounting for 35.4% of the total value in 2024. This lead position is attributed to their central role in powering electric propulsion systems, onboard electronics, and auxiliary functions in both hybrid and all-electric aircraft.

As per the Argonne National Laboratory, lithium-ion battery technology has seen steady improvements in energy density, cycle life, and thermal management, making them increasingly viable for aerospace applications.

In addition, companies like Saft, Panasonic, and CATL are working closely with aerospace OEMs to design customized battery packs optimized for weight, safety, and longevity. According to Rolls-Royce Electrical, future aircraft may incorporate modular battery systems that allow for rapid swapping or recharging during turnaround times. As battery technology continues to evolve, this component segment will remain a driving force behind the broader electrification movement in aviation.

Power Electronics

Power electronics are witnessing the fastest growth in the aircraft electrification components market, expanding at a CAGR of approximately 13.2%. This surge is driven by the increasing demand for high-efficiency voltage regulation, frequency control, and signal processing in electric and hybrid-electric aircraft.

As per the IEEE Transactions on Aerospace and Electronic Systems, modern aircraft require sophisticated power electronic modules to manage bidirectional energy flows between generators, batteries, and propulsion motors. According to Infineon Technologies, the adoption of silicon carbide (SiC) and gallium nitride (GaN)-based semiconductors is enabling lighter, faster-switching power converters that enhance system reliability and reduce thermal losses. Apart from these, as aircraft become more digitally connected and autonomous, the need for real-time power monitoring and fault-tolerant electronics is accelerating innovation in this field. With ongoing developments in smart grid-like energy architectures, power electronics are becoming indispensable for next-generation electrified flight.

COUNTRY-LEVEL ANALYSIS

Germany Aircraft Electrification Market Analysis

Germany held the largest market share in Europe, contributing over 25% of total aircraft electrification activity. The country's strong industrial base, supported by leading manufacturers like Siemens, MTU Aero Engines, and Airbus Deutschland, positions it at the forefront of aviation electrification.

As per the Fraunhofer Institute for Manufacturing Engineering and Automation, Germany is home to numerous R&D initiatives focused on hybrid-electric propulsion, hydrogen fuel cells, and lightweight battery integration. Moreover, the federal government has committed significant funding through its National Innovation Program for Hydrogen and Fuel Cell Technology, supporting the development of zero-emission aircraft concepts. With major test centers in Oberpfaffenhofen and Hamburg, Germany plays a pivotal role in shaping Europe’s roadmap for sustainable aviation.

United Kingdom Aircraft Electrification Market Analysis

The UK is a hub for advanced propulsion research. The country benefits from a strong presence of academic and industry-led research institutions, including Cranfield University, the University of Cambridge, and Rolls-Royce.

Companies like Reaction Engines and Wright Electric are pioneering electric commuter aircraft and novel thermal management systems for electrified flight. Despite Brexit-related challenges, the UK remains a strategic hub for aerospace innovation, particularly in power electronics and propulsion system development.

France Aircraft Electrification Market Analysis

France is a major contributor to hybrid-electric development. The country is home to Airbus headquarters and a major center for Safran Group’s electrification R&D activities.

The Aerospace Valley cluster in Toulouse, France, hosts one of the most comprehensive ecosystems for electric flight development, spanning battery chemistry, motor design, and system integration. The French government, through the Direction Générale de l'Armement (DGA), supports defense-related electrification projects alongside civil aviation applications. According to ONERA, the French aerospace research agency, collaborative efforts between public labs and private firms are accelerating the maturity of hybrid-electric demonstrators. With a focus on regional aircraft electrification, France plays a crucial role in advancing clean aviation technologies across Europe.

Sweden Aircraft Electrification Market Analysis

Sweden is an emerging leader in all-electric flight in the European aircraft electrification market. The country has emerged as a leader in all-electric aircraft development, largely driven by companies like Heart Aerospace and Einride. Additionally, the Swedish government has set ambitious targets for fossil-free domestic flights by 2030, encouraging airlines to adopt electric aircraft for short-haul routes. Stockholm Arlanda Airport is also piloting dedicated charging infrastructure and operational protocols for electric aircraft. With a strong emphasis on sustainability and innovation, Sweden is carving out a niche in the global electric aviation landscape.

Spain Aircraft Electrification Market Analysis

Spain is seeing a growing focus on sustainable aviation infrastructure. The country is leveraging its strong aeronautics sector to develop electrification capabilities, particularly in power distribution and lightweight structural components. Barcelona and Seville host major manufacturing and R&D facilities for companies like Airbus and GMV, supporting the integration of electric systems into next-generation aircraft. Additionally, Spain’s participation in Clean Aviation Joint Undertaking programs is strengthening its position in sustainable aviation. With growing investment in green air mobility and charging networks, Spain is positioning itself as a key player in the electrification transition.

COMPETITIVE LANDSCAPE

The competition in the aircraft electrification market is intensifying as traditional aerospace leaders, emerging startups, and cross-industry innovators converge to redefine aviation’s future. Established players such as Airbus, Boeing, Rolls-Royce, and Siemens dominate due to their deep engineering expertise, robust supply chains, and access to capital. These companies are driving large-scale electrification projects that integrate into existing aircraft platforms and lay the groundwork for next-generation electric propulsion systems. However, nimble startups focused on urban air mobility and regional electric aircraft—such as Eviation, Heart Aerospace, and Lilium—are challenging conventional paradigms with disruptive designs and agile development cycles. Additionally, automotive and battery technology firms are entering the aerospace space, bringing fresh perspectives on powertrain design and energy storage. This evolving landscape fosters both collaboration and rivalry, prompting accelerated innovation while also raising questions about scalability, certification, and infrastructure readiness. As governments push for greener aviation alternatives, the competitive dynamics will continue to evolve, shaping the path toward widespread adoption of electrified flight across commercial, military, and general aviation sectors.

KEY MARKET PLAYERS

Some of the key market players of Aircraft Electrification market are:

- GE Aviation (US)

- Raytheon Company (US)

- Airbus SE

- AMETEK (US)

- Meggitt PLC (UK)

- Rolls-Royce Holdings plc

- Siemens Energy & Automation (Siemens AG)

- BAE Systems (UK)

- Honeywell International Inc. (US)

- Safran (France)

- Thales Group (France)

- United Technologies Corporation (US)

- Radiant Power Corporation (US)

- EaglePicher Technologies LLC (Canada)

- Astronics Corporation (US)

- Pioneer Magnetics (US)

- Carlisle Interconnect Technologies (US)

- Esterline Technologies (US)

- Crane Aerospace & Electronics (US)

- Hartzell Engine Technologies (US)

- PBS AEROSPACE (US)

- Nabtesco Corporation (Japan)

- Avionic Instruments, LLC (US)

Top Players In The Market

- Airbus is a global leader in aviation and plays a pivotal role in advancing aircraft electrification through its extensive R&D initiatives and strategic partnerships. The company is actively developing hybrid-electric propulsion systems and all-electric demonstrators to support sustainable aviation goals. Through programs like E-Fan X and CityAirbus, Airbus is exploring urban air mobility and regional electric flight solutions. Its contributions extend beyond technology development to shaping regulatory frameworks and industry standards for electric flight, making it a key driver of global innovation in aerospace electrification.

- Rolls-Royce has been at the forefront of electrifying aircraft propulsion with its ACCEL (Accelerating the Electrification of Flight) program, which aims to set new benchmarks in electric flight performance. The company focuses on high-power-density electric motors, advanced battery systems, and integration into existing and future aircraft platforms. By collaborating with academic institutions and government agencies, Rolls-Royce is helping define the technical and operational roadmap for electrified propulsion. Its commitment to decarbonizing aviation positions it as a major contributor to the evolution of electric aircraft technologies worldwide.

- Siemens has made significant strides in aircraft electrification by developing lightweight, high-efficiency electric propulsion systems tailored for small and regional aircraft. The company's expertise in power electronics, energy management, and digital twin technologies supports scalable electrification solutions across multiple aviation segments. Siemens collaborates closely with OEMs and research institutions to accelerate the commercialization of electric aircraft components. With a strong focus on smart energy systems and integrated powertrain architectures, Siemens continues to influence the trajectory of electric flight innovation on a global scale.

Top Strategies Used By Key Market Participants

Key players in the aircraft electrification market are leveraging strategic partnerships and joint ventures to pool resources, share R&D costs, and accelerate technology development. Collaborations between aerospace giants, battery manufacturers, and software developers are enabling the rapid prototyping and validation of electric propulsion systems tailored for different aircraft categories.

Another crucial strategy involves continuous investment in R&D to advance core electrification technologies, including high-density batteries, efficient power electronics, and fault-tolerant motor drives. Companies are focusing on improving system reliability, thermal management, and weight reduction to meet the demanding requirements of aviation applications and bring viable electric aircraft to market.

Lastly, firms are engaging proactively with regulators and standardization bodies to shape certification protocols and infrastructure requirements for electric flight. By participating in policy discussions and demonstration programs, industry leaders aim to align technological progress with evolving airworthiness regulations, ensuring safe and scalable adoption of electrified aviation solutions globally.

RECENT MARKET NEWS

- In February 2023, Airbus launched its ZEROe initiative’s first full-scale demonstrator, a hydrogen-fueled turboprop engine, aimed at validating emissions-free propulsion technologies for future commercial aircraft, marking a major milestone in its decarbonization roadmap.

- In August 2023, Rolls-Royce completed ground testing of its fully electric propulsion system developed under the ACCEL program, setting the stage for flight trials and reinforcing its leadership in high-performance electric aircraft powertrains.

- In March 2024, Siemens announced a strategic alliance with a Swedish battery startup to co-develop ultra-lightweight battery packs optimized for aviation use, enhancing energy density and safety for future electric aircraft applications.

- In October 2024, Eviation Aircraft unveiled a revised version of its Alice all-electric commuter aircraft, incorporating feedback from early test flights and securing commitments from regional airlines for future deliveries, signaling growing market confidence.

- In January 2025, Boeing entered a joint venture with a German propulsion tech firm to develop hybrid-electric engines for retrofitting existing regional aircraft, aiming to reduce emissions without requiring entirely new airframe designs.

MARKET SEGMENTATION

This research report on the global aircraft electrification market is segmented and sub-segmented by application, system, platform, technology, component, and region.

By Application

- Power Conversion

- Energy Storage

By System

- Propulsion Systems

- Aircraft Systems

By Platform

- Commercial Aircraft

- Military Aircraft

- General Aviation

By Technology

- More Electric

- Hybrid Electric

- Fully Electric

By Component

- Batteries

- Fuel Cells

- Solar Cells

- Electric Actuators

- Electric Pumps

- Generators

- Motors

- Power Electronics

- Distribution Devices

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What are the main drivers of the global aircraft electrification market?

Key drivers include the need to reduce carbon emissions, rising fuel costs, advancements in battery technology, stringent environmental regulations, and the growing demand for more efficient and quieter aircraft.

What are the primary challenges facing the aircraft electrification market?

Significant challenges include the high cost of electric aircraft development, limited battery energy density, safety concerns, infrastructure requirements for charging, and the need for regulatory approval.

What types of aircraft are most likely to be electrified first?

Initially, smaller aircraft, such as urban air mobility vehicles, regional jets, and unmanned aerial vehicles (UAVs), are likely to be electrified due to their lower power requirements. Over time, larger commercial aircraft may also adopt electric systems.

What advancements in technology are supporting the aircraft electrification market?

Significant advancements include improvements in battery energy density, power electronics, electric motors, and hybrid-electric propulsion systems. Innovations in material science and thermal management are also crucial.

What is aircraft electrification?

Aircraft electrification refers to the integration of electric power systems into aircraft operations, including fully electric propulsion, hybrid-electric systems, and more efficient electrical subsystems, aiming to reduce emissions and improve performance.

Why is the aircraft electrification market growing so rapidly?

The market is driven by increasing environmental concerns, stricter emission regulations, advancements in battery and electric motor technologies, and rising investments from aerospace companies and governments toward sustainable aviation solutions.

Which regions are leading in aircraft electrification adoption?

North America currently leads due to strong R&D initiatives and presence of major players like Boeing and startups like Eviation. Europe follows closely, supported by government green aviation policies and companies like Airbus. Asia-Pacific is emerging rapidly, especially in China and Japan, with growing investments in electric mobility.

How does aircraft electrification contribute to sustainability goals?

Electric propulsion systems significantly reduce carbon emissions, noise pollution, and dependency on fossil fuels. They support global efforts to meet net-zero targets set by international aviation bodies and national governments.

What are the biggest challenges facing the aircraft electrification industry?

Key challenges include limited battery energy density, high initial costs, regulatory complexities, lack of charging infrastructure, and thermal management issues in high-power applications.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com