Global Aircraft Fuel Systems Market Size, Share, Trends & Growth Forecast Report, Segmented By Application (Military, Commercial, UAV), Engine Type, Component, And Country (North America, Europe, Asia Pacific, Middle East And Africa, Latin America) - Industry Analysis From (2026 To 2034)

Global Aircraft Fuel Systems Market Size

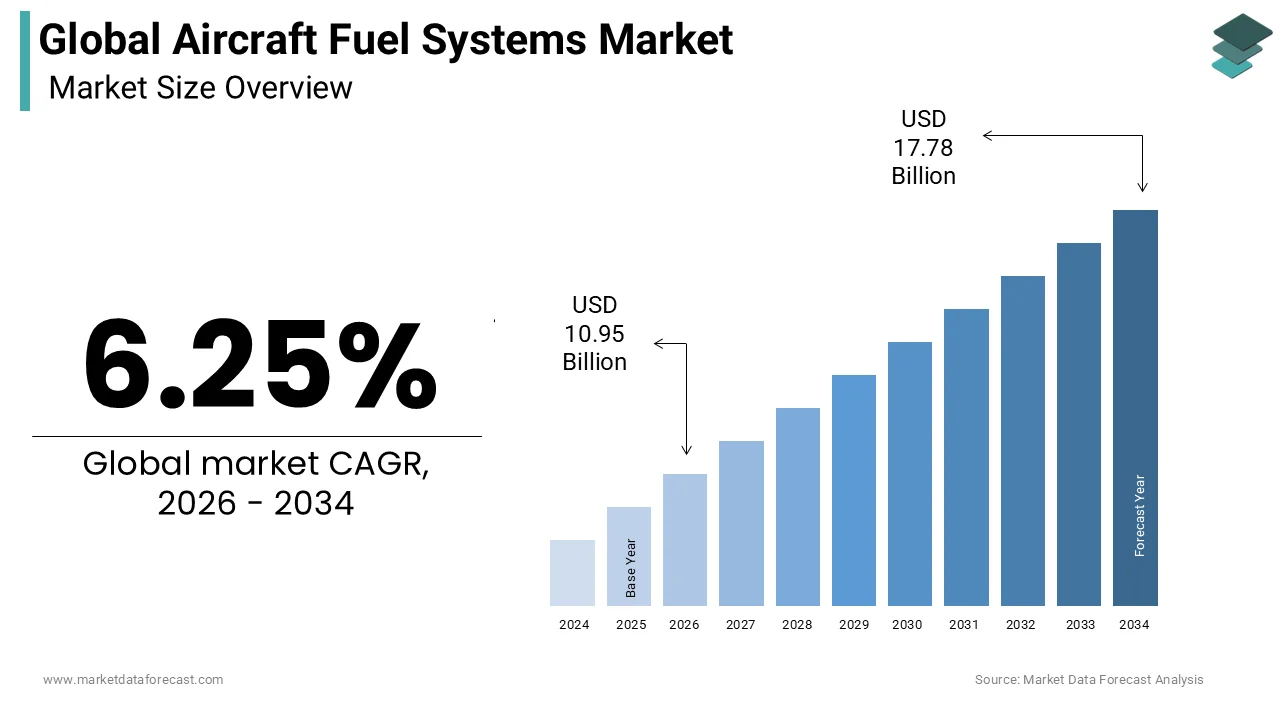

The Global Aircraft Fuel Systems market size was calculated at USD 10.31 billion in 2025 and is anticipated to reach USD 17.78 billion by 2034, from USD 10.95 billion in 2026, growing at a CAGR of 6.25% during the forecast period.

Aircraft fuel systems are responsible for storing, transferring, and delivering fuel to aircraft engines while maintaining precise pressure and flow rates. These systems include tanks, pumps, valves, filters, and management units that ensure safe and efficient operation across various flight conditions. The integrity of these systems is paramount as they directly influence flight safety, operational efficiency, and environmental compliance. Modern aviation demands advanced fuel management capabilities to support longer ranges, heavier payloads, and stricter emission standards. According to the International Air Transport Association, the demand for air travel is expected to double by 2040, requiring robust infrastructure and reliable fuel delivery mechanisms. The complexity of contemporary aircraft designs necessitates sophisticated fuel systems capable of handling alternative fuels and integrating with digital monitoring platforms. As per Boeing, the global airplane fleet will nearly double over the next 20 years, driving demand for new aircraft and subsequent fuel system installations. The transition towards sustainable aviation fuels requires modifications to existing fuel systems to accommodate different chemical properties and viscosity levels. Regulatory bodies such as the Federal Aviation Administration enforce stringent certification processes for fuel system components to prevent leaks, fires, and contamination. The integration of health monitoring sensors within fuel systems enables predictive maintenance, reducing downtime and enhancing safety. This technological evolution underscores the critical role of fuel systems in supporting the broader aerospace industry’s growth and sustainability goals.

MARKET DRIVERS

Surge in Global Air Passenger Traffic Driving Component Demand

The exponential rise in global air passenger traffic is one of the major factors propelling the expansion of the global aircraft fuel systems market. As more individuals choose air travel for both leisure and business purposes, airlines are compelled to expand their fleets and increase flight frequencies. According to ACI World, global air travel is on track to reach 9.8 billion passengers in 2025, significantly surpassing pre-pandemic levels. This resurgence in travel activity necessitates the production of new aircraft, each equipped with advanced fuel systems designed for optimal performance and safety. The introduction of narrow-body and wide-body aircraft models by major manufacturers like Airbus and Boeing directly correlates with increased demand for sophisticated fuel management components. These modern aircraft feature complex fuel distribution networks that require high precision engineering to handle varying load conditions and long-haul operations. The need for fuel efficiency drives innovation in system design, leading to lighter materials and smarter control algorithms. Airlines prioritize aircraft with lower operating costs, which translates to higher investment in efficient fuel systems that minimize waste and maximize range. The growth of low-cost carriers in emerging markets further amplifies this trend as these operators seek reliable and economical solutions for high utilization rates. Consequently, manufacturers of fuel system components experience sustained demand driven by the continuous expansion of the global aviation sector and the relentless pursuit of operational excellence.

Stringent Environmental Regulations Promoting Efficient System Design

Strict environmental regulations imposed by international aviation authorities are further contributing to the expansion of the aircraft fuel systems market. The aviation industry faces increasing pressure to reduce carbon emissions and noise pollution, prompting regulatory bodies to implement tighter standards. According to the International Air Transport Association, the aviation industry has committed to achieving net-zero carbon emissions by 2050, which requires significant technological advancements in all aircraft subsystems, including fuel management. Modern fuel systems must optimize fuel combustion and minimize leakage to meet these ambitious targets. The adoption of sustainable aviation fuels necessitates modifications to existing fuel systems to ensure compatibility with biofuels and synthetic alternatives. These alternative fuels often have different chemical properties, requiring specialized pumps, seals, and filters to prevent degradation and maintain performance. Regulatory frameworks, such as the Carbon Offsetting and Reduction Scheme for International Aviation, encourage airlines to invest in newer aircraft equipped with advanced fuel systems that offer superior efficiency. Manufacturers are responding by integrating real-time monitoring capabilities that allow for precise fuel usage tracking and immediate detection of inefficiencies. This regulatory push not only drives innovation but also creates a competitive advantage for companies that can deliver compliant and high-performance solutions. The alignment of fuel system technology with environmental goals ensures long-term viability and supports the industry’s transition towards a more sustainable future.

MARKET RESTRAINTS

High Certification and Compliance Costs Restricting Market Entry

The rigorous certification processes and high compliance costs associated with aircraft fuel systems are impeding the global market growth. Aviation components must undergo extensive testing and validation to meet safety standards set by authorities such as the Federal Aviation Administration and the European Union Aviation Safety Agency. According to industry experts, obtaining certification for a single fuel system component can take several years and cost millions of dollars due to the comprehensive nature of the required tests. These tests include structural integrity assessments, leak detection under extreme conditions, and performance verification across various altitudes and temperatures. The financial burden of compliance discourages small and medium-sized enterprises from entering the market, limiting competition and innovation potential. Established players benefit from existing certifications and established relationships with regulators, creating high barriers to entry for newcomers. Additionally, any design changes or updates require re-certification, which adds to the ongoing operational costs and delays product launches. The complexity of global regulations means that manufacturers must navigate different requirements in various regions, further increasing administrative and technical expenses. This environment favors large corporations with substantial resources and expertise, leaving limited room for agile startups to introduce disruptive technologies. Consequently, the market remains consolidated with few dominant players controlling the majority of supply, which can stifle price competition and slow the adoption of novel solutions.

Volatility in Raw Material Prices Impacting Production Stability

Fluctuations in the prices of raw materials used in aircraft fuel systems pose a significant challenge to the aircraft fuel systems market growth. Components such as pumps, valves, and tanks rely heavily on specialized alloys, aluminum, titanium, and high-grade plastics, which are subject to global commodity price volatility. According to the World Bank, metal prices have experienced significant swings in recent years due to supply chain disruptions, geopolitical tensions, and changing demand patterns. These price fluctuations make it difficult for manufacturers to predict production costs and maintain consistent pricing strategies. When raw material costs rise unexpectedly, manufacturers face pressure to absorb these increases or pass them on to customers, potentially losing a competitive advantage. The reliance on specific materials with limited suppliers exacerbates this issue, as any disruption in supply can lead to shortages and further price hikes. Additionally, the aerospace industry requires materials with strict quality specifications, limiting the ability to switch to cheaper alternatives without compromising safety and performance. Long-term contracts with suppliers help mitigate some risk but do not eliminate exposure to market dynamics. This uncertainty affects investment decisions and can delay the development of new products as companies hesitate to commit resources amidst unpredictable cost structures. The need for continuous quality assurance adds another layer of complexity, making it challenging to balance cost efficiency with regulatory compliance in a volatile raw material landscape.

MARKET OPPORTUNITIES

Integration of Sustainable Aviation Fuels: Creating New Design Opportunities

The growing adoption of sustainable aviation fuels presents a substantial opportunity for the aircraft fuel systems market. As airlines strive to meet carbon reduction targets, the demand for biofuels and synthetic fuels is increasing rapidly. According to the International Air Transport Association, sustainable aviation fuel production needs to scale up significantly to meet 2050 net-zero goals, creating an urgent need for compatible infrastructure. Current fuel systems are primarily designed for conventional jet fuel, which differs in viscosity, density, and chemical composition from many sustainable alternatives. Manufacturers have the opportunity to develop adaptive fuel systems that can handle a blend of traditional and sustainable fuels without compromising performance or safety. This involves creating advanced filtration systems, corrosion-resistant materials, and smart sensors that monitor fuel quality in real time. Companies that pioneer these technologies can secure long-term contracts with airlines and aircraft manufacturers seeking to future-proof their fleets. The transition also opens avenues for retrofitting existing aircraft with upgraded fuel systems that support sustainable options, extending the lifecycle of older models. Furthermore, government incentives for green aviation technologies provide financial support for research and development in this area. By positioning themselves as leaders in sustainable fuel compatibility, manufacturers can differentiate their offerings and capture a growing segment of the market focused on environmental responsibility and regulatory compliance.

Advancements in Digital Monitoring and Predictive Maintenance Technologies

The integration of digital monitoring and predictive maintenance technologies into aircraft fuel systems offers a promising opportunity for the aircraft fuel systems market. Modern aircraft are increasingly equipped with Internet of Things sensors that collect real-time data on fuel flow, pressure, temperature, and component health. According to Deloitte, predictive maintenance can reduce maintenance costs by up to 30 percent and decrease unplanned downtime by 50 percent, providing significant economic benefits for airlines. Fuel system manufacturers can leverage this trend by developing smart components that communicate with central aircraft systems to provide early warnings of potential failures. This proactive approach allows for timely interventions, preventing costly repairs and ensuring continuous flight operations. The data generated by these systems also enables optimization of fuel consumption patterns, leading to improved efficiency and reduced environmental impact. Manufacturers who embed advanced analytics capabilities into their fuel systems can offer value-added services such as performance reporting and maintenance scheduling. This shift from reactive to predictive maintenance aligns with the broader industry trend towards digitalization and data-driven decision-making. Additionally, the ability to remotely monitor fuel system health supports the growth of unmanned aerial vehicles and autonomous aircraft, which rely heavily on automated diagnostics. By embracing digital transformation, fuel system providers can create new revenue streams through software subscriptions and service contracts while strengthening customer loyalty through enhanced reliability and transparency.

MARKET CHALLENGES

Complexity of Supply Chain Management Amidst Geopolitical Instability

The intricate global supply chain for aircraft fuel systems faces significant challenges in the global market expansion. Manufacturing these systems requires sourcing specialized components from multiple countries, each with its own regulatory environment and political climate. According to the International Monetary Fund, geopolitical tensions have led to increased trade barriers and sanctions affecting the flow of critical materials and technologies. Disruptions in key regions can cause delays in production schedules and increase costs for manufacturers who rely on just-in-time inventory practices. The concentration of certain raw material supplies in politically sensitive areas exacerbates this vulnerability, making it difficult to secure consistent access. Additionally, logistical challenges such as port congestion and shipping delays further complicate the procurement process. Manufacturers must navigate complex customs regulations and tariff structures, which vary by region and can change abruptly. This uncertainty forces companies to hold larger inventories, tying up capital and increasing storage costs. The lack of transparency in multi-tier supply chains makes it difficult to identify and mitigate risks proactively. Companies must invest in diversified sourcing strategies and build resilience into their operations, but this requires significant time and resources. The interdependence of global markets means that a disruption in one region can have cascading effects worldwide, impacting the entire aerospace industry. Managing these complexities requires robust risk management frameworks and strong relationships with suppliers to ensure continuity of supply.

Shortage of Skilled Workforce Hindering Innovation and Production

A persistent shortage of skilled engineers and technicians specializing in aircraft fuel systems is further challenging the global market expansion. The complexity of modern fuel systems requires expertise in fluid dynamics, materials science, and digital integration, which is in short supply globally. According to the Aerospace Industries Association, the sector faces a widening skills gap as experienced professionals retire and fewer students pursue careers in aerospace engineering. This talent shortage limits the capacity of manufacturers to develop new technologies and scale production efficiently. Training new employees takes considerable time and investment, delaying project timelines and increasing operational costs. The competition for qualified personnel drives up wages, further straining budgets, especially for smaller firms. Additionally, the rapid pace of technological change means that existing workers require continuous upskilling to stay relevant, which adds to the training burden. The lack of standardized educational programs focused specifically on aircraft fuel systems exacerbates the problem, leaving many graduates unprepared for industry demands. This workforce constraint hinders the ability of companies to respond quickly to market opportunities and regulatory changes. It also affects the quality and reliability of products, as inexperienced staff may struggle with complex assembly and testing procedures. Addressing this challenge requires collaborative efforts between industry, academia, and government to promote STEM education and create attractive career pathways in aerospace engineering.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.25% |

| Segments Covered | By Application, Engine Type, Component, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, the Middle East and Africa, And Latin America |

| Market Leaders Profiled | Parker Hannifin Corporation, Eaton Corporation plc, Safran S.A., Collins Aerospace, Woodward, Inc., GKN Aerospace, Crane Aerospace & Electronics, Meggitt PLC, Senior plc, Triumph Group, Inc., Marshall Aerospace, Ametek, Inc., Cobham Limited, RTX Corporation, Honeywell International Inc. |

SEGMENTAL ANALYSIS

By Application Insights

The commercial aviation segment dominated the market by capturing the highest share of the global market in 2025. The growth of the commercial aviation segment in the global market can be credited to the relentless expansion of global air travel, fleet modernization initiatives, and the sheer volume of passenger and cargo flights that require robust and efficient fuel management solutions to ensure operational safety and cost effectiveness. According to the International Air Transport Association, global air passenger traffic is projected to reach 8 billion passengers by 2037, necessitating a significant increase in aircraft deliveries. Major manufacturers like Boeing and Airbus have order books exceeding 10,000 aircraft, which directly translates to sustained demand for advanced fuel systems, including tanks, pumps, and monitoring units. The shift towards fuel-efficient narrow-body aircraft, such as the Airbus A320neo and Boeing 737 MAX, requires sophisticated fuel systems that optimize consumption and reduce weight. Airlines are increasingly prioritizing total cost of ownership, which drives investment in lightweight composite fuel tanks and smart fuel management systems that provide real-time data on fuel usage. Regulatory pressures to lower carbon emissions further compel commercial operators to adopt newer aircraft equipped with state-of-the-art fuel technologies. The recovery of the tourism sector post-pandemic has accelerated this trend as airlines rush to replace older, less efficient fleets with modern alternatives. Additionally, the growth of low-cost carriers in emerging markets contributes significantly to this segment as these operators expand their networks and require reliable fuel systems for high-frequency operations. The commercial segment benefits from standardized certification processes and established supply chains that facilitate large-scale production and deployment.

On the other hand, the UAV segment is estimated to record a CAGR of 12.5% during the forecast period in the global market, owing to the increasing adoption of drones in military surveillance, logistics delivery, and agricultural monitoring, where extended flight endurance is critical. According to the Federal Aviation Administration, the number of registered commercial drones in the United States alone surpassed 500,000 in 2023, reflecting a broader global trend towards autonomous aerial operations. Military applications remain a primary driver as defense agencies worldwide invest in long-endurance UAVs for reconnaissance and combat missions, requiring specialized fuel systems that can handle varying altitudes and temperatures. The development of hybrid electric UAVs also creates demand for complex fuel management systems that integrate traditional combustion engines with electric power sources. Commercial logistics companies are testing drone delivery services, which require lightweight and reliable fuel systems to maximize payload capacity and range. Technological advancements in miniaturization allow for the integration of precise fuel injection and monitoring components into smaller UAV platforms. Government funding for drone research and development supports innovation in fuel efficiency and alternative fuel compatibility. The versatility of UAVs across multiple industries ensures diverse revenue streams for fuel system manufacturers. As regulations evolve to permit beyond visual line of sight operations, the demand for secure and redundant fuel systems will continue to accelerate, driving substantial growth in this niche but rapidly expanding segment.

By Engine Type Insights

The jet aircraft engine segment held the largest share of the global market in 2025. The dominance of the jet aircraft engine segment in the global market is primarily driven by its widespread use in commercial airliners, high-performance military jets, the high fuel flow requirements, and complex pressure management needs of jet engines, which necessitate advanced fuel delivery and control systems. According to Boeing, the global commercial jet fleet is expected to grow by 4 percent annually over the next two decades, driving continuous demand for new fuel system installations. Jet engines operate at extreme temperatures and pressures, requiring fuel systems made from high-grade alloys and composites that can withstand harsh conditions without failure. The transition to more fuel-efficient turbofan engines has led to the development of integrated fuel management systems that optimize combustion efficiency and reduce emissions. Manufacturers are focusing on lightweight designs to improve overall aircraft performance, which increases the value proposition of advanced jet fuel system components. The prevalence of wide-body aircraft for long-haul international flights further boosts this segment as these planes carry larger fuel volumes and require more complex distribution networks. Maintenance and replacement cycles for jet fuel systems also contribute significantly to market revenue as airlines adhere to strict safety protocols. The integration of health monitoring sensors in jet fuel systems enables predictive maintenance, reducing downtime and enhancing safety. This segment benefits from strong relationships between engine manufacturers and fuel system suppliers, ensuring consistent quality and innovation. The strategic importance of jet propulsion in both civil and military aviation secures its position as the primary driver of market growth.

However, the UAV engine segment is estimated to register a promising CAGR of 12.2% during the forecast period, owing to the proliferation of small and medium-sized drones across various sectors, and the need for specialized fuel systems that cater to the unique operational profiles of unmanned aircraft, including vertical takeoff and landing capabilities. According to Deloitte, the global drone market is expected to exceed 50 billion dollars by 2030, with a significant portion allocated to propulsion and fuel management technologies. Small piston and rotary engines used in UAVs require compact and lightweight fuel systems that do not compromise payload capacity. The development of hybrid propulsion systems for UAVs creates opportunities for innovative fuel management solutions that balance internal combustion and electric power sources. Military investments in tactical drones for surveillance and target acquisition drive demand for ruggedized fuel systems that can operate in remote and hostile environments. Commercial applications in agriculture and infrastructure inspection also contribute to this growth as operators seek longer flight times and greater reliability. Advances in additive manufacturing allow for the production of complex fuel system components with reduced weight and improved performance. The regulatory landscape is evolving to support wider drone adoption, which encourages manufacturers to invest in safer and more efficient fuel technologies. The versatility of UAV engines across different platforms ensures a dynamic and rapidly expanding market for specialized fuel system components.

By Component Insights

The fuel pump segment accounted for the largest share of the global market in 2025. The growth of the fuel pump segment in the global market is attributed to its critical role in ensuring consistent fuel delivery to engines under varying flight conditions. Fuel pumps are essential for maintaining the required pressure and flow rate, which directly impacts engine performance and safety. According to Zion Market Research, the global aircraft pumps market was worth USD 3.80 billion in 2023, driven by the need for high reliability and precision in aerospace applications. Modern aircraft utilize multiple stages of fuel pumping, including booster pumps and main engine-driven pumps, which increases the complexity and value of these components. The shift towards electric fuel pumps in newer aircraft models offers advantages in terms of weight reduction and controllability compared to traditional mechanical systems. These electric pumps allow for more precise fuel metering and integration with digital flight control systems, enhancing overall efficiency. Maintenance requirements for fuel pumps are stringent, leading to regular replacement and an upgrade, which sustains aftermarket demand. Manufacturers are investing in materials that resist corrosion and wear, extending the lifespan of pumps and reducing operational costs. The integration of smart sensors in fuel pumps enables real-time monitoring of performance metrics, allowing for predictive maintenance and early fault detection. This technological advancement reduces the risk of in-flight failures and enhances safety standards. The universal requirement for fuel pumps across all types of aircraft, from small general aviation planes to large commercial jets, ensures steady demand. The critical nature of this component means that airlines and operators prioritize quality and reliability over cost, making it a lucrative segment for specialized manufacturers.

However, the fuel valve segment is promising and is estimated to register a CAGR of 10.2% during the forecast period due to the increasing complexity of fuel management architectures. Fuel valves play a pivotal role in controlling fuel flow direction, isolation, and shutoff, which is crucial for safety during emergencies and routine operations. For instance, the demand for advanced solenoid and motor-operated valves is rising as aircraft manufacturers seek to automate fuel management processes. The introduction of fly-by-wire technology in modern aircraft requires precise electronic control of fuel valves to optimize engine performance and balance fuel load across multiple tanks. Safety regulations mandate redundant valve systems to prevent fuel leakage and fire hazards, which increases the number of valves per aircraft. The development of lightweight composite materials for valve bodies helps reduce overall aircraft weight, contributing to fuel efficiency goals. Innovations in valve design focus on minimizing pressure drop and improving response times, which enhances engine responsiveness. The growing adoption of sustainable aviation fuels necessitates valves that are compatible with different chemical properties and viscosities. Aftermarket services for valve maintenance and repair also contribute to segment growth as airlines strive to maintain high safety standards. The integration of diagnostic capabilities in smart valves allows for continuous health monitoring, reducing unplanned maintenance events. This segment benefits from ongoing research into materials science and fluid dynamics, leading to more efficient and reliable components. The critical safety function of fuel valves ensures that they remain a priority for certification and investment in the aerospace industry.

REGIONAL ANALYSIS

North America Aircraft Fuel Systems Market Analysis

North America dominated the market and held 36.1% of the global market share in 2025. The region’s leadership is anchored by the presence of major aerospace manufacturers such as Boeing and Lockheed Martin, along with a robust network of suppliers and service providers. According to the Aerospace Industries Association, the United States aerospace industry generated over 900 billion dollars in revenue in 2023, supporting extensive research and development in fuel system technologies. The high volume of domestic air travel and a large commercial fleet drive consistent demand for new installations and replacements. Military spending in North America remains substantial with significant investments in next-generation fighter jets and transport aircraft that require advanced fuel management systems. The region benefits from stringent safety regulations enforced by the Federal Aviation Administration, which mandates regular upgrades and maintenance of fuel components. Innovation hubs in states like Washington and California foster collaboration between academia and industry, leading to breakthroughs in lightweight materials and digital monitoring. The adoption of sustainable aviation fuels is gaining momentum, supported by government incentives and corporate sustainability goals. Supply chain resilience is a key focus area as manufacturers seek to localize production of critical components. The presence of skilled labor and advanced manufacturing facilities ensures high-quality output and timely delivery. North America continues to set global standards for aircraft fuel system performance and safety, influencing practices in other regions.

Europe Aircraft Fuel Systems Market Analysis

Europe maintains a strong position in the aircraft fuel systems market, driven by the presence of leading aircraft manufacturer Airbus and a dense network of specialized suppliers. The European Union’s commitment to environmental sustainability through the Green Deal initiative accelerates the adoption of fuel-efficient technologies and alternative fuels. According to the European Automobile Manufacturers Association, although focused on automotive, the broader transport sector in Europe is heavily regulated for emissions, which influences aerospace standards similarly. Countries like France, Germany, and the United Kingdom are key contributors to aerospace innovation, investing heavily in research and development for next-generation fuel systems. The region faces strict regulatory oversight from the European Union Aviation Safety Agency, which ensures high safety and quality standards for all aircraft components. The growth of low-cost carriers in Europe increases the demand for narrow-body aircraft, which require optimized fuel systems for short-haul efficiency. Collaborative projects among European nations promote the development of common standards and shared infrastructure for sustainable aviation. The region is also a leader in recycling and circular economy practices for aerospace materials, including fuel system components. Skilled engineering talent and established industrial bases support continuous innovation and production excellence. Europe’s focus on reducing carbon footprint drives investment in hybrid and electric propulsion systems, which require novel fuel management solutions. The region remains a critical hub for aerospace technology, influencing global trends in safety and sustainability.

Asia Pacific Aircraft Fuel Systems Market Analysis

Asia Pacific is emerging as the fastest-growing region in the aircraft fuel systems market due to rapid expansion in air travel and fleet modernization. China, India, and Southeast Asian countries are witnessing a surge in the middle-class population, leading to increased demand for air transportation. According to the International Air Transport Association, the Asia Pacific is expected to become the largest aviation market by 2035, surpassing North America in passenger volume. Governments in the region are investing heavily in airport infrastructure and airline expansion programs, which drive demand for new aircraft and associated fuel systems. Local manufacturing capabilities are strengthening, with companies in China and Japan developing indigenous aircraft programs that require domestic fuel system supplies. The rise of low-cost carriers in countries like Indonesia and Vietnam contributes to high aircraft utilization rates and frequent maintenance cycles. Regulatory frameworks are evolving to align with international safety standards, prompting upgrades in existing fleets. The region benefits from competitive labor costs and growing technical expertise, which attracts global manufacturers to establish production facilities. Partnerships between local and international firms facilitate technology transfer and capacity building. The focus on regional connectivity through initiatives like the Belt and Road Initiative supports the growth of regional airports and aircraft operations. Asia Pacific’s dynamic market environment offers significant opportunities for innovation and expansion in the aircraft fuel systems sector.

COMPETITION OVERVIEW

The competition in the aircraft fuel systems market is characterized by a high degree of consolidation among established aerospace giants who possess extensive technical expertise and certified product portfolios. These dominant players leverage their long-standing relationships with original equipment manufacturers to secure lucrative contracts for new aircraft programs. The barrier to entry remains exceptionally high due to stringent regulatory requirements and the need for rigorous certification processes that can take years to complete. Competitors differentiate themselves through continuous innovation in lightweight materials, digital monitoring capabilities, and compatibility with alternative fuels. Price competition is moderate as safety and reliability often outweigh cost considerations for buyers. However, emerging companies are attempting to disrupt the market by offering niche solutions for unmanned aerial vehicles and regional aircraft. Strategic alliances and supply chain integration are critical for maintaining competitive advantage as manufacturers seek to reduce lead times and improve responsiveness to fluctuating demand. The focus on sustainability further intensifies competition as firms race to develop eco-friendly technologies that comply with evolving global emission standards.

KEY MARKET PLAYERS

A few major players in the global aircraft fuel systems market include

- Parker Hannifin Corporation

- Eaton Corporation plc

- Safran S.A

- Collins Aerospace

- Woodward, Inc

- GKN Aerospace

- Crane Aerospace & Electronics

- Meggitt PLC

- Senior plc

- Triumph Group, Inc

- Marshall Aerospace

- Ametek, Inc

- Cobham Limited

- RTX Corporation

- Honeywell International Inc

Top Strategies Used by Key Market Participants

Key players in the aircraft fuel systems market primarily employ strategic partnerships and collaborations to enhance their technological capabilities and expand their global reach. Companies frequently engage in joint ventures with aircraft manufacturers to co-develop integrated fuel management solutions that meet specific design requirements. Innovation through research and development remains a central strategy as firms invest heavily in creating lightweight materials and smart sensors for improved efficiency. Mergers and acquisitions are utilized to acquire specialized technologies and enter new geographic markets quickly. Additionally, manufacturers focus on sustainability by developing fuel systems compatible with sustainable aviation fuels to align with environmental regulations. Digital transformation initiatives, including predictive maintenance tools, are increasingly adopted to offer value-added services and strengthen customer relationships in the competitive aerospace landscape.

Leading Players in the Global Aircraft Fuel Systems Market

- Parker Hannifin Corporation stands as a pivotal entity in the aerospace sector by delivering advanced fuel management and motion control technologies. The company focuses on developing lightweight composite fuel tanks and high-precision valves that enhance aircraft efficiency and safety. Recent initiatives include expanding its manufacturing capabilities in North America to meet the rising demand for next-generation commercial aircraft. Parker Hannifin actively collaborates with major airframe manufacturers to integrate smart sensors into fuel systems enabling real time monitoring and predictive maintenance. This strategic focus on digitalization and material innovation allows the company to address stringent environmental regulations while improving operational reliability for global airlines seeking sustainable aviation solutions.

- Safran SA plays a critical role in the market through its expertise in aircraft equipment and propulsion systems, including sophisticated fuel delivery mechanisms. The French multinational emphasizes research and development to create fuel systems compatible with sustainable aviation fuels and hybrid electric architectures. Safran recently strengthened its position by securing long-term contracts with leading aircraft manufacturers for supplying integrated fuel management units. The company invests heavily in additive manufacturing techniques to produce complex fuel system components with reduced weight and enhanced durability. These efforts support the industry transition towards greener aviation while maintaining high-performance standards for both commercial and military applications worldwide.

- Eaton Corporation contributes significantly to the aircraft fuel systems landscape by providing robust fuel pumping and valve solutions designed for extreme operational conditions. The company leverages its extensive engineering experience to develop systems that ensure precise fuel metering and distribution across various aircraft platforms. Eaton has recently focused on enhancing its supply chain resilience by diversifying production sites and adopting automated manufacturing processes. The firm actively participates in industry consortia to establish standards for alternative fuel compatibility and safety protocols. By prioritizing innovation in fluid power management and electrical integration, Eaton supports the aerospace industry's goals of reducing emissions and improving overall flight safety and efficiency.

MARKET SEGMENTATION

This research report on the Global Aircraft Fuel Systems market has been segmented and sub-segmented based on application, engine type, component, and region.

By Application

- Military

- Commercial

- UAV

By Engine Type

- Jet aircraft engine

- Helicopter engine

- Turboprop engine

- UAV engine

By Component

- Fuel tank

- Fuel valve

- Fuel pump

- Fuel filter

- Fuel gauge

- Fuel line

By Region

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What factors are driving the growth of the aircraft fuel systems market?

Increasing aircraft production, rising air passenger traffic, fleet modernization, and demand for fuel-efficient aircraft are major growth drivers.

2. Which aircraft type dominates the market?

Commercial aircraft account for the largest market share due to the growing demand for air travel and expansion of airline fleets worldwide.

3. What are the main components of an aircraft fuel system?

Key components include fuel tanks, pumps, valves, filters, fuel gauges, fuel management systems, and fuel transfer systems.

4. Why are advanced aircraft fuel systems important?

Advanced fuel systems improve fuel efficiency, reduce aircraft weight, enhance operational safety, and minimize maintenance costs.

5. Which region holds the largest share of the Global Aircraft Fuel Systems Market?

North America holds the largest market share, supported by major aircraft manufacturers, defense spending, and technological advancements.

6. What challenges does the aircraft fuel systems market face?

High development costs, stringent aviation safety regulations, complex certification processes, and supply chain disruptions are key challenges.

7. What opportunities exist in the aftermarket segment?

The growing global aircraft fleet increases demand for maintenance, repair, overhaul (MRO), component replacement, and system upgrades.

8. Who are the major customers in this market?

Commercial airlines, aircraft OEMs, military organizations, business jet manufacturers, and MRO service providers are the primary customers.

9. What technologies are shaping the future of aircraft fuel systems?

Digital fuel monitoring, smart sensors, predictive maintenance, lightweight composite materials, and automated fuel management technologies are transforming the market.

10. What is the future outlook for the Global Aircraft Fuel Systems Market?

The market is expected to experience steady growth over the coming years, driven by increasing aircraft production, technological innovations, fleet expansion, and the aviation industry's focus on fuel efficiency and sustainability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com