Global Aircraft Health Monitoring System Market Market Size, Share, Trends & Growth Forecast Report – Segmented By End-User (OEMS, Airlines, MRO), Subsystem, Transmission Mode, Component, Fit, Aircraft type and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Aircraft Health Monitoring System Market Report Summary

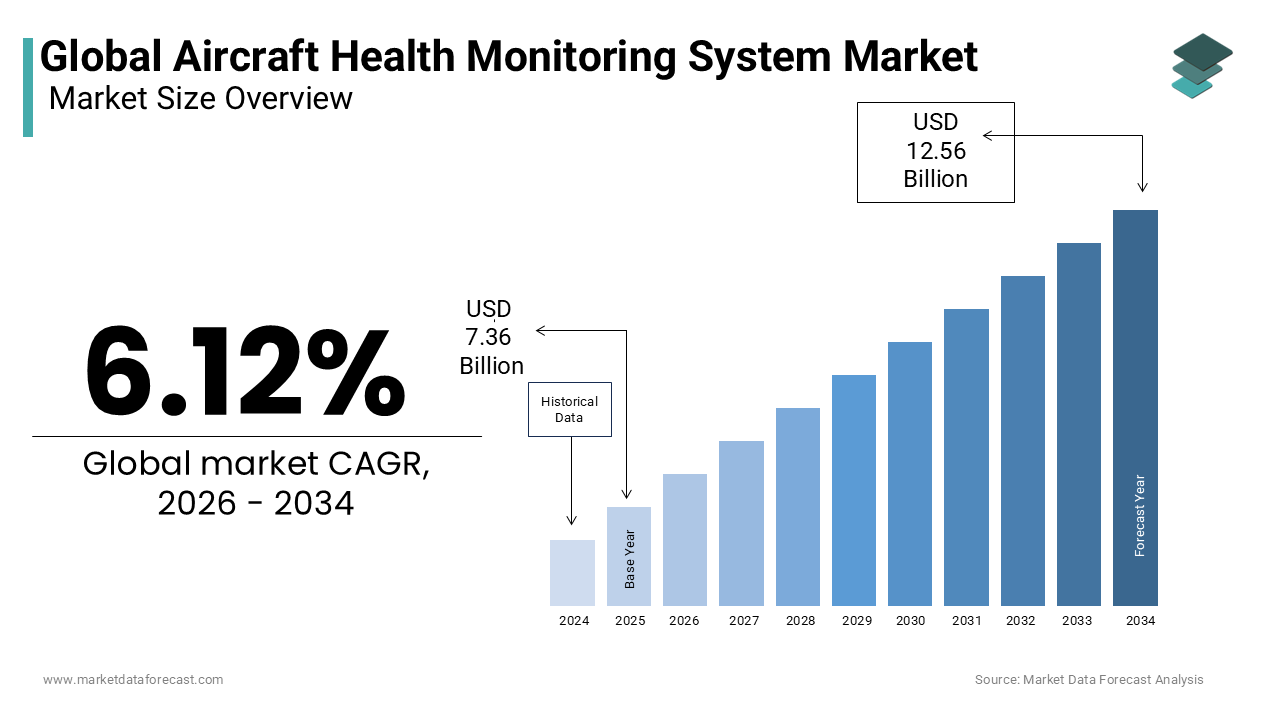

The global aircraft health monitoring system market was valued at USD 7.36 billion in 2025 and is anticipated to reach USD 7.81 billion in 2026 from USD 12.56 billion by 2034, growing at a CAGR of 6.12% during the forecast period from 2026 to 2034. The growth of the global aircraft health monitoring system market is driven by rising global air traffic, increasing emphasis on predictive maintenance, and stringent aviation safety regulations. Growing investments in digital aviation technologies, increasing adoption of Internet of Things (IoT)-enabled aircraft monitoring systems, and expanding commercial aircraft fleets are further accelerating market growth. Moreover, the integration of artificial intelligence and machine learning for predictive analytics, advancements in digital twin technologies, and increasing deployment of real-time fleet monitoring solutions are supporting the expansion of the global aircraft health monitoring system market.

Key Market Trends

-

Rising adoption of artificial intelligence and machine learning for predictive aircraft maintenance.

-

Increasing deployment of digital twin technologies to monitor aircraft performance in real time.

-

Growing utilization of IoT-enabled sensors for continuous monitoring of aircraft components.

-

Rising investment in cloud-based fleet health monitoring and predictive analytics platforms.

-

Increasing adoption of satellite-enabled real-time aircraft data transmission systems.

Segmental Insights

- Based on end user, the airlines segment dominated the global aircraft health monitoring system market in 2025. The dominance of the segment is attributed to increasing focus on reducing unscheduled maintenance events, maximizing aircraft availability, improving fleet utilization, and minimizing operational costs through predictive maintenance strategies. Rising commercial air traffic and increasing pressure to maintain high dispatch reliability continue to strengthen segment growth.

- The MRO (Maintenance, Repair, and Overhaul) segment is projected to witness the fastest CAGR of 9.1% during the forecast period owing to increasing outsourcing of maintenance operations, growing demand for predictive maintenance services, expanding global MRO facilities, and rising adoption of advanced diagnostic and digital maintenance technologies.

- Based on subsystem, the engine segment dominated the global aircraft health monitoring system market in 2025. The growth of the segment is driven by the high value of aircraft engines, increasing focus on engine reliability, stringent regulatory monitoring requirements, growing adoption of real-time engine performance analytics, and rising demand for reducing engine-related maintenance costs through predictive diagnostics.

- The avionics and electrical systems segment is anticipated to register the fastest CAGR of 10.4% during the forecast period due to increasing aircraft digitalization, expanding adoption of advanced cockpit electronics, growing integration of connected avionics systems, rising regulatory emphasis on electrical system safety, and increasing deployment of intelligent sensor technologies across aircraft electrical networks.

- Based on transmission mode, the ground-based transmission segment dominated the global aircraft health monitoring system market in 2025. The dominance of the segment is attributed to its established infrastructure, lower implementation costs, compatibility with existing maintenance management systems, and widespread utilization for post-flight data analysis and fleet-wide maintenance planning.

- The onboard real-time transmission segment is expected to witness the fastest CAGR of 12.4% during the forecast period owing to increasing deployment of high-throughput satellite communications, growing adoption of real-time aircraft diagnostics, expanding availability of onboard data processing technologies, and rising demand for continuous monitoring of critical aircraft systems during flight.

Regional Insights

- North America dominated the global aircraft health monitoring system market and accounted for 36.1% of the global market share in 2025. The region's leadership is driven by the presence of major aircraft manufacturers, advanced aviation infrastructure, stringent Federal Aviation Administration (FAA) regulations, extensive commercial airline operations, and high investments in predictive maintenance technologies. Strong research and development capabilities further strengthen regional market growth.

- Europe held a significant share of the global aircraft health monitoring system market owing to stringent aviation safety regulations, widespread adoption of digital twin technologies, strong aerospace manufacturing capabilities, increasing investments in sustainable aviation, and the presence of major industry participants including Airbus, Rolls-Royce, and Safran. Continuous innovation in predictive maintenance further supports market expansion.

- Asia Pacific is projected to witness the fastest growth during the forecast period due to rapid commercial fleet expansion, increasing passenger air traffic, growing aviation infrastructure investments, rising aircraft deliveries across China and India, and increasing adoption of digital maintenance technologies by regional airlines. Expanding local MRO capabilities continue to accelerate market growth.

- Latin America continues to maintain steady growth owing to ongoing fleet modernization, strengthening aviation safety regulations, increasing predictive maintenance adoption, expanding partnerships with global aviation technology providers, and growing commercial airline operations across major regional economies.

- The Middle East & Africa is expected to experience notable growth during the forecast period due to rapid expansion of airline fleets, increasing investments in smart airport infrastructure, growing adoption of advanced aircraft maintenance technologies, expansion of aviation hubs across the Gulf region, and rising demand for enhanced operational efficiency and safety.

Competitive Landscape

The global aircraft health monitoring system market is highly competitive and characterized by the presence of leading aerospace manufacturers, avionics companies, and digital aviation technology providers competing through technological innovation, predictive analytics, artificial intelligence integration, and advanced sensor technologies. Leading companies are focusing on developing digital twin platforms, cloud-based maintenance analytics, cybersecurity-enhanced monitoring systems, and real-time aircraft diagnostics to improve operational reliability and reduce maintenance costs. Strategic collaborations with airlines, aircraft manufacturers, and MRO providers, along with continuous investments in research and development, continue to strengthen competitive positioning across the global aircraft health monitoring system market. The prominent players operating in the global aircraft health monitoring system market include Honeywell International Inc., RTX Corporation (Collins Aerospace), General Electric Company (GE Aerospace), Airbus SE, The Boeing Company, Safran S.A., Thales Group, Lufthansa Technik AG, Meggitt PLC (Parker Meggitt), Curtiss-Wright Corporation, Rolls-Royce Holdings plc, Teledyne FLIR LLC, FLYHT Aerospace Solutions Ltd., CAMP Systems International, Inc., and Emerson Electric Co.

Global Aircraft Health Monitoring System Market Size

The aircraft health monitoring system market size was valued at USD 7.36 billion in 2025 and is anticipated to reach USD 7.81 billion in 2026 from USD 12.56 billion by 2034, growing at a CAGR of 6.12% during the forecast period from 2026 to 2034.

Aircraft health monitoring systems are designed to continuously assess the structural and operational integrity of aircraft components. These systems utilize an intricate network of sensors, embedded within airframes and engines, to capture real-time data on vibration, temperature, pressure, and stress levels. The primary objective is to transition maintenance strategies from reactive or scheduled intervals to predictive models that anticipate failures before they occur. According to the Airports Council International, the global airline industry is projected to reach approximately 10.2 billion passengers annually by 2026, which necessitates unprecedented levels of fleet availability and safety compliance. The Federal Aviation Administration mandates rigorous maintenance protocols, where any deviation can result in severe regulatory penalties and grounded fleets. For instance, airlines lose billions of dollars in potential revenue annually due to unscheduled maintenance events, which directly impacts passenger trust. The integration of Internet of Things capabilities allows for seamless data transmission to ground stations, enabling engineers to diagnose issues remotely. This technological evolution is critical, as modern aircraft, such as the Boeing 787 and Airbus A350, generate terabytes of data per flight. The market is thus driven by the imperative to minimize downtime while maximizing safety standards in an increasingly congested airspace environment, where operational efficiency is paramount for carrier profitability and regulatory adherence.

MARKET DRIVERS

Rising Global Air Traffic Volume Demands Enhanced Operational Reliability

The market for aircraft health monitoring solutions is expected to see significant growth over the next few years as carriers prioritize digital fleet management. According to the International Civil Aviation Organization, global air passenger numbers are expected to reach 10.2 billion by 2026, reflecting a steady recovery and expansion beyond pre-pandemic levels. This surge places immense pressure on airline fleets to maintain high dispatch reliability rates, which often exceed 99% for major carriers. Unscheduled maintenance events caused by unexpected component failures can lead to significant financial losses, with each hour of aircraft grounding costing airlines between 10,000 and 150,000 dollars, depending on the aircraft type. As per data from the Bureau of Transportation Statistics, mechanical issues account for nearly 15% of all operational delays in the United States alone. Health monitoring systems mitigate these risks by providing early warnings for potential failures, allowing maintenance teams to schedule repairs during planned downtimes rather than facing emergency groundings. For instance, a single engine failure detected mid-flight can result in diversion costs exceeding 50,000 dollars, whereas proactive replacement based on sensor data costs a fraction of that amount. The increasing frequency of flights means that even minor inefficiencies compound rapidly across large fleets. Consequently, airlines are prioritizing technologies that ensure continuous operational readiness to meet the demands of a traveling public that expects punctuality and safety without compromise.

Stringent Regulatory Compliance and Safety Mandates Drive Adoption

The stringent maintenance mandates continue to influence operator investment, which is likely to boost the aircraft health monitoring system market growth. The European Union Aviation Safety Agency and the Federal Aviation Administration have implemented strict guidelines requiring detailed documentation and proof of component integrity throughout an aircraft’s lifecycle. As per the National Transportation Safety Board, mechanical failures contribute to approximately 12% of aviation incidents globally, highlighting the critical need for proactive detection systems. These regulations mandate that operators demonstrate due diligence in maintenance practices, which traditional manual inspections often fail to provide with sufficient granularity. Health monitoring systems offer auditable digital records of component performance, ensuring compliance with airworthiness directives. For example, the FAA requires specific monitoring parameters for turbine engines, including vibration limits and temperature thresholds, which must be recorded and analyzed regularly. Non-compliance can result in fines exceeding 1 million dollars per violation and potential suspension of operating certificates. Additionally, insurance providers are beginning to link premium rates to the sophistication of an airline’s maintenance technology stack, offering discounts of up to 10% for carriers utilizing advanced predictive analytics. This financial incentive, combined with legal obligations, creates a compelling business case for investment. The shift towards evidence-based maintenance rather than time-based schedules aligns with regulatory preferences for data-driven safety management systems, thereby reducing liability exposure for operators while enhancing overall aviation safety standards globally.

MARKET RESTRAINTS

High Initial Implementation Costs and Integration Complexity Restrain Market Growth

The substantial capital expenditure required for deploying aircraft health monitoring systems is one of the significant impediments to the global market, particularly for small and medium-sized airlines. Installing a comprehensive network of sensors across an entire fleet involves not only hardware costs but also extensive software licensing fees and integration expenses. According to industry analysis, the initial setup cost for a single narrow-body aircraft can range from 50,000 to 100,000 dollars, excluding ongoing subscription fees for data analytics platforms. For regional carriers operating fleets of 20 to 30 aircraft, this represents a multi-million dollar investment that may strain limited financial resources. Furthermore, integrating these new systems with legacy maintenance management software often requires custom development work, which can extend implementation timelines by 6 to 12 months. As per industry surveys, nearly 40% of smaller carriers cite budget constraints as the primary reason for delaying technology upgrades. The complexity is compounded by the need for specialized training for maintenance personnel, who must interpret complex data streams rather than relying on traditional visual inspections. This transition requires additional investment in human capital, with training programs costing approximately 5,000 dollars per technician. Many operators struggle to justify the return on investment in the short term, despite long-term benefits. The financial burden is particularly acute in regions where labor costs are low and manual inspection remains economically viable, thereby slowing the universal adoption of these advanced monitoring technologies across the global aviation sector.

Data Security Vulnerabilities and Cyber Threats Impede Trust and Adoption

The rising connectivity of aircraft systems introduces significant cybersecurity risks that deter some operators from fully embracing cloud-based health monitoring solutions, which is further hindering the expansion of the aircraft health monitoring system market. Modern aircraft generate vast amounts of sensitive operational data that, if compromised, could reveal proprietary performance metrics or even be manipulated to cause safety hazards. According to the Cybersecurity and Infrastructure Security Agency, the aviation sector experienced a 30% increase in cyber-attacks between 2023 and 2025, targeting both ground infrastructure and airborne systems. The potential for malicious actors to inject false data into health monitoring streams poses a critical threat, as it could lead to incorrect maintenance decisions or mask genuine faults. Airlines are required to comply with stringent data protection regulations, such as the General Data Protection Regulation in Europe, which imposes heavy fines for data breaches exceeding 20 million euros or 4% of global turnover. The cost of implementing robust encryption and secure transmission protocols adds another layer of expense to already costly systems. As per a study by the International Air Transport Association, 65% of airlines consider cybersecurity the top concern when adopting new digital technologies. The fear of reputational damage following a security incident further complicates decision-making processes. Operators must balance the benefits of real-time data access with the imperative to protect their networks from evolving threats. This tension slows down the deployment of fully integrated monitoring ecosystems as companies proceed with caution, ensuring that every connection point is secured against potential exploitation by sophisticated cyber-criminals.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning Offers Predictive Capabilities

The incorporation of artificial intelligence and machine learning algorithms into health monitoring systems presents a promising opportunity for the aircraft health monitoring system market. Traditional monitoring methods rely on predefined thresholds, which often fail to detect subtle anomalies that precede major failures. AI-driven models can analyze historical data patterns across thousands of flights to identify early warning signs that human analysts might overlook. According to McKinsey and Company, airlines utilizing AI-based predictive maintenance can reduce maintenance costs by up to 25% while increasing aircraft availability by 15%. These systems learn from each flight, improving their diagnostic precision over time. For example, machine learning models can predict bearing failures in engines up to 100 flight hours in advance, allowing for planned replacements during routine checks. This capability minimizes the risk of in-flight incidents and reduces the need for spare parts inventory, as procurement becomes more predictable. The global market for AI in aviation is projected to grow at a CAGR of 42% through 2030, as per Statista, indicating strong industry confidence in this technology. Airlines can leverage these insights to optimize maintenance schedules across their entire fleet, ensuring that resources are allocated efficiently. The ability to process vast datasets in real-time enables operators to make informed decisions that enhance safety while reducing operational disruptions. This technological leap transforms maintenance from a cost center into a strategic advantage, driving competitiveness in an increasingly data-centric industry landscape.

Expansion of Internet of Things Connectivity Enables Real-Time Fleet Management

The proliferation of Internet of Things devices and enhanced connectivity solutions, such as 5G and satellite communications creates new opportunities for the aircraft health monitoring system market. Modern aircraft are equipped with hundreds of sensors that transmit data continuously to ground stations, enabling immediate analysis and response. As per GSMA Intelligence, the number of connected IoT devices utilizing cellular networks is expected to reach 5.7 billion by 2026, facilitating seamless data exchange between aircraft and maintenance centers. This connectivity allows airlines to monitor multiple parameters simultaneously, including fuel efficiency, engine performance, and structural integrity across their entire fleet from a centralized dashboard. Real-time data transmission eliminates the delay associated with post-flight downloads, ensuring that critical issues are addressed immediately. For instance, if a sensor detects abnormal vibration levels during cruise, the system can alert engineers on the ground, who can prepare repair kits and personnel before the aircraft lands. This proactive approach reduces turnaround times and improves schedule reliability. Satellite communication advancements now enable coverage over remote oceans and polar routes, where previously data gaps existed. According to industry reports, global aviation connectivity revenues are growing at 8% annually, driven by demand for real-time operational data. This expanded connectivity framework supports more sophisticated monitoring applications and enables airlines to optimize routes based on actual aircraft performance data, leading to fuel savings and reduced emissions while maintaining high safety standards.

MARKET CHALLENGES

Shortage of Skilled Data Analysts and Maintenance Technicians Poses Operational Challenges

The rapid advancement of health monitoring technologies has outpaced the availability of qualified personnel capable of interpreting complex datasets and managing sophisticated analytical platforms, which is a major challenge to the global aircraft health monitoring system market. Traditional maintenance technicians are trained in mechanical and electrical systems but often lack the data science skills required to leverage AI-driven insights effectively. According to the International Air Transport Association, the aviation industry faces a significant shortage of skilled professionals globally by 2026, including pilots, mechanics, and data analysts. This gap is particularly acute in the realm of predictive maintenance, where understanding algorithm outputs is crucial for making accurate repair decisions. Training programs take considerable time and investment, with certified data analyst courses costing upwards of 10,000 dollars per employee and requiring several months to complete. Airlines struggle to retain talent, as tech companies offer higher salaries for similar skill sets, creating a competitive labor market. As per Boeing estimates, the industry needs to train 769,000 new maintenance technicians by 2032 to meet growing demand. Without adequate staffing, airlines cannot fully utilize the capabilities of their monitoring systems, leading to underutilization of expensive technology investments. The reliance on external consultants for data analysis increases operational costs and reduces internal expertise development. This human capital challenge threatens to bottleneck the effectiveness of health monitoring initiatives, as organizations find themselves with powerful tools but insufficient expertise to deploy them optimally across their maintenance operations.

Interoperability Issues between Legacy Systems and New Technologies Create Fragmentation

The aviation industry operates with a diverse mix of aircraft generations, ranging from decades-old models to state-of-the-art jets, each equipped with different avionics and data protocols, which is further challenging the global market expansion. This heterogeneity creates significant interoperability challenges when implementing unified health monitoring systems across mixed fleets. Older aircraft often lack the digital infrastructure required for seamless integration with modern cloud-based analytics platforms, necessitating costly retrofitting projects. According to the Aircraft Electronics Association, upgrading legacy systems to support current data standards can cost between 200,000 and 500,000 dollars per aircraft, depending on complexity. Even when hardware upgrades are feasible, software incompatibilities persist as different manufacturers use proprietary data formats that do not easily communicate with third-party monitoring solutions. This fragmentation forces airlines to maintain multiple parallel systems, increasing operational complexity and the risk of data silos. As per SITA, nearly 70% of airlines report difficulties in integrating new digital solutions with existing IT infrastructure. The lack of standardized data protocols means that valuable insights from one aircraft type may not be applicable to another, limiting the scalability of predictive models. Engineers must navigate disparate interfaces and data structures, which increases the likelihood of errors and reduces overall efficiency. Until industry-wide standards for data exchange and system compatibility are established, airlines will continue to face hurdles in achieving a cohesive and fully integrated health monitoring ecosystem across their diverse fleets.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.12% |

| Segments Covered | By End User, Subsystem,Transmission Mode and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Honeywell International Inc., RTX Corporation (Collins Aerospace), General Electric Company (GE Aerospace), Airbus SE, The Boeing Company, Safran S.A., Thales Group, Lufthansa Technik AG, Meggitt PLC (Parker Meggitt), Curtiss-Wright Corporation, Rolls-Royce Holdings plc, Teledyne FLIR LLC, FLYHT Aerospace Solutions Ltd., CAMP Systems International, Inc., and Emerson Electric Co., among others. |

SEGMENTAL ANALYSIS

By End User Insights

The airlines segment dominated the market by capturing the major share of the global market in 2025 due to their direct operational responsibility for fleet availability and cost management. The dominance of airlines segment in the global market can be credited to the urgent need to minimize unscheduled maintenance events, which severely impact profitability. According to the International Air Transport Association, airlines lose an estimated 10 million flight hours annually due to technical delays and cancellations, which translates to billions of dollars in lost revenue. Health monitoring systems allow carriers to transition from reactive repairs to predictive maintenance, thereby reducing aircraft-on-ground time by up to 20%, as per data from Boeing. This capability is critical, as each hour of unexpected downtime can cost a wide-body operator between 100,000 and 150,000 dollars. Furthermore, airlines face intense pressure to maintain high dispatch reliability rates, often exceeding 99%, to remain competitive. By leveraging real-time data, airlines can optimize spare parts inventory and labor scheduling, which reduces overall maintenance costs by approximately 15%, according to McKinsey and Company. The financial imperative to maximize asset utilization drives airlines to invest heavily in these technologies, ensuring that every aircraft spends more time generating revenue rather than undergoing unnecessary inspections. This economic motivation solidifies the position of airlines as the largest consumers of health monitoring solutions globally.

On the other end, the MRO segment is predicted to record a CAGR of 9.1% during the forecast period in the global market owing to the increasing outsourcing of maintenance activities by airlines seeking to reduce fixed costs and improve operational flexibility. As per Aviation Week, the global MRO market is expected to reach 95 billion dollars by 2026, creating a substantial demand for advanced diagnostic tools. MRO facilities are adopting health monitoring systems to enhance their service offerings and provide value-added analytics to their airline clients. These systems enable MROs to perform more accurate fault isolation, which reduces turnaround time by up to 30%, according to SITA. Additionally, the aging global fleet requires more frequent and complex maintenance interventions, which necessitates sophisticated monitoring capabilities. Industry reports indicate that the average age of commercial aircraft has increased, leading to higher maintenance requirements. MRO providers utilize these systems to comply with stringent regulatory standards while improving efficiency. The ability to offer predictive insights as part of their service portfolio allows MROs to differentiate themselves in a competitive market. This strategic shift towards data-driven maintenance services fuels the rapid adoption of health monitoring technologies within the MRO sector.

By Subsystem Insights

The engine subsystem segment led the market by holding the largest share of the global market in 2025. The growth of the engine subsystem segment in the global market is attributed to the critical nature of propulsion integrity and the high cost associated with engine failures. Engines are the most expensive components on an aircraft, and their failure can result in catastrophic safety incidents and massive financial losses. According to Rolls-Royce, engine-related maintenance accounts for approximately 40% of total aircraft maintenance costs and is making proactive monitoring essential for cost control. Health monitoring systems track parameters such as vibration, temperature, and pressure in real-time, allowing for early detection of anomalies. The Federal Aviation Administration mandates strict monitoring protocols for turbine engines, requiring continuous data collection to ensure airworthiness. As per GE Aerospace, modern engines generate over 1 terabyte of data per flight, which is analyzed to predict component wear and tear. This data-driven approach enables operators to schedule engine washes and part replacements optimally, extending engine life by up to 15%. The complexity of modern high-bypass turbofan engines, with thousands of moving parts, necessitates sophisticated monitoring solutions. Airlines prioritize engine health because an in-flight shutdown can cost over 500,000 dollars in diversion and repair expenses. Consequently, the high stakes involved in engine performance drive the dominant adoption of monitoring systems for this subsystem across the global aviation industry.

The avionics and electrical systems segment is experiencing the fastest growth and is expected to exhibit a CAGR of 10.4% during the forecast period owing to the increasing digitalization of aircraft cockpits and cabin systems. Modern aircraft rely heavily on complex electronic networks for navigation, communication, and flight control, making their reliability paramount. According to Honeywell, the number of electronic components in new-generation aircraft has increased by 50% compared to previous models, raising the risk of system failures. Health monitoring systems for avionics detect issues such as software glitches, sensor drifts, and wiring faults before they affect flight operations. The European Union Aviation Safety Agency has introduced new regulations requiring enhanced monitoring of electrical systems to prevent incidents like those caused by lithium battery fires. As per SAE International, electrical faults account for nearly 20% of all reported technical issues in commercial aviation. The integration of Internet of Things sensors into avionics bays allows for continuous monitoring of heat and humidity levels, which can degrade electronic components. Airlines are increasingly adopting these systems to avoid costly avionics replacements, which can exceed 100,000 dollars per unit. The trend towards more electric aircraft further accelerates the demand for robust monitoring solutions in this segment, ensuring seamless operation of critical digital infrastructure.

By Transmission Mode Insights

The ground-based transmission modes segment captured the highest share of the global market in 2025. The growth of this segment in the global market is majorly attributed to their established infrastructure and lower implementation costs compared to onboard real-time systems. Most airlines rely on post-flight data downloads or periodic transmissions via ACARS, which are sufficient for many routine maintenance tasks. According to SITA, 70% of airlines still primarily use ground-based data processing for non-critical health monitoring applications. This approach avoids the high bandwidth costs associated with continuous real-time satellite transmission. Ground-based systems allow for comprehensive analysis using powerful server clusters that can process large datasets without the weight and power constraints of onboard computers. The International Air Transport Association notes that ground-based solutions are preferred for long-term trend analysis and fleet-wide performance benchmarking. These systems integrate easily with existing maintenance management software, providing a familiar workflow for engineers. The initial investment for ground-based infrastructure is significantly lower, making it accessible to smaller carriers. As per Boeing, the majority of predictive maintenance algorithms are currently deployed on ground servers where computing power is abundant. This cost-effectiveness and ease of integration sustain the dominance of ground-based transmission modes in the current market landscape despite the emergence of newer technologies.

On the other side, the onboard real-time transmission systems segment is the fastest-growing segment and is anticipated to register a CAGR of 12.4% during the forecast period owing to the adoption of high-throughput satellite communications, such as Ka-band and LEO satellites, enables continuous data streaming from aircraft to ground stations. According to Inmarsat, global aviation connectivity revenues are growing at 8% annually, facilitating real-time monitoring capabilities. Onboard systems allow airlines to receive alerts during flight, enabling pilots and ground crews to prepare for potential issues before landing. This capability reduces turnaround time and improves schedule reliability, which is crucial for low-cost carriers. The Federal Aviation Administration encourages the use of real-time data for critical safety parameters to enhance situational awareness. As per industry reports, the installation of advanced avionics with real-time data links has increased by 25% in new aircraft deliveries. Onboard processing units can filter and prioritize data, ensuring that only critical information is transmitted, thus optimizing bandwidth usage. The ability to monitor engine performance and structural integrity in real-time provides a significant competitive advantage. This technological advancement is driving rapid adoption as airlines seek to maximize operational efficiency and safety through instant access to vital aircraft health data.

REGIONAL ANALYSIS

North America Aircraft Health Monitoring System Market Analysis

North America had the largest share of 36.1% of the global market in 2025 and is expected to remain the global leader in the coming years due to massive investment in predictive maintenance and advanced digital tools. The region's dominance is underpinned by the presence of major aircraft manufacturers, such as Boeing, and extensive airline operations. According to the Federal Aviation Administration, the United States has the world's largest commercial fleet, with over 7,500 active aircraft requiring advanced maintenance solutions. The strict regulatory environment enforced by the FAA mandates rigorous compliance with safety standards, which drives the adoption of monitoring technologies. Major airlines like Delta and American Airlines have invested heavily in predictive maintenance platforms to improve operational efficiency. As per industry analysis, the North American MRO market is valued at 25 billion dollars, reflecting strong demand for technical services. The region also benefits from a mature technology ecosystem with leading software providers offering sophisticated analytics tools. The high labor costs in North America further incentivize automation and predictive maintenance to reduce manual inspection requirements. Government initiatives supporting aviation safety and innovation continue to fuel market growth. The concentration of research and development activities in the United States ensures that North America remains at the forefront of technological advancements in aircraft health monitoring.

Europe Aircraft Health Monitoring System Market Analysis

The European market is likely to experience sustained growth over the next few years as regional carriers focus on digital twin technologies and sustainability goals. Europe represents the second-largest market for aircraft health monitoring systems, driven by stringent safety regulations and a dense network of international flights. The European Union Aviation Safety Agency enforces comprehensive maintenance protocols that require detailed documentation and proactive fault detection. According to Eurostat, the European aviation sector carried over 900 million passengers in 2025, creating immense pressure on fleet reliability. Major carriers such as Lufthansa and Air France-KLM have pioneered the use of digital twin technology for predictive maintenance. As per Airbus, the European aerospace industry invests over 5 billion euros annually in research and development, including health monitoring innovations. The region's focus on sustainability also drives adoption, as efficient maintenance reduces fuel consumption and emissions. The presence of leading engine manufacturers like Rolls-Royce and Safran facilitates the integration of advanced monitoring systems. Regulatory mandates for noise and emission reductions further compel airlines to optimize engine performance through continuous monitoring. The collaborative nature of the European aviation industry promotes standardization and knowledge sharing, which accelerates technology adoption. These factors collectively sustain Europe's strong position in the global market.

Asia Pacific Aircraft Health Monitoring System Market Analysis

The Asia-Pacific region is expected to lead global growth in health monitoring system adoption over the next few years due to fleet expansion and rapid digital integration. Asia-Pacific is the fastest-growing regional market for aircraft health monitoring systems due to the rapid expansion of air travel and fleet modernization. According to the International Civil Aviation Organization, Asia-Pacific is expected to account for 40% of global air traffic by 2030. Countries like China and India are expanding their commercial fleets aggressively, with China alone adding over 200 new aircraft annually. As per Boeing, the Asia-Pacific MRO market is projected to grow at 6% annually, driven by increasing maintenance requirements. Governments in the region are investing in aviation infrastructure and promoting local manufacturing, which boosts demand for advanced technologies. Airlines such as Singapore Airlines and Cathay Pacific are early adopters of digital maintenance solutions to maintain their competitive edge. The rising middle class in emerging economies is driving passenger growth, which necessitates higher fleet availability. Regulatory bodies in countries like Japan and Australia are aligning their standards with global best practices, encouraging technology adoption. The availability of skilled IT professionals in the region supports the development and implementation of complex monitoring systems. These dynamics position Asia-Pacific as a key growth engine for the global market.

Latin America Aircraft Health Monitoring System Market Analysis

The Latin American aviation sector is likely to continue its path toward modernization and increased safety oversight over the next few years. Latin America holds a modest but steadily growing share of the aircraft health monitoring system market, characterized by gradual fleet upgrades and regulatory improvements. According to the International Air Transport Association, Latin American airlines are focusing on cost optimization to remain competitive in a price-sensitive market. Major carriers like LATAM and Avianca are increasingly adopting predictive maintenance tools to reduce operational disruptions. As per IATA, the region's air traffic is recovering strongly, with passenger numbers reaching 90% of pre-pandemic levels. The high-altitude operations in countries like Colombia and Peru place additional stress on aircraft components, necessitating robust monitoring. Regulatory agencies such as ANAC in Brazil are strengthening safety oversight, which drives compliance with international standards. The limited availability of local MRO facilities encourages airlines to use remote monitoring services provided by global vendors. Economic volatility in some countries poses challenges, but the overall trend towards modernization supports market growth. Partnerships with global technology providers enable local airlines to access advanced solutions without heavy upfront investments. This collaborative approach facilitates the gradual penetration of health monitoring systems across the region.

COMPETITIVE LANDSCAPE

The competition in the aircraft health monitoring system market is characterized by intense rivalry among established aerospace giants and emerging technology specialists who strive to offer superior predictive analytics and real time data processing capabilities. Major players differentiate themselves through proprietary algorithms and exclusive partnerships with aircraft manufacturers which allow for deeper integration of monitoring sensors into new airframes. The market sees continuous innovation as companies race to develop more accurate machine learning models that can predict component failures with greater precision and earlier warning times. Competitive pressure drives significant investment in cybersecurity measures to protect the increasing volume of transmitted data from potential breaches. Smaller niche firms often compete by offering specialized solutions for specific subsystems such as avionics or landing gear which larger corporations may overlook. The landscape is further complicated by the need for interoperability across diverse fleet types forcing vendors to adapt their platforms for seamless integration. This dynamic environment encourages constant technological advancement and strategic alliances to maintain relevance and capture growing demand from airlines seeking to optimize maintenance costs and enhance operational safety standards globally.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the global aircraft health monitoring system market include

- Honeywell International Inc.

- RTX Corporation (Collins Aerospace)

- General Electric Company (GE Aerospace)

- Airbus SE

- The Boeing Company

- Safran S.A.

- Thales Group

- Lufthansa Technik AG

- Meggitt PLC (Parker Meggitt)

- Curtiss-Wright Corporation

- Rolls-Royce Holdings plc

- Teledyne FLIR LLC

- FLYHT Aerospace Solutions Ltd.

- CAMP Systems International, Inc.

- Emerson Electric Co.

Top Players in the Global Market

GE Aerospace

GE Aerospace stands as a pivotal force in aviation technology by integrating advanced sensor networks directly into its engine designs. The company actively develops digital twin technologies that simulate engine performance under various conditions to predict maintenance needs accurately. Recent initiatives include expanding its FlightPulse application which provides pilots with real time data analytics for fuel efficiency and engine health. GE Aerospace collaborates closely with airlines to customize monitoring solutions that reduce unscheduled downtime significantly. Their focus on artificial intelligence enables precise fault detection before components fail thereby enhancing safety and operational reliability. This proactive approach solidifies their reputation as a leader in predictive maintenance innovation while supporting global carriers in optimizing fleet performance through data driven insights and continuous technological advancement in propulsion systems.

Rolls Royce

Rolls Royce leverages its extensive expertise in propulsion systems to deliver comprehensive health monitoring solutions through its IntelligentEngine vision. The company utilizes vast amounts of data from connected engines to provide actionable insights for maintenance planning and operational efficiency. Recent actions include enhancing its Rhythm service platform which offers predictive analytics and remote diagnostics for airline customers globally. Rolls Royce invests heavily in machine learning algorithms to identify patterns that indicate potential failures early in the lifecycle. Their commitment to sustainability drives innovations that monitor engine performance to minimize fuel consumption and emissions. By offering tailored support packages based on real time data Rolls Royce strengthens customer relationships and ensures high dispatch reliability for its global client base while maintaining technological leadership in the aerospace sector.

Safran

Safran plays a critical role in the market by providing integrated avionics and landing system monitoring capabilities that complement engine health data. The company focuses on developing smart sensors and embedded software that track structural integrity and system performance across various aircraft subsystems. Recent efforts include partnering with technology firms to enhance cybersecurity measures for data transmission and storage within their monitoring platforms. Safran’s Prognostics and Health Management solutions enable airlines to anticipate maintenance requirements for electrical and hydraulic systems effectively. Their investment in research and development aims to create lighter and more efficient monitoring hardware that reduces overall aircraft weight. By delivering robust and reliable data analytics tools Safran supports operators in achieving higher safety standards and operational efficiency while reinforcing its position as a key innovator in aerospace technology solutions.

Top Strategies Used by Key Market Participants

Key players in the aircraft health monitoring system market primarily focus on strategic partnerships and collaborations to expand their technological capabilities and market reach. Companies actively invest in research and development to integrate artificial intelligence and machine learning algorithms into their platforms for enhanced predictive accuracy. Mergers and acquisitions are frequently employed to acquire specialized software firms or sensor manufacturers that complement existing product portfolios. Leading participants also prioritize cloud computing infrastructure to handle the vast amounts of data generated by modern aircraft efficiently. Customization of services for specific airline needs helps build long term customer relationships and ensures high retention rates. Additionally firms emphasize cybersecurity enhancements to protect sensitive operational data from emerging threats. These strategies collectively drive innovation and strengthen competitive positioning in the rapidly evolving digital aviation landscape.

MARKET SEGMENTATION

The research report on the global aircraft health monitoring system market has been segmented and sub-segmented based on categories.

By End User

- OEMS

- Airlines

- MRO

By Sub-system

- Engines

- Avionics

- Aircraft Structures

- Environmental Control and Ancillary Systems

By Transmission Mode

- Onboard

- Ground-based

By Component

- Hardware

- Software

- Services

By Fit

- Line-fit

- Retrofit

By Aircraft Type

- Fixed-Wing

- Rotary Wing

- Military Unmmaned Aerial Vehicles

- Advanced Air Mobility

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com