Global Aircraft Survivability Equipment Market Size, Share, Trends & Growth Forecast Report – Segmented By Type ( Electronic Warfare Systems, Countermeasure Systems, Survivability Software Sensor, Systems), Application, End Use, Platform and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Aircraft Survivability Equipment Market Report Summary

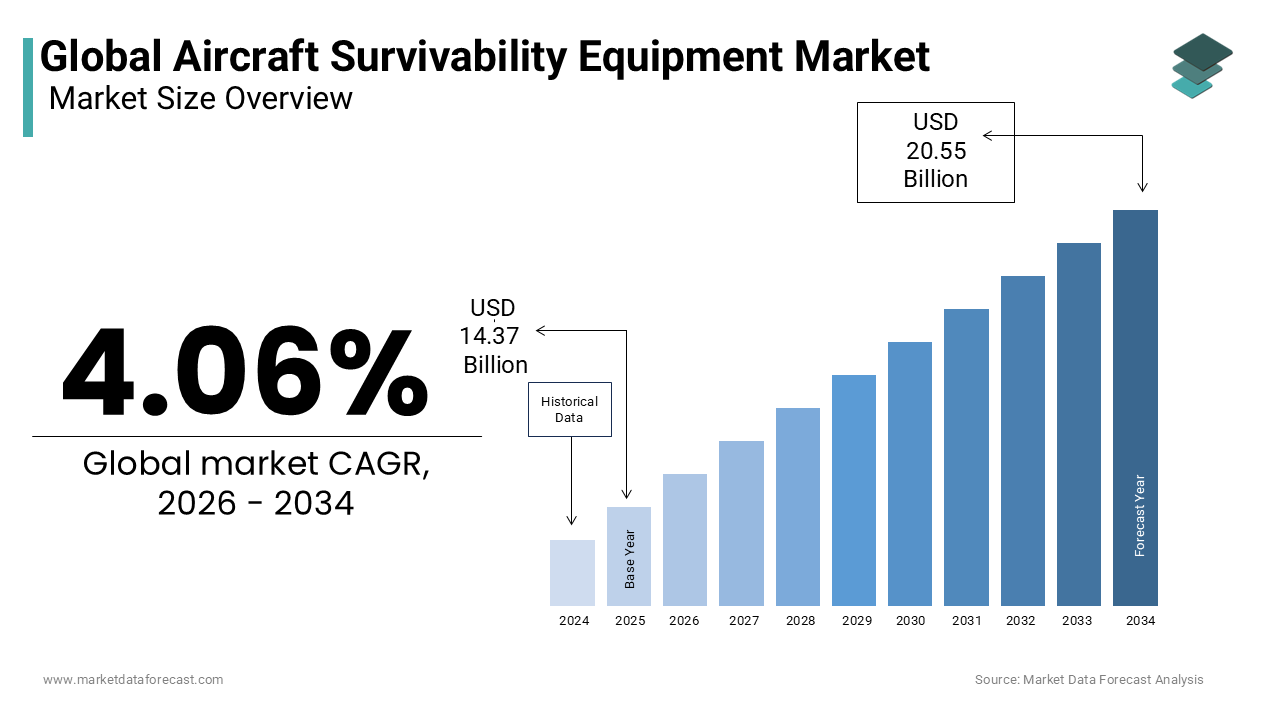

The global aircraft survivability equipment market was valued at USD 14.37 billion in 2025 and is anticipated to reach USD 14.95 billion in 2026 from USD 20.55 billion by 2034, growing at a CAGR of 4.06% during the forecast period from 2026 to 2034. The growth of the global aircraft survivability equipment market is driven by rising geopolitical tensions, increasing military modernization programs, and growing procurement of advanced combat aircraft worldwide. Expanding investments in electronic warfare capabilities, increasing demand for integrated self-protection systems, and rising deployment of advanced missile warning and countermeasure technologies are further accelerating market growth. Moreover, the integration of artificial intelligence into electronic warfare systems, advancements in cognitive threat detection technologies, and increasing adoption of survivability solutions for unmanned aerial vehicles (UAVs) are supporting the expansion of the global aircraft survivability equipment market.

Key Market Trends

-

Rising adoption of artificial intelligence-based cognitive electronic warfare systems.

-

Increasing integration of directed infrared countermeasure (DIRCM) technologies into military aircraft.

-

Growing deployment of lightweight survivability equipment for unmanned aerial vehicles.

-

Rising investments in multi-spectral threat detection and integrated electronic warfare suites.

-

Increasing focus on open-architecture survivability software enabling rapid system upgrades.

Segmental Insights

- Based on type, the electronic warfare systems segment dominated the global aircraft survivability equipment market in 2025. The dominance of the segment is attributed to the increasing proliferation of advanced radar-guided missile systems, growing deployment of active jamming technologies, rising modernization of military aviation fleets, and expanding investments in comprehensive electronic protection systems capable of countering multi-frequency threats. Continuous advancements in digital radio frequency memory technologies further strengthen segment growth.

- The survivability software segment is projected to witness the fastest CAGR of 9.4% during the forecast period owing to increasing integration of artificial intelligence, growing adoption of cognitive electronic warfare platforms, expanding software-defined defense systems, and rising demand for autonomous threat detection and adaptive countermeasure capabilities.

- Based on application, the military aircraft segment dominated the global aircraft survivability equipment market in 2025. The growth of the segment is driven by mandatory installation of self-protection systems on combat aircraft, increasing defense modernization initiatives, expanding procurement of fighter aircraft and military helicopters, and growing emphasis on crew safety and mission survivability in contested operational environments.

- The unmanned aerial vehicles (UAVs) segment is anticipated to register the fastest CAGR of 10.4% during the forecast period due to increasing deployment of military drones for intelligence, surveillance, reconnaissance, and strike missions, growing investments in autonomous defense systems, rising demand for lightweight countermeasure technologies, and expanding utilization of UAVs in high-threat operational environments.

- Based on end use, the government segment dominated the global aircraft survivability equipment market in 2025. The dominance of the segment is attributed to rising military expenditures, increasing procurement of advanced defense platforms, expanding long-term modernization programs, and strong investments in electronic warfare capabilities by national defense organizations worldwide.

- The defense contractors segment is expected to witness the fastest CAGR of 8.2% during the forecast period owing to increasing outsourcing of aircraft modernization programs, growing performance-based logistics contracts, expanding lifecycle support services, and rising participation of private defense companies in military fleet upgrades and sustainment activities.

Regional Insights

- North America dominated the global aircraft survivability equipment market and accounted for 41.1% of the global market share in 2025. The region's leadership is driven by the world's largest defense budget, continuous modernization of military aircraft, extensive investments in sixth-generation fighter programs, and strong presence of leading defense contractors. Ongoing research and development in electronic warfare and directed energy technologies further strengthen regional market growth.

- The United Kingdom held a significant share of the global aircraft survivability equipment market owing to its leadership in advanced defense programs, increasing investments in the Tempest Future Combat Air System, strong aerospace manufacturing capabilities, and active participation in multinational defense modernization initiatives. Continuous innovation in electronic warfare technologies further supports market expansion.

- China is projected to witness the fastest growth during the forecast period due to rapid military modernization, expanding indigenous fighter aircraft production, increasing investments in electronic warfare capabilities, growing deployment of stealth aircraft, and rising development of artificial intelligence-enabled survivability systems.

- Brazil continues to maintain a notable position in the global market owing to modernization of military aviation assets, integration of advanced survivability systems into newly acquired combat aircraft, growing domestic aerospace manufacturing capabilities, and increasing focus on strengthening national defense preparedness.

- Israel is expected to experience significant growth during the forecast period due to continuous operational deployment of advanced electronic warfare technologies, strong indigenous defense innovation, expanding exports of aircraft self-protection systems, and ongoing investments in combat-proven survivability solutions for both domestic and international defense markets.

Competitive Landscape

The global aircraft survivability equipment market is highly competitive and characterized by the presence of major defense contractors competing through continuous technological innovation, advanced electronic warfare capabilities, artificial intelligence integration, and next-generation threat detection systems. Leading companies are focusing on developing cognitive electronic warfare platforms, multi-spectral threat detection technologies, directed infrared countermeasure systems, and open-architecture survivability software capable of rapid upgrades against evolving threats. Strategic defense partnerships, long-term government contracts, investments in research and development, and expansion into unmanned aerial vehicle protection technologies continue to strengthen competitive positioning across the global aircraft survivability equipment market. The prominent players operating in the global aircraft survivability equipment market include BAE Systems plc, RTX Corporation, Northrop Grumman Corporation, L3Harris Technologies, Inc., Lockheed Martin Corporation, Raytheon Technologies, Elbit Systems Ltd., Saab AB, Leonardo S.p.A., Thales Group, Israel Aerospace Industries Ltd. (IAI), ASELSAN A.S., Chemring Group PLC, Terma A/S, Indra Sistemas, S.A., and Rheinmetall AG.

Global Aircraft Survivability Equipment Market Size

The global aircraft survivability equipment market size was valued at USD 14.37 billion in 2025 and is anticipated to reach USD 14.95 billion in 2026 from USD 20.55 billion by 2034, growing at a CAGR of 4.06% during the forecast period from 2026 to 2034.

Aircraft survivability equipment are a sophisticated array of defensive systems designed to protect military and commercial aviation assets from hostile threats including radar guided missiles, infrared homing projectiles, and laser designators. This critical sector includes radar warning receivers, missile approach warning systems, directed infrared countermeasures, and chaff flare dispensers that collectively enhance the probability of mission success and crew survival. The operational integrity of these systems is paramount in modern asymmetric warfare where portable air defense systems pose significant risks to low flying aircraft. According to the Stockholm International Peace Research Institute, global military expenditure reached 2443 billion US dollars in 2024, reflecting heightened geopolitical tensions and increased investment in defense capabilities across major powers. The proliferation of advanced surface to air missiles in conflict zones such as Eastern Europe and the Middle East has accelerated the urgency for upgrading legacy fleets with modern electronic warfare suites. Furthermore, the United States Department of Defense mandates strict survivability standards for all new tactical aircraft requiring integrated self-protection systems capable of detecting and neutralizing multiple simultaneous threats. The integration of artificial intelligence into threat detection algorithms allows for faster response times and more accurate threat classification, thereby reducing false alarms and enhancing pilot situational awareness. This technological evolution transforms passive defense mechanisms into active intelligent shields that adapt to evolving threat landscapes, ensuring the continued relevance and necessity of advanced survivability equipment in contemporary aerial operations.

MARKET DRIVERS

Escalation of Geopolitical Conflicts Drives Demand for Advanced Countermeasure Systems

The intensification of regional conflicts and the resurgence of great power competition are expected to continue driving significant demand for advanced aircraft survivability equipment, which is a key market driver. According to the International Institute for Strategic Studies, the number of active armed conflicts globally increased by approximately 15% in 2024, which is leading to higher attrition rates for rotary wing and fixed wing aircraft operating in contested environments. Modern battlefields are saturated with man portable air defense systems and sophisticated radar networks that require aircraft to be equipped with state of the art electronic warfare suites to survive. For instance, the ongoing conflicts in Eastern Europe have demonstrated the vulnerability of helicopters to infrared guided missiles, prompting immediate upgrades to directed infrared countermeasure systems on NATO allied fleets. These systems use high energy lasers to disrupt the guidance heads of incoming missiles, providing a last line of defense that is far more effective than traditional flares. Additionally, the rise of drone swarms and loitering munitions has created new threat vectors that necessitate rapid adaptation of survivability equipment to detect and jam small unmanned aerial vehicles. Governments are allocating substantial portions of their defense budgets to procure these advanced systems, ensuring that their air forces maintain operational superiority in high threat environments. This urgent need to mitigate risk and preserve valuable assets drives consistent procurement of cutting edge survivability technologies across global defense sectors.

Modernization of Legacy Fleet Platforms Necessitates Integration of Digital Survivability Suites

Extensive modernization programs aimed at extending the service life of legacy military aircraft platforms are likely to remain a primary driver for the aircraft survivability equipment market throughout the next several years as older systems become obsolete against modern threats. According to the United States Air Force, nearly 60% of its tactical fighter fleet consists of fourth generation aircraft that require comprehensive avionics and survivability upgrades to remain viable in near peer conflicts. These retrofit programs involve replacing analog radar warning receivers with digital radio frequency memory based jammers and integrating full spectrum missile approach warning sensors that provide 360 degree coverage. The complexity of integrating these new digital systems into existing airframes requires specialized engineering and rigorous flight testing to ensure electromagnetic compatibility and structural integrity. For example, the F 16 Viper upgrade program includes the installation of advanced electronic warfare pods that enhance situational awareness and self-protection capabilities without altering the fundamental aerodynamics of the aircraft. Similarly, naval aviation forces are upgrading their helicopter fleets with next generation countermeasure dispensers that can deploy both chaff and flares in precise sequences to defeat multi spectral threats. The sheer volume of aircraft undergoing mid-life updates ensures a steady and predictable demand for survivability equipment manufacturers who can provide modular and scalable solutions. This sustained modernization effort supports long term revenue streams and fosters continuous innovation in defensive technologies to meet evolving operational requirements.

MARKET RESTRAINTS

High Development and Certification Costs Restrict Market Entry for New Innovators

The exorbitant costs associated with research, development, and regulatory certification that creates high barriers to entry for smaller firms is hindering the aircraft survivability equipment market growth. Developing a new radar warning receiver or directed infrared countermeasure system requires extensive investment in advanced signal processing algorithms, hardware miniaturization, and rigorous laboratory testing. According to the Government Accountability Office, the average cost to develop and certify a new electronic warfare suite for a tactical aircraft can exceed 500 million US dollars, involving years of engineering effort and thousands of flight test hours. These financial demands limit the number of capable suppliers to a few large defense contractors who possess the necessary capital and technical expertise. Furthermore, the certification process involves strict compliance with military standards such as MIL STD 810 for environmental durability and MIL STD 461 for electromagnetic interference, which adds layers of complexity and expense. Small and medium sized enterprises often struggle to secure the funding required to navigate this lengthy and costly approval pathway, limiting innovation and competition in the market. Additionally, the niche nature of the industry means that production volumes are relatively low, preventing economies of scale that could otherwise reduce unit costs. This financial constraint slows the pace of technological disruption and maintains the dominance of incumbent players who can absorb the high upfront investments required for product development.

Technical Complexity of Integrating Multi Spectral Sensors in Compact Airframes

Integrating multi spectral sensors and countermeasure systems into increasingly compact and stealthy airframes is further inhibiting the aircraft survivability equipment market expansion. Modern fifth generation fighters such as the F 35 Lightning II and F 22 Raptor have strict internal volume constraints to maintain low observable characteristics, making it difficult to fit bulky radar warning antennas and flare dispensers without compromising aerodynamic performance or radar cross section. According to Lockheed Martin, engineers must utilize conformal antenna arrays embedded within the aircraft skin, which requires sophisticated manufacturing techniques and materials science innovations to ensure seamless integration. These embedded systems must also withstand extreme thermal and mechanical stresses during high speed maneuvers and supersonic flight without degrading signal quality. The complexity is further compounded by the need to manage electromagnetic interference between the survivability suite and other onboard avionics such as communication and navigation systems. Ensuring that the jamming signals do not disrupt friendly communications requires advanced frequency hopping and spatial nulling technologies that add computational burden to the central mission computer. Additionally, the cooling requirements for high power directed infrared countermeasure lasers necessitate efficient thermal management systems that do not add excessive weight or drag. These intricate engineering challenges extend development timelines and increase the risk of project delays, thereby restraining the speed at which new survivability technologies can be fielded.

MARKET OPPORTUNITIES

Expansion of Unmanned Aerial Vehicle Fleets Creates Demand for Lightweight Survivability Solutions

The rapid proliferation of unmanned aerial vehicles in military operations presents a significant opportunity for the aircraft survivability equipment market as developers seek lightweight and compact defensive systems tailored for drone platforms over the next few years. According to the Drone Industry Insights, the global military drone market is expected to grow by 12% annually through 2030, driven by the increasing use of unmanned systems for reconnaissance, strike, and electronic warfare missions. Unlike manned aircraft, drones have strict payload and power limitations, requiring survivability equipment that is significantly smaller and more energy efficient than traditional systems. Manufacturers are developing miniaturized radar warning receivers and laser warning sensors that can be integrated into small tactical drones without affecting their endurance or flight performance. Furthermore, the rise of swarm tactics necessitates distributed survivability solutions where individual drones share threat data to create a collective defensive shield. This network centric approach allows for coordinated jamming and decoy deployment that enhances the survival probability of the entire swarm. Companies that can produce ruggedized, low power, and highly integrated survivability modules will capture a growing segment of the market as air forces expand their unmanned fleets. This shift toward autonomous and semi-autonomous platforms opens new avenues for innovation in miniaturized electronics and artificial intelligence driven threat response algorithms.

Adoption of Artificial Intelligence for Cognitive Electronic Warfare Enhances Threat Response Capabilities

The integration of artificial intelligence and machine learning into aircraft survivability equipment offers a promising opportunity for the aircraft survivability equipment market. Traditional rule based systems struggle to keep pace with rapidly evolving radar and missile technologies, but AI driven cognitive electronic warfare systems can learn and adapt in real time. According to DARPA, the agency is actively funding projects that utilize deep learning algorithms to identify unknown radar signatures and automatically generate optimal jamming strategies within milliseconds. This capability allows aircraft to counter novel threats that have not been previously cataloged in database libraries, providing a significant tactical advantage. Furthermore, AI can optimize the allocation of countermeasures by predicting missile trajectories and selecting the most effective decoy or jamming technique based on historical data and current sensor inputs. This reduces the workload on pilots and improves the efficiency of defensive operations. As adversaries develop more sophisticated agile radars and dual mode seekers, the ability of survivability systems to autonomously adapt becomes critical. Manufacturers who embed AI processors into their hardware can offer superior performance and future proof their products against emerging threats. This technological leap creates a premium market segment for intelligent survivability suites that deliver enhanced protection through adaptive and predictive capabilities.

MARKET CHALLENGES

Supply Chain Vulnerabilities for Specialized Semiconductor Components Disrupt Production

The aircraft survivability equipment market faces significant challenges due to supply chain vulnerabilities for specialized semiconductor components such as gallium nitride transmitters and field programmable gate arrays, which are essential for high performance electronic warfare systems. According to the Semiconductor Industry Association, global shortages of advanced chips have led to lead times exceeding 50 weeks for certain critical components, impacting the production schedules of major defense contractors. These semiconductors are required for high power radio frequency amplifiers and fast signal processing units that form the core of modern radar warning and jamming systems. The concentration of manufacturing capacity in specific geographic regions exposes the supply chain to geopolitical risks and trade restrictions that can abruptly halt component flows. Additionally, the stringent quality requirements for military grade chips mean that alternative sources cannot be easily qualified, leading to prolonged delays when primary suppliers face disruptions. This scarcity forces manufacturers to hold larger inventories, tying up working capital and increasing storage costs. Furthermore, the inability to secure timely deliveries of key components can delay the delivery of complete survivability suites to air forces, affecting readiness levels and operational planning. Mitigating these supply chain risks requires diversifying sourcing strategies and investing in domestic manufacturing capabilities, but these measures take time and significant capital to implement effectively.

Rapid Obsolescence of Digital Components Requires Continuous Software Updates

The rapid pace of technological advancement in digital electronics leads to frequent obsolescence of hardware components used in aircraft survivability equipment, which is further challenging the global market expansion. According to the Department of Defense, the average lifecycle of a digital component in an electronic warfare system is less than five years, compared to the 30 year service life of the aircraft platform itself. This mismatch creates a sustainment challenge where older hardware becomes unsupported by manufacturers, making it difficult to source replacement parts or integrate new software features. To address this issue, survivability systems must be designed with open architecture standards that allow for modular upgrades without replacing the entire unit. However, implementing such flexibility requires significant upfront engineering effort and rigorous testing to ensure compatibility with legacy interfaces. Furthermore, the constant need for software patches to counter new threat signatures places a burden on maintenance crews who must manage complex version control and cybersecurity protocols. Failure to keep software up to date can leave aircraft vulnerable to newly developed radar modes or missile guidance techniques. This dynamic environment requires manufacturers to provide long term support contracts and regular technology refreshes, which increases the total cost of ownership for operators. Managing this lifecycle disparity remains a persistent challenge for the industry as it strives to balance innovation with long term reliability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.06% |

| Segments Covered | By Type, Application, End Use and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | BAE Systems plc, RTX Corporation, Northrop Grumman Corporation, L3Harris Technologies, Inc., Lockheed Martin Corporation, Elbit Systems Ltd., Saab AB, Leonardo S.p.A., Thales Group, Israel Aerospace Industries Ltd. (IAI), ASELSAN A.S., Chemring Group PLC, Terma A/S, Indra Sistemas, S.A., and Rheinmetall AG, among others. |

SEGMENTAL ANALYSIS

By Type Insights

The electronic warfare systems segment accounted for the major share of the global market in 2025 and is likely to continue for the next few years, driven by the exponential proliferation of advanced surface to air missile networks and sophisticated radar installations across global conflict zones. According to the International Institute for Strategic Studies, the number of deployed mobile radar systems has increased by 22% over the last five years, forcing military aviation fleets to rely heavily on active jamming capabilities. These systems emit high power radio frequency signals to degrade enemy sensor performance and break the lock of incoming guided munitions. Modern combat environments require aircraft to simultaneously counter multiple threat emitters operating across diverse frequency bands, which necessitates the deployment of comprehensive electronic warfare suites. The sheer complexity of the modern electromagnetic spectrum means that passive defenses are no longer sufficient for mission survival. Consequently, air forces are allocating substantial portions of their modernization budgets to procure and upgrade these active jamming systems, ensuring that their tactical fleets can penetrate heavily defended airspace without suffering unacceptable attrition rates. This continuous threat evolution guarantees the sustained dominance of electronic warfare systems in the global survivability equipment landscape.

On the other side, the survivability software segment is predicted to register a CAGR of 9.4% during the forecast period in the global market owing to the revolutionary integration of artificial intelligence and cognitive electronic warfare capabilities. According to the Defense Advanced Research Projects Agency, traditional threat libraries are becoming obsolete as adversaries deploy agile radars that constantly change their frequency and pulse patterns. Cognitive software utilizes machine learning algorithms to analyze unknown radar emissions in real time and automatically generate optimal jamming waveforms within milliseconds. This autonomous adaptability allows aircraft to counter novel and previously uncataloged threats without requiring manual pilot intervention or waiting for ground crews to upload new threat databases. The ability of the software to learn and adapt on the fly provides a decisive tactical advantage in highly dynamic combat scenarios. As military branches prioritize autonomous decision making to reduce pilot cognitive load, the demand for intelligent survivability software is accelerating rapidly. This technological paradigm shift ensures that software development will outpace hardware procurement in terms of growth velocity over the forecast period.

By Application Insights

The military aircraft segment led the market with the highest share of the global market in 2025 and is expected to maintain its leading position in the market over the next few years due to the mandatory installation of comprehensive survivability suites on all combat and tactical transport platforms. According to the Royal United Services Institute, every fixed wing fighter bomber and rotary wing attack helicopter deployed by modern armed forces must be equipped with radar warning receivers, missile approach warning systems, and countermeasure dispensers to meet basic operational safety standards. These systems are not optional upgrades but fundamental requirements for force protection, ensuring that aircrews can survive in hostile environments. The sheer volume of military aircraft in global inventories, which exceeds 40,000 active tactical platforms, creates a massive baseline demand for survivability equipment. Furthermore, the rigorous operational tempo of military aviation means that these systems are subjected to constant wear and tear, necessitating frequent maintenance, replacement, and modernization. The uncompromising requirement to protect human life and multimillion dollar assets ensures that military aircraft will continue to drive the majority of revenue and technological investment in the survivability equipment sector for the foreseeable future.

However, the UAV segment is predicted to register a promising CAGR of 10.4% during the forecast period in the global market owing to the increasing deployment of autonomous systems into highly contested and denied airspace. According to Drone Industry Insights, the use of medium and high altitude long endurance drones for intelligence, surveillance, and reconnaissance missions over active combat zones has tripled in the last three years. Operating in these lethal environments exposes unmanned platforms to the same radar guided and infrared threats that target manned aircraft, necessitating the integration of advanced self protection systems. Historically, drones were considered expendable, but the rising cost and strategic value of modern unmanned platforms require them to be equipped with miniature radar warning receivers and automated countermeasure dispensers. This shift in operational doctrine ensures that unmanned aerial vehicles can survive initial enemy engagements and continue to deliver critical data. The urgent need to protect these high value intelligence assets is accelerating the procurement of specialized survivability equipment tailored specifically for unmanned platforms.

By End Use Insights

The government end use segment held the largest share of the global market in 2025 and is likely to retain the leading position in the market for the next few years due to the direct procurement of survivability equipment by national defense ministries for their armed forces. According to the Stockholm International Peace Research Institute, global military expenditure reached a record 2.4 trillion dollars in 2024, with a significant portion allocated to aviation survivability and electronic warfare programs. Governments possess the sovereign authority and financial resources to mandate the installation of specific survivability suites on their military fleets, ensuring a guaranteed and substantial revenue stream for defense contractors. These direct procurement programs often involve multiyear contracts worth billions of dollars, covering the initial installation as well as long term sustainment and upgrade services. The strategic imperative of national security compels governments to prioritize the acquisition of the most advanced and reliable survivability technologies regardless of cost. This unwavering commitment to force protection ensures that government agencies will remain the primary customers and the dominant driving force behind the financial growth of the aircraft survivability equipment market globally.

On the other hand, the defense contractors end use segment is anticipated to showcase the fastest CAGR of 8.2% during the forecast period owing to the increasing reliance on private enterprise for the maintenance, repair, and overhaul of legacy military fleets. According to the Government Accountability Office, the average age of tactical military aircraft has increased significantly, prompting defense ministries to outsource the integration of modern survivability upgrades to specialized private contractors. These contractors possess the agile engineering capabilities and specialized facilities required to retrofit older airframes with advanced digital radar warning receivers and directed infrared countermeasures without disrupting active flight operations. The shift towards performance based logistics contracts means that contractors are now financially incentivized to maintain high operational readiness rates for survivability systems, creating a recurring revenue model. By taking over the lifecycle management of these critical defensive systems, defense contractors are capturing a larger share of the total sustainment budget. This expanding role in fleet modernization and long term support ensures that the defense contractor segment will grow at the fastest pace in the coming years.

REGIONAL ANALYSIS

North America Aircraft Survivability Equipment Market Analysis

North America led the market by capturing 41.1% of the global market share in 2025. The dominance of North America in the global market is primarily driven by its unparalleled defense budget and aggressive modernization programs. According to the Department of Defense, the United States is currently investing heavily in the Next Generation Air Dominance program, which requires the development of highly advanced integrated electronic warfare and survivability suites for future sixth generation fighter aircraft. The primary driver in this region is the strategic pivot towards great power competition, which necessitates the ability to penetrate and survive in highly contested airspace defended by sophisticated surface to air missile networks. American defense contractors are at the forefront of developing cognitive electronic warfare systems and directed energy countermeasures that provide unprecedented protection against emerging threats. Furthermore, the massive existing fleet of legacy tactical aircraft requires continuous software and hardware upgrades to maintain viability against modern adversaries. The combination of massive federal funding, a robust domestic defense industrial base, and the urgent operational requirements of the United States Air Force and Navy ensures that North America remains the undisputed leader and primary innovator in the global survivability equipment landscape.

United Kingdom Aircraft Survivability Equipment Market Analysis

The United Kingdom is likely to maintain its central role as the powerhouse of the European aircraft survivability equipment market for the next few years, characterized by collaborative multinational defense programs and strict interoperability standards. According to the Ministry of Defence, the United Kingdom is leading the development of the Tempest future combat air system, which integrates cutting edge survivability software and sensor fusion directly into the airframe design. The market in this region is heavily influenced by the need to counter advanced air defense systems, prompting NATO allies to invest heavily in electronic warfare and radar warning technologies. British engineering firms are pioneering the miniaturization of threat detection sensors, allowing for seamless integration onto both manned fighters and unmanned wingmen. Furthermore, the European market places a strong emphasis on open architecture standards, ensuring that survivability systems can be rapidly updated with new threat libraries across different allied platforms. The collaborative nature of European defense procurement, combined with the technological expertise of United Kingdom based aerospace companies, ensures that the region remains a critical hub for the development and deployment of advanced aircraft survivability solutions.

China Aircraft Survivability Equipment Market Analysis

China is anticipated to remain the fastest growing and most influential market in the Asia Pacific aircraft survivability equipment sector over the next few years and is driven by massive military modernization and indigenous technological development. According to the Ministry of National Defense of the People's Republic of China, the rapid expansion of the People's Liberation Army Air Force requires the continuous integration of advanced self-protection systems on thousands of new tactical aircraft including the J 20 stealth fighter. The market in China is characterized by a strong push for technological self-reliance with domestic institutes developing sophisticated digital radio frequency memory jammers and active electronically scanned array radar warning receivers. The geopolitical tensions in the Indo Pacific region have accelerated the deployment of these advanced survivability suites to ensure air superiority in potential conflict scenarios. Furthermore, the Chinese government is heavily investing in artificial intelligence driven cognitive electronic warfare to counter the advanced threat libraries of Western adversaries. This massive scale of indigenous development and fleet expansion ensures that China will continue to drive the growth and technological innovation of the aircraft survivability equipment market in the Asia Pacific region.

Brazil Aircraft Survivability Equipment Market Analysis

Brazil is expected to maintain its position in the Latin American aircraft survivability equipment market for the next few years due to the gradual modernization and the integration of advanced systems onto newly acquired platforms. According to the Brazilian Air Force, the recent acquisition and integration of the Saab Gripen fighter jet has necessitated the procurement and local support of state of the art electronic warfare and countermeasure systems. The market in Brazil is primarily driven by the need to secure vast territorial borders and protect critical infrastructure from illicit trafficking and regional instability. Brazilian defense authorities are increasingly focusing on retrofitting their existing legacy fleets with modern radar warning receivers and missile approach warning systems to extend their operational viability. Furthermore, the local aerospace industry is developing indigenous survivability solutions to reduce reliance on foreign suppliers and promote technological sovereignty. The combination of new platform acquisitions and the urgent need to upgrade older aircraft ensures a steady demand for survivability equipment. Although the market is smaller compared to North America or Europe, the strategic focus on regional security and technological independence provides a stable foundation for market growth in Brazil and the broader Latin American region.

Israel Aircraft Survivability Equipment Market Analysis

Israel is projected to continue acting as the primary catalyst for the Middle East and Africa aircraft survivability equipment market for the next few years and is renowned for its combat proven defensive technologies and active operational environments. According to the Israel Ministry of Defense, the continuous exposure of Israeli air forces to dense and diverse threat environments, including advanced surface to air missiles and portable infrared systems, drives the relentless innovation of survivability equipment. The market in this region is characterized by the rapid fielding of combat tested electronic warfare systems and directed infrared countermeasures that are immediately refined based on real world operational feedback. Israeli defense companies are global leaders in developing compact and highly effective self-protection kits for helicopters and tactical transport aircraft operating in hostile urban environments. Furthermore, the region's strategic position drives massive export sales of these proven survivability systems to allied nations facing similar asymmetric threats. The combination of active combat experience, rapid technological iteration, and strong export demand ensures that Israel remains the most dynamic and influential market for aircraft survivability equipment in the Middle East and Africa.

COMPETITIVE LANDSCAPE

Competition in the aircraft survivability equipment market is characterized by a highly consolidated landscape dominated by a few major defense contractors with extensive technological expertise and government relationships. High barriers to entry due to stringent security clearances complex certification requirements and significant research and development costs protect incumbent players from new competitors. Leading companies differentiate themselves through superior signal processing capabilities advanced sensor fusion technologies and proven combat performance records. Price competition is secondary to technical performance and reliability as governments prioritize mission success and crew survival over cost savings. However vendors compete aggressively on lifecycle support services software update speeds and interoperability with allied systems. The shift toward cognitive electronic warfare and artificial intelligence driven threat response creates new battlegrounds for innovation where software agility becomes a key differentiator. Strategic alliances and joint ventures are frequently utilized to share development risks and access specialized technologies. Regional players focus on niche markets or specific national security needs while global leaders leverage their broad portfolios to secure large scale modernization contracts. Overall the market remains stable with continuous technological advancement and strong government funding driving sustained competitive intensity among top tier manufacturers.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the global aircraft survivability equipment market include

- BAE Systems plc

- RTX Corporation

- Leonardo S.p.A.

- Raytheon Technologies

- Northrop Grumman Corporation

- L3Harris Technologies, Inc.

- Lockheed Martin Corporation

- Elbit Systems Ltd.

- Saab AB

- Thales Group

- Israel Aerospace Industries Ltd. (IAI)

- ASELSAN A.S.

- Chemring Group PLC

- Terma A/S

- Indra Sistemas, S.A.

- Rheinmetall AG

Top Players in the Global Market

BAE Systems

BAE Systems stands as a premier global provider of advanced aircraft survivability solutions offering comprehensive electronic warfare suites and countermeasure systems. The company specializes in digital radar warning receivers and directed infrared countermeasures that protect tactical aircraft from modern missile threats. Recent strategic initiatives include the development of next generation cognitive electronic warfare capabilities that utilize artificial intelligence to adapt to unknown threat signatures in real time. BAE Systems actively collaborates with international defense agencies to integrate these advanced sensors into fifth generation fighter platforms. Their commitment to open architecture standards ensures rapid software updates and seamless interoperability with allied forces. By focusing on technological innovation and combat proven reliability BAE Systems continues to enhance the survival probability of aircrews operating in highly contested environments worldwide.

Leonardo S.p.A

Leonardo S.p.A contributes significantly to the global market through its sophisticated Miysis suite which integrates radar warning laser warning and missile approach warning systems into a unified defensive platform. The company leverages extensive expertise in sensor fusion and signal processing to deliver high performance survivability equipment for both rotary and fixed wing aircraft. Recent actions to strengthen its position involve expanding production capacities for gallium nitride based transmitters which offer superior power efficiency and jamming capabilities. Leonardo also invests heavily in research and development for miniaturized sensors tailored for unmanned aerial vehicles. The company focuses on providing modular and scalable solutions that meet diverse operational requirements. Through continuous innovation and strategic partnerships Leonardo maintains a strong reputation for delivering cutting edge defensive technologies that ensure mission success and pilot safety globally.

Raytheon Technologies

Raytheon Technologies plays a pivotal role in the aircraft survivability market by providing industry leading AN ALR 69A radar warning receivers and advanced countermeasure dispensers. The company utilizes its deep expertise in radio frequency engineering to create robust systems that detect and classify complex electromagnetic threats with high accuracy. Recent efforts to bolster its market presence include the integration of machine learning algorithms into legacy systems to enhance threat identification speed and reduce false alarms. Raytheon Technologies actively supports global military customers with comprehensive lifecycle management and rapid technology insertion programs. The company emphasizes rigorous testing and quality assurance to meet stringent military standards. By combining hardware excellence with intelligent software solutions Raytheon Technologies delivers reliable and effective self protection systems that safeguard critical aviation assets against evolving airborne and ground based dangers.

Top Strategies Used by the Key Market Participants

Key players in the aircraft survivability equipment market prioritize research and development to create cognitive electronic warfare systems that adapt autonomously to emerging threats. Strategic partnerships with original equipment manufacturers enable companies to integrate survivability suites directly into new aircraft designs ensuring optimal performance and reduced integration costs. Expansion into the unmanned aerial vehicle sector drives innovation in miniaturized sensors and low power countermeasure systems tailored for drone platforms. Investment in open architecture software allows for rapid updates and third party application integration enhancing system flexibility and lifecycle value. Focus on international export markets through foreign military sales programs helps participants diversify revenue streams and strengthen global defense alliances while maintaining technological leadership.

MARKET SEGMENTATION

The research report on the global aircraft survivability equipment market has been segmented and sub-segmented based on categories.

By Type

- Electronic Warfare Systems

- Countermeasure Systems

- Survivability Software

- Sensor Systems

By Application

- Military Aircraft

- Commercial Aircraft

- Unmanned Aerial Vehicles

By End Use

- Government

- Defense Contractors

By Platform

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com