Global Airport Information System Market Size, Share, Trends & Growth Forecast Report Segmented By Application, System Area, Deployment Mode, Airport Size, and Region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa), Industry Analysis from 2026 to 2034

Global Airport Information System Market Report Summary

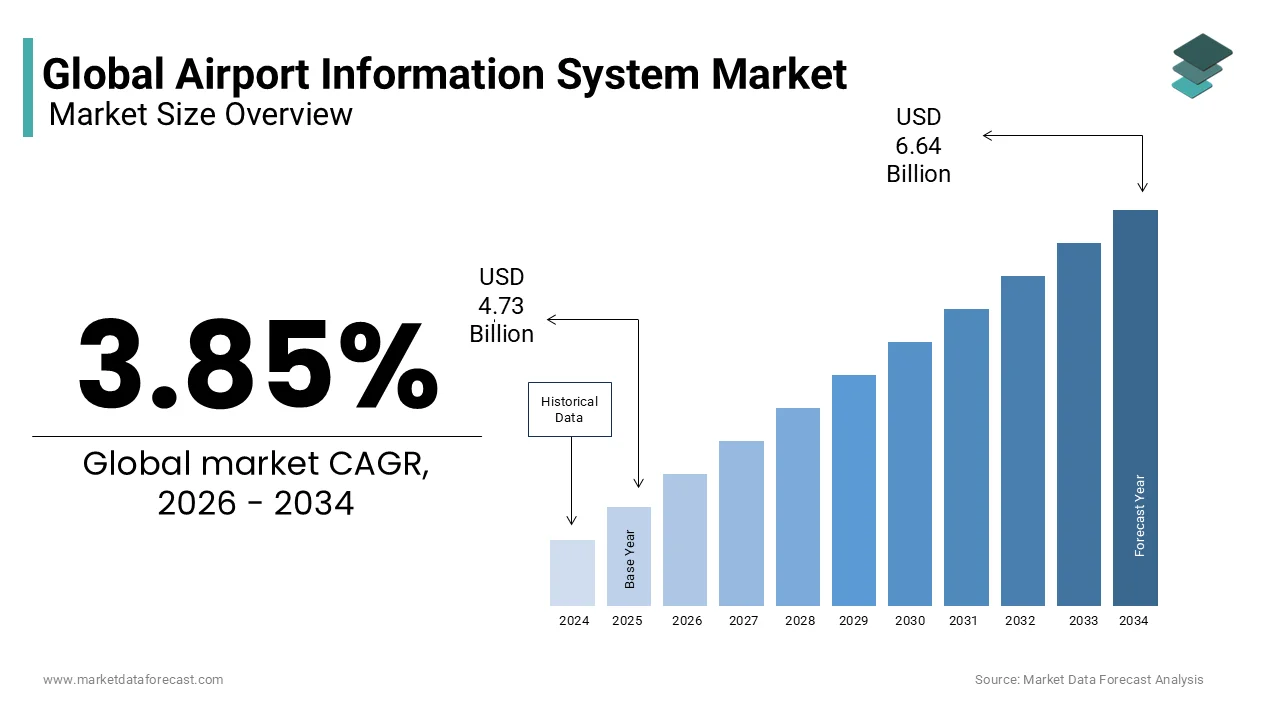

The global airport information system market was valued at USD 4.73 billion in 2025, is estimated to reach USD 4.91 billion in 2026, and is projected to reach USD 6.64 billion by 2034, growing at a CAGR of 3.85% during the forecast period from 2026 to 2034. The growth of the global airport information system market is driven by increasing investments in airport modernization, rising air passenger traffic, and the growing need for efficient airport operations and passenger management. Airports are increasingly adopting digital information systems to enhance operational efficiency, improve passenger experience, and enable real-time data management. Additionally, the integration of cloud computing, artificial intelligence, Internet of Things (IoT), and automation technologies is further supporting the expansion of airport information systems worldwide.

Key Market Trends

-

Rising investments in smart airport infrastructure are driving the adoption of advanced airport information systems.

-

Increasing demand for real-time passenger information and operational efficiency is accelerating digital transformation across airports.

-

Growing integration of artificial intelligence, IoT, and data analytics is enhancing airport decision-making and resource management.

-

Expansion of self-service technologies, including automated check-in and biometric processing, is improving passenger experience.

-

Increasing focus on cybersecurity and secure data management is driving investments in advanced airport information platforms.

Segmental Insights

-

Based on application, the passenger information segment dominated the global airport information system market in 2025. The segment's leadership is attributed to the increasing demand for real-time flight updates, passenger communication, wayfinding solutions, and enhanced traveler experience across airports.

-

Based on system area, the terminal side systems segment held the largest share of the global airport information system market in 2025. The segment's dominance is driven by the growing need for efficient terminal operations, passenger processing, baggage handling, and airport resource management.

-

Based on deployment mode, the on-premise segment accounted for the largest share of the global airport information system market in 2025. The segment's growth is supported by airports' preference for enhanced data security, system reliability, regulatory compliance, and greater control over mission-critical operational infrastructure.

Regional Insights

-

The global airport information system market is witnessing steady growth due to increasing airport digitalization, expanding aviation infrastructure, and rising demand for intelligent airport management solutions.

-

North America remains the leading regional market, supported by continuous investments in airport modernization, the presence of major international aviation hubs, and widespread adoption of advanced digital technologies. Ongoing infrastructure upgrades and smart airport initiatives are expected to sustain the region's dominant position over the forecast period.

-

Europe continues to be a significant market due to the implementation of smart airport technologies, increasing passenger traffic, and stringent aviation safety and operational standards.

Competitive Landscape

The global airport information system market is highly competitive, with technology providers focusing on cloud-based platforms, artificial intelligence, automation, and integrated airport management solutions to strengthen their market presence. Companies are investing in digital transformation, cybersecurity, biometric technologies, and strategic partnerships to improve airport operations, enhance passenger experiences, and support the development of smart airports. Key players operating in the global airport information system market include SITA N.V., Amadeus IT Group, S.A., Honeywell International Inc., THALES Group, Indra Sistemas, S.A., RTX Corporation, Airport Information Systems, IBM Corporation, NEC Corporation, Samsung Electronics Co., Ltd., T-Systems International GmbH, Siemens AG, VISION BOX – Soluções de Visão por Computador, S.A., Materna IPS GmbH, Beumer Group, INFORM Institut für Operations Research und Management GmbH, ADB SAFEGATE, Frequentis AG, and Damarel Systems International Ltd.

Global Airport Information System Market Size

The global airport information system market size was valued at USD 4.73 billion in 2025, and is expected to be worth USD 6.64 billion by 2034 from USD 4.91 billion by 2026. The market is growing at a CAGR of 3.85% during the forecast period.

Airport information system is designed to manage the complex operational workflows of modern aviation hubs. These systems include flight information display systems, resource management platforms, baggage handling controls, and passenger processing interfaces that collectively ensure seamless terminal operations. The integration of these digital tools is critical for maintaining schedule adherence, enhancing passenger experience, and optimizing resource allocation across airside and landside activities. According to Airports Council International, global passenger traffic reached 9.4 billion in 2024, reflecting a robust recovery that places unprecedented strain on existing IT infrastructure. This surge in volume necessitates real-time data processing capabilities to handle dynamic scheduling changes and unexpected disruptions efficiently. The European Union mandates strict data privacy and security standards under the General Data Protection Regulation, which compels airports to upgrade their legacy systems to compliant cloud-based architectures. Furthermore, the rise of biometric identification technologies requires robust backend information systems capable of securely processing and storing sensitive passenger data while interfacing with border control agencies. As airports transition toward smart hub models, the demand for interconnected information systems that support Internet of Things devices and artificial intelligence-driven analytics becomes paramount. This technological evolution transforms static operational data into actionable insights, enabling proactive decision-making and reducing turnaround times for aircraft and passengers alike.

MARKET DRIVERS

Surge in Passenger Volumes Necessitates Advanced Resource Management Capabilities

The exponential growth in global air travel is expected to drive increased investment in sophisticated airport information systems to manage complex resource allocation in real time over the next few years, which is a key market driver. According to the International Air Transport Association, the industry expects a steady rise in passenger numbers, requiring airports to optimize every square meter of terminal space and every minute of ground time. Modern resource management systems integrate flight data with gate assignment algorithms, check-in counter availability, and baggage belt status to create a unified operational picture. This integration allows airport operators to dynamically adjust resources based on live flight updates rather than static schedules, significantly improving efficiency. For instance, during peak hours, automated systems can reassign gates to minimize taxiing times or redirect passenger flows to less congested security checkpoints. The complexity of managing mixed fleets, including narrow-body, wide-body, and regional aircraft, further amplifies the need for intelligent software that can calculate optimal stand usage based on aircraft size and turnaround requirements. Without such advanced information systems, airports risk severe congestion, leading to missed slots and financial penalties. Consequently, major hubs are investing heavily in next-generation operational databases that leverage machine learning to predict traffic patterns and suggest pre-emptive resource adjustments, ensuring smooth operations despite increasing volume pressures.

Regulatory Mandates for Data Security and Privacy Drive Infrastructure Modernization

Regulatory compliance is further fuelling the expansion of the airport information system market as airports replace legacy platforms to meet evolving cybersecurity and privacy standards over the next few years. The European Union General Data Protection Regulation imposes heavy fines for data breaches and mandates strict controls on how passenger personal information is collected, stored, and shared. According to the European Union Agency for Cybersecurity, the aviation sector faces a persistent threat landscape, highlighting the vulnerability of outdated IT systems to malicious interference. Airports must ensure that their flight information display systems, passenger processing databases, and biometric verification tools meet rigorous encryption and access control standards. This regulatory pressure drives the adoption of cloud-based airport information systems that offer built-in security features, regular automatic updates, and centralized monitoring capabilities. Furthermore, international standards, such as those set by the International Civil Aviation Organization, require robust cybersecurity measures to protect aviation data. Compliance with these regulations often necessitates a complete overhaul of legacy on-premise servers, which lack the agility and security protocols of modern cloud architectures. Airlines and ground handlers also demand secure data exchange protocols to share sensitive operational information without risking exposure. Consequently, airports prioritize vendors who can provide certified, secure solutions that guarantee data integrity while maintaining operational continuity, driving significant investment in modern airport information infrastructure.

MARKET RESTRIANTS

High Implementation Costs and Budget Constraints Restrict Adoption in Developing Regions

Financial barriers are likely to continue influencing the adoption rate of advanced information systems in resource-constrained settings, which is a significant impediment to the global market growth. A full-scale deployment involving flight information display systems, resource management modules, and integrated baggage handling controls requires a significant capital commitment depending on airport size and complexity. According to the World Bank, many airports in emerging markets operate with tight budget constraints and often prioritize physical assets like runways and terminals over digital systems. The high cost is exacerbated by the need for specialized hardware, servers, networking equipment, and customized software licensing fees. Additionally, the ongoing maintenance and upgrade costs associated with these complex systems create a long-term financial burden that many smaller airports struggle to sustain. The return on investment for information systems is often indirect, as it primarily enhances operational efficiency and passenger satisfaction rather than generating direct revenue streams. This makes it challenging for airport authorities to justify large upfront expenditures, especially when facing competing priorities such as safety enhancements or capacity expansions. Consequently, many airports in Latin America and Africa continue to rely on fragmented or manual processes that hinder operational efficiency and limit their ability to attract premium international carriers requiring advanced digital integration.

Integration Complexities with Legacy Infrastructure Impede Seamless Digital Transformation

The integration of modern systems with legacy infrastructure is further hampering the airport information system market growth. Many older airports operate on disparate, siloed systems for flight scheduling, baggage handling, and passenger processing that were developed by different vendors over decades. According to industry analysis, infrastructure compatibility issues account for a substantial percentage of delays in airport modernization projects, as engineers must devise custom middleware and application programming interfaces to enable communication between old and new technologies. The lack of standardized data formats among different systems creates interoperability challenges, requiring extensive customization and testing to ensure accurate data flow. For example, integrating a new cloud-based resource management system with an on-premise legacy flight database may require complex data mapping and synchronization protocols to prevent discrepancies. Additionally, the risk of operational disruption during the migration phase forces airports to implement changes gradually, which extends the timeline and increases costs. The scarcity of skilled IT professionals who understand both aviation operations and modern software architecture further complicates the integration process. As a result, airport authorities often hesitate to undertake comprehensive digital transformations, opting instead for incremental upgrades that may not fully realize the benefits of a unified information ecosystem, thereby slowing overall market adoption rates in mature aviation markets.

MARKET OPPORTUNITIES

Expansion of Biometric Processing Creates Demand for Integrated Identity Management Systems

The adoption of biometric technology is projected to grow as airports increasingly seek to create seamless, touchless passenger journeys, which is a notable opportunity for the global market. According to the International Air Transport Association, a majority of passengers express willingness to share biometric data for faster processing, driving airports to implement facial recognition and fingerprint scanning at key touchpoints. These biometric systems require robust backend information platforms that can securely capture, store, and match passenger identity data against government databases in real time. The integration of biometrics with flight information systems allows for automatic boarding pass validation and gate access without physical documents, enhancing both security and convenience. Major hubs, including those in the Middle East and Asia, have already deployed end-to-end biometric corridors relying on sophisticated information systems to manage the data flow between cameras, databases, and border control agencies. This shift creates demand for scalable, cloud-based identity management solutions that can handle millions of daily transactions with low latency. Furthermore, the standardization of biometric data formats through industry initiatives encourages interoperability across airlines and airports, fostering a broader ecosystem for information system providers. Manufacturers who offer integrated, biometric-ready platforms gain a competitive edge by enabling airports to future-proof their operations and meet evolving passenger expectations for frictionless travel experiences.

Growth of Smart Airport Initiatives Drives Adoption of IoT Enabled Operational Platforms

The trend toward smart airport development is expected to open significant opportunities for the airport information system market. According to SITA, a majority of airports are currently investing in smart technologies to enhance operational efficiency and passenger experience, creating a fertile ground for connected information systems. Modern airport information platforms act as the central nervous system, aggregating data from IoT sensors embedded in baggage belts, parking spots, restrooms, and boarding bridges. This real-time data enables predictive maintenance, automated resource allocation, and proactive passenger notifications. For instance, smart information systems can detect a baggage belt malfunction before it causes a delay and automatically reroute luggage to an alternative carousel while notifying ground staff. The ability to visualize terminal conditions through digital twins allows operators to simulate scenarios and optimize layouts for better flow. Providers who embed advanced analytics and artificial intelligence into their information systems can offer value-added services such as demand forecasting and anomaly detection. This transformation from passive data recording to active, intelligent management aligns with broader airport digitalization strategies and opens new revenue streams through service contracts and data insights, driving innovation and differentiation in the airport information system market.

MARKET CHALLENGES

Cybersecurity Threats Pose Critical Risks to Operational Continuity and Data Integrity

Cybersecurity management is anticipated to become a foundational requirement for connected airport infrastructure as threats continue to evolve over the next few years, which is a significant challenge to the global market expansion. Ransomware and distributed denial of service attacks can cripple flight information display systems, baggage handling controls, and passenger processing databases, leading to widespread operational disruptions. According to international aviation reports, cyber incidents in the sector have risen in frequency, causing significant financial damages and reputational harm. The interconnected nature of modern airport information systems means that a breach in one module can compromise the entire network, exposing sensitive passenger data and disrupting flight operations. Airports must constantly update their security protocols and invest in advanced threat detection systems, which add to the operational complexity and cost. The shortage of cybersecurity experts in the aviation industry further exacerbates the vulnerability of these systems. Additionally, the reliance on third-party vendors for software components introduces supply chain risks, where vulnerabilities in external code can be exploited by attackers. Ensuring continuous protection against evolving threats requires vigilant monitoring and rapid response capabilities, which many airports struggle to maintain. This persistent security challenge undermines confidence in digital transformation initiatives and may lead to hesitation in adopting fully cloud-based or interconnected information systems.

Shortage of Skilled IT Personnel Hinders Effective System Management and Innovation

Workforce development is expected to remain a significant area of focus as the industry attempts to address the scarcity of specialized personnel over the next few years. According to international labor organizations, the global aviation sector faces a significant deficit of skilled workers, including IT specialists and systems analysts, which directly impact the deployment and upkeep of complex digital platforms. Managing integrated airport information systems requires a unique blend of technical skills in cloud computing, data analytics, and cybersecurity, along with a deep understanding of airline operations and regulatory requirements. The aging workforce in many developed countries means that institutional knowledge is retiring faster than it is being replaced, leading to gaps in expertise required for troubleshooting and optimizing these systems. Training programs for new entrants are often lengthy and costly that requires certification in multiple disciplines, which discourages rapid workforce expansion. This labor scarcity results in slower implementation timelines for new projects and delayed response times for system failures, increasing the risk of operational disruptions. Airports may face penalties for non-compliance with service level agreements if systems are not maintained properly due to a lack of qualified staff. Furthermore, the competition for skilled IT talent from other sectors, such as finance and technology, drives up wage costs, squeezing margins for service providers and limiting the capacity for innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.85% |

| Segments Covered | By Application, System Area, Deployment Mode, Airport Size, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | SITA N.V., Amadeus IT Group, S.A., Honeywell International Inc., THALES Group, Indra Sistemas, S.A., RTX Corporation, Airport Information Systems, IBM Corporation, NEC Corporation, Samsung Electronics Co., Ltd., T-Systems International GmbH, Siemens AG, VISION BOX – SOLUÇÕES DE VISÃO POR COMPUTADOR, S.A., Materna IPS GmbH, Beumer Group, INFORM Institut für Operations Research und Management GmbH, ADB SAFEGATE, Frequentis AG, and Damarel Systems International Ltd. |

SEGMENTAL ANALYSIS

By Application Insights

The passenger information application segment held the dominant share of the global market in 2025 and is expected to maintain its leading market position as the continued growth in air travel volumes necessitates reliable and accurate flight updates over the next few years. For instance, global passenger traffic continues to recover, placing unprecedented strain on terminal communication networks. Modern passenger information systems must process massive amounts of real-time data from airline operational databases to update flight information display systems instantly. This ensures that travelers receive accurate gate assignments, boarding times, and delay notifications, which is critical for managing crowd flow and preventing terminal congestion. The complexity of managing mixed fleets and dynamic scheduling changes requires highly resilient software architectures that can handle millions of simultaneous data transactions without latency. Airports prioritize these systems because accurate information directly correlates with passenger satisfaction and reduces the operational burden on customer service desks. Furthermore, the integration of mobile applications and digital signage allows airports to push targeted updates to specific terminal zones, ensuring that critical information reaches the right audience at the right time, thereby solidifying the dominance of this application segment.

On the other side, the security segment is projected to experience rapid expansion and register a CAGR of 9.4% during the forecast period owing to the integration of biometric technologies and automated screening processes. According to international security mandates, airports are increasingly required to implement advanced identity verification systems to prevent unauthorized access and streamline border control operations. Modern airport information systems now serve as the central nervous system for security operations, aggregating data from facial recognition cameras, fingerprint scanners, and automated boarding pass readers. This integration allows for the creation of seamless biometric corridors where passengers can progress from check-in to the boarding gate without presenting physical documents. The ability of these information systems to securely match passenger identity data against government watchlists in milliseconds is revolutionizing airport security protocols. Furthermore, the shift toward credential authentication technology allows airports to verify the identity of staff and crew members continuously, reducing the risk of insider threats. This technological transformation from manual document checks to automated biometric verification requires massive investments in backend information platforms capable of handling complex cryptographic operations, thereby accelerating the growth of the security application segment.

By System Area Insights

The terminal side systems segment captured the highest share of the global market in 2025 and is expected to hold the leading position in the market as major airports continue to prioritize non-aeronautical revenue streams over the next few years. For instance, activities such as retail, dining, and parking account for a significant portion of total revenue for many global airports, which is making terminal management systems essential for financial viability. Modern terminal side information systems integrate flight data with passenger flow analytics to predict peak shopping times and dynamically adjust digital advertising content on retail screens. These systems also manage complex resource allocation, including check-in counter assignments, baggage belt distribution, and gate seating availability, ensuring that terminal space is utilized with maximum efficiency. The ability to monitor real-time passenger density allows terminal managers to deploy additional staff to congested areas or open new security lanes proactively. Furthermore, the integration of customer relationship management modules enables airports to personalize marketing offers based on passenger demographics and flight destinations. This deep level of operational and commercial integration makes terminal side systems a foundational pillar of airport information infrastructure and is driving sustained investment and market leadership.

However, the airside systems segment is projected to be the fastest-growing segment and record a CAGR of 10.5% during the forecast period owing to the critical need to optimize aircraft turnaround times and maximize runway capacity. For instance, the global commercial aircraft fleet is expected to grow steadily over the coming decades, leading to potential congestion on airport aprons and taxiways. Modern airside information systems utilize advanced algorithms and real-time tracking data from aircraft transponders and ground support equipment to optimize gate assignments and taxi routes. This minimizes the time aircraft spend idling on the tarmac, reducing fuel consumption and emissions while increasing the overall throughput of the airfield. The integration of visual docking guidance systems with central airside management platforms ensures that aircraft are parked precisely within their designated stands, preventing damage and accelerating the connection of ground services. Furthermore, predictive analytics within these systems allow airside operators to anticipate bottlenecks and reroute ground traffic dynamically. As airlines demand faster turnaround times to maintain profitability, airports are aggressively upgrading their airside information systems to extract every possible minute of efficiency from their existing infrastructure, thereby fueling the rapid expansion of this segment.

By Deployment Mode Insights

The on-premise segment captured the dominant share of the global market in 2025 and is likely to remain the leading market segment during the forecast period due to the requirement for air-gap security and strict data sovereignty regulations in critical aviation operations. According to the European Union General Data Protection Regulation and various national aviation security mandates, sensitive passenger data and critical operational flight information must often be stored and processed within the physical boundaries of the airport or the host country. On-premise systems provide airport authorities with complete physical control over their servers and data, ensuring compliance with these rigorous legal frameworks. Furthermore, the mission-critical nature of airport operations means that any reliance on external internet connections introduces risks of latency or downtime during cyberattacks or network outages. On-premise deployments guarantee that flight information display systems, baggage handling controls, and security databases remain fully operational even if the external internet connection is severed. This reliability and data security make on-premise solutions the default choice for major international hubs and military airports where operational continuity and national security are paramount. The high initial capital investment is justified by the long-term assurance of data sovereignty and uninterrupted service delivery.

On the other hand, the cloud and Software as a Service (SaaS) deployment segment is projected to be the fastest-growing and grow at a CAGR of 11.1% during the forecast period due to the urgent need for scalability and the reduction of capital expenditure. For instance, a majority of airports are actively increasing their investment in cloud computing to achieve greater operational agility and reduce the financial burden of maintaining physical data centers. Cloud-based airport information systems allow operators to instantly scale their computing resources up or down based on seasonal traffic fluctuations without purchasing additional physical hardware. This shift from a capital expenditure model to an operational expenditure model frees up financial resources that can be redirected toward passenger-facing innovations. Furthermore, cloud platforms provide automatic software updates and security patches, ensuring that airports always operate on the latest version of the software without the need for costly and disruptive manual upgrades. The ability to access operational data from anywhere in the world via secure web portals also enables remote management and centralized oversight for airport groups that manage multiple facilities. This combination of financial flexibility, operational agility, and reduced maintenance overhead is driving the rapid adoption of cloud and SaaS solutions across the global aviation industry.

REGIONAL ANALYSIS

North America Airport Information System Market Analysis

North America is expected to maintain its position as a major market for information systems, accounting for a significant share of global revenue, as aviation hubs continue to modernize their infrastructure over the next few years. According to the Federal Aviation Administration, modernization programs require massive upgrades to airport IT infrastructure to support advanced surveillance and data sharing. The primary driver in this region is the intense focus on enhancing passenger throughput and security efficiency at major congested hubs such as Atlanta, Chicago, and Los Angeles. Airports are heavily investing in integrated biometric screening systems and automated bag-drop technologies to reduce queue times and improve the overall traveler experience. Furthermore, strict cybersecurity mandates issued by transport security authorities compel airports to continuously upgrade their information systems to defend against sophisticated threats. The presence of leading global technology providers and a mature digital infrastructure ecosystem fosters rapid innovation and early adoption of cloud-based operational platforms. This combination of regulatory pressure, large passenger volumes, and advanced technological capabilities ensures that the United States remains a leader in the North American airport information system landscape.

Europe Airport Information System Market Analysis

Europe is projected to remain a key regional market, characterized by strict environmental regulations and an emphasis on seamless cross-border data integration, over the next few years. According to European Commission initiatives, the harmonization of air traffic management and airport operational data is a priority to reduce flight delays and carbon emissions. The market in Germany is heavily influenced by the need to integrate airport information systems with advanced rail networks, promoting seamless multimodal travel for passengers. Airports like Frankfurt and Munich are pioneering the use of artificial intelligence to optimize gate assignments and reduce aircraft taxiing times, thereby directly contributing to the region's sustainability goals. Furthermore, the stringent data privacy requirements of the General Data Protection Regulation drive the adoption of highly secure on-premise and private cloud architectures that protect passenger identity data. The strong emphasis on interoperability and cross-border data sharing among European airlines and ground handlers necessitates robust and standardized information platforms. This regulatory environment, combined with a commitment to sustainable aviation operations, ensures that Europe remains a major player in advanced airport information system deployments.

Asia Pacific Airport Information System Market Analysis

Asia Pacific is expected to be the fastest-growing market, driven by massive investments in infrastructure and the rapid adoption of smart technologies over the next few years. According to regional aviation authorities, initiatives mandating the construction of smart, safe, green, and humanistic aviation hubs are driving investments in digital infrastructure. The market in countries like China is characterized by the rapid deployment of fully integrated smart airport platforms that utilize 5G networks, artificial intelligence, and big data to manage every aspect of terminal operations. Major hubs have implemented end-to-end biometric processing and automated baggage handling systems that set new global standards for operational efficiency. Governments in the region are actively promoting the use of locally developed software and hardware solutions, stimulating the regional IT manufacturing sector. Furthermore, the explosive growth of the domestic middle class and the expansion of high-speed rail integration require highly sophisticated information systems to manage complex passenger flows. This scale of infrastructure development, combined with government support for digital innovation, ensures that the Asia Pacific region will continue to be a dominant force in the airport information system market.

Latin America Airport Information System Market Analysis

Latin America is likely to see steady growth in its airport information system market as privatization and digital transformation initiatives continue to gain momentum over the next few years. According to regional government aviation ministries, the concession of major international airports to private operators has included strict mandates for the modernization of passenger processing and operational IT systems. The market is primarily driven by the need to replace aging legacy systems with modern cloud-based platforms that can handle the increasing volume of international tourists and domestic travelers. Private operators are investing heavily in integrated resource management systems and mobile applications to improve the passenger experience and generate new non-aeronautical revenue streams. Furthermore, the geographic vastness of the region requires robust communication networks to connect remote regional airports with major central hubs, ensuring consistent operational visibility. The push to improve global aviation competitiveness rankings has accelerated the adoption of advanced security information systems and automated check-in technologies. Although the market faces economic challenges, the ongoing privatization trend and the urgent need for operational efficiency provide a strong foundation for the sustained growth of airport information systems in the region.

Middle East and Africa Airport Information System Market Analysis

The Middle East and Africa are projected to experience premium demand as regional aviation hubs continue to prioritize technological supremacy and ultra-modern infrastructure over the next few years. According to civil aviation authorities, the region is home to some of the busiest international airports in the world, requiring exceptionally advanced and resilient IT infrastructure. The market in this region is driven by the ambition to create fully autonomous and frictionless travel experiences utilizing cutting-edge technologies. Airports in the United Arab Emirates are pioneering the use of smart tunnels, biometric corridors, and artificial intelligence-driven predictive maintenance for all terminal systems. The extreme focus on luxury and premium passenger service necessitates highly personalized information systems that can anticipate passenger needs and provide bespoke navigation and retail offers. Furthermore, the region's status as a global transit hub requires seamless data integration with hundreds of international airlines, ensuring accurate real-time flight updates and efficient baggage transfer for connecting passengers. This relentless pursuit of technological excellence and operational perfection ensures that the region continues to drive premium demand for the most advanced airport information systems globally.

COMPETITIVE LANDSCAPE

The competition within the airport information system market is highly intense and characterized by the presence of several dominant global technology conglomerates alongside specialized regional software developers. These industry leaders continuously vie for supremacy by offering comprehensive integrated platforms that manage everything from flight scheduling to passenger processing. A major competitive differentiator is the ability to provide seamless interoperability between legacy infrastructure and modern cloud based solutions. Companies are aggressively investing in research and development to integrate advanced artificial intelligence and biometric capabilities into their core offerings. This technological race is further complicated by stringent regulatory requirements regarding data privacy and cybersecurity which force vendors to maintain rigorous compliance standards. Strategic alliances and joint ventures are frequently utilized to penetrate emerging markets and secure long term contracts with major international aviation hubs. Furthermore the shift toward software as a service models has intensified price competition as providers offer scalable subscription based pricing to attract cost conscious airport operators. Ultimately the market landscape remains dynamic with continuous innovation and strategic consolidation defining the battle for global dominance among top tier technology providers. These ongoing efforts ensure that only the most adaptable and technologically advanced firms will successfully capture future growth opportunities.

KEY MARKET PLAYERS

Some of the key players dominating the global airport information system market are

- SITA N.V.

- Amadeus IT Group, S.A.

- Honeywell International Inc.

- THALES Group

- Indra Sistemas, S.A.

- RTX Corporation

- Airport Information Systems

- IBM Corporation

- NEC Corporation

- Samsung Electronics Co., Ltd.

- T-Systems International GmbH

- Siemens AG

- VISION BOX – SOLUÇÕES DE VISÃO POR COMPUTADOR, S.A.

- Materna IPS GmbH

- Beumer Group

- INFORM Institut für Operations Research und Management GmbH

- ADB SAFEGATE

- Frequentis AG

- Damarel Systems International Ltd.

Top Players in the Market

- SITA is a premier global provider of information technology and telecommunications services for the air transport industry. The company contributes significantly to the global market by delivering comprehensive airport management solutions including passenger processing and flight operations systems. Recently SITA launched an advanced artificial intelligence driven platform to optimize terminal resource allocation and enhance passenger flow management. This strategic initiative allows airports to reduce operational bottlenecks and improve overall efficiency. By continuously integrating biometric technologies and cloud based architectures into their core offerings SITA strengthens its global footprint and ensures seamless digital transformation for aviation hubs worldwide delivering exceptional value.

- Amadeus IT Group stands as a leading technology company serving the global travel and aviation sector. The firm plays a crucial role in the market by providing robust airport operational databases and departure control systems that streamline daily airline and airport operations. To reinforce its competitive position Amadeus recently introduced a next generation cloud native passenger processing suite designed to accelerate check in and boarding procedures. This modernization effort enables aviation stakeholders to scale their operations effortlessly while delivering highly personalized traveler experiences. Through relentless innovation in software development Amadeus continues to empower airports with cutting edge digital infrastructure solutions.

- Collins Aerospace is a major global provider of integrated technology solutions for the aerospace and defense industries. Within the airport information system landscape the company delivers critical common use passenger processing systems and self service kiosk technologies. The company recently expanded its biometric integration capabilities by launching a new facial recognition platform that enables touchless passenger journeys from curb to gate. This deployment significantly enhances security protocols while simultaneously reducing wait times for travelers. By focusing on seamless hardware and software integration Collins Aerospace solidifies its reputation as a vital partner for modernizing airport terminal operations across the globe today.

Top Strategies Used by the Key Market Participants

Key participants in the airport information system market primarily focus on strategic partnerships and technological integrations to expand their global footprint. Companies are heavily investing in research and development to incorporate artificial intelligence and machine learning into their software platforms enabling predictive analytics for terminal operations. Furthermore market leaders are aggressively pursuing mergers and acquisitions to acquire specialized software firms that offer niche capabilities like biometric processing and advanced baggage tracking. Another major strategy involves transitioning clients from legacy on premise servers to scalable cloud based architectures which reduces maintenance costs and improves system agility. Finally vendors are prioritizing the development of open application programming interfaces to ensure seamless interoperability with third party aviation applications.

MARKET SEGMENTATION

This research report on the global airport information system market is segmented and sub-segmented into the following categories.

By Application

- Maintenance

- Ground Handling

- Finance and Operations

- Security

- Passenger Information

By System Area

- Airside Systems

- Flight Information Display Systems (FIDS)

- Airport Operations Database (AODB)

- Resource Management Systems (RMS)

- Air Traffic Management (ATM) Integration

- Terminal-Side Systems

- Departure Control Systems (DCS)

- Common-Use Passenger Processing (CUPPS/CUTE)

- Self-Service Kiosks and Digital Signage

By Deployment Mode

On-premise

Cloud/SaaS

By Airport Size

Class A

Class B

Class C

Class D

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Airport Information System Market?

The Airport Information System Market comprises software and hardware solutions that help airports manage operations, passenger services, flight information, baggage handling, security, and resource allocation efficiently.

2. What factors are driving the growth of the Airport Information System Market?

The market is driven by increasing air passenger traffic, airport modernization projects, digital transformation initiatives, smart airport development, and growing investments in automation technologies.

3. What are the major applications of airport information systems?

Airport information systems are widely used for maintenance, ground handling, finance and operations, security management, and passenger information services.

4. Which deployment modes are available for airport information systems?

Airport information systems are commonly deployed through on-premise infrastructure and cloud-based Software-as-a-Service (SaaS) platforms, depending on operational requirements.

5. What are the key components of an airport information system?

Key components include Flight Information Display Systems (FIDS), Airport Operations Databases (AODB), Resource Management Systems (RMS), Departure Control Systems (DCS), and Common-Use Passenger Processing Systems (CUPPS/CUTE).

6. How do airport information systems improve airport operations?

These systems streamline airport workflows by enabling real-time data sharing, efficient resource allocation, automated passenger processing, enhanced operational visibility, and better decision-making.

7. Which region dominates the Airport Information System Market?

North America holds a significant market share due to advanced airport infrastructure, early adoption of digital technologies, and continuous investments in smart airport solutions.

8. Which region is expected to witness the fastest growth?

The Asia-Pacific region is projected to experience the fastest growth because of expanding airport infrastructure, increasing air travel demand, and government investments in aviation modernization.

9. What challenges does the Airport Information System Market face?

Key challenges include high implementation costs, cybersecurity risks, integration with legacy airport systems, data privacy concerns, and compliance with aviation regulations.

10. What is the future outlook for the Airport Information System Market?

The market is expected to witness steady growth, supported by increasing adoption of artificial intelligence, IoT, cloud computing, biometric technologies, and smart airport initiatives aimed at improving operational efficiency and passenger experience.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com