Asia Pacific Coconut Milk Market Size, Share, Trends, & Growth Forecast Report – Segmented by Form (Liquid and Powder), Nature, Application, Distribution Channel, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2025 to 2033

Asia Pacific Coconut Milk Market Summary

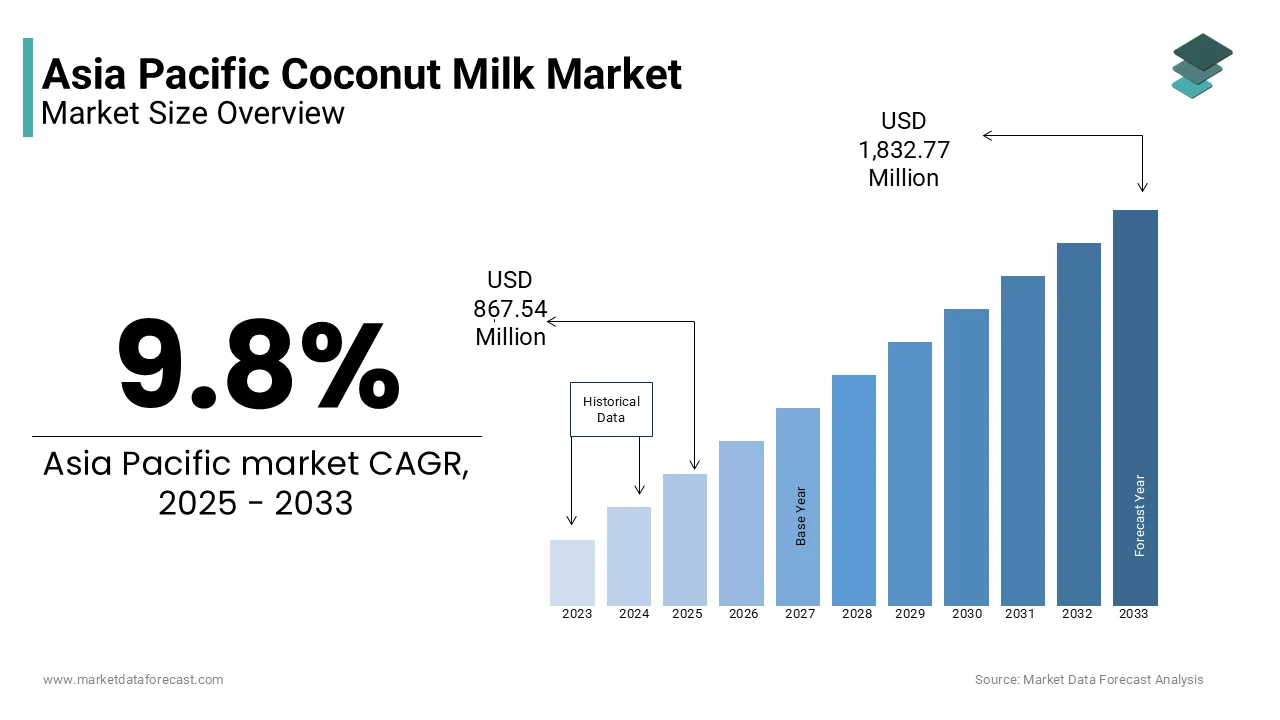

The Asia Pacific coconut milk market size was estimated at USD 790.11 million in 2024 and is projected to reach USD 1,832.77 million by 2033, growing at a CAGR of 9.8% from 2025 to 2033. The primary driver behind the growth of the Asia Pacific coconut milk market is the increasing adoption of plant-based diets and the preference for lactose-free alternatives among consumers.

Key Market Trends & Insights

Thailand coconut milk market was the largest by capturing 18.7% of the share in 2024

Indonesia was next by holding 12.4% of the Asia Pacific coconut milk market share in 2024

Based on form, the liquid form segment occupied the 52.3% of the Asia Pacific weight management market share in 2024

Based on nature, the conventional weight management market was the largest with prominent share in 2024.

Market Size & Forecast

2024 Market Size: USD 790.11 Million

2033 Projected Market Size: USD 1,832.77 Million

CAGR (2025-2033): 9.8%

Thailand: Largest market in 2024

Indonesia: Fastest growing market

Asia Pacific Coconut Milk Market Size

Asia Pacific coconut milk market size was valued at USD 790.11 million in 2024, and the market size is expected to reach USD 1,832.77 million by 2033 from USD 867.54 million in 2025. The market's promising CAGR for the predicted period is 9.8% during the forecast period.

Coconut milk is derived from the grated pulp of mature coconuts and is valued for its creamy texture and nutritional profile, including natural electrolytes, medium-chain triglycerides, and essential minerals. While the region remains the largest consumer and producer of coconut milk worldwide, its role extends beyond domestic use into export markets with rising demand in North America and Europe for plant-based dairy alternatives. Countries such as Thailand, Indonesia, and the Philippines are central to coconut cultivation and processing, collectively accounting for over 70% of global coconut production according to the Food and Agriculture Organization (FAO).

MARKET DRIVERS

Surge in Demand for Plant-Based Diets and Lactose-Free Alternatives

A primary driver behind the growth of the Asia Pacific coconut milk market is the increasing adoption of plant-based diets and the preference for lactose-free alternatives among consumers. Many individuals are turning to non-dairy substitutes like coconut milk with rising concerns about dairy-related allergies, digestive sensitivities, and environmental sustainability. According to the Asia Plant-Based Foods Association, per capita consumption of plant-based milk in the region grew by 18% between 2020 and 2023, with coconut milk being one of the most preferred choices due to its creamy consistency and neutral flavor profile. This trend is especially prominent in urban centers where consumer awareness about health and wellness is higher. In Japan, for example, retail sales of coconut milk-based beverages increased significantly following endorsements from nutritionists and influencers promoting their benefits for gut health and cholesterol management.

Expansion of Coconut Milk Use in Cosmetics and Personal Care

Another significant factor propelling the Asia Pacific coconut milk market is its growing application in the cosmetics and personal care industry. Coconut milk contains lauric acid, vitamins, and natural fats that make it an effective ingredient in skincare and haircare formulations.

In Thailand, local cosmetic brands have leveraged indigenous knowledge of coconut-based remedies to develop shampoos, lotions, and facial creams that appeal to both domestic and international consumers. Likewise, in South Korea, the K-beauty industry has incorporated fermented coconut milk into toners and masks to enhance skin hydration and microbiome balance. The presence of natural emollients and antimicrobial properties makes coconut milk a favored component in formulations targeting acne-prone or sensitive skin.

MARKET RESTRAINTS

Volatility in Coconut Yields Due to Climate Change and Farming Challenges

One of the primary restraints affecting the Asia Pacific coconut milk market is the fluctuating availability of raw coconuts due to climate change and agricultural challenges. Coconut trees require stable temperatures, consistent rainfall, and fertile soil for optimal yield, all of which have been disrupted by extreme weather events across major producing nations such as the Philippines, Indonesia, and India. According to the International Coconut Community, the average coconut yield in Southeast Asia declined by nearly 15% in 2023 due to prolonged droughts and erratic monsoons.

These disruptions have led to supply shortages, impacting both fresh coconut availability and industrial processing capacity. For instance, in the Philippines, which accounts for over 30% of global coconut production, government data showed a 20% drop in copra output in 2023 compared to the previous year, directly influencing coconut milk processors.

Additionally, aging coconut plantations and limited replanting efforts have contributed to lower productivity. Farmers face financial constraints in adopting modern irrigation systems and high-yield varieties, slowing the recovery of production levels.

Price Competition and Margin Pressure from Alternative Plant Milks

The Asia Pacific coconut milk market faces significant pressure from competing plant-based milk options such as almond, oat, soy, and rice milk, which offer similar nutritional benefits at potentially lower price points. According to Mintel’s 2023 Beverage Trends report, the average retail price of almond and oat milk was approximately 15–20% lower than that of coconut milk in major markets like Australia and Singapore, influencing consumer purchasing decisions.

Soy milk remains a dominant alternative due to its long-standing cultural acceptance across East and Southeast Asia. In China, for example, soy-based beverages continue to dominate supermarket shelves, which is limiting coconut milk’s penetration into mainstream consumer habits despite aggressive marketing by new entrants.

Furthermore, multinational dairy companies have entered the plant-based segment by launching hybrid or fortified versions of traditional milks, intensifying competition. As a result, coconut milk brands must continuously innovate in terms of formulation, packaging, and value proposition to justify premium pricing. The intense competitive landscape creates margin pressures and increases the need for strategic differentiation, posing a challenge for sustained market expansion.

MARKET OPPORTUNITIES

Increasing Demand for Ready-to-Drink (RTD) Coconut-Based Beverages

An emerging opportunity within the Asia Pacific coconut milk market is the rising popularity of ready-to-drink (RTD) coconut-based beverages, particularly among younger, on-the-go consumers. Urbanization and fast-paced lifestyles have led to a surge in demand for convenient, nutritious drinks that align with health-conscious trends. Brands are capitalizing on this trend by introducing flavored coconut shakes, protein-enriched coconut drinks, and blended nut-coconut beverages designed to appeal to fitness enthusiasts and health-focused consumers. In India, several startups have launched cold-pressed coconut milk mixes that can be diluted with water, offering convenience without compromising freshness. Moreover, manufacturers are leveraging digital marketing and social media to promote these beverages as natural energy boosters and post-workout refreshments. In Japan and South Korea, coconut-based sports drinks have found a niche audience among gym-goers and active millennials seeking hydrating alternatives without artificial additives.

Integration of Coconut Milk in Functional and Medicated Skincare Products

The integration of coconut milk into functional and medicated skincare products presents a lucrative opportunity for the Asia Pacific coconut milk market. As the global skincare industry shifts toward natural, bioactive ingredients, coconut milk has gained attention for its anti-inflammatory, antimicrobial, and moisturizing properties. According to a 2023 study published in the International Journal of Cosmetic Science, lauric acid, a key component of coconut milk, demonstrated strong efficacy in treating acne and strengthening the skin barrier. This scientific validation has encouraged cosmetic laboratories and dermatological brands to incorporate coconut milk extracts into therapeutic formulations targeting eczema, psoriasis, and dry skin conditions. In Thailand, local beauty brands have introduced coconut-based ointments and healing balms endorsed by dermatologists, gaining traction among consumers seeking gentle yet effective treatments.

MARKET CHALLENGES

Limited Awareness and Consumer Education in Emerging Markets

Despite its historical significance in tropical cuisines, the Asia Pacific coconut milk market faces a notable challenge stemming from limited awareness and consumer education regarding its nutritional and functional benefits in less developed regions. While coconut milk enjoys widespread recognition in countries like Thailand, Indonesia, and the Philippines, its adoption in parts of Central and South Asia remains constrained due to unfamiliarity and misconceptions around saturated fat content.

According to a 2023 consumer perception survey conducted by Euromonitor International across rural markets in India and Bangladesh, nearly 40% of respondents associated coconut milk primarily with high-fat content rather than its potential health benefits, such as supporting heart health when consumed in moderation. Additionally, confusion between refined coconut oil and natural coconut milk has led to hesitancy in certain consumer groups.

Infrastructure Limitations in Coconut Processing and Distribution

A critical challenge facing the Asia Pacific coconut milk market is the lack of modern infrastructure for efficient processing, storage, and distribution of coconut milk products. Many coconut-producing regions still rely on small-scale, traditional extraction methods that result in inconsistency in quality, shelf life, and scalability. According to the International Fund for Agricultural Development (IFAD), only 30% of coconut processing units in the Philippines and Indonesia meet contemporary hygiene and preservation standards, leading to high spoilage rates and reduced marketability. Moreover, the perishable nature of fresh coconut milk necessitates cold chain logistics, which are not widely available in rural and remote areas. In India’s coastal states, where coconut farming is prevalent, inadequate refrigeration facilities contribute to post-harvest losses exceeding 20%, as reported by the Indian Council of Agricultural Research in 2023.

Limited access to advanced packaging technologies also hampers the ability of local manufacturers to extend product longevity and enter export markets. Without investment in mechanized processing plants, temperature-controlled transportation, and innovative packaging formats, the regional coconut milk market struggles to meet the demands of both domestic and international buyers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.8% |

| Segments Covered | By Form, Nature, Application, Distribution Channel, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | WhiteWave Foods, McCormick, Theppadungporn Coconut Co. Ltd., Goya Foods, Pureharvest, Edward & Sons, Ducoco, iTi Tropicals, Thai Agri Foods, Turtle Mountain, Pacific Foods, and others |

SEGMENTAL ANALYSIS

By Form Insights

The liquid form segment occupied the 52.3% of the Asia Pacific weight management market share in 2024 with the increasing consumer preference for ready-to-consume (RTC) products that offer convenience without compromising on nutritional value. Liquid-based meal replacements, protein shakes, and slimming beverages are increasingly being integrated into daily diets due to their ease of consumption and rapid absorption. Additionally, the rise of fitness culture and increased awareness around nutrition has led to greater demand for fortified liquids containing essential vitamins, dietary fiber, and plant-based proteins.

The powder segment is likely to expand with an anticipated CAGR of 14.7% from 2025 to 2033. This accelerated growth is largely attributed to the versatility, longer shelf life, and cost-effectiveness associated with powdered formulations such as protein powders, meal replacement blends, and weight loss shakes.

One key driver is the rising popularity of home-prepared health drinks and smoothies, particularly among fitness enthusiasts and working professionals seeking personalized nutrition solutions. According to Euromonitor International, the sale of weight management powder mixes in India saw a year-on-year increase of 22% in 2023, driven by influencer-backed campaigns promoting DIY wellness routines.

By Nature Insights

The conventional weight management market was the largest with prominent share in 2024. Conventional weight management products, including mass-market protein bars, meal replacement shakes, and appetite suppressants, continue to be the preferred choice for budget-conscious consumers across developing economies like India, Indonesia, and the Philippines. Furthermore, pharmaceutical-grade weight loss drugs and synthetic supplements remain under the conventional umbrella and are widely prescribed in countries like Japan and South Korea, where medicalized weight management is gaining traction.

The organic weight management segment is swiftly emerging with a CAGR of 19.4% from 2025 to 2033. A defining factor behind this growth is the heightened awareness regarding the potential health risks associated with artificial additives, preservatives, and synthetic sweeteners commonly found in conventional weight loss products. Simultaneously, regulatory bodies across the region have introduced stricter labeling norms and certification frameworks that enhance consumer confidence in organic claims. In India, the Food Safety and Standards Authority of India (FSSAI) revised its organic standards in mid-2023 by enabling more domestic brands to enter this rapidly expanding category.

By Application Insights

The food and beverage application segment was accounted in holding 48.6% of the Asia Pacific weight management market share in 2024. Urbanization and fast-paced lifestyles have significantly influenced dietary habits, prompting individuals to seek convenient yet nutritious options that support weight control. According to Euromonitor International, sales of weight-focused snack bars and shakes in India rose by 16% year-on-year in 2023, reflecting a growing inclination toward on-the-go healthy eating. Supported by regulatory incentives encouraging healthier formulations and heightened marketing efforts by major FMCG companies, the food and beverage application segment remains central to the ongoing evolution of the Asia Pacific weight management industry.

The personal care application segment is likely to register a CAGR of 16.9% in the next coming years. This growth is attributed to the rising integration of body-shaping, cellulite-reducing, and skin-firming ingredients into topical cosmetics and skincare products marketed for weight and body contour management. An emerging trend is the use of slimming creams, body wraps, and massage oils infused with caffeine, green tea extract, and algae-based compounds designed to stimulate fat breakdown and improve circulation. Moreover, beauty tech startups and K-beauty brands have been instrumental in driving this segment forward through influencer endorsements and social media-driven campaigns. In South Korea, several cosmetic companies launched bioelectric-emitting body lotions aimed at accelerating fat metabolism, gaining significant traction among young consumers.

By Distribution Channel Insights

Supermarkets held 39.8% of the Asia Pacific weight management market share in 2024 with the wide range of branded and private-label weight management products available in these stores by offering consumers choice, credibility, and convenience under one roof. Major supermarket chains across the region, including Woolworths in Australia, AEON in Japan, and Big Bazaar in India, have dedicated sections for health and wellness products, featuring items such as protein bars, low-calorie cereals, and fortified beverages. Moreover, promotional strategies such as bundled offers, loyalty programs, and in-store sampling have enhanced consumer engagement and trial rates. In Singapore, Cold Storage and Giant supermarkets reported a 19% increase in sales of imported organic weight management products during festive seasons, reflecting strong consumer trust in quality-assured retail environments.

The specialist retailers segment is likely to register a CAGR of 18.1% from 2025 to 2033. These niche outlets, including health food stores, nutraceutical boutiques, and fitness-focused retail chains, have capitalized on the increasing demand for curated, expert-curated product selections tailored to individual health goals. A key driver behind this growth is the rising consumer preference for personalized recommendations and higher-quality products that may not be readily available in mass-market retail settings. In addition, specialist retailers often carry premium, organic, and functional formulations that align with evolving consumer preferences. In Japan, chain stores like Natural Healthy House and Welcia Pharmacy expanded their weight management product lines by 20% in 2023, incorporating imported probiotic-rich shakes and plant-based protein powders.

REGIONAL ANALYSIS

Thailand coconut milk market was the largest by capturing 18.7% of the share in 2024 due to its extensive coconut cultivation base, advanced processing infrastructure, and established export networks that supply both raw materials and finished products to global markets.

Thai coconut milk exports reached USD 1.2 billion in 2023, with the U.S., EU, and Middle Eastern countries serving as primary destinations. According to the Thai Department of Agricultural Extension, the country produced over 2.8 million metric tons of coconuts in 2023, with nearly 40% processed into coconut milk and related derivatives. Major domestic players such as Chaokoh, Amira Nature Foods, and Thai Agri-Food Corporation have leveraged mechanized extraction techniques and innovative packaging formats to meet international quality standards.

Indonesia was next by holding 12.4% of the Asia Pacific coconut milk market share in 2024 with a combination of robust production volumes and growing domestic demand. As one of the world’s top three coconut producers, Indonesia contributes nearly 17% of global output, according to the Food and Agriculture Organization (FAO). Domestic utilization of coconut milk has expanded significantly in recent years in household cooking, beverage manufacturing, and personal care products. In 2023, local sales of coconut milk-based beverages increased by 12%, supported by rising health consciousness and product diversification. Moreover, Indonesia has invested in enhancing its industrial processing capabilities. Indonesia is well-positioned to strengthen its influence within the regional coconut milk market while addressing challenges related to climate resilience and smallholder productivity with increasing government focus on agro-industrial development and export diversification.

The Philippines coconut milk market growth is esteemed to grow steadily with its status as a key player through a strategic emphasis on value-added coconut milk exports rather than bulk raw material shipments. The country’s Coconut Development Program has encouraged processors to adopt aseptic packaging, extended shelf-life technologies, and organic certifications to cater to premium international markets. Companies like Pure Harvest and Malayan Marketing Corp have expanded their product ranges to include flavored coconut beverages, ready-to-drink mixes, and infant-nutrition blends.

India coconut milk market is likely to have prominent growth opportunities in the next coming years with the strong traditional usage in Southern and coastal regions. According to the Indian Council of Agricultural Research, the country produced over 23 billion coconuts in 2023, with Kerala, Tamil Nadu, and Karnataka dominating cultivation. Brands like Parle Agro and Hector Beverages have introduced chilled and ambient-pack coconut milk beverages, targeting health-conscious consumers and expanding reach beyond traditional demographics. Moreover, the Ayurveda and wellness sectors have contributed to the incorporation of coconut milk in herbal tonics and immunity-boosting formulations.

Vietnam coconut milk market growth is anticipated to grow with increasing export activity and rising domestic consumption. According to Vietnam’s Ministry of Agriculture and Rural Development, coconut production in the Mekong Delta reached 1.4 million metric tons in 2023, with over 30% allocated for processing into coconut milk and related products. Vietnam has emerged as a reliable supplier to North America and Europe, particularly for organic and preservative-free coconut milk variants. Vietnamese exporters have benefited from trade agreements such as EVFTA and CPTPP, which have reduced import tariffs and facilitated easier access to premium markets.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

WhiteWave Foods, McCormick, Theppadungporn Coconut Co. Ltd., Goya Foods, Pureharvest, Edward & Sons, Ducoco, iTi Tropicals, Thai Agri Foods, Turtle Mountain, and Pacific Foods are playing dominating role in the Asia Pacific coconut milk market.

The Asia Pacific coconut milk market features a highly competitive landscape characterized by the coexistence of multinational corporations, regional powerhouses, and local artisanal producers. While large-scale processors leverage economies of scale and extensive distribution networks to dominate export markets, smaller domestic brands capitalize on authentic formulations and cultural relevance to retain consumer loyalty. The competition extends beyond pricing and availability to include product differentiation, branding, and alignment with emerging lifestyle trends such as plant-based diets, wellness-focused consumption, and eco-friendly packaging. Manufacturers are increasingly investing in research and development to create innovative formats like fortified beverages, fermented coconut milk, and functional blends tailored for specific health benefits. At the same time, sustainability has become a central battleground, with companies striving to showcase responsible sourcing, minimal environmental impact, and support for smallholder farmers.

TOP PLAYERS IN THE MARKET

Thai Agri-Food Corporation

Thai Agri-Food Corporation is a leading player in the Asia Pacific coconut milk market, known for its commitment to quality and large-scale production capabilities. The company has built a strong reputation by supplying premium coconut milk products to domestic and international markets. It plays a strategic role in sourcing, processing, and exporting value-added coconut derivatives.

Chaokoh (CP Alliance Corporation)

Chaokoh is one of the most recognized names in the coconut milk industry, especially across Southeast Asia and global export markets. Known for its iconic canned coconut milk, the brand has consistently delivered consistency and reliability in taste and texture. Chaokoh has expanded into new formats such as chilled and ready-to-drink options. Its deep-rooted expertise and long-standing distribution networks have made it a trusted staple in kitchens worldwide, contributing significantly to the global coconut milk supply chain.

Amira Nature Foods Ltd.

Amira Nature Foods is a key exporter of packaged coconut milk, particularly to North America, Europe, and the Middle East. The company differentiates itself through product diversification, including organic and preservative-free variants. Amira emphasizes traceability, clean labeling, and modern packaging solutions to cater to health-conscious consumers. Its ability to align with evolving dietary trends and maintain high-quality standards has reinforced its influence in both regional and international coconut milk markets.

TOP STRATEGIES USED BY KEY PLAYERS

One major strategy deployed by leading players in the Asia Pacific coconut milk market is product innovation and diversification , where companies continuously introduce new formats such as chilled beverages, functional drinks, and organic variants to meet shifting consumer preferences and expand usage beyond traditional cooking applications.

Another key approach is expanding export capabilities and strengthening global distribution networks , allowing manufacturers to increase their reach in Western markets where plant-based nutrition is gaining traction, supported by compliance with international food safety and sustainability certifications.

A third critical strategy involves investing in sustainable sourcing and ethical practices , ensuring transparent supply chains from farm to shelf, which appeals to environmentally conscious consumers and aligns with global regulatory expectations while securing long-term raw material availability.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Thai Agri-Food Corporation launched a new line of organic-certified coconut milk products aimed at premium retail markets in Australia and Japan by enhancing its foothold in the health-conscious consumer segment.

- In August 2023, Chaokoh partnered with a leading foodservice distributor in South Korea to expand its presence in cafes and restaurants offering coconut-based beverages and desserts, tapping into the growing trend of fusion cuisine.

- In January 2024, Amira Nature Foods introduced a range of ambient-packed coconut milk beverages in the Middle East, targeting expatriate communities and expanding its cross-border sales footprint.

- In October 2024, San Miguel Pure Foods entered the coconut milk sector by launching a locally sourced and bottled coconut drink in the Philippines, leveraging its strong domestic brand equity in food and beverages.

- In May 2023, Nutraceutical International collaborated with Vietnamese coconut suppliers to develop a line of coconut milk-based protein shakes, aiming to capture demand from fitness enthusiasts in North America and Europe.

MARKET SEGMENTATION

This research report on the Asia Pacific coconut milk market has been segmented and sub-segmented based on the following categories.

By Form

- Liquid

- Powder

By Nature

- Organic

- Conventional

By Application

- Household

- Food and beverage

- Cosmetics

- Personal care

By Distribution Channel

- Supermarkets

- Hypermarkets

- Specialist retailers

- Convenience stores

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

What are the key factors driving the growth of the coconut milk market in Asia Pacific?

Key drivers include rising health awareness, the growing vegan population, increased lactose intolerance, and the demand for natural and organic food products.

What are the major applications of coconut milk in the food and beverage industry in Asia Pacific?

Coconut milk is widely used in beverages, desserts, curries, soups, sauces, and baked goods. It is also a key ingredient in vegan dairy alternatives, including coconut milk-based yogurt and ice cream.

What are the challenges facing the coconut milk market in Asia Pacific?

Key challenges include fluctuations in coconut prices due to climate change, high production costs, and competition from other plant-based alternatives like almond and soy milk.

What are the packaging trends for coconut milk products in the Asia Pacific region?

Sustainable and eco-friendly packaging options, including tetra packs, aluminum cans, and glass bottles, are becoming increasingly popular as companies strive to reduce their environmental footprint.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com