Asia Pacific Vascular Graft Market Size, Share, Trends & Growth Forecast Report By Indication (Endovascular Aneurysm Repair [Abdominal & Thoracic], Peripheral Vascular, Hemodialysis Access), By Raw Material (Polyester, ePTFE, Polyurethane, Biosynthetic), By End User (Hospitals, Ambulatory Surgical Centers), and Country (India, China, Japan, South Korea, Australia, Rest of APAC) – Industry Analysis From 2025 to 2033.

Asia Pacific Vascular Graft Market Size

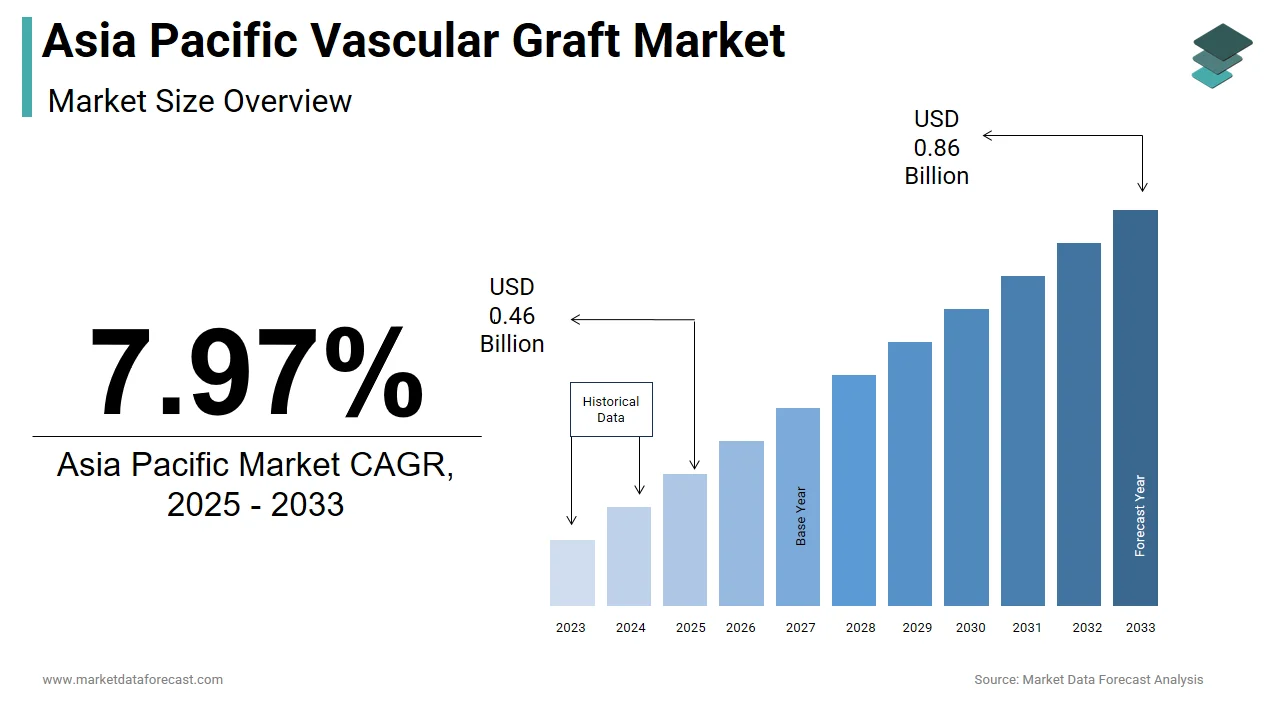

The size of the Asia Pacific vascular graft market was worth USD 0.43 billion in 2024. The Asia Pacific market is anticipated to grow at a CAGR of 7.97% from 2025 to 2033 and be worth USD 0.86 billion by 2033 from USD 0.46 billion in 2025.

The Asia Pacific vascular graft market includes a range of synthetic and biological conduits used to replace or bypass damaged blood vessels in patients suffering from peripheral artery disease (PAD), aortic aneurysms, and other cardiovascular conditions. These grafts are primarily made from materials such as polytetrafluoroethylene (PTFE), polyester (Dacron), or autologous veins and arteries, each selected based on the patient’s condition and anatomical requirements. As cardiovascular diseases continue to rise across the region, vascular grafts have become essential components of surgical interventions aimed at restoring blood flow and preventing limb amputation or life-threatening complications.

MARKET DRIVERS

Rising Prevalence of Peripheral Arterial Disease and Diabetic Complications

One of the primary drivers of the Asia Pacific vascular graft market is the increasing incidence of peripheral arterial disease (PAD) and related diabetic complications that necessitate surgical intervention. PAD, characterized by narrowed or blocked arteries in the limbs, often leads to critical limb ischemia, gangrene, and amputations if left untreated. According to the International Diabetes Federation (IDF), Asia accounts for over 60% of the global diabetic population, with countries like India, China, and Thailand experiencing rapid growth in diabetes-related vascular complications. This surge in diabetic foot ulcers and lower extremity infections has led to a higher number of revascularization procedures where vascular grafts are employed to restore circulation. In India alone, the Indian Journal of Endocrinology and Metabolism reports that nearly 25% of diabetic patients develop foot ulcers during their lifetime, many of which require surgical intervention. Moreover, with expanding access to tertiary care hospitals and government initiatives promoting early diagnosis and treatment, more patients are undergoing bypass surgeries using vascular grafts.

Expansion of Healthcare Infrastructure and Access to Advanced Surgical Facilities

Another significant driver of the Asia Pacific vascular graft market is the rapid modernization of healthcare infrastructure, particularly in emerging economies such as India, Indonesia, and Vietnam, where investment in hospitals, surgical centers, and medical device supply chains is accelerating. Governments in these countries have launched initiatives to improve surgical capacity and equip regional hospitals with advanced operating theaters capable of performing complex vascular procedures. For example, India's National Health Mission (NHM) has funded the establishment of cardiothoracic surgery units in district hospitals, allowing rural populations to access vascular interventions previously available only in metropolitan cities. In addition, private hospital chains such as Apollo Hospitals and Fortis Healthcare are investing in dedicated vascular clinics and hybrid operating rooms, enhancing procedural efficiency and patient outcomes. The combination of improved surgical access, trained vascular surgeons, and enhanced reimbursement policies is driving widespread adoption of vascular graft technologies across the Asia Pacific region.

MARKET RESTRAINTS

High Cost of Vascular Graft Procedures and Limited Reimbursement Coverage

A key restraint affecting the Asia Pacific vascular graft market is the high cost associated with vascular graft implantation procedures, which remains a barrier to widespread accessibility, especially in low- and middle-income countries. Vascular graft surgeries involve not only the cost of the graft material but also preoperative diagnostics, surgical fees, postoperative care, and potential revision procedures, making them financially burdensome for many patients. This financial burden discourages patients from seeking timely surgical interventions, leading to delayed treatments and worsening clinical outcomes. A study published by the Indian Heart Journal found that the average cost of a lower limb bypass surgery exceeds USD 8,000 in India, which is beyond the reach of a large portion of the population without insurance coverage. Furthermore, limited reimbursement policies in public and private health insurance schemes restrict access to vascular graft procedures. In China, despite the presence of basic insurance coverage, out-of-pocket expenditures remain high due to exclusions on certain types of grafts and limited coverage for postoperative complications.

Shortage of Trained Vascular Surgeons and Specialized Medical Centers

Another major constraint in the Asia Pacific vascular graft market is the scarcity of trained vascular surgeons and the uneven distribution of specialized vascular care centers, particularly in rural and semi-urban areas. Unlike cardiology or general surgery, vascular surgery remains a relatively niche specialty in many parts of the region, limiting the availability of skilled professionals who can perform complex grafting procedures. According to the Asian Society for Vascular Surgery, many countries in Southeast Asia have fewer than one vascular surgeon per million population, compared to developed nations where the ratio is significantly higher. This lack of expertise translates into reduced procedural volumes and delays in treatment, particularly in regions where alternative amputation rates remain high due to the unavailability of bypass services.

MARKET OPPORTUNITIES

Growth of Minimally Invasive Vascular Interventions and Hybrid Operating Rooms

A significant opportunity emerging in the Asia Pacific vascular graft market is the increasing adoption of minimally invasive endovascular techniques combined with traditional open surgical approaches in hybrid operating rooms. These hybrid procedures, which integrate catheter-based interventions with surgical graft placements, offer improved patient outcomes, shorter recovery times, and reduced hospital stays. Countries such as Japan, South Korea, and Australia have invested heavily in upgrading their surgical infrastructure with real-time imaging capabilities, enabling precise placement of stent grafts alongside conventional bypass grafts. Moreover, manufacturers are responding to this trend by developing next-generation vascular grafts compatible with endovascular delivery systems. Companies like Terumo and B. Braun are introducing tapered and fenestrated grafts designed for complex aortic repairs, aligning with the shift toward personalized and less invasive treatment strategies.

Expansion of Telemedicine and Remote Patient Monitoring for Post-Surgical Care

The integration of telemedicine and digital health platforms into post-surgical vascular care presents a promising avenue for growth in the Asia Pacific vascular graft market. With vast geographical disparities and limited follow-up access in rural areas, remote monitoring tools are becoming essential for ensuring long-term graft patency and patient compliance with rehabilitation protocols. Digital platforms now enable clinicians to monitor wound healing, detect early signs of graft failure, and manage anticoagulation therapy remotely through wearable sensors and mobile apps. In addition, governments and private healthcare providers are investing in cloud-based patient registries and AI-driven analytics to track vascular graft performance and optimize clinical decision-making.

MARKET CHALLENGES

Risk of Graft Failure and Long-Term Complications

One of the foremost challenges in the Asia Pacific vascular graft market is the persistent risk of graft failure, infection, and thrombosis following implantation, which affects long-term patient outcomes and increases the need for revision surgeries. Despite advancements in biomaterial engineering and surgical techniques, synthetic grafts, particularly those made from PTFE or Dacron, are prone to occlusion and infection, especially in patients with compromised immune function or poor circulation. According to the Journal of Vascular Surgery, primary patency rates for infrainguinal bypass grafts fall below 50% within two years, highlighting the limitations of current graft technologies. Infection rates after vascular graft implantation can range from 2% to 5%, as reported by the Asian Journal of Surgery, leading to severe complications such as sepsis and graft explantation. These risks not only impact patient prognosis but also create economic burdens due to repeated hospitalizations and additional surgical interventions.

Regulatory Hurdles and Delayed Approvals for New Graft Technologies

Another pressing challenge in the Asia Pacific vascular graft market is the lengthy and inconsistent regulatory approval processes across different countries, which delay the commercialization of novel graft technologies. In countries like Malaysia and the Philippines, overlapping responsibilities between health ministries and national regulatory agencies further complicate the process. This fragmentation discourages multinational companies from launching cutting-edge graft solutions in smaller markets, limiting patient access to advanced treatments. Unless regulatory harmonization efforts accelerate across the region, delays in approvals will continue to constrain innovation and market expansion in the vascular graft sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Indication, Raw Material, End-user, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Endologix Inc., LeMaitre Vascular, Inc., MAQUET Holding B.V.B. Braun Melsungen AG, & Co. KG, Medtronic plc, C. R. Bard, Inc., Cardinal Health Inc., Cook Medical Inc., Terumo Corporation, and W. L. Gore & Associates, Inc. |

SEGMENTAL ANALYSIS

By Indication Insights

The abdominal aneurysm repair segment dominated the Asia Pacific vascular graft market by accounting for 36.4% of total revenue in 2024. This dominance is primarily attributed to the high prevalence of abdominal aortic aneurysms (AAAs), which pose significant health risks if left untreated. One key driver behind this segment’s leadership is the rising incidence of AAA among aging populations in countries like Japan, China, and Australia, where lifestyle-related cardiovascular diseases are increasingly prevalent. According to the World Health Organization (WHO), cardiovascular diseases account for over 30% of all deaths in the Asia Pacific region, with a significant proportion linked to aortic pathologies. The widespread adoption of endovascular aneurysm repair (EVAR) procedures in urban centers has further expanded the use of specialized stent grafts for treating AAAs.

The peripheral vascular repair segment is projected to be the fastest-growing indication in the Asia Pacific vascular graft market, expected to expand at a CAGR of 9.7% between 2025 and 2033. This rapid ascent is driven by the escalating burden of peripheral artery disease (PAD), particularly among diabetic and elderly populations. A major growth catalyst is the surge in diabetes-related lower limb complications across South and Southeast Asia, where poor circulation often leads to critical limb ischemia and gangrene. According to the International Diabetes Federation (IDF), Asia accounts for more than half of the world’s diabetic population, with India alone reporting over 77 million cases in 2023. As per the Indian Journal of Endocrinology and Metabolism, a significant share of diabetic patients develop foot ulcers during their lifetime , many of whom require vascular graft-based revascularization to prevent amputation. Furthermore, improved access to vascular surgery services in emerging economies such as Indonesia, Vietnam, and the Philippines is contributing to increased procedural volumes. Public health initiatives promoting early diagnosis and intervention are also playing a role in expanding treatment coverage.

By Raw Material Insights

The polyester-based vascular grafts hold the largest share of the Asia Pacific vascular graft market by capturing 42.8% of total revenue in 2024. This influence is largely due to polyester’s long-standing use in vascular surgery, especially for aortic and infrainguinal bypass procedures, owing to its durability, mechanical strength, and proven clinical track record. One of the primary reasons for polyester’s widespread adoption is its compatibility with both open surgical and endovascular approaches, allowing for versatile application in treating a variety of vascular pathologies. In addition, in Japan, where hybrid vascular procedures are gaining traction, polyester remains the preferred material for thoracic and abdominal aneurysm repairs due to its superior suture retention and low risk of degradation. Moreover, polyester grafts have been extensively studied and validated through decades of clinical data, reinforcing physician confidence in their long-term performance.

ePTFE is emerging as the fastest-growing raw material in the Asia Pacific vascular graft market, projected to grow at a CAGR of 10.1%. This rapid expansion is driven by increasing applications in peripheral vascular repair, dialysis access, and small-diameter grafting, where traditional materials face limitations. A key growth enabler is the material’s exceptional flexibility, non-thrombogenic properties, and ease of handling during complex surgical procedures, making it ideal for below-the-knee bypasses and arteriovenous fistulas. Also, advancements in surface modification technologies, such as heparin coating and microporous designs, have enhanced ePTFE graft patency and reduced infection risks, addressing historical concerns regarding long-term performance. As per the Indian Journal of Surgery, ePTFE graft usage in hemodialysis access procedures has grown in recent years , reflecting broader adoption trends.

By End-User Insights

Hospitals represented the largest end-user segment in the Asia Pacific vascular graft market by accounting for a substantial share of total revenue in 2024. This is because of the fact that vascular graft implantation procedures are highly specialized and require advanced surgical infrastructure, multidisciplinary teams, and post-operative intensive care units—resources typically concentrated in hospital settings. A core growth factor is the concentration of vascular surgeries in tertiary care hospitals, particularly in metropolitan cities across Japan, South Korea, and Australia, where hybrid operating rooms equipped with real-time imaging facilitate both open and endovascular procedures. Also, government investments in cardiothoracic and vascular surgery departments within regional medical centers have expanded access to vascular graft procedures beyond urban hubs, particularly in India and Indonesia.

Ambulatory Surgery Centers (ASCs) are the quickest expanding end-user segment in the Asia Pacific vascular graft market, expected to expand at a CAGR of 9.3%. This growth is fueled by the increasing shift toward outpatient vascular procedures, particularly in minimally invasive interventions such as dialysis access creation and superficial vein bypasses. One of the key drivers is the cost-effectiveness and convenience offered by ASCs compared to traditional hospital settings, attracting both patients and physicians seeking efficient healthcare delivery models. Moreover, technological advancements in vascular graft design and preoperative planning tools have enabled shorter operative times and quicker recovery, making ASCs viable for select procedures. In Japan, the Ministry of Health, Labour and Welfare has approved certain vascular interventions for day-care surgery under strict guidelines, encouraging ASC adoption.

COUNTRY LEVEL ANALYSIS

Japan held the largest share of the Asia Pacific vascular graft market, contributing approximately 28% of total regional revenue in 2024. The country’s progress is underpinned by its aging population, well-developed healthcare infrastructure, and high prevalence of cardiovascular diseases. A key growth driver is Japan’s rapidly aging demographic, with a major share of the population aged 65 years or older, as per the National Institute of Population and Social Security Research. This demographic shift has led to a surge in age-related vascular conditions such as abdominal aortic aneurysms and peripheral artery disease. Also, Japan has one of the most advanced healthcare systems in the region, with widespread availability of hybrid operating theaters and skilled vascular surgeons, enabling high procedural volumes.

China has a strong presence and is driven by rising cardiovascular disease prevalence, government-backed healthcare modernization efforts, and growing urbanization. A major growth engine is the increasing burden of lifestyle-related diseases such as hypertension, diabetes, and obesity, which contribute to vascular deterioration. This rising disease burden has led to a corresponding increase in vascular interventions requiring graft implantation. Simultaneously, the Chinese government has prioritized improving access to advanced surgical care through national health programs and hospital upgrades, particularly in Tier II and Tier III cities. Also, domestic manufacturers such as MicroPort Scientific and Lepu Medical are investing in the local production of vascular grafts, reducing import dependency and lowering costs.

India is positioning itself as a rapidly growing player in the region. The country’s growth is being driven by expanding healthcare infrastructure, rising awareness about vascular diseases, and increasing government and private sector investments in cardiothoracic surgery. A core growth factor is the surge in diabetes-related peripheral vascular complications, many of whom are at risk of developing critical limb ischemia. Moreover, India's National Health Mission (NHM) has funded the establishment of vascular surgery units in district hospitals, expanding access beyond metropolitan areas. Private hospital chains such as Apollo Hospitals and Fortis Healthcare are also investing heavily in dedicated vascular clinics and hybrid operating rooms.

Australia represents a smaller but high-value segment characterized by advanced surgical practices, robust reimbursement mechanisms, and stringent quality controls. A key growth driver is Australia’s well-established healthcare system, which ensures broad access to vascular surgery services across both public and private hospitals, even in regional areas. Additionally, Australia maintains one of the highest per capita rates of endovascular procedures in the region, supported by favorable Medicare coverage for aneurysm repairs and limb salvage surgeries. The country is also a hub for clinical trials and product development, with institutions like Monash University and Royal Melbourne Hospital collaborating with global manufacturers on next-generation graft technologies.

South Korea is positioning itself as a technologically advanced market driven by high healthcare expenditure and early adoption of minimally invasive vascular procedures. A major growth factor is the country’s integration of digital health technologies into vascular surgery, including robotic-assisted procedures and AI-driven preoperative planning tools. Moreover, South Korea’s universal health insurance system provides substantial coverage for vascular procedures, ensuring timely access for patients and encouraging higher treatment rates.

KEY MARKET PLAYERS

Endologix Inc., LeMaitre Vascular, Inc., MAQUET Holding B.V.B. Braun Melsungen AG, & Co. KG, Medtronic plc, C. R. Bard, Inc., Cardinal Health Inc., Cook Medical Inc., Terumo Corporation, and W. L. Gore & Associates, Inc. are the key players in the Asia Pacific vascular graft market.

TOP LEADING PLAYERS IN THE MARKET

Terumo Corporation

Terumo is a leading global manufacturer of vascular grafts and interventional devices, with a strong foothold in the Asia Pacific market. The company has been at the forefront of developing biocompatible and durable graft solutions tailored for both open surgical and endovascular applications. In the Asia Pacific region, Terumo supports a wide range of vascular procedures through localized product development, strategic distribution partnerships, and collaborations with research institutions to enhance graft performance.

Braun Melsungen AG

Braun is a key player in the Asia Pacific vascular graft market, offering a diverse portfolio of synthetic and bioengineered grafts. Known for its high-quality manufacturing standards and long-term clinical reliability, the company has expanded its presence by aligning with regional hospitals and surgical centers. It also invests in physician education programs and integrated procedural kits that streamline graft deployment, making it a preferred supplier among vascular surgeons across Japan, China, and India.

Getinge AB

Getinge plays a significant role in the vascular graft ecosystem through its advanced surgical systems, perfusion technologies, and support services for complex revascularization procedures. While primarily known for critical care equipment, the company’s integration of vascular graft-compatible surgical tools and perioperative monitoring systems has strengthened its relevance in the Asia Pacific market. Getinge collaborates closely with public healthcare providers to improve outcomes in high-risk vascular interventions, contributing to improved patient survival rates and procedural efficiency.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Localization of Product Offerings and Manufacturing Facilities

Major players are tailoring their vascular graft portfolios to suit regional anatomical variances, disease prevalence, and surgical practices. Companies are also establishing or expanding local production units and logistics networks to reduce lead times and ensure better supply chain responsiveness.

Collaboration with Academic and Medical Institutions

To build credibility and drive adoption, industry leaders are engaging in joint research initiatives with universities, teaching hospitals, and professional societies. These collaborations help in generating clinical evidence, training surgeons, and integrating new graft technologies into standard treatment protocols across different healthcare systems.

Integration of Digital Surgical Planning Tools

Companies are increasingly incorporating digital tools such as AI-based preoperative modeling, intraoperative imaging software, and simulation platforms into their vascular graft offerings. This approach enhances physician confidence, improves patient-specific graft selection, and streamlines surgical workflow, reinforcing brand loyalty and clinical preference in the Asia Pacific vascular graft market.

COMPETITION OVERVIEW

The competition within the Asia Pacific vascular graft market is shaped by a combination of established multinational firms and emerging domestic manufacturers striving to capture increasing demand driven by rising cardiovascular disease burden and greater access to surgical treatments. Multinational companies with strong R&D capabilities, broad product portfolios, and well-established regulatory pathways continue to dominate the premium segment due to their long-standing clinical validation and surgeon trust. However, regional players are gaining traction by offering cost-competitive alternatives that cater to price-sensitive healthcare systems and under-resourced hospitals.

A notable shift in competitive dynamics is occurring as healthcare providers prioritize procedural efficiency, patient safety, and post-surgical outcomes, leading to increased scrutiny over graft durability, infection rates, and thrombogenicity. Companies are responding by investing in next-generation graft coatings, antimicrobial integration, and surface modification technologies aimed at improving patency and reducing revision surgeries. Additionally, partnerships with national health programs and participation in government tenders have become strategic focal areas for market expansion.

Moreover, technological convergence between medical device makers and digital health platforms is redefining how vascular grafts are selected, deployed, and monitored post-operatively.

RECENT MARKET DEVELOPMENTS

- In May 2024, Terumo Corporation launched a dedicated vascular innovation center in Singapore to support surgical training, product testing, and clinician engagement in Southeast Asia. This initiative was designed to deepen Terumo’s technical support network and facilitate faster adoption of its latest graft technologies in the region.

- In February 2024, B. Braun entered into a strategic collaboration with a leading Indian hospital network to co-develop vascular surgery protocols using its prosthetic grafts. This move aimed at enhancing surgeon familiarity with the company's product line and securing institutional procurement contracts in major urban and rural surgical hubs.

- In July 2024, Getinge AB introduced a mobile vascular surgery training unit across Indonesia and the Philippines to educate local medical teams on best practices in graft implantation and perioperative management. This initiative was intended to improve clinical outcomes while strengthening Getinge’s brand value in secondary healthcare markets.

- In January 2024, LeMaitre Vascular expanded its distribution footprint in South Korea by partnering with a local distributor specialized in vascular implants. This step was taken to increase market penetration and accelerate product availability in a country with growing elderly-driven vascular disease rates.

- In September 2024, Lifeline Scientific (now part of XVIVO Perfusion Inc.) initiated a clinical awareness campaign in Australia to promote graft preservation techniques and extend vascular conduit viability during complex procedures. This effort focused on building surgeon relationships and reinforcing the company’s commitment to advancing vascular graft utilization through enhanced surgical support systems.

MARKET SEGMENTATION

This Asia Pacific vascular graft market research report is segmented and sub-segmented into the following categories.

By Indication

- Endovascular Aneurysm Repair

- Abdominal Aortic Aneurysms Repair

- Thoracic Aortic Aneurysm Repair

- Peripheral Vascular

- Hemodialysis Access

By Raw Material

- Polyester Grafts

- ePTFE

- Polyurethane Grafts

- Biosynthetic Grafts

By End User

- Hospitals

- Ambulatory Surgical Centers

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

What are some key drivers of the APAC Vascular Graft Market?

The rising prevalence of cardiovascular diseases, a growing aging population, and technological advancements in vascular graft materials and designs are majorly driving the vascular graft market in the Asia-Pacific region.

Who are the major players in the APAC Vascular Graft Market?

Medtronic, Terumo Corporation, W.L. Gore & Associates, B. Braun Melsungen AG, and LeMaitre Vascular, Inc. are a few of the key players in the APAC vascular graft market.

Which countries are included in the APAC Vascular Graft Market?

China, Japan, India, South Korea and Australia are the countries included in this research report.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com