Asia Pacific Stevia Market Size, Share, Trends, & Growth Forecast Report – Segmented by Extract Type (Whole Leaf, Powdered, Liquid), Application, Form, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis, Size, Share, Growth, Trends, And Forecasts 2026 to 2034

Market Size, 2025

$211 MnMarket Estimate, 2026

$234 MnMarket Forecast, 2034

$545 MnCAGR, 2026–2034

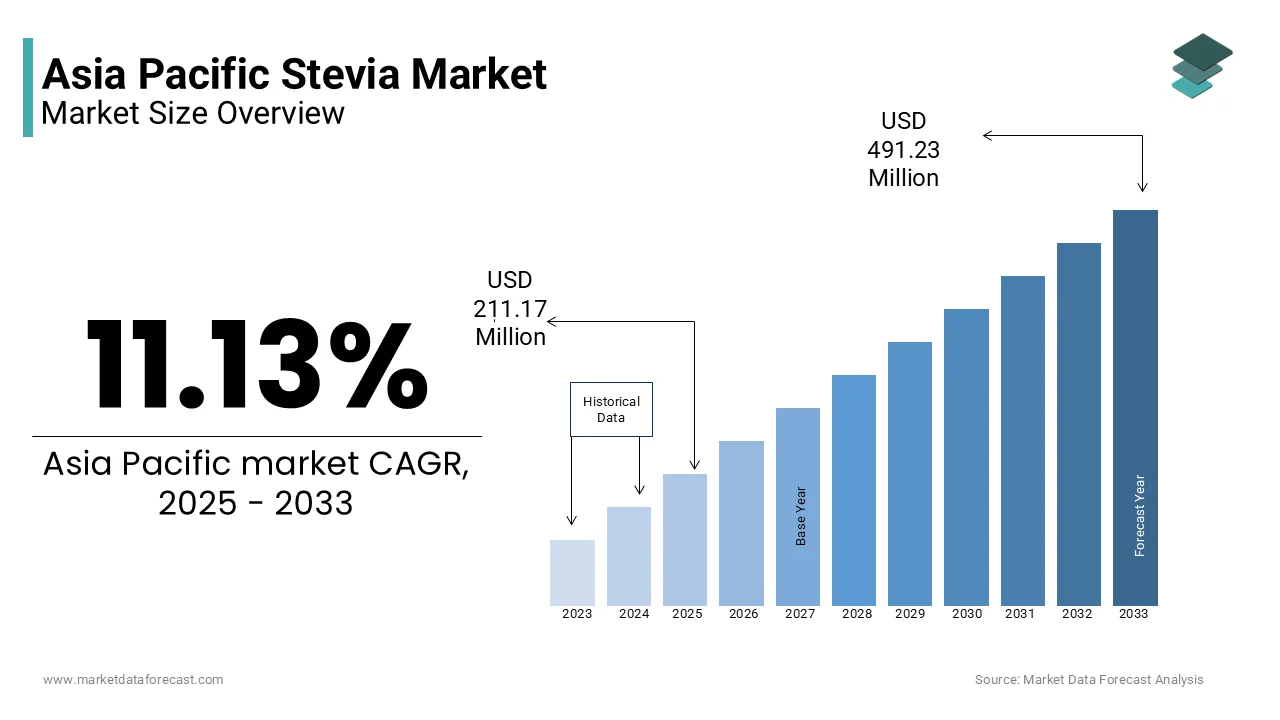

11.13%Asia Pacific Stevia Market Size

The Asia Pacific stevia market size was valued at USD 211.17 million in 2025, and the market size is predicted to reach USD 545.89 million by 2034 from USD 234.67 million in 2026. The market is growing at a CAGR of 11.13%.

Stevia, derived from the leaves of Stevia rebaudiana, is prized for its zero-calorie profile and intense sweetness, making it a preferred choice for health-conscious individuals and diabetics. The region’s growing awareness of lifestyle diseases has positioned stevia as a key ingredient in food and beverage formulations.

MARKET DRIVERS

Rising Health Consciousness Among Consumers

The surge in health consciousness across the Asia Pacific region is a significant driver propelling the stevia market. With increasing urbanization and disposable incomes, consumers are prioritizing wellness and seeking alternatives to traditional sugar. This trend has led to a higher demand for natural sweeteners like stevia, which cater to fitness enthusiasts and individuals managing weight or metabolic conditions. In countries like Australia and South Korea, where gym memberships and dietary supplements are gaining popularity, stevia-based beverages and snacks are becoming mainstream. For instance, a large share of adults engage in regular physical activity, driving the adoption of low-calorie products. In addition, public health campaigns promoting reduced sugar intake have reinforced consumer trust in stevia. Governments, such as Singapore’s Health Promotion Board, have launched initiatives to combat obesity, indirectly boosting the demand for healthier sweeteners.

Growing Demand for Clean Label Products

The demand for clean label products is another critical factor fueling the growth of the Asia Pacific stevia market. Consumers are increasingly scrutinizing product labels for artificial additives and synthetic ingredients, favoring natural and minimally processed alternatives. Stevia, being plant-based and free from chemical residues, aligns perfectly with this consumer preference. Japan, a pioneer in clean label trends, has witnessed widespread adoption of stevia in functional foods and beverages. Similarly, in India, the Food Safety and Standards Authority encourages the use of natural sweeteners, fostering innovation in stevia-based products.

MARKET RESTRAINTS

MARKET RESTRAINTS

Aftertaste Perception and Consumer Acceptance

One of the primary restraints hindering the Asia Pacific stevia market is the lingering perception of its aftertaste. Despite advancements in refining processes, some consumers still associate stevia with a bitter or licorice-like flavor, which can deter adoption. Taste remains a critical barrier for high-intensity sweeteners, particularly among older demographics who are accustomed to traditional sugar. This challenge is particularly pronounced in markets like Thailand and Vietnam, where sugarcane-based sweeteners dominate culinary traditions. To counteract this issue, manufacturers are investing in blending stevia with other natural sweeteners like erythritol to mask undesirable flavors. However, these solutions often increase production costs, limiting affordability for price-sensitive consumers. Public education campaigns aimed at dispelling misconceptions about stevia’s taste are underway but require time to gain traction.

High Production Costs and Pricing Challenges

Another significant restraint is the relatively high production cost of stevia compared to conventional sweeteners. Cultivating Stevia rebaudiana requires specific climatic conditions and meticulous agricultural practices, which elevate input costs. Also, the yield per hectare for stevia is considerably lower than sugarcane, making it less economically viable for mass production. In emerging economies like Indonesia and the Philippines, where affordability is a key purchasing criterion, stevia struggles to compete with cheaper alternatives like cane sugar. Also, small-scale farmers face difficulties transitioning to stevia cultivation due to limited access to capital and technical expertise.

MARKET OPPORTUNITIES

Expansion in Functional Foods and Beverages

The burgeoning functional foods and beverages segment presents a lucrative opportunity for the Asia Pacific stevia market. Consumers are increasingly seeking products that offer health benefits beyond basic nutrition, such as weight management and blood sugar regulation. Stevia’s natural origin and zero-calorie properties make it an ideal sweetener for fortifying these products.

In South Korea, for instance, the Ministry of Food and Drug Safety has approved stevia for use in fortified beverages targeting millennials and Gen Z consumers. Similarly, in China, the National Health Commission has endorsed stevia-based energy drinks, aligning with the country’s "Healthy China 2030" initiative. Manufacturers are capitalizing on this trend by launching innovative formulations, such as stevia-sweetened probiotic drinks and protein bars, catering to diverse consumer needs.

Increasing Adoption in Bakery and Confectionery

The bakery and confectionery sector offers another promising avenue for stevia’s expansion in the Asia Pacific market. With rising concerns about sugar-related health issues, companies are reformulating their products to incorporate natural sweeteners. Stevia’s ability to deliver sweetness without compromising texture makes it a valuable ingredient in low-sugar cakes, cookies, and chocolates. In Japan, major brands like Meiji have successfully integrated stevia into their confectionery lines, appealing to health-conscious consumers. Similarly, in India, startups are experimenting with stevia-infused traditional sweets like laddoos and barfis, bridging the gap between cultural preferences and modern health trends.

MARKET CHALLENGES

Competition from Alternative Sweeteners

Intense competition from alternative sweeteners poses a significant challenge to the Asia Pacific stevia market. Products like monk fruit extract, allulose, and tagatose are gaining traction due to their unique taste profiles and perceived health benefits. Monk fruit, in particular, is emerging as a formidable competitor due to its absence of bitterness and alignment with clean label trends. In China, the world’s largest producer of monk fruit, local manufacturers enjoy a competitive edge in terms of cost and availability. This proximity creates pricing pressure for stevia suppliers attempting to penetrate similar markets.

Regulatory Hurdles and Fragmentation

Regulatory hurdles and fragmentation across the Asia Pacific region represent another challenge for the stevia market. Each country has its own set of guidelines governing the use of natural sweeteners, complicating compliance for multinational companies. According to the Asia-Pacific Economic Cooperation (APEC), inconsistent regulations create logistical barriers, delaying product launches and increasing operational costs. Furthermore, stringent labeling requirements and safety assessments add to the complexity. In India, for example, the Food Safety and Standards Authority mandates rigorous testing for stevia extracts, prolonging approval timelines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.13% |

| Segments Covered | By Extract Type, Application, Form, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Nestlé S.A., The Coca-Cola Company, PepsiCo Inc., Cargill Inc., Evolva Holding S.A., PureCircle Ltd., Stevia Corp., Ingredion Inc., GLG Life Tech Corp., and Tate & Lyle Plc, and others |

SEGMENTAL ANALYSIS

By Extract Type Insights

The powdered stevia segment dominated the Asia Pacific stevia market by commanding a 55.6% of the total market share in 2025. This influence is supported by its versatility and ease of integration into a wide range of food and beverage products. One key factor behind its popularity is its compatibility with dry formulations, such as tabletop sweeteners and bakery mixes. Another driving force is consumer familiarity and convenience. In countries like India and China, where urban households prioritize quick and easy solutions, powdered stevia serves as a direct sugar substitute for daily use. Also, advancements in refining technologies have improved the taste profile of powdered stevia, addressing earlier concerns about bitterness and enhancing its appeal among health-conscious consumers.

Liquid stevia is the fastest-growing segment, with a projected CAGR of 14.2%. This rapid expansion is fueled by its increasing adoption in beverages and liquid-based applications. A major driver is the booming functional beverage market. Liquid stevia’s solubility and ability to blend seamlessly into drinks make it an ideal choice for this segment. Another significant factor is its rising use in dietary supplements and health tonics. In Japan, the Ministry of Health has approved liquid stevia for use in fortified energy drinks, aligning with the country’s focus on preventive healthcare. Furthermore, startups in South Korea are innovating by combining liquid stevia with probiotics and vitamins, creating niche products that cater to millennials.

By Application Insights

The beverages segment was the largest application category by accounting for a 35.6% of the Asia Pacific stevia market. This dominance is attributed to the growing demand for low-calorie and sugar-free drinks, particularly among health-conscious millennials. Also, the functional beverage market in the region grew in 2022, with stevia playing a pivotal role in product formulations. Sports drinks, energy beverages, and flavored waters are increasingly incorporating stevia to meet consumer preferences for natural sweetness without added calories. Another driving factor is the influence of government-led campaigns promoting reduced sugar consumption. In Singapore, the Health Promotion Board launched the “War on Diabetes” initiative, encouraging beverage manufacturers to adopt stevia as a healthier alternative to artificial sweeteners. Besides, multinational companies like Coca-Cola and PepsiCo have introduced stevia-sweetened variants in markets like Australia and Japan, further strengthen beverages as the leading application segment.

Tabletop sweeteners segment is emerging with a highest CAGR of 12.8%. This growth is driven by the increasing prevalence of lifestyle diseases and the need for convenient sugar substitutes in households. Tabletop stevia provides an accessible solution for managing blood sugar levels and reducing calorie intake. Additionally, e-commerce platforms have played a crucial role in boosting accessibility, with online retailers offering a variety of branded stevia products. The segment’s affordability and ease of use ensure its continued expansion, positioning it as a key growth driver in the stevia market.

By Form Insights

The Dry stevia segment commanded with a 60.8% which is primarily due to its widespread use in processed foods and packaged goods. One key factor behind its dominance is its stability during storage and transportation, making it a preferred choice for manufacturers. Like, dry stevia is used in large share of sugar-free confectionery products, underscoring its critical role in the food industry. Another driving force is its affordability compared to liquid formulations. In emerging economies like Indonesia and Thailand, small-scale producers rely on dry stevia to keep costs low while meeting consumer demand for natural sweeteners. Dry stevia can be stored for up to two years without degradation, ensuring consistent quality and reducing wastage.

The liquid stevia segment is the quickly advancing, with a CAGR of 13.5% and is driven by its rising popularity in beverages and liquid-based formulations. A major factor is the growing trend of personalized nutrition, where consumers seek customizable sweetening options. Additionally, advancements in extraction technologies have improved the taste and clarity of liquid stevia, making it suitable for premium products.

REGIONAL ANALYSIS

China led the Asia Pacific stevia market with a 28.4% share. It is driven by its status as the world’s largest producer and exporter of stevia extracts. The country’s advanced agricultural infrastructure supports large-scale cultivation of Stevia rebaudiana. Also, domestic demand for natural sweeteners is surging, particularly in urban centers like Shanghai and Beijing, where health-conscious consumers dominate.

Japan is a key player in the market and is characterized by its early adoption of stevia and robust regulatory framework. Government initiatives promoting preventive healthcare further bolster its prominence in the market.

Indian market is supported by its large population and rising incidence of diabetes. It’s affordability and availability in retail outlets make it a popular choice among middle-income households.

Australia holds a significant position in the market. This is driven by its emphasis on clean label products and wellness trends. Also, stevia as a safe alternative to sugar, fostering its adoption in health-focused snacks and beverages. The country’s strong e-commerce infrastructure also enhances accessibility for consumers.

South Korea commands a smaller share, marked by its innovative approach to stevia-based products. Startups are leveraging stevia to create unique formulations, catering to younger, health-conscious consumers.

COMPETITIVE LANDSCAPE

The Asia Pacific stevia market is highly competitive, characterized by the presence of multinational corporations and regional players striving to gain market share. Global giants like Cargill and PureCircle leverage their technological expertise and extensive distribution networks to maintain dominance, while local manufacturers focus on affordability and customization to cater to specific regional needs. The market’s competitive landscape is shaped by factors such as pricing strategies, product innovation, and regulatory compliance. Environmental regulations, in particular, are pushing companies to develop sustainable alternatives, creating new avenues for differentiation. Additionally, the rise of e-commerce platforms for grocery and health products has intensified competition, as companies vie for online visibility and customer engagement.

KEY MARKET PLAYERS

The key players in the Asia Pacific stevia market are

- Nestlé S.A.

- The Coca-Cola Company

- PepsiCo Inc.

- Cargill Inc.

- Evolva Holding S.A.

- PureCircle Ltd.

- Stevia Corp.

- Ingredion Inc.

- GLG Life Tech Corp.

- Tate & Lyle Plc

TOP PLAYERS IN THE MARKET

- Cargill is a global leader in the stevia market, with a significant presence in the Asia Pacific region. The company’s proprietary stevia-based sweetener, EverSweet, has gained traction for its superior taste and versatility in food and beverage applications. Cargill’s contribution to the global market lies in its focus on sustainable sourcing and advanced fermentation technologies, ensuring high-quality products while minimizing environmental impact. By collaborating with local farmers, Cargill supports sustainable agricultural practices, reinforcing its leadership position in the region.

- PureCircle, now part of Ingredion, is renowned for its expertise in developing innovative stevia solutions tailored to consumer preferences. The company’s emphasis on next-generation stevia extracts, such as Reb M and Reb D, addresses taste challenges and enhances product appeal. PureCircle’s commitment to clean label trends and sustainability aligns with the growing demand for natural sweeteners, making it a trusted partner for global brands seeking healthier alternatives.

- GLG Life Tech Corporation is a key player in the Asia Pacific stevia market, known for its vertically integrated supply chain and cost-effective solutions. The company focuses on producing high-purity stevia extracts that meet stringent regulatory standards. GLG’s partnerships with manufacturers and retailers enable it to cater to diverse applications, from tabletop sweeteners to functional beverages. Its dedication to innovation and quality ensures a strong foothold in both regional and global markets.

TOP STRATEGIES USED BY KEY PLAYERS

Focus on Taste Improvement and Product Innovation

- Leading players are investing heavily in research and development to enhance the taste profile of stevia-based products. By leveraging advanced extraction techniques and blending stevia with other natural sweeteners, companies aim to eliminate bitterness and improve consumer acceptance. These innovations not only differentiate their offerings but also expand the range of applications, from beverages to baked goods.

Expansion into Emerging Markets

- Companies are aggressively expanding their footprint in emerging economies like India and Vietnam, where urbanization and health awareness are driving demand for natural sweeteners. This includes establishing local manufacturing units and distribution networks to ensure affordability and accessibility.

Sustainability and Ethical Sourcing Initiatives

- Sustainability remains a cornerstone strategy for key players in the stevia market. By promoting ethical sourcing practices and supporting small-scale farmers, companies align with global environmental goals while ensuring a steady supply of raw materials.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, PureCircle partnered with the Indian Ministry of Health to launch a nationwide campaign promoting the benefits of stevia in managing diabetes. This initiative aims to educate consumers and boost adoption of stevia-based products across the country.

- In May 2025, Cargill acquired a Singapore-based startup specializing in liquid stevia formulations for beverages. This acquisition enhances Cargill’s ability to cater to the growing demand for customized sweetening solutions in the Asia Pacific region.

- In July 2025, GLG Life Tech Corporation introduced a new line of organic-certified stevia extracts tailored for premium health products in Japan. These products align with the country’s focus on clean label trends and wellness.

- In September 2025, Tate & Lyle established a joint venture with the Vietnamese government to build a state-of-the-art stevia processing facility near Ho Chi Minh City. This collaboration aims to address local supply chain challenges while supporting Vietnam’s agricultural modernization efforts.

- In November 2025, Morita Kagaku Kogyo launched a mobile application offering personalized stevia product recommendations for consumers in Australia. The app integrates dietary preferences and health goals to provide actionable insights, enhancing customer satisfaction and loyalty.

MARKET SEGMENTATION

This research report on the Asia Pacific stevia market has been segmented and sub-segmented based on the following categories.

By Extract Type

- Introduction

- Whole Leaf

- Powdered

- Liquid

By Application

- Dairy, Bakery & Confectionery

- Tabletop Sweeteners

- Beverages

- Convenience Foods

By Form

- Introduction

- Dry

- Liquid

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is driving the growth of the Asia Pacific stevia market?

Rising demand for natural sweeteners and growing health awareness are the key drivers.

2. Which countries in Asia Pacific lead the stevia market?

China, India, Japan, and South Korea are the major contributors to market demand.

3. Why is stevia popular among health-conscious consumers?

Stevia is zero-calorie, plant-based, and suitable for diabetic and weight-management diets.

4. What industries use stevia the most in Asia Pacific?

Food & beverages, pharmaceuticals, and nutraceuticals use stevia widely.

5. Is the demand for stevia rising in beverages?

Yes, beverage makers increasingly use stevia as a sugar alternative in soft drinks and teas.

6. How does stevia compare to artificial sweeteners?

Stevia is natural with fewer side effects, making it preferred over synthetic sweeteners.

7. What forms of stevia are commonly available?

Powder, liquid extracts, and stevia leaf products are widely sold.

8. What challenges does the Asia Pacific stevia market face?

Higher production costs and taste-profile concerns can limit adoption.

9. Which companies dominate the Asia Pacific stevia market?

Key players include PureCircle, Cargill, Tate & Lyle, and regional producers.

10. How is the shift toward clean-label products impacting stevia demand?

Clean-label preferences are boosting stevia adoption as a natural sweetener.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com