Global Artificial Pancreas Device Systems Market Size, Share, Trends & Growth Forecast Report By Type, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$301 MnMarket Estimate, 2026

$347.66 MnMarket Forecast, 2034

$1101 MnCAGR, 2026–2034

15.5%Global Artificial Pancreas Device Systems Market Size

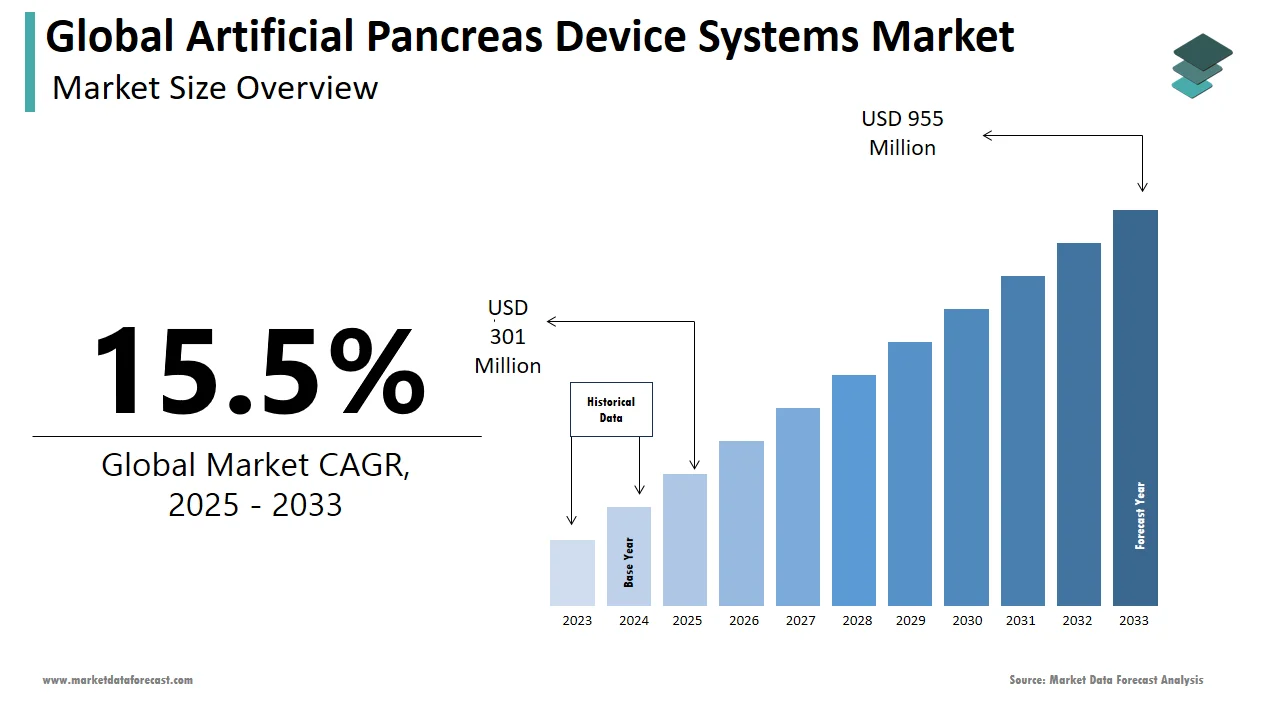

The size of the global artificial pancreas device systems market was worth USD 301 million in 2025. The global market is anticipated to grow at a CAGR of 15.5% from 2026 to 2034 and be worth USD 1,101 million by 2034 from USD 347.66 million in 2026.

MARKET DRIVERS

The growing diabetic population and the increasing prevalence of diabetes are the main reasons for the increasing demand for an artificial pancreas device system (APDS) during the forecast period.

According to the International Diabetes Federation (IDF), in 2021, more than 537 million adults (20-79 years old) worldwide will be living with diabetes globally. The total number of people living with diabetes is estimated to reach 643 million by 2030 and 783 million by 2045. Low- and middle-income countries are the most affected, particularly in Asia, Africa, and Latin America. The rising prevalence of pancreatic cancer, pancreatitis, and other chronic conditions also drives the market. In addition, the increasing incidence of obesity due to age-related factors, physical inactivity, and unhealthy eating habits are also contributing to the widespread adoption of APDS in the world.

APDS automatically monitors glucose levels and delivers insulin doses throughout the day in controlled amounts. Almost 1 in 2 adults (240 million) live with diabetes and are undiagnosed. In 2021, approximately 6.7 million deaths were due to diabetes. Hence, the use of APDS will decrease the death rate and complications in diabetic patients across the globe. There is a massive requirement for an effective and long-lasting alternative drug that can substitute insulin. However, type 2 diabetes can be well controlled in most patients with oral medications, but people with type 1 diabetes should use insulin first. Various technological innovations, including the development of software-based wireless systems that integrate with automated controls, further contribute to the market's growth. At least US$966 billion in healthcare spending was spent on diabetes in 2021, including 9% of total spending for adults.

More than 10% of the diabetic population is affected by type 1 diabetes. People with type 1 diabetes need to inject insulin daily to control their blood sugar and symptoms. In addition, worldwide, more than 1.2 million children and adolescents (0-19 years old) live with type-1 diabetes. Thus, it increases the demand for APDS and further drives the market's growth. Growing demand for effective minimally invasive (MI) diabetes monitoring and drug delivery systems is also driving market growth. Local governments in many countries are investing heavily in research and development (R&D) to improve healthcare infrastructure worldwide.

MARKET RESTRAINTS

However, certain restraints and difficulties encountered may hinder the growth of the artificial pancreas device system market, such as the lack of trained professionals in underdeveloped regions like Africa and South America and limited resources for research and development.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Medtronic Plc, Johnson & Johnson, Insulet Corp, Tandem Diabetes Care, F. Hoffmann-La Roche Ltd, Beta Bionics, Bigfoot Biomedical Inc., Inreda Diabetic B.V., Dexcom, Inc., Cellnovo., and Others. |

SEGMENTAL ANALYSIS

By Type Insights

Based on type, the control-to-target system segment held the largest share of the worldwide market in 2024 and is expected to grow with the highest CAGR during the forecast period. The CTT system is anticipated to witness the fastest growth with a healthy CAGR. CTT system is a fully automated system that minimizes patient intervention, and this factor will contribute to the market growth rate.

By End User Insights

Based on end-user, the hospital segment held the leading share of the global market in 2024 and is anticipated to grow at a notable share of the global market during the forecast period. The growth of this segment can be attributed to the growing number of hospitals with the latest adoption of APDS and the presence of skilled labor.

REGIONAL ANALYSIS

Europe Artificial Pancreas Device Systems Market Analysis

Europe dominated the artificial pancreas device system market, and it is likely to continue the same trend during the forecast period. According to Beyond Type 1, approximately 1.64 million people have type 1 diabetes. In addition, 5 million people are estimated to be diagnosed with type 1 diabetes by 2050. A higher incidence of diabetes will be the primary driver leading the market in this region. According to the Administration of Food and Drug Administration, using an artificial pancreas is associated with better blood sugar control in people with type 1 diabetes than the normal methods. Hence, owing to this factor, major players are increasing funding to develop better and more innovative devices to cater to the growing market demand across European countries.

North America Artificial Pancreas Device Systems Market Analysis

During the forecast period, North America is estimated to be a significant market shareholder, owing to various factors such as the rising geriatric population, the high incidence rate of diabetes and its complications, well-developed medical facilities, and technological advancements. According to the Centers for Disease Control and Prevention (CDC) National Diabetes Statistics 2020 report, approximately 34.24 million people of all ages had diabetes in the United States in 2018. The percentage of adults with diabetes has increased with age to reach 26.8% among those over 65. Additionally, nearly 88 million American adults were estimated to have prediabetes in 2018. According to the Institute for Health Metrics and Evaluation, the prevalence rate of diabetes mellitus in 2019 was estimated at 11,847 per 100,000 and 11,366 per 100,000 in 2018 in the U.S. The elderly population is more susceptible to acquiring diabetes with age and a preference for a sedentary lifestyle in the region. Based on the Bureau of Population Reference's Aging in America population bulletin, the number of Americans age 65 and older is expected to nearly double, from 52 million in 2018 to 95 million by 2060.

Asia Pacific Artificial Pancreas Device Systems Market Analysis

However, the Asia Pacific region is projected to witness the fastest growth in the studied market. The development of this regional market is due to factors such as growing demand for APDS in developing countries, increasing healthcare expenditure, and the availability of a large population base. According to an article published by NCBI, Asian countries account for more than 60% of the global diabetic population, driving the growth of the APDS market in the region.

KEY MARKET PARTICIPANTS

Some of the noteworthy companies that dominate the global artificial pancreas device systems market in this report are

- Medtronic Plc

- Johnson & Johnson

- Insulet Corp

- Tandem Diabetes Care

- F. Hoffmann-La Roche Ltd

- Beta Bionics

- Bigfoot Biomedical Inc.

- Inreda Diabetic B.V.

- Dexcom, Inc.

- Cellnovo

MARKET SEGMENTATION

This research report on the global artificial pancreas device systems market has been segmented and sub-segmented based on type, end-user, and region.

By Type

- Control to Range

- Control to Target Systems

By End User

- Hospital

- Medical Centers

- Others

By Region

- North America

- The U.S.

- Canada

- Rest of North America

- Europe

- UK

- France

- Spain

- Germany

- Italy

- Rest of EU

- Asia-Pacific

- India

- China

- Japan

- South Korea

- Australia & New Zealand

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Chile

- Rest of Latin America

- Middle East

- Africa

Frequently Asked Questions

1. What is the global artificial pancreas device systems market?

The global artificial pancreas device systems market includes automated insulin dosing devices that combine CGM sensors and pumps to maintain glucose levels without manual adjustments.

2. What was the size of the global artificial pancreas device systems market in 2025?

The global artificial pancreas device systems market was valued at USD 301 million in 2025 due to increasing type-1 diabetes cases and demand for automated therapy.

3. What is the expected value of the global artificial pancreas device systems market by 2034?

The global artificial pancreas device systems market is projected to reach USD 1,101 million by 2034 due to rising clinical acceptance and advancing device algorithms.

4. What CAGR is expected in the global artificial pancreas device systems market?

The global artificial pancreas device systems market is forecasted to grow at a 15.5% CAGR from 2026-2034 supported by improved automation and self-monitoring technologies.

5. What components lead the global artificial pancreas device systems market?

Insulin pumps, CGM sensors and AI-based dosing algorithms dominate usage in the global artificial pancreas device systems market.

6. Who uses the global artificial pancreas device systems market most?

Patients with type-1 diabetes, young adults and pediatric users rely heavily on the global artificial pancreas device systems market for glucose self-management.

7. What drives demand in the global artificial pancreas device systems market?

The global artificial pancreas device systems market grows due to reduced finger-prick monitoring, fewer hypoglycemic episodes and improved lifestyle independence.

8. Which regions lead the global artificial pancreas device systems market?

North America leads the global artificial pancreas device systems market, while Europe and Asia-Pacific expand due to improved reimbursement and device availability.

9. What challenges affect the global artificial pancreas device systems market?

Device cost, insurance gaps, replacement frequency and learning curve issues affect growth in the global artificial pancreas device systems market.

10. How does CGM technology impact the global artificial pancreas device systems market?

Real-time sensor accuracy strengthens dosage precision and accelerates adoption in the global artificial pancreas device systems market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com