- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$2.14 BnMarket Estimate, 2026

$2.43 BnMarket Forecast, 2034

$6.79 BnCAGR, 2026–2034

13.69%Executive Summary: Asia Pacific Ablation Devices Market

- Market Scope: Comprehensive regional Asia Pacific ablation devices market analysis covering device types, clinical applications, end-user settings, geographic leadership frameworks, key growth drivers, and strategic industry trends.

- Market Valuation: Valued at USD 2.14 billion (2025), estimated at USD 2.43 billion (2026), and projected to reach USD 6.79 billion by 2034, registering a robust CAGR of 13.69% (2026–2034).

- Primary Growth Drivers: Rising prevalence of cardiac arrhythmias and cancer, an aging geriatric population, and significant improvements in regional healthcare infrastructure. Notable trends include the rapid adoption of minimally invasive oncological treatments, technological advancements in AI-integrated mapping and pulsed field ablation systems, and strategic expansions by multinational manufacturers.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Device Type | Radiofrequency ablation devices (dominated the market with a 38.5% share in 2025) | Cryoablation devices (projected to grow at a CAGR of 13.2%) |

| By Application | Cardiovascular disease treatment (held the largest application share at 36.4% in 2025) | Cancer treatment (fastest-growing segment with a CAGR of 14.1%) |

| By End User | Hospitals (remain the dominant end-user segment for ablation procedures) | Ambulatory Surgical Centers (expected to expand at a CAGR of 11.8%) |

| By Region / Country | China (led the regional market with a 25.3% share in 2025, followed by Japan at 18.2%) | India (positioned for lucrative growth driven by government initiatives like Ayushman Bharat) |

Major Market Players & Market Structure

Market Structure: Highly competitive medical device landscape featuring leading multinational companies competing through regional innovation hubs, manufacturing expansions, electrophysiology training partnerships, and integrated imaging collaborations.

Key Companies: Abbott Laboratories, Boston Scientific Corporation, Medtronic PLC, Conmed Corporation, Olympus Corporation, Biotronik, and Edwards Lifesciences.

Asia Pacific Ablation Devices Market Size

The Asia Pacific ablation devices market reached USD 2.14 billion in 2025, is expected to grow to USD 2.43 billion in 2026, and is anticipated to touch USD 6.79 billion by 2034, at a CAGR of 13.69% from 2026 to 2034.

The ablation devices are widely utilized in cardiology, oncology, and pain management to treat conditions such as cardiac arrhythmias, tumors, and chronic nerve pain. Over recent years, the region has witnessed a surge in demand for these devices due to rising prevalence of lifestyle diseases, improving healthcare infrastructure, and growing adoption of advanced therapeutic solutions. According to the World Health Organization, non-communicable diseases account for over 60% of total deaths in the Asia Pacific region, significantly driving the need for efficient interventional therapies. Moreover, the increasing geriatric population across countries like Japan and South Korea further amplifies the demand for ablation-based treatments. The expansion of private healthcare networks and rising disposable incomes are also contributing to greater patient access to ablation procedures.

MARKET DRIVERS

Rise in Prevalence of Cardiac Arrhythmias

One of the most significant drivers fueling the Asia Pacific ablation devices market is the escalating incidence of cardiac arrhythmias, particularly atrial fibrillation (AFib). This surge is primarily attributed to aging populations, rising obesity rates, and increased diagnosis capabilities. Countries such as Australia, Japan, and South Korea report high hospitalization rates due to rhythm disorders, directly boosting the utilization of catheter ablation procedures. Moreover, technological advancements have enhanced the precision and safety of ablation systems. For instance, the uptake of cryoablation and radiofrequency ablation technologies has grown rapidly in urban hospitals. Additionally, government initiatives aimed at expanding cardiovascular care access, especially in Southeast Asian nations, are accelerating device adoption. In India, the National Health Mission has supported the establishment of over 200 dedicated electrophysiology labs since 2018, according to the Indian Heart Rhythm Society.

Expansion of Healthcare Infrastructure and Private Medical Facilities

Another pivotal driver propelling the Asia Pacific ablation devices market is the rapid development of healthcare infrastructure, particularly in emerging economies. Countries such as Indonesia, Vietnam, and the Philippines have seen substantial investments in private healthcare facilities, which are increasingly adopting advanced diagnostic and therapeutic equipment. In tandem, rising health insurance penetration and out-of-pocket expenditure in the private sector have improved patient affordability for complex procedures. The Insurance Information Institute reports that private health insurance coverage in Thailand increased by nearly 12% in 2022 alone, enabling broader access to ablation therapies. Furthermore, strategic collaborations between international device manufacturers and local distributors have facilitated easier access to ablation systems. For example, Boston Scientific and Abbott have established regional hubs in Singapore and Malaysia to streamline supply chains and reduce costs.

MARKET RESTRAINTS

High Cost of Advanced Ablation Technologies

One of the primary constraints hindering the growth of the Asia Pacific ablation devices market is the prohibitively high cost associated with advanced ablation technologies. Sophisticated systems such as robotic-assisted platforms and high-resolution mapping devices often require significant capital investment, making them inaccessible to smaller hospitals and clinics, especially in low- and middle-income countries. Even in moderately developed markets such as Bangladesh and Laos, only a handful of tertiary care centers can afford to integrate next-generation ablation systems into their routine practices. Additionally, the lack of standardized reimbursement policies across several Asia Pacific nations limits patient access to these procedures. In Malaysia, for instance, despite growing awareness about cardiac ablation therapies, public hospitals face delays in procuring advanced devices due to budgetary limitations.

Shortage of Trained Professionals and Standardized Training Programs

A significant restraint affecting the Asia Pacific ablation devices market is the scarcity of skilled healthcare professionals trained in advanced ablation techniques. Performing ablation procedures requires specialized knowledge in electrophysiology, imaging, and real-time navigation, yet the availability of adequately trained cardiologists and technicians remains uneven across the region. This shortage is particularly pronounced in rural and semi-urban areas where access to structured education programs in interventional cardiology is limited. In India, despite having a large pool of general cardiologists, fewer than 10% receive formal training in ablation procedures, as in a 2023 publication by the Indian Pacing and Electrophysiology Journal. The lack of accredited training centers and standardized certification processes contributes to inconsistent procedural outcomes and slower adoption of newer ablation technologies. Moreover, the learning curve associated with advanced ablation systems such as contact force sensing catheters and 3D electroanatomical mapping requires prolonged hands-on experience, which is often unavailable in lower-tier medical institutions. Japan and South Korea, although leading in technology adoption, still face challenges in scaling up workforce readiness due to rigid regulatory requirements for specialist accreditation.

MARKET OPPORTUNITIES

Increasing Incidence of Cancer and Growing Adoption of Minimally Invasive Oncological Treatments

The rising prevalence of cancer and the increasing shift toward minimally invasive tumor ablation techniques is likely to showcase huge growth opportunities for the Asia Pacific ablation devices market. According to the International Agency for Research on Cancer (IARC), the Asia Pacific region accounts for nearly 50% of all new cancer cases globally, with liver, lung, and thyroid cancers being particularly prevalent in countries such as China, India, and Japan. The effectiveness of these techniques in treating small-to-moderate-sized tumors, especially in early-stage cancers, is gaining traction among oncologists. In a 2023 clinical review published in Cancer Imaging, ablation therapies were found to achieve local tumor control rates exceeding 85% in hepatocellular carcinoma patients who were not eligible for surgery. Moreover, regulatory approvals and favorable reimbursement policies in countries like Australia and South Korea have accelerated the integration of ablation into standard cancer care protocols. The Korean Ministry of Health and Welfare introduced updated guidelines in 2023 endorsing the use of thermal ablation for certain types of liver malignancies, encouraging wider application.

Technological Advancements and Innovations in Ablation Systems

Technological evolution is emerging as a transformative opportunity in the Asia Pacific ablation devices market, driven by innovations that enhance procedural accuracy, reduce complications, and expand treatment indications. Manufacturers are increasingly investing in AI-integrated mapping systems, robotic-assisted platforms, and real-time monitoring tools to improve clinical outcomes. One notable advancement is the introduction of high-resolution electroanatomical mapping systems, which enable physicians to visualize cardiac structures with greater precision. Companies like Abbott and Biosense Webster have launched AI-powered platforms that facilitate faster lesion creation and better identification of arrhythmogenic substrates. Additionally, the emergence of pulsed field ablation (PFA), which selectively targets cardiac tissue without damaging surrounding structures, is gaining attention across the region. Clinical trials conducted in Singapore and Australia have demonstrated PFA's potential to reduce procedural time and improve patient recovery rates. With ongoing research and product launches, coupled with rising investments from multinational firms, the Asia Pacific market is well-positioned to benefit from these cutting-edge developments.

MARKET CHALLENGES

Regulatory Hurdles and Lengthy Approval Processes

One of the foremost challenges confronting the Asia Pacific ablation devices market is the complexity and variability of regulatory frameworks across different countries. Each nation maintains its own set of approval procedures, requiring manufacturers to undergo multiple compliance checks before introducing a product to the market. Japan, for instance, enforces stringent evaluation standards through the Pharmaceuticals and Medical Devices Agency (PMDA) is mandating extensive clinical data even for modified versions of existing devices. Similarly, in India, the Central Drugs Standard Control Organization (CDSCO) has implemented revised guidelines in 2023 that require additional post-market surveillance and quality documentation, increasing the regulatory burden on foreign manufacturers. Moreover, inconsistent enforcement of quality standards across regions complicates supply chain logistics and increases operational costs. In countries like Thailand and the Philippines, frequent policy updates and unclear documentation requirements add further layers of complexity. This regulatory fragmentation hinders uniform market expansion and restricts smaller innovators from entering highly regulated markets, ultimately slowing the diffusion of advanced ablation technologies throughout the region.

Limited Awareness and Low Patient Uptake in Rural Areas

A critical challenge impeding the growth of the Asia Pacific ablation devices market is the limited awareness and low patient uptake of ablation therapies in rural and underserved regions. Despite the increasing availability of ablation technologies in urban hospitals, a significant portion of the population residing in remote areas lacks adequate information about minimally invasive treatment options. This disparity stems from inadequate healthcare outreach programs and insufficient dissemination of medical education in rural settings. Furthermore, the absence of mobile diagnostic units and telemedicine networks in many rural districts exacerbates the problem, preventing timely diagnosis and intervention. Even when patients are aware of ablation procedures, affordability and accessibility remain major barriers. Public health facilities in rural areas often lack the necessary infrastructure to perform ablation, pushing patients toward expensive private clinics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Device Technology, Application, End-uses, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Abbott Laboratories, Boston Scientific Corporation, Medtronic PLC, Conmed Corporation, and Olympus Corporation. |

SEGMENTAL ANALYSIS

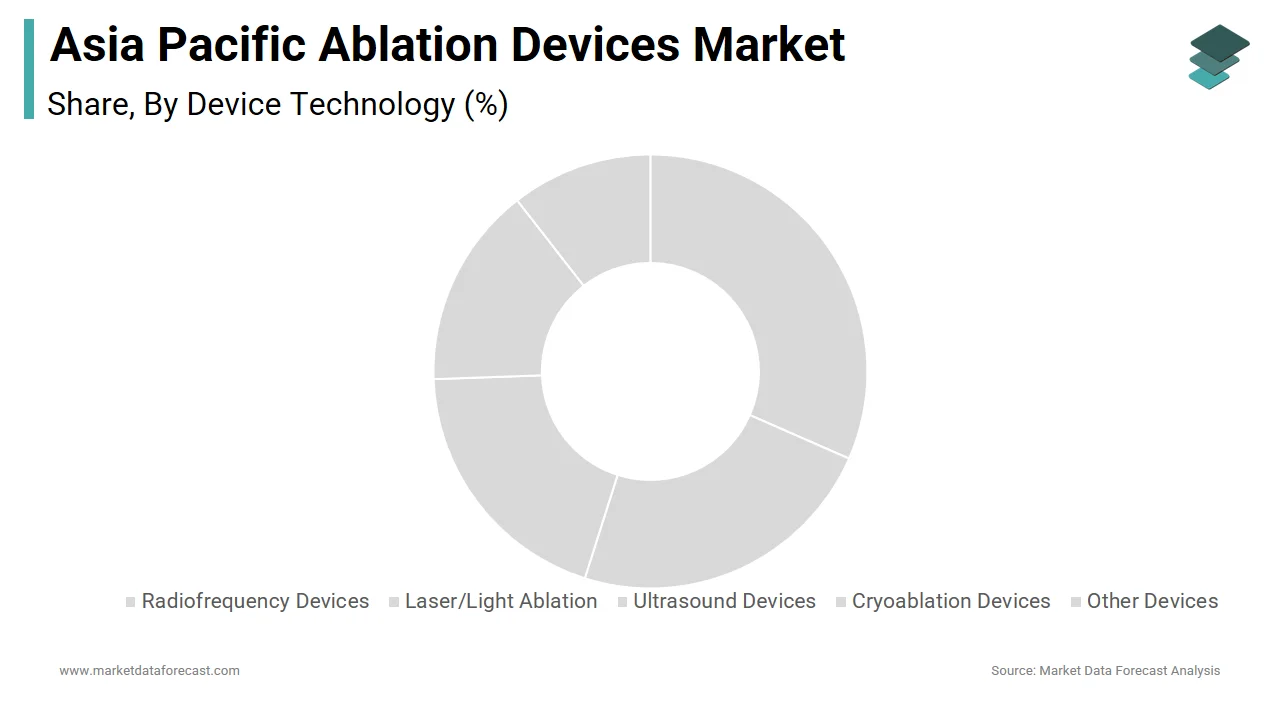

By Device Technology Insights

The radiofrequency ablation devices segment held 38.5% of the Asia Pacific ablation devices market share in 2025, with the widespread adoption of RFA across multiple clinical applications such as cardiology, oncology, and chronic pain management. The Asia Pacific Heart Rhythm Society reported in early 2025 that atrial fibrillation alone affects over 15 million individuals across major countries like China, India, and Japan. As RFA catheterization is considered a gold standard for treating complex arrhythmias, hospitals are increasingly investing in RF mapping and ablation systems. Another contributing element is the robust presence of global manufacturers in the region. Companies such as Abbott and Medtronic have localized their production and distribution networks, especially in China and India, leading to lower procurement costs.

The cryoablation devices segment is projected to grow with an anticipated CAGR of 13.2% in the coming years, owing to the rising preference for cryoablation in treating atrial fibrillation due to its ability to create transmural lesions without charring tissue or causing thromboembolic complications. Similarly, in South Korea, reimbursement policies introduced by the National Health Insurance Service now cover cryo-based ablations for selected cardiac conditions, significantly boosting adoption. Another key growth enabler is the expanding application of cryoablation in oncology. For instance, in Australia, public hospitals have integrated cryoablation for early-stage renal tumors due to its minimal invasiveness and shorter recovery times.

By Application Insights

The cardiovascular disease treatment segment accounted in holding 36.4% of the Asia Pacific ablation devices market share in 2025, with the surging burden of heart rhythm disorders and the critical role ablation plays in managing conditions like atrial fibrillation, ventricular tachycardia, and supraventricular tachycardia. According to the World Heart Federation, cardiovascular diseases account for more than 35% of all deaths in the Asia Pacific, with arrhythmias being a significant contributor to hospitalizations and mortality. Countries like Japan and South Korea are witnessing high penetration of electrophysiological studies and catheter ablation procedures, supported by an aging demographic prone to heart rhythm anomalies. Additionally, government-led initiatives to expand cardiovascular care infrastructure are accelerating adoption. In China, the Ministry of Health has sanctioned over 500 new electrophysiology labs since 2019, according to a 2023 white paper by Frost & Sullivan. Private healthcare providers in India are also investing heavily in catheter labs, with Apollo Hospitals reporting a 45% year-on-year increase in ablation procedures in 2023.

The cancer treatment segment is swiftly emerging with a CAGR of 14.1% in the coming years. This rapid expansion is primarily fueled by the escalating incidence of cancers amenable to minimally invasive ablation techniques, such as liver, lung, and thyroid malignancies. According to the International Agency for Research on Cancer, the Asia Pacific region accounts for nearly half of all new cancer cases globally, with China and India bearing the largest shares. Liver cancer, in particular, is a strong growth driver. In China alone, the National Cancer Center reported over 400,000 new cases of hepatocellular carcinoma in 2023, many of which were treated using radiofrequency or microwave ablation due to limited surgical options. Moreover, the expansion of dedicated cancer centers and improved insurance coverage for interventional oncology procedures is further enhancing access. In Australia, the Medical Services Advisory Committee updated reimbursement guidelines in 2023 to include thermal ablation for early-stage kidney and lung cancers, encouraging broader implementation. Coupled with increasing awareness and investment in precision oncology, cancer treatment continues to be the fastest-growing application area for ablation devices across the Asia Pacific.

By End User Insights

The hospitals segment was the largest by capturing a dominant share of the Asia Pacific ablation devices market in 2025 due to the extensive use of ablation procedures in tertiary and secondary care hospitals for a range of therapeutic applications, including cardiology, oncology, and pain management. In Japan, for example, the Ministry of Health, Labour and Welfare reported in 2023 that over 200 hospitals had fully operational electrophysiology labs, facilitating thousands of cardiac ablation procedures annually. Additionally, the presence of experienced medical professionals and multidisciplinary teams in hospitals enhances procedural success rates and patient outcomes. As per the Asian Heart Institute’s 2023 clinical review, complication-free discharge rates after ablation procedures in large hospitals exceed 95%, reinforcing hospitals’ central role in delivering these services.

The Ambulatory Surgical Centers (ASCs) segment is likely to grow with a CAGR of 11.8% in the next coming years due to a shift toward outpatient procedures, cost efficiencies, and enhanced patient convenience offered by ASCs compared to traditional hospital settings. One major growth driver is the rising preference for non-invasive ablation procedures for chronic pain and minor cardiac dysfunctions. In South Korea, the Korean Society for Interventional Pain Physicians reported in 2023 that over 40% of pain management clinics had incorporated radiofrequency ablation into their outpatient offerings, reducing hospital admissions and lowering overall healthcare costs.

COUNTRY-LEVEL ANALYSIS

China Ablation Devices Market Insights

China was the largest contributor in the Asia Pacific ablation devices market by accounting for 25.3% of share in 2025 with a combination of a large patient pool suffering from cardiovascular diseases, aggressive domestic manufacturing expansion, and increasing government support for modernizing healthcare infrastructure. In addition to rising disease prevalence, the proliferation of private hospitals and the expansion of urban healthcare networks have facilitated greater access to ablation therapies. As reported by the National Health Commission of China in 2023, over 800 new electrophysiology labs were established in Tier-1 and Tier-2 cities over the past five years, significantly boosting procedural volumes. Moreover, multinational companies such as Abbott and Medtronic have intensified their presence through joint ventures and localized R&D, catering to the growing demand for advanced ablation systems.

Japan Ablation Devices Market Insights

Japan ablation devices market held 18.2% of the share in 2025. The country's mature healthcare system, coupled with an aging population and high prevalence of chronic conditions, supports a thriving demand for ablation technologies. Furthermore, favorable reimbursement policies by the Ministry of Health, Labour and Welfare encourage widespread utilization of ablation therapies.

India Ablation Devices Market Insights

India ablation devices market growth is likely to pose a lucrative CAGR in the coming years. One of the major growth drivers is the surge in cardiovascular ailments, particularly in urban centers. The Indian Council of Medical Research reported in 2023 that over 10 million Indians suffer from atrial fibrillation, leading to heightened demand for catheter ablation. Government initiatives such as the Ayushman Bharat scheme have also played a pivotal role in improving access to ablation therapies in public hospitals. As per the National Health Authority, over 50,000 cardiac ablation procedures were subsidized under the scheme in FY 2023 alone.

Australia Ablation Devices Market Insights

Australia ablation devices market growth is driven by the country's benefits from a well-developed healthcare ecosystem, high healthcare expenditure per capita, and strong regulatory support for medical innovation. According to the Australian Institute of Health and Welfare, cardiovascular diseases remain one of the leading causes of death, affecting over 4.2 million Australians, which fuels consistent demand for ablation-based interventions.

South Korea Ablation Devices Market Insights

South Korea ablation devices market is steadily growing with a technologically advanced healthcare system and rising prevalence of chronic diseases. According to the Korean Society of Cardiology, the country recorded over 1.2 million diagnosed cases of arrhythmias in 2023, with a significant portion undergoing ablation therapy. Additionally, South Korea benefits from a highly integrated supply chain for medical devices, supported by partnerships between domestic firms and international players. Companies such as Samsung Medison and Sejong Healthcare have developed indigenous ablation solutions tailored for local and export markets.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC ablation devices market profiled in this report are Abbott Laboratories, Boston Scientific Corporation, Medtronic PLC, Conmed Corporation, and Olympus Corporation.

TOP LEADING PLAYERS IN THE MARKET

Abbott Laboratories

Abbott is a leading global player in the ablation devices market and maintains a strong presence across the Asia Pacific region. The company offers a wide portfolio of ablation technologies, including advanced catheters and mapping systems that cater to cardiac and oncological applications. Abbott’s strategic partnerships with regional healthcare providers have enabled it to enhance distribution and improve access to its products.

Boston Scientific Corporation

Boston Scientific is a dominant force in the Asia Pacific ablation devices landscape due to its comprehensive product offerings and strong local partnerships. The company focuses on expanding its footprint through localized manufacturing and tailored solutions for diverse patient populations. Boston Scientific also invests heavily in clinical education programs, ensuring physician readiness and procedural adoption of its ablation technologies.

Medtronic plc

Medtronic plays a pivotal role in shaping the Asia Pacific ablation devices market by offering cutting-edge ablation platforms aimed at treating cardiac arrhythmias and chronic pain. The company’s robust distribution network and collaborations with healthcare institutions support widespread adoption of its technologies. Medtronic emphasizes patient-centric innovation and works closely with regulatory bodies to expedite product approvals in the region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players in the Asia Pacific ablation devices market is product innovation and technology development. Companies are continuously enhancing their portfolios with next-generation ablation systems that offer improved precision, shorter procedure times, and better patient outcomes. This includes integrating AI, robotics, and real-time imaging into existing platforms to meet evolving clinical demands.

Another key approach is strategic collaborations and partnerships with regional distributors, hospitals, and research institutions. These alliances enable companies to expand their reach, navigate complex regulatory landscapes, and accelerate market entry while maintaining compliance and localization standards.

COMPETITION OVERVIEW

The Asia Pacific ablation devices market is characterized by intense competition driven by the presence of established global players and an increasing number of regional manufacturers entering the space. Multinational corporations such as Abbott, Boston Scientific, and Medtronic maintain a dominant position due to their extensive product portfolios, advanced technologies, and strong distribution networks. However, domestic firms in countries like China and India are rapidly gaining traction by offering cost-effective alternatives that cater to price-sensitive segments. The level of innovation and differentiation among products plays a crucial role in shaping competitive advantage, with companies striving to introduce novel platforms that integrate artificial intelligence, enhanced imaging, and robotic assistance. Additionally, regulatory variations across countries present both opportunities and challenges for new entrants, as well as established players seeking to expand their regional footprint. Strategic mergers, acquisitions, and collaborative ventures are increasingly used as tools to consolidate market presence and respond to evolving clinical and commercial demands.

RECENT MARKET DEVELOPMENTS

- In February 2024, Abbott launched a new regional innovation center in Singapore focused on advancing ablation technologies tailored for the Asia Pacific population. This initiative aims to accelerate R&D and bring localized solutions faster to market.

- In June 2023, Boston Scientific expanded its manufacturing facility in Malaysia to increase production capacity for radiofrequency ablation devices and streamline supply chain efficiency across Southeast Asia.

- In November 2023, Medtronic partnered with a leading Indian hospital chain to establish dedicated electrophysiology training centers, which is supporting physician education and improve clinical adoption of ablation procedures in emerging markets.

- In March 2024, Biotronik entered into a distribution agreement with a South Korean medtech firm to broaden its reach in the cardiology segment through enhanced local sales and service capabilities.

- In September 2023, Edwards Lifesciences announced a collaboration with a Japanese diagnostics company to develop integrated imaging systems for use in conjunction with ablation procedures by enhancing procedural accuracy and patient safety.

MARKET SEGMENTATION

This Asia Pacific ablation devices market research report is segmented and sub-segmented into the following categories.

By Device Technology

- Radiofrequency Devices

- Laser/Light Ablation

- Ultrasound Devices

- Cryoablation Devices

- Other Devices

By Application

- Cancer Treatment

- Cardiovascular Disease Treatment

- Ophthalmologic Treatment

- Gynecological Treatment

- Urological Treatment

- Cosmetic Surgery

- Other Applications

By End Users

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC