Asia Pacific Aerospace Avionics Market Research Report – Segmented By Systems Type (Communications Power & data management, Weather detection, Flight management, Electronic flight display, Payload & mission management, Traffic & collision management), Fit Type, & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Asia Pacific Aerospace Avionics Market Size

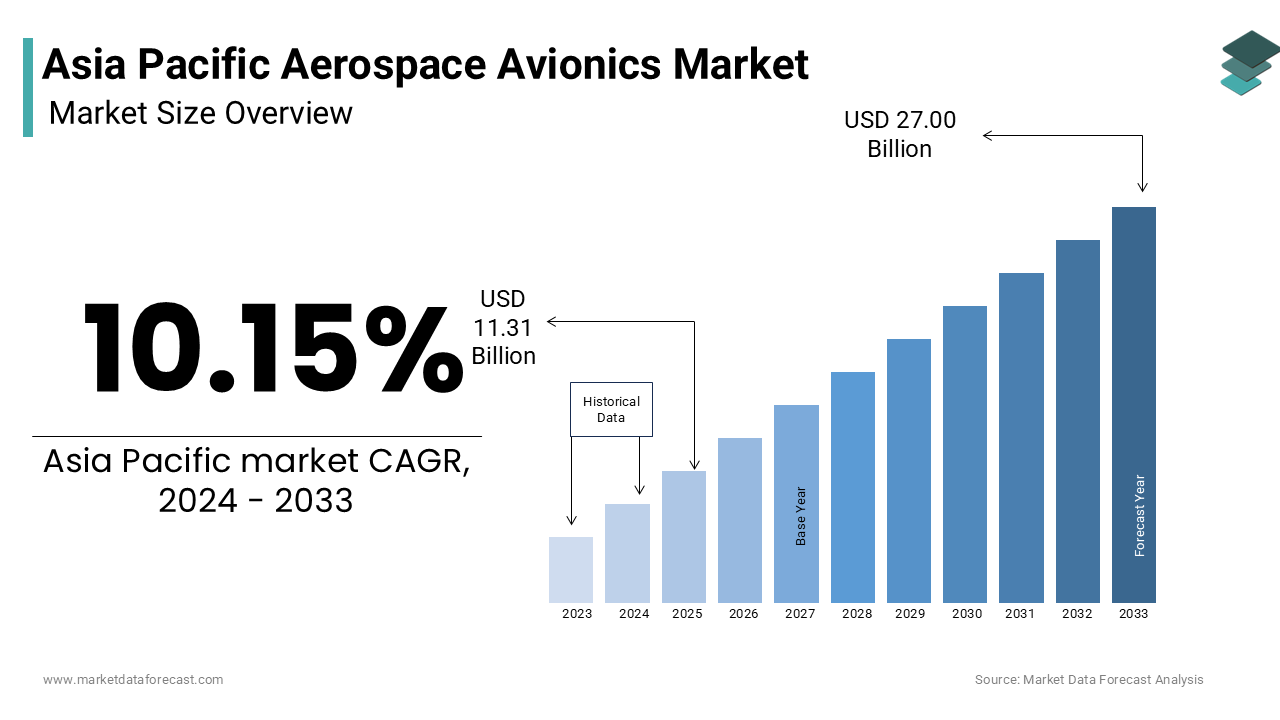

The Asia Pacific aerospace avionics market size was valued at USD 12.46 billion in 2025 and is anticipated to reach USD 13.72 billion in 2026 from USD 29.73 billion by 2034, growing at a CAGR of 10.15% during the forecast period from 2026 to 2034.

The aerospace avionics are ranging from flight management computers and inertial reference units to weather radar and satellite communication terminals. The region hosts more than 3,200 commercial airports, according to the Airports Council International, which is creating a vast operational ecosystem where advanced avionics are essential for managing congestion and ensuring all-weather flight operations. Additionally, the increasing militarization of regional airspace, particularly in the South China Sea and Indo-Pacific, has accelerated the integration of next-generation electronic warfare and secure communication systems in defense platforms.

MARKET DRIVERS

Expansion of Commercial Air Transport Fleets and Fleet Modernization Initiatives

The rising air travel, fleet expansion, and regulatory mandates for upgraded navigation systems is amplifying the growth of the Asia Pacific aerospace avionics market. As per the International Air Transport Association, passenger traffic in the region surpassed 1.4 billion in 2023, recovering to 95% of pre-pandemic levels and surpassing growth rates in other global regions. This surge has prompted airlines to accelerate aircraft deliveries and retrofit older fleets with modern avionics compliant with Performance-Based Navigation (PBN) and Automatic Dependent Surveillance-Broadcast (ADS-B) standards. Additionally, the Civil Aviation Administration of China mandates that all commercial aircraft operating in its airspace be equipped with GBAS (Ground-Based Augmentation Systems)-compatible receivers by 2027.

Rising Defense Modernization and Indigenous Combat Aircraft Programs

The geopolitical landscape in Asia Pacific has triggered a strategic shift toward defense self-reliance, significantly boosting the growth of the Asia Pacific aerospace avionics market. Nations including Japan, India, South Korea, and Australia are investing heavily in next-generation fighter jets, unmanned aerial vehicles (UAVs), and airborne early warning systems, all of which rely on sophisticated electronic systems for situational awareness and combat effectiveness. South Korea’s KF-21 Boramae fighter, which completed its first flight in 2022, incorporates domestically produced mission computers and radar warning receivers, reducing foreign dependency. Additionally, Australia’s Project AIR 7000 Phase 2B involves the procurement of P-8A Poseidon maritime patrol aircraft equipped with advanced signals intelligence (SIGINT) systems.

MARKET RESTRAINTS

Stringent Certification and Regulatory Harmonization Delays

The fragmented regulatory environment to the seamless deployment of aerospace avionics, as differing certification standards delay product integration and increase compliance costs is restricting the growth of the Asia Pacific aerospace avionics market. This delay impedes the adoption of next-generation technologies, particularly in regional airlines and defense contractors reliant on timely upgrades. A 2023 audit by the Comptroller and Auditor General of India revealed that 38% of avionics retrofit projects in public sector airlines faced delays exceeding six months due to certification bottlenecks.

Supply Chain Vulnerabilities and Semiconductor Shortages

The persistent disruptions due to its reliance on a globally concentrated semiconductor supply chain, which has been strained by geopolitical tensions and production imbalances is hampering the growth of the Asia Pacific aerospace avionics market. Avionics systems require specialized microprocessors, field-programmable gate arrays (FPGAs), and radiation-hardened chips, many of which are manufactured in the United States, Taiwan, and Germany. As per the Semiconductor Industry Association, global shortages of aerospace-grade semiconductors persisted through 2023, with lead times extending beyond 52 weeks for components like analog-to-digital converters and memory modules. Similarly, India’s HAL experienced production halts in the Su-30MKI fleet upgrade program because of delayed deliveries of Israeli-made radar processing units, according to the Ministry of Defence.

MARKET OPPORTUNITIES

Growth of Unmanned Aerial Systems (UAS) and Urban Air Mobility (UAM)

The rapid development of unmanned aerial systems and urban air mobility platforms is greatly influencing the growth of the Asia Pacific aerospace avionics market. India’s Drone Rules 2021 have spurred the development of indigenous UAVs like the Rustom and Tapas, equipped with domestically produced avionics by DRDO and BEL. Additionally, Australia’s Civil Aviation Safety Authority has approved beyond visual line of sight (BVLOS) operations for emergency medical drones on advanced avionics compliance.

Regional Airspace Modernization and CNS/ATM Infrastructure Development

The ongoing modernization of communication, navigation, and surveillance/air traffic management (CNS/ATM) infrastructure is creating new opportunities for the growth of the Asia Pacific aerospace avionics market. As per the International Civil Aviation Organization, only 55% of flights in the region currently operate under PBN procedures, far below the 85% target set for 2030, necessitating widespread avionics upgrades. Southeast Asian nations are collaborating under the ASEAN Single Aviation Market to harmonize airspace procedures, driving adoption of common avionics standards.

MARKET CHALLENGES

Cybersecurity Threats to Avionics Systems in Connected Aircraft

The increasing digitization and connectivity of avionics systems expose aircraft to growing cybersecurity risks for manufacturers and operator is declining the growth of the Asia Pacific aerospace avionics market. Modern aircraft rely on integrated networks such as the Aircraft Communications Addressing and Reporting System (ACARS) and Internet Protocol-based data links, which, while enhancing operational efficiency, create potential entry points for cyber intrusions. As per a 2023 report by the Asia Pacific Risk Centre, there was a 240% increase in attempted cyberattacks on aviation networks in the region between 2020 and 2023, including probing of onboard maintenance and flight control systems. The integration of passenger Wi-Fi with avionics networks, even through isolated gateways, raises concerns about lateral movement by malicious actors.

High Costs and Long Development Cycles for Avionics Integration

The financial and temporal burden associated with avionics development and certification for regional manufacturers and defense integrators is also to degrade the growth of the Asia Pacific aerospace avionics market. The complexity of integrating multiple subsystems such as radar, electronic warfare, and communication modules into a unified architecture demands extensive simulation, ground testing, and flight validation, prolonging time-to-market. Additionally, the need for redundancy, fault tolerance, and compliance with DO-254 (hardware) and DO-178C (software) standards significantly increases engineering effort. Smaller firms in Southeast Asia often lack the capital and technical expertise to navigate these requirements, limiting innovation. As per a 2023 McKinsey analysis, nearly 60% of avionics projects in the region exceed their initial budget by at least 35%, primarily due to integration delays and certification rework. These barriers hinder the emergence of competitive domestic suppliers and reinforce reliance on foreign technology, constraining the region’s ability to achieve true technological sovereignty in aerospace electronics.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 10.15% |

| Segments Covered | By Systems Type, Fit Type and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the rest of APAC. |

| Market Leaders Profiled | Honeywell International Inc., L3Harris Technologies, Inc., Collins Aerospace (RTX Corporation), Thales Group, Safran, Cobham Limited, Panasonic Avionics Corporation, Elbit Systems Ltd., Diehl Stiftung & Co. KG, Garmin Ltd., and Northrop Grumman Corporation |

SEGMENTAL ANALYSIS

By Systems Insights

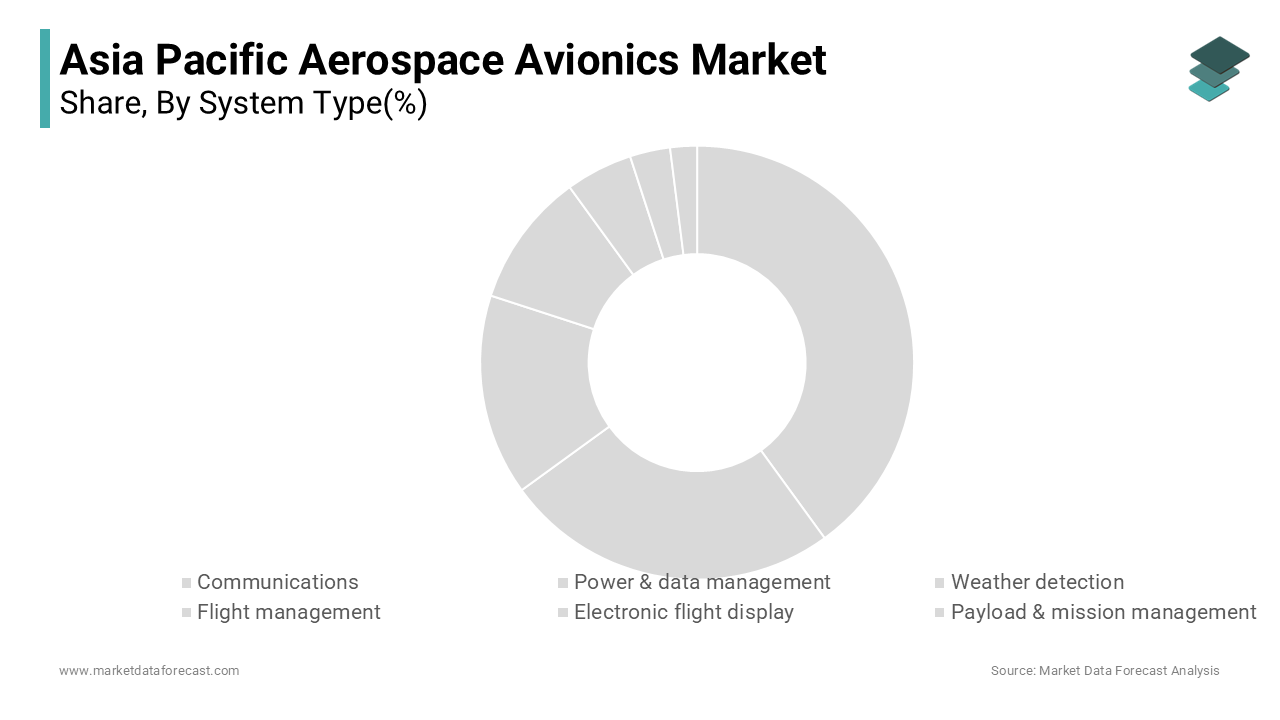

The flight management system (FMS) segment was accounted in holding 24.3% of the Asia Pacific aerospace avionics market share in 2025 with the central computational hub for navigation, performance optimization, and flight planning in both commercial and military aircraft. An FMS integrates data from GPS, inertial reference systems, and air data computers to calculate optimal flight paths, reducing fuel consumption and ensuring compliance with airspace regulations. In long-haul operations across the Pacific, where flight efficiency directly impacts profitability, advanced FMS platforms such as Honeywell’s EASy III and Collins Aerospace’s Pro Line Fusion are standard in new Airbus and Boeing deliveries. In India, the implementation of the GAGAN satellite-based augmentation system necessitates FMS upgrades for precision approaches at 200+ airports, as confirmed by the Airports Authority of India.

The electronic flight display (EFD) segment is likely to grow with a CAGR of 9.8% in the next coming years with the widespread transition from analog instrumentation to glass cockpits, which enhance situational awareness and reduce pilot workload. Modern EFDs, such as primary flight displays (PFDs) and multi-function displays (MFDs), consolidate flight data into intuitive digital interfaces, a necessity in increasingly congested Asian airspace.

By Platform Insights

The commercial aviation segment held a prominent share of the Asia Pacific aerospace avionics market in 2025 with passenger traffic recovering to 95% of pre-pandemic levels by the end of 2023. Airlines across China, India, and Southeast Asia are expanding fleets to meet rising demand, with over 4,500 new aircraft deliveries expected by 2035, as projected in Airbus’s Asia Pacific Market Forecast. China Southern Airlines and IndiGo Asia’s largest carriers by fleet size are in the process of integrating over 300 new narrow-body jets, each requiring advanced avionics compliant with Performance-Based Navigation (PBN) and Automatic Dependent Surveillance-Broadcast (ADS-B) standards. Additionally, the expansion of low-cost carriers in Indonesia, Vietnam, and the Philippines has accelerated the induction of modern, digitally integrated aircraft like the Airbus A320neo and Boeing 737 MAX.

The military aviation segment is expected to grow with a CAGR of 10.3% in the next coming years by escalating geopolitical tensions, territorial disputes, and national defense modernization programs across the Indo-Pacific. Additionally, the proliferation of unmanned combat aerial vehicles (UCAVs) such as India’s Rustom-2 and China’s CH-5 has created demand for compact, high-reliability avionics for autonomous navigation and payload control.

By Fit Insights

The line-fit segment was the largest and held 58.3% of the Asia Pacific aerospace avionics market share in 2025 with the region’s robust aircraft delivery pipeline and the integration of avionics during original equipment manufacturing, ensuring compliance with airline specifications and regulatory standards from inception. Similarly, IndiGo’s record order of 500 Airbus A320neo aircraft includes full line-fit avionics packages compliant with Indian DGCA and EASA standards. The advantage of line-fit lies in system integration efficiency; factory-installed avionics undergo rigorous testing and certification, reducing post-delivery modifications. Additionally, airlines prefer line-fit solutions to ensure uniformity across fleets, simplifying maintenance and pilot training.

The retrofit segment is expected to grow with a CAGR of 9.6% from 2026 to 2034 with regulatory mandates, fleet modernization, and the need to extend the operational life of aging aircraft. Many airlines in the region operate fleets with average ages exceeding 10 years in Indonesia, the Philippines, and India, where cost constraints delay fleet renewal.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific aerospace avionics market with 32.3% of share in 2025 with its dual strategy of commercial fleet expansion and indigenous technological development. Additionally, the COMAC C919 program, which entered commercial service in 2023, features a full avionics suite co-developed with Honeywell and Rockwell Collins, marking a shift toward technology transfer and localized integration. The People’s Liberation Army Air Force is modernizing its fleet with J-20 stealth fighters and Y-20 transport aircraft, both equipped with advanced AESA radars and electronic warfare systems.

India was positioned second 19.3% of the Asia Pacific aerospace avionics market share in 2025 with a confluence of civil aviation expansion, defense indigenization, and strategic infrastructure development. IndiGo, the largest airline in Asia by fleet size, operates over 300 aircraft, all requiring modern avionics, while Air India’s fleet renewal program includes 400 new aircraft orders. The UDAN scheme has spurred the induction of regional aircraft, each needing certified navigation and communication systems.

Japan aerospace avionics market is expected to grow at highest CAGR during the forecast period with the technological sophistication, regulatory rigor, and a strong defense-industrial base. Japanese airlines such as ANA and Japan Airlines operate some of the most modern fleets globally, with over 90% of aircraft equipped with glass cockpits and satellite communication systems. The Ministry of Land, Infrastructure, Transport and Tourism mandates that all aircraft flying in Japanese airspace comply with PBN and ADS-B standards by ensuring continuous demand for upgraded avionics. Mitsubishi Heavy Industries’ involvement in the F-35 program includes final assembly and avionics integration for Japanese and international variants, which is enhancing domestic technical capability.

Australia aerospace avionics market is expected to grow steadily in the next coming years. The country’s position is defined by its strategic role in regional defense, advanced air traffic management, and support for next-generation aviation technologies. As a Tier 1 partner in the F-35 program, Australia has integrated advanced avionics into its fleet of 72 stealth fighters, with ongoing upgrades to mission computers and electronic warfare systems. The Royal Australian Air Force operates E-7A Wedgetail airborne early warning aircraft, each equipped with Northrop Grumman’s multi-role electronic scanning array radar, one of the most sophisticated avionics systems in the region. The country also hosts major MRO facilities in Brisbane and Melbourne, serving regional airlines and defense contractors.

South Korea aerospace avionics market is expected to be driven by the defense modernization, technological innovation, and in global aerospace supply chains. The country is also a key manufacturing hub for Boeing, producing wing components and avionics enclosures for the 787 Dreamliner. Hyundai’s Supernal is developing urban air mobility vehicles with fully digital cockpits, requiring compact, high-reliability avionics. Additionally, the government’s “Smart Air Mobility” initiative includes testbeds in Seoul and Incheon for autonomous flight operations.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Asia Pacific Aerospace Avionics Market include

- Honeywell International Inc.

- L3Harris Technologies, Inc.

- Collins Aerospace (RTX Corporation)

- Thales Group

- Safran

- Cobham Limited

- Panasonic Avionics Corporation

- Elbit Systems Ltd.

- Diehl Stiftung & Co. KG

- Garmin Ltd.

- Northrop Grumman Corporation

COMPETITIVE LANDSCAPE

The competitive dynamics of the Asia Pacific aerospace avionics market are defined by a strategic interplay between global technology leaders and emerging regional players seeking to capitalize on defense autonomy and civil aviation growth. Multinational corporations such as Honeywell, Collins Aerospace, and Thales dominate through technological superiority, OEM partnerships, and extensive support networks, particularly in high-value commercial and military programs. Their integration into platforms like the F-35, COMAC C919, and Airbus A320neo provides deep market entrenchment. However, national champions in India, Japan, South Korea, and China are gaining traction by leveraging government-backed indigenization initiatives to develop sovereign avionics capabilities. Competition is further intensified by the rise of MRO providers and aerospace startups focusing on niche applications such as UAV avionics and digital retrofits. The market is also witnessing a shift from product-centric sales to performance-based service models, including pay-per-flight and health monitoring contracts. Geopolitical factors influence procurement decisions, with countries favoring suppliers that offer technology transfer and local manufacturing. As regulatory mandates for airspace modernization drive retrofit demand, competition is expanding beyond hardware to include software, cybersecurity, and data integration. This evolving landscape fosters collaboration, innovation, and strategic positioning, making the region one of the most dynamic and contested avionics markets globally.

Top Players in the Market

Honeywell Aerospace is a top most player in the Asia Pacific aerospace avionics market through its advanced flight management, navigation, and connectivity solutions integrated across commercial, business, and military aircraft. The company supplies core avionics systems for platforms such as the COMAC C919, Mitsubishi SpaceJet, and various Airbus and Boeing models operated by regional carriers. In 2023, Honeywell expanded its engineering center in Bengaluru, India, to accelerate the development of satellite communication terminals tailored for Asian airspace requirements.

Collins Aerospace, a Raytheon Technologies company, plays a role in shaping avionics integration across Asia Pacific through its comprehensive suite of flight control, communication, and display systems. Its Pro Line and Primus Epic avionics are widely deployed in business jets, regional aircraft, and military platforms operated in Japan, Australia, and India. In 2022, Collins secured a major contract with Japan’s Ministry of Defense to support F-35 avionics sustainment, reinforcing its position in defense logistics. The company also launched a digital cockpit upgrade program for Indian regional airlines in collaboration with HAL, enabling compliance with GAGAN and ADS-B mandates.

Thales Group has established a strong foothold in the Asia Pacific avionics landscape by delivering secure communication, navigation, and mission systems for civil and military operators. Its FlytX avionics suite is integrated into the Airbus A320neo family flown by major carriers such as Singapore Airlines and IndiGo, while its AVIONICS 2020 suite supports modernization programs in India and Australia. In 2023, Thales collaborated with the Indian Air Force to upgrade avionics in MiG-29 and Mirage 2000 fleets, enhancing combat capability through digital cockpit retrofits. The company also partnered with Sydney-based Fleet Space Technologies to explore secure satellite data links for unmanned systems.

Top Strategies Used by the Key Market Participants

Leading players in the Asia Pacific aerospace avionics market are deploying strategic initiatives centered on technological innovation, regional partnerships, and lifecycle support to their positions. A primary focus is on developing integrated modular avionics (IMA) architectures that enhance scalability and reduce weight, aligning with the region’s demand for fuel-efficient and digitally connected aircraft. Companies are investing in indigenous R&D centers in India, China, and Singapore to co-develop systems with local OEMs and comply with national defense indigenization policies. Strategic joint ventures and technology transfer agreements such as those between global firms and entities like HAL, KAI, and COMAC are enabling localized production and certification, accelerating market access. To address regulatory complexity, manufacturers are aligning product development with regional CNS/ATM mandates, including GAGAN, ADS-B, and OneSKY, ensuring compliance from design inception. Expansion of MRO and retrofit services through regional service hubs in Malaysia, Australia, and Thailand is enhancing after-sales support and customer retention. Digital transformation is another key thrust, with firms integrating predictive maintenance algorithms and secure data links into avionics platforms. Additionally, participation in urban air mobility and unmanned system programs is opening new revenue streams.

RECENT MARKET DEVELOPMENTS

- In June 2022, Honeywell Aerospace expanded its research and development center in Bengaluru, India, to focus on satellite communication and navigation systems for regional aircraft by enhancing its support for GAGAN-enabled flight operations and strengthening its presence in South Asia’s growing MRO sector.

- In September 2022, Collins Aerospace secured a multi-year contract with Japan’s Ministry of Defense to provide sustainment and technical support for F-35 fighter jet avionics with its role in defense electronics and deepening its integration into Japan’s national security infrastructure.

- In March 2023, Thales Group partnered with the Indian Air Force to modernize avionics in MiG-29 and Mirage 2000 fighter fleets by delivering digital cockpit retrofits with enhanced situational awareness systems, thereby expanding its footprint in India’s military modernization programs.

- In November 2023, Collins Aerospace inaugurated a new avionics testing and certification facility in Singapore, designed to support OEMs and MRO providers across Southeast Asia with faster turnaround times and compliance with regional airworthiness standards.

- In May 2025, Honeywell launched a joint development program with COMAC to optimize avionics integration for the C919 aircraft, focusing on flight management and connectivity systems tailored for Asian airspace with its strategic partnership in China’s commercial aviation ambitions.

MARKET SEGMENTATION

This research report on the Asia Pacific Aerospace Avionics Market is segmented and sub-segmented into the following categories.

By Systems Type

- Communications

- Power & data management

- Weather detection

- Flight management

- Electronic flight display

- Payload & mission management

- Traffic & collision management

By Fit Type

- Line-fit

- Retro-fit

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

Who are the key market players in the Asia Pacific Aerospace Avionics Market?

Key players include Honeywell International Inc., L3Harris Technologies, Collins Aerospace, Thales Group, Safran, Cobham Limited, Panasonic Avionics, Elbit Systems Ltd., Diehl Stiftung & Co. KG, Garmin Ltd., and Northrop Grumman Corporation.

Which countries are part of the Asia Pacific Aerospace Avionics Market?

The market covers China, Japan, India, South Korea, Australia, and the rest of Asia Pacific.

What factors are driving the growth of the Asia Pacific Aerospace Avionics Market?

Growth drivers include rising air passenger traffic, fleet expansion, advancements in avionics technology, and the increasing adoption of unmanned aircraft systems.

What challenges does the Asia Pacific Aerospace Avionics Market face?

Key challenges include high development costs, stringent regulatory standards, and cybersecurity concerns in digital avionics systems.

How does the demand for unmanned aircraft systems impact the market?

The growing use of unmanned aircraft systems for defense and commercial applications is significantly boosting the avionics demand in the region.

What future opportunities exist in the Asia Pacific Aerospace Avionics Market?

Opportunities lie in next-generation avionics integration for electric aircraft, urban air mobility, and advanced unmanned aircraft systems.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com