- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

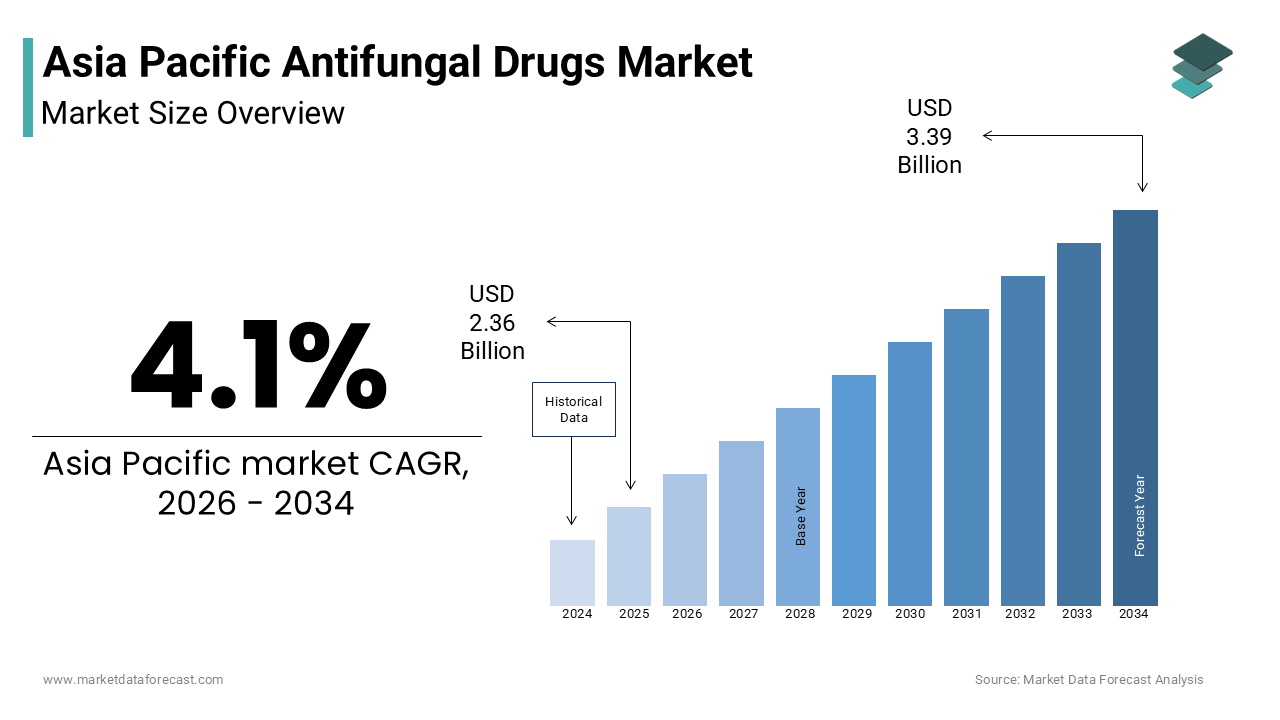

Market Size, 2025

$2.36 BnMarket Estimate, 2026

$2.46 BnMarket Forecast, 2034

$3.39 BnCAGR, 2026–2034

4.1%Asia Pacific Antifungal Drugs Market Report Summary

The Asia Pacific antifungal drugs market was valued at USD 2.36 billion in 2025, is estimated to reach USD 2.46 billion in 2026, and is projected to reach USD 3.39 billion by 2034, growing at a CAGR of 4.1% during the forecast period from 2026 to 2034. The growth of the Asia Pacific antifungal drugs market is driven by the rising prevalence of fungal infections supported by tropical climatic conditions, increasing cases of diabetes and immunocompromised populations, and expanding healthcare infrastructure. Additionally, the growing incidence of hospital-acquired infections and increasing awareness regarding fungal disease diagnosis and treatment are further contributing to market expansion. Government initiatives to improve access to essential medicines and advancements in antifungal therapies are also supporting sustained growth across the region.

Key Market Trends

- Rising demand for systemic antifungal therapies due to increasing invasive fungal infections.

- Growing focus on novel antifungal drug development to address drug resistance issues.

- Increasing adoption of advanced formulations with improved safety and efficacy profiles.

- Expansion of healthcare infrastructure and insurance coverage improving treatment accessibility.

- Rising awareness of fungal infections and early diagnosis across emerging economies.

Segmental Insights

- Based on drug type, the azoles segment was the largest and held a significant share of the Asia Pacific antifungal drugs market in 2025. The segment’s dominance is attributed to its broad-spectrum activity, cost-effectiveness, and widespread use in treating both superficial and systemic fungal infections.

- The echinocandins segment is projected to witness the fastest growth during the forecast period. The growth of this segment is driven by increasing antifungal resistance and the need for effective treatments against severe invasive infections.

- Based on therapeutic indications, the candidiasis segment was the largest, occupying a prominent share of the Asia Pacific antifungal drugs market in 2025. The dominance of this segment stems from the high prevalence of Candida infections among diabetic and immunocompromised populations.

- The aspergillosis segment is expected to grow at the fastest rate, supported by increasing cancer cases, organ transplants, and rising awareness of invasive fungal infections.

- Based on application, the ointments segment accounted for the largest share due to the high prevalence of superficial fungal infections and preference for topical treatments.

- The drugs (systemic therapy) segment is projected to grow rapidly, driven by the increasing incidence of severe and invasive fungal infections requiring oral or intravenous treatment.

Regional Insights

The Asia Pacific antifungal drugs market is witnessing steady growth across major countries, supported by increasing disease burden, improving healthcare systems, and rising awareness.

- China was the largest contributor, driven by a large patient population, increasing hospital infrastructure, and rising prevalence of fungal infections linked to diabetes.

- India holds a significant share, supported by widespread use of low-cost generic antifungals and a high incidence of dermatophytosis and other fungal infections.

- Japan continues to perform strongly, fueled by an aging population, advanced healthcare infrastructure, and high adoption of innovative antifungal therapies.

- South Korea is witnessing notable growth, driven by increasing cancer cases, strong healthcare systems, and high adoption of advanced treatments.

- Australia also maintains steady growth, supported by strong regulatory frameworks, high healthcare awareness, and increasing incidence of invasive fungal infections.

Competitive Landscape

The Asia Pacific antifungal drugs market is highly competitive, characterized by the presence of global pharmaceutical companies and strong regional generic manufacturers. Leading players focus on innovation, development of new drug classes, and improving formulations to address antifungal resistance. Strategic collaborations, expansion of distribution networks, and investments in research and development are key strategies adopted by companies to strengthen their market position. Additionally, increasing emphasis on affordability, regulatory compliance, and physician education is shaping the competitive landscape. Prominent players in the Asia Pacific antifungal drugs market include Pfizer, Novartis, Sanofi-Aventis, Merck & Co., Bayer Healthcare, Gilead Sciences, GlaxoSmithKline, Abbott Laboratories, and Cipla Limited.

Asia Pacific Antifungal Drugs Market Size

The Asia Pacific antifungal drugs market size was valued at USD 2.36 billion in 2025 and is anticipated to reach USD 2.46 billion in 2026 from USD 3.39 billion by 2034, growing at a CAGR of 4.1% during the forecast period from 2026 to 2034

Antifungal drugs encompass a diverse range of pharmaceutical agents designed to treat fungal infections affecting the skin, nails, and internal organs. These therapeutics are critical for managing conditions ranging from superficial dermatophytosis to life-threatening invasive fungal diseases in immunocompromised patients. The region faces a unique epidemiological landscape characterized by high humidity and tropical climates which foster fungal proliferation. According to the World Health Organization, fungal infections affect more than 1 billion people globally, with a significant burden concentrated in tropical and subtropical regions of Asia. The prevalence of underlying conditions such as diabetes and HIV further exacerbates susceptibility. As per the International Diabetes Federation, there were approximately 206 million adults living with diabetes in the Western Pacific region in 2021, creating a vast population at risk for chronic fungal complications like candidiasis and onychomycosis. Furthermore, the rising incidence of hospital-acquired infections in expanding healthcare systems contributes to the demand for systemic antifungals. According to the United Nations Department of Economic and Social Affairs, the number of people aged 60 or over in Asia is expected to reach 1.3 billion by 2050, increasing the pool of individuals with weakened immune systems. Government initiatives to improve diagnostic capabilities and access to essential medicines are also shaping the market. As healthcare infrastructure develops across emerging economies, the recognition and treatment of fungal pathogens are becoming prioritized. This convergence of climatic, demographic, and clinical factors establishes a robust foundation for the expansion of antifungal therapies throughout the Asia Pacific region.

MARKET DRIVERS

High Prevalence of Diabetes and Immunocompromised States

The escalating prevalence of diabetes mellitus and other immune-compromising conditions is one of the major factors propelling the growth of the Asia-Pacific antifungal drugs market. Patients with diabetes are significantly more susceptible to fungal infections due to impaired immune responses and higher glucose levels in tissues that promote fungal growth. According to the International Diabetes Federation, the number of adults with diabetes in the Western Pacific Region is projected to rise to 260 million by 2045. This massive patient pool creates a sustained demand for both topical and systemic antifungal treatments for conditions such as vulvovaginal candidiasis, oral thrush, and diabetic foot infections. Additionally, the rising incidence of HIV in certain parts of Southeast Asia contributes to the burden of opportunistic fungal infections. As per the World Health Organization, there were approximately 6.5 million people living with HIV in the Asia Pacific region in 2022. These individuals frequently require prophylactic and therapeutic antifungal interventions to manage infections like pneumocystis pneumonia and cryptococcal meningitis. The growing number of organ transplant recipients and cancer patients undergoing chemotherapy further expands the vulnerable population. These clinical realities necessitate consistent and often long-term use of antifungal medications. As healthcare systems in countries like India, China, and Indonesia improve diagnosis rates for these underlying conditions, the prescription volume for antifungal agents continues to rise. This demographic and clinical trend ensures a steady growth trajectory for the market.

Tropical Climate and Environmental Factors Favoring Fungal Growth

The distinctive tropical and subtropical climate prevalent across much of the Asia Pacific region creates an ideal environment for the proliferation of pathogenic fungi, which is driving high incidence rates of fungal infections and driving the regional market expansion. High temperatures and humidity levels facilitate the survival and transmission of dermatophytes, yeasts, and molds. According to the Lancet Planetary Health, rising global temperatures are expanding the suitable habitat for fungal pathogens, exposing new populations to infection risks. In countries such as Thailand, Vietnam, and the Philippines, superficial fungal infections like tinea pedis, tinea cruris, and cutaneous candidiasis are endemic. The warm and moist conditions encourage fungal colonization on the skin and nails, leading to chronic and recurrent infections that require prolonged treatment. Agricultural practices in rural areas also expose workers to soil-borne fungi such as Aspergillus and Fusarium, increasing the risk of invasive diseases. As per the World Health Organization, environmental factors such as high humidity and poor sanitation play a crucial role in the epidemiology of fungal diseases in tropical regions. Urbanization and crowded living conditions in rapidly growing cities further facilitate the spread of contagious fungal infections. Public health data from these regions consistently show higher consultation rates for dermatological issues compared to temperate zones. This environmental predisposition ensures a baseline demand for over-the-counter and prescription antifungal products. As urban density increases and climate patterns shift, the burden of fungal diseases is likely to intensify, which is sustaining market growth.

MARKET RESTRAINTS

Emergence of Antifungal Drug Resistance

The increasing emergence of resistance to commonly used antifungal agents poses a significant restraint on the effectiveness and market growth of existing therapies in the Asia Pacific region. Overuse and misuse of azoles, particularly in agriculture and empirical clinical practice, have accelerated the development of resistant strains such as Candida auris and Aspergillus fumigatus. According to the World Health Organization, antifungal resistance is a growing global concern, with Candida auris identified as a high-priority pathogen due to its multi-drug resistance. This pathogen is difficult to identify and treat, leading to higher mortality rates and prolonged hospital stays. In India, as per studies published in medical journals, fluconazole resistance among Candida isolates has been reported at rates exceeding 20% in some clinical settings, limiting treatment options for invasive candidiasis. The lack of rapid diagnostic tools often leads to inappropriate empirical prescribing, which further exacerbates resistance patterns. Healthcare providers face challenges in selecting effective therapies, resulting in treatment failures and increased healthcare costs. The pipeline for new classes of antifungal drugs is limited compared to antibiotics, leaving few alternatives for resistant infections. Regulatory bodies are struggling to implement strict stewardship programs to curb misuse. This growing resistance crisis undermines confidence in existing treatments and necessitates costly research and development efforts. Until new mechanisms of action are introduced and stewardship is improved, resistance will remain a critical barrier to market expansion.

Limited Diagnostic Capabilities in Rural Areas

The lack of advanced diagnostic infrastructure in rural and underserved areas of the Asia Pacific region significantly hinders the accurate identification and treatment of fungal infections. Many healthcare facilities in remote parts of countries like Indonesia, Papua New Guinea, and rural India lack access to microbiological laboratories capable of performing fungal cultures and sensitivity testing. According to the World Health Organization, only about 19% of people in low-and-middle-income countries have access to basic diagnostic testing. Without precise diagnosis, clinicians often rely on empirical treatment, which may be ineffective against specific fungal species. This leads to delayed appropriate therapy, prolonged illness, and increased risk of complications. The inability to distinguish between bacterial and fungal infections results in the inappropriate use of antibiotics or antifungals, contributing to resistance. Patients in these areas often present with advanced stages of invasive fungal diseases, which are more difficult and expensive to treat. The absence of point-of-care diagnostic tests for fungal pathogens means that many cases go unreported or misdiagnosed. This diagnostic gap limits the market potential for newer and more specialized antifungal agents which require confirmed indications for prescription. Governments and non-governmental organizations are working to improve laboratory networks, but progress is slow. Until diagnostic accessibility improves, a significant portion of the population will remain underserved, restricting market penetration.

MARKET OPPORTUNITIES

Development of Novel Antifungal Agents and Formulations

The urgent need for effective treatments against resistant fungal strains presents a lucrative opportunity for the development of novel antifungal agents and innovative drug delivery systems in the Asia Pacific market. Pharmaceutical companies are investing in research to discover new classes of antifungals with unique mechanisms of action such as fosmanogepix and ibrexafungerp. According to the Global Action Fund for Fungal Infections, the limited number of current antifungal classes just four main groups highlights the significant unmet medical need for new agents. New formulations such as lipid-based amphotericin B and echinocandins offer improved safety profiles and efficacy for invasive infections. In Japan and South Korea, strong regulatory support for orphan drugs and innovative therapies encourages the approval of these new agents. The rising burden of rare and resistant fungal infections drives demand for these advanced treatments. Additionally, the development of topical formulations with better penetration and longer duration of action offers opportunities in the superficial segment. Companies that can demonstrate superior efficacy and safety in clinical trials will gain competitive advantage. Collaborations between academic institutions and biotech firms in the region are accelerating drug discovery. As patent expiries of older drugs occur, the introduction of next-generation therapies will capture market share. This innovation pipeline provides a pathway for sustained growth and improved patient outcomes.

Expansion of Healthcare Infrastructure and Insurance Coverage

The ongoing expansion of healthcare infrastructure and the broadening of health insurance coverage in emerging Asia Pacific economies offer significant opportunities for the antifungal drugs market. Governments in countries like China, India, and Thailand are implementing universal health coverage schemes that include essential medicines such as antifungals. According to the World Bank, health expenditure per capita in East Asia and the Pacific has more than doubled over the last two decades, improving general access to medical care. The establishment of new hospitals and clinics in tier 2 and tier 3 cities brings diagnostic and treatment capabilities closer to patients. This decentralization of healthcare services increases the detection and treatment rates of fungal infections. Private insurance providers are also expanding their formularies to cover branded and generic antifungal agents. The inclusion of newer and more expensive antifungals in reimbursement lists reduces out-of-pocket expenses for patients. In Australia and New Zealand, robust pharmaceutical benefits schemes ensure affordable access to advanced therapies. As financial barriers decrease, the utilization of prescribed antifungal medications rises. Manufacturers can leverage these policy changes to introduce premium products into previously inaccessible markets. The formalization of healthcare delivery systems creates a structured channel for distribution and sales, driving market expansion.

MARKET CHALLENGES

High Cost of Advanced Antifungal Therapies

The prohibitive cost of newer and advanced antifungal therapies acts as a major challenge to their widespread adoption in the Asia Pacific region, particularly in low-and-middle-income countries. Drugs such as echinocandins and lipid formulations of amphotericin B are significantly more expensive than conventional azoles. According to the World Health Organization, the cost of liposomal amphotericin B remains a major barrier to the treatment of serious infections like cryptococcal meningitis in developing regions. In countries with limited healthcare budgets such as Vietnam and the Philippines, these costs are often borne by patients out-of-pocket. This financial burden restricts access to life-saving treatments for invasive fungal infections, which have high mortality rates if untreated. Public hospitals often face budget constraints that limit the procurement of expensive antifungals, leading to rationing or reliance on less effective alternatives. The lack of comprehensive insurance coverage for newer agents further exacerbates affordability issues. Healthcare providers are forced to make difficult decisions regarding resource allocation, potentially compromising patient care. The economic disparity between urban and rural areas means that advanced therapies are largely accessible only to affluent populations. This inequity hinders the overall market potential for premium antifungal products. Until pricing strategies are adjusted or subsidies are introduced, the high cost will remain a significant barrier to equitable access and market growth.

Regulatory Hurdles and Approval Delays

Navigating the complex and heterogeneous regulatory landscapes across the Asia Pacific region presents a formidable challenge for manufacturers of antifungal drugs. Each country has distinct requirements for clinical trials, registration, and post-marketing surveillance, which complicates the approval process. According to the Asian Harmonization Working Party, varying technical requirements and review timelines across member economies can delay the availability of new medicines. For instance, obtaining approval in China through the National Medical Products Administration may require local clinical trials even if global data is available. This requirement increases the time and cost of market entry. In smaller markets like Laos and Cambodia, regulatory frameworks are less established, leading to unpredictable approval timelines. The lack of mutual recognition agreements means that approvals in one country do not automatically translate to others. Small and medium-sized enterprises often lack the resources to manage these diverse regulatory pathways effectively. Furthermore, frequent changes in regulatory policies create uncertainty for long-term planning. The delay in launching new antifungal agents means that patients in the region may wait years longer than those in Europe or North America for access to innovative treatments. These regulatory inefficiencies slow down the dissemination of critical therapies and hinder market expansion. Until greater regulatory convergence is achieved, manufacturers will continue to face significant obstacles.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.1%. |

| Segments Covered | By Drug Type, Therapeutic Indications, Application and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the Rest of Asia Pacific. |

| Market Leaders Profiled | Alternaria, Pfizer, Novartis, Sanofi-Aventis, Merck & Co., Aspergillus, Kramer Laboratories, Bayer Healthcare, Enzon Pharmaceuticals, Glaxosmithkline Gilead, and Abbott Laboratories. |

SEGMENTAL ANALYSIS

By Drug Type Insights

The azoles segment dominated the Asia Pacific antifungal drugs market by accounting for the 46.4% of the regional market share in 2025. The dominance of azoles segment in the Asia-Pacific market is attributed to the broad spectrum of activity, efficacy against a wide range of fungal pathogens, and the availability of both topical and systemic formulations. Azoles including fluconazole, itraconazole, voriconazole, and posaconazole are the cornerstone of antifungal therapy due to their ability to treat both superficial and invasive fungal infections. According to the World Health Organization, several azoles are included in the Model List of Essential Medicines for the treatment of various fungal infections common in Asia. The oral bioavailability of many azoles allows for effective outpatient management, reducing the need for hospitalization. In countries like India and China, where healthcare costs are a significant concern, the availability of generic azoles makes them the preferred choice for physicians and patients. Fluconazole remains the first-line treatment for vulvovaginal candidiasis affecting millions of women annually. The extensive clinical experience and established safety profile of azoles further reinforce their dominance. Physicians are comfortable prescribing these agents for empirical therapy while awaiting diagnostic results. The wide range of indications, from dermatophytosis to invasive candidiasis, ensures high prescription volumes. As the burden of fungal infections rises with increasing diabetes rates, the demand for versatile and affordable azole therapies continues to grow, solidifying their market leadership.

However, the echinocandins segment is anticipated to record the highest CAGR of 12.2% over the forecast period owing to the rising incidence of invasive candidiasis and the need for effective treatments against azole-resistant strains. The emergence of azole-resistant Candida species, particularly Candida glabrata and Candida krusei, has shifted clinical preference towards echinocandins such as caspofungin, micafungin, and anidulafungin. As per the World Health Organization, rising resistance to first-line antifungal agents is a critical driver for the use of alternative classes like echinocandins in intensive care settings. Echinocandins work by inhibiting beta-glucan synthesis in the fungal cell wall, a mechanism distinct from azoles, making them effective against resistant strains. In hospitals across Japan, South Korea, and Australia, echinocandins are increasingly recommended as first-line therapy for invasive candidiasis in critically ill patients. The superior safety profile and lack of significant drug-drug interactions compared to azoles make them ideal for complex patients on multiple medications. Clinical guidelines from infectious disease societies support the use of echinocandins for moderate-to-severe candidiasis. As awareness of resistance patterns grows among clinicians in the Asia Pacific region, the adoption of echinocandins accelerates. The ability to save lives in severe cases justifies the higher cost, leading to increased procurement in tertiary care centers. This clinical necessity drives the rapid growth of the echinocandin segment.

By Therapeutic Indications Insights

The candidiasis segment led the market by capturing 41.9% of the Asia-Pacific market share in 2025 due to the high prevalence of Candida infections in both community and hospital settings and the wide range of affected patient populations. Candidiasis is highly prevalent among individuals with diabetes mellitus and immunocompromised conditions, which are widespread in the Asia Pacific region. According to the International Diabetes Federation, there were approximately 206 million adults living with diabetes in the Western Pacific region in 2021, providing a large population at risk for candidiasis. High blood sugar levels promote fungal growth, leading to recurrent vulvovaginal and oral candidiasis. Additionally, the rising number of HIV patients and organ transplant recipients increases the susceptibility to invasive candidiasis. As per the World Health Organization, candidiasis is one of the most common opportunistic infections seen in people living with advanced HIV disease. The chronic nature of these underlying conditions requires long-term or recurrent antifungal treatment, driving consistent demand. In hospital settings, Candida species are the most common cause of invasive fungal infections, necessitating the use of systemic antifungals. The ease of transmission and colonization in healthcare environments further contributes to the high incidence rates. As the population ages and the prevalence of chronic diseases increases, the burden of candidiasis is expected to grow. This sustained clinical demand ensures that candidiasis remains the leading therapeutic indication in the antifungal drugs market.

On the other end, the aspergillosis segment is anticipated to grow at the fastest CAGR of 11.6% over the forecast period owing to the increasing recognition of invasive aspergillosis in immunocompromised patients and the development of more effective diagnostic tools. The increasing number of patients undergoing chemotherapy and hematopoietic stem cell transplantation for hematologic malignancies is a key driver for the growth of the aspergillosis segment. According to the Global Cancer Observatory, the number of new cancer cases in Asia is projected to increase by over 50% by 2040. These patients are severely immunocompromised and highly susceptible to invasive pulmonary aspergillosis. Aspergillus fumigatus is the most common cause of invasive mold infections in this population. The high mortality rate associated with untreated aspergillosis necessitates prompt and effective antifungal therapy. Voriconazole and isavuconazole are the standard of care for invasive aspergillosis, and their usage is increasing with the growing number of cancer treatments. Hospitals are implementing prophylactic antifungal protocols for high-risk patients, further driving drug consumption. The improvement in survival rates for cancer patients means a larger population living with prolonged immunosuppression, requiring ongoing monitoring and treatment. As oncology services expand in the region, the demand for specialized antifungals for aspergillosis will continue to accelerate. This clinical imperative positions aspergillosis as the fastest-growing indication segment.

By Application Insights

The ointments segment held 36.1% of the Asia-pacific market share in 2025. The leading position of ointments segment in the Asia-Pacific market is primarily driven by the high preference for topical treatments for superficial fungal infections, which are the most common type of fungal disease in the region. Superficial fungal infections such as tinea pedis, tinea cruris, and cutaneous candidiasis are extremely common in the hot and humid climate of the Asia Pacific region. According to the World Health Organization, skin diseases are a major cause of health burden, with fungal infections like ringworm affecting significant portions of the population in tropical areas. Patients and physicians prefer topical ointments for these conditions due to their localized action, minimal systemic side effects, and ease of application. Ointments provide a moisturizing effect, which is beneficial for dry and scaly lesions common in dermatophytosis. The availability of over-the-counter antifungal ointments containing clotrimazole, miconazole, and terbinafine makes them easily accessible without a prescription. In rural areas where access to healthcare facilities is limited, self-medication with topical ointments is the primary mode of treatment. The low cost and wide availability of generic topical formulations further enhance their popularity. The high recurrence rate of superficial infections also leads to repeat purchases. This strong consumer preference for convenient and safe topical treatments ensures that ointments remain the leading application segment in the antifungal drugs market.

The drugs segment is anticipated to register a CAGR of 10.1% over the forecast period in the Asia-Pacific market due to the rising incidence of invasive fungal infections and the need for systemic therapy. The increasing burden of invasive fungal infections requiring systemic treatment is the primary driver for the growth of the oral and systemic drugs segment. According to the Lancet Microbe, over 6.5 million people worldwide are estimated to be affected by invasive fungal infections annually, with a high proportion of cases in Asia. Conditions such as invasive candidiasis, aspergillosis, and cryptococcal meningitis cannot be treated with topical agents and require oral or intravenous antifungals. The growing population of immunocompromised individuals, including those with HIV, cancer, and organ transplants, is expanding the pool of patients needing systemic therapy. In hospitals across the region, the use of systemic azoles and echinocandins is increasing to manage these severe infections. The shift towards oral step-down therapy from intravenous administration for stable patients also boosts the sales of oral formulations. As healthcare systems improve their capacity to diagnose and treat invasive diseases, the demand for systemic antifungal drugs rises. This clinical necessity drives the rapid growth of the drugs segment, outpacing topical applications.

REGIONAL ANALYSIS

China Anti Fungal Drugs Market Analysis

China dominated the market by capturing 33.1% of the Asia-Pacific market share in 2025 due to the massive patient population and a growing burden of fungal infections due to high diabetes prevalence. The increasing incidence of invasive fungal infections in hospitals driven by the expansion of critical care services is further propelling the dominance of the Chinese market. According to the National Health Commission of China, the total number of hospital beds in China reached approximately 9.75 million by 2022, increasing the potential for hospital-acquired infections. The government is investing in improving diagnostic capabilities for fungal diseases, which is uncovering previously undiagnosed cases. The presence of a strong domestic pharmaceutical industry ensures the availability of affordable generic antifungals. Rising health awareness and increasing disposable income are driving demand for branded and advanced therapies. The aging population further contributes to the susceptibility to fungal infections. These factors ensure China’s dominant position in the regional market.

India Anti Fungal Drugs Market Analysis

India had the second largest share of the Asia-Pacific antifungal drugs market in 2025. The widespread use of over-the-counter topical antifungals for conditions like tinea and candidiasis are fuelling the Indian market expansion. According to the Indian Council of Medical Research, the prevalence of dermatophytosis has reached epidemic proportions in some parts of India, with many cases showing resistance to standard treatments. The availability of low-cost generic antifungals produced by local manufacturers makes treatment accessible to the masses. However, the issue of antifungal resistance is becoming a significant concern, prompting regulatory actions. The growing healthcare infrastructure is improving the diagnosis and treatment of invasive fungal infections. Government initiatives to control diabetes and HIV also indirectly support the market. These dynamics sustain India’s strong market presence.

Japan Anti Fungal Drugs Market Analysis

Japan holds a promising share of the Asia Pacific antifungal drugs market due to the high incidence of invasive aspergillosis and candidiasis in elderly and immunocompromised patients. As per the Japanese Ministry of Health, Labour and Welfare, the proportion of people aged 65 and over has reached approximately 29% of the population, a demographic at high risk for serious infections. The national health insurance system covers expensive systemic antifungals, ensuring patient access. Japan is a leader in the adoption of new-generation azoles and echinocandins. The strong regulatory framework ensures high standards of drug quality and safety. The focus on precision medicine and early diagnosis drives the use of advanced therapies. These elements maintain Japan’s prominent market position.

Australia Anti Fungal Drugs Market Analysis

Australia represents a mature segment of the Asia Pacific antifungal drugs market owing to the increasing prevalence of invasive fungal infections in hospitalized patients and the strong emphasis on antimicrobial stewardship. According to the Australian Institute of Health and Welfare, invasive fungal infections are a significant contributor to morbidity and mortality in high-risk patient groups. The Pharmaceutical Benefits Scheme subsidizes the cost of antifungal drugs, improving accessibility. The high rate of diabetes and immunosuppressive therapies contributes to demand. Australia is also a hub for clinical research in antifungal resistance. The focus on evidence-based practice ensures optimal use of antifungals. These factors contribute to Australia’s stable market performance.

South Korea Anti Fungal Drugs Market Analysis

South Korea holds a noteworthy share of the Asia Pacific antifungal drugs market. The rising incidence of cancer and hematologic malignancies which increase the risk of invasive fungal infections are driving the market expansion in South Korea. According to Statistics Korea, the number of cancer cases has been steadily increasing, leading to higher utilization of specialized medical care. The national health insurance system provides comprehensive coverage for antifungal treatments. The country has a high adoption rate of new and effective antifungal agents. Strong investment in healthcare infrastructure supports the diagnosis and treatment of fungal diseases. The presence of local pharmaceutical companies enhances market competition. These factors drive the steady growth of the market in South Korea.

COMPETITIVE LANDSCAPE

The competitive landscape of the Asia Pacific antifungal drugs market is characterized by intense rivalry among multinational pharmaceutical giants and dominant local generic manufacturers. Global leaders leverage their proprietary technologies and established brand reputations to maintain dominance in the hospital and prescription segments. They continuously innovate by developing new drug classes and delivery systems to address emerging resistance issues. Meanwhile domestic players in countries like India and China are gaining traction by providing cost effective generic alternatives that cater to price sensitive populations. These local firms benefit from strong manufacturing capabilities and extensive distribution networks. The market sees frequent strategic moves such as licensing agreements and joint ventures aimed at enhancing product portfolios and geographic presence. Price competition is particularly fierce in the topical and over the counter segments where affordability drives consumer choice. Regulatory compliance and quality assurance remain critical differentiators as healthcare systems strive to ensure patient safety. This dynamic environment fosters continuous improvement in product quality and accessibility ultimately benefiting patients through better treatment options across the region.

KEY MARKET PLAYERS

Companies playing a significant role in the Asia Pacific Antifungal drugs market include

- Alternaria

- Pfizer

- Novartis

- Sanofi-Aventis

- Merck & Co.

- Aspergillus

- Kramer Laboratories

- Bayer Healthcare

- Enzon Pharmaceuticals

- GlaxoSmithKline

- Gilead Sciences

- Abbott Laboratories

Top Players in the Asia Pacific Anti-Fungal Drugs Market

Pfizer Inc

Pfizer Inc is a global pharmaceutical leader with a significant presence in the Asia Pacific antifungal drugs market. The company offers a robust portfolio including fluconazole and voriconazole which are essential for treating invasive fungal infections. Pfizer contributes to the global market by maintaining high manufacturing standards and ensuring consistent supply chains. Recent actions include expanding distribution networks in India and China to improve access to critical antifungal therapies. The company strengthens its market position through strategic partnerships with local healthcare providers and government bodies. Pfizer also invests in clinical research to support the efficacy of its existing formulations. These initiatives enhance brand reliability and ensure that patients in the Asia Pacific region receive timely and effective treatment for serious fungal conditions.

Gilead Sciences Inc

Gilead Sciences Inc is a major player in the Asia Pacific antifungal drugs market known for its innovative amphotericin B formulations and echinocandins. The company focuses on developing advanced therapies for invasive aspergillosis and candidiasis. Gilead contributes to the global market by pioneering lipid based drug delivery systems that reduce toxicity. Recent actions involve launching educational programs for clinicians in Japan and Australia to promote early diagnosis and appropriate use of antifungals. The company strengthens its position by collaborating with research institutions to study resistance patterns. Gilead also expands its regulatory approvals for new indications in key Asian markets. These efforts demonstrate a commitment to improving patient outcomes and solidify its reputation as a leader in specialized antifungal treatments across the diverse Asia Pacific healthcare landscape.

Cipla Limited

Cipla Limited is a prominent pharmaceutical company headquartered in India with a strong footprint in the Asia Pacific antifungal drugs market. The company provides a wide range of affordable generic antifungal medications including azoles and allylamines. Cipla contributes to the global market by ensuring accessibility of essential medicines in low and middle income countries. Recent actions include expanding its manufacturing capacity and launching new topical formulations in Southeast Asian markets. The company strengthens its market position through aggressive pricing strategies and extensive distribution networks. Cipla also engages in public health initiatives to raise awareness about fungal infections. Its focus on quality and affordability makes it a preferred partner for governments and healthcare providers. These strategies enable Cipla to maintain a competitive edge and serve a large patient base in the region.

Top Strategies Used by the Key Market Participants

Key players in the Asia Pacific antifungal drugs market primarily focus on product diversification and strategic partnerships to strengthen their positions. Companies invest in research and development to create novel formulations with improved safety profiles and efficacy against resistant strains. This emphasis on innovation helps firms differentiate their offerings in a crowded market. Strategic collaborations with local distributors and healthcare institutions enable companies to navigate regulatory complexities and expand market reach. Manufacturers also prioritize expanding production facilities in key countries to reduce costs and ensure supply chain stability. Additionally many organizations engage in educational initiatives to train physicians on proper diagnosis and treatment protocols. By adopting these multifaceted approaches market participants aim to capture greater market share and sustain long term growth in this evolving regional sector.

MARKET SEGMENTATION

This research report on the Asia Pacific antifungal drugs market has been segmented and sub-segmented into the following categories.

By Drug Type

- Echinocandins

- Azoles

- Polyenes

- Allylamines

- Others

By Therapeutic Indications

- Aspergillosis

- Dermatophytosis

- Candidiasis

- Others

By Application

- Powders

- Ointments

- Drugs

- Pastes

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC