- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

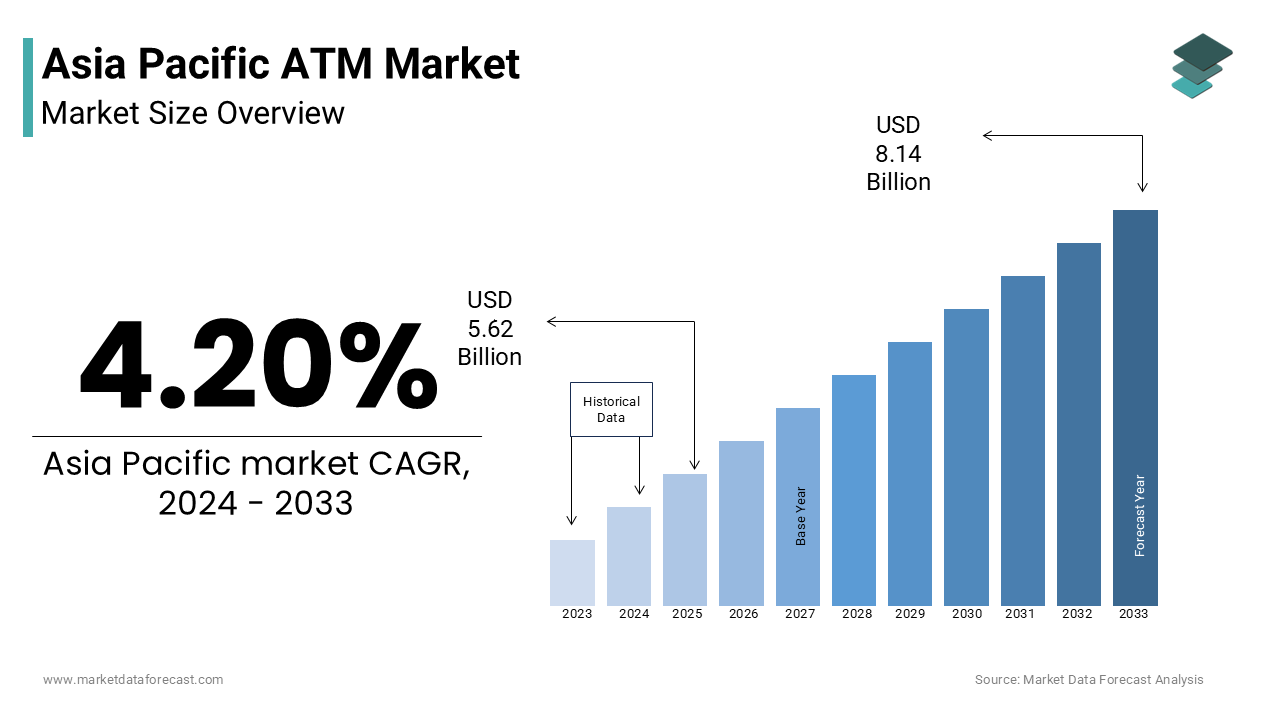

Asia Pacific ATM Market Size

The Asia Pacific ATM market is projected to grow from USD 5.62 billion in 2024 to USD 8.14 billion by 2033, at a CAGR of 4.20%.

The ATM market refers to the deployment, operation, and management of automated teller machines across banking and financial institutions in the region. These machines enable customers to perform essential banking transactions such as cash withdrawals, balance inquiries, fund transfers, and bill payments without requiring direct interaction with bank personnel. Asia Pacific has emerged as a dynamic hub for ATM growth due to rapid financial inclusion initiatives, increasing digital banking adoption, and government-led infrastructure development. Countries like India, China, and Indonesia are expanding their ATM networks to support growing banking populations and facilitate access to cash-based economies. Moreover, technological advancements have transformed traditional ATMs into intelligent self-service terminals capable of supporting cardless transactions, real-time fraud detection, and integration with mobile banking platforms. As per the Global Financial Inclusion Index, more than 70% of adults in Southeast Asia now use formal financial services, further reinforcing the need for expanded ATM coverage.

MARKET DRIVERS

Expanding Financial Inclusion Initiatives Across the Region

One of the primary drivers fueling the growth of the ATM market in the Asia Pacific is the widespread implementation of financial inclusion programs by national governments and banking regulators. According to the World Bank, over 800 million adults in the region were brought into the formal banking system between 2014 and 2022 through initiatives such as India’s Pradhan Mantri Jan Dhan Yojana and Indonesia’s National Financial Inclusion Strategy. In rural areas where physical bank branches are sparse, ATMs serve as critical touchpoints for delivering financial services. For instance, in the Philippines, the Bangko Sentral ng Pilipinas reported that ATM installations in remote municipalities increased by nearly 40% between 2020 and 2023. Additionally, microfinance banks and cooperative credit unions have been leveraging low-cost ATMs to serve underbanked communities. Furthermore, mobile banking and digital wallets often require cash-out options, which are facilitated through ATMs. As per the Asian Development Bank, approximately 65% of digital wallet users in Vietnam rely on ATMs for converting e-money into physical currency.

Rising Demand for Cash-Based Transactions Despite Digital Payments Growth

QR code payments, and contactless cards, and cash remain a dominant medium of transaction in many parts of the Asia Pacific. As per the International Monetary Fund (IMF), cash still accounts for more than 50% of all retail transactions in countries like Thailand, Malaysia, and Vietnam. This preference for cash fuels the continued need for extensive ATM networks to support daily liquidity requirements. In India, despite the government’s push toward digital payments post-demonetization, cash withdrawals from ATMs grew by 18% year-on-year in 2023, as reported by the Reserve Bank of India. A key reason is the informal economy's reliance on cash for daily wage disbursements, small business transactions, and consumer purchases. Additionally, cross-border travelers and expatriates frequently depend on ATMs for foreign currency withdrawals. Japan, for example, has enhanced its ATM interoperability with international networks to accommodate tourists using foreign-issued cards, as noted by Japan Exchange Group.

MARKET RESTRAINTS

Increasing Adoption of Digital Payment Solutions

A significant restraint affecting the Asia Pacific ATM market is the accelerating shift toward digital payment solutions, which reduces the frequency of cash withdrawals. Mobile wallets, contactless cards, and QR-based payment systems are becoming increasingly popular among consumers, particularly in urban areas where smartphone penetration is high. In countries like South Korea and Singapore, where fintech innovation is well-established, consumers prefer using digital payment apps for everyday transactions rather than withdrawing cash. Banks are also incentivizing digital transactions through fee waivers and loyalty rewards, further discouraging cash-based interactions. In Australia, major banks have introduced no-fee digital transfers and higher fees for out-of-network ATM withdrawals, nudging consumers away from traditional cash dispensers.

High Maintenance and Security Costs Associated with ATM Operations

Maintaining a large and widely distributed ATM network comes with substantial operational and security costs, which pose a major constraint on market growth. Banks and financial institutions must invest heavily in regular servicing, cash replenishment, software updates, and cybersecurity measures to ensure smooth and secure operations. Security threats such as skimming, card cloning, and cyberattacks further escalate expenses. In 2023, the Hong Kong Monetary Authority reported a 22% increase in ATM-related fraud cases, prompting banks to deploy advanced security features like biometric authentication, EMV chip compliance, and AI-based fraud detection systems. Remote and rural ATMs face additional challenges related to infrastructure reliability, including power outages and connectivity issues. In India, for instance, the Indian Bank Association found that nearly 30% of ATMs in tier-3 and tier-4 cities experience technical disruptions monthly, increasing repair and downtime costs.

MARKET OPPORTUNITIES

Integration of Biometric and Smart Authentication Technologies

A promising opportunity for the Asia Pacific ATM market lies in the integration of biometric and smart authentication technologies to enhance security and user convenience. Traditional PIN-based authentication is increasingly vulnerable to fraud, prompting banks to adopt fingerprint scanning, facial recognition, iris identification, and voice verification as alternative verification methods. According to the International Biometrics & Identification Association (IBIA), biometric ATM deployments in the Asia Pacific grew by over 30% between 2021 and 2023, which is driven by regulatory mandates and rising consumer demand for secure banking experiences.

India has been at the forefront of this transformation, with several public sector banks introducing Aadhaar-linked biometric ATMs to authenticate transactions. As per the Unique Identification Authority of India (UIDAI), more than 50,000 Aadhaar-enabled ATMs were operational nationwide by mid-2023, enabling seamless banking for millions of rural users. Beyond security, smart authentication enhances financial inclusion by catering to illiterate or elderly users who struggle with conventional PIN entry. In Indonesia, local banks have launched voice-guided ATMs equipped with biometric login features to improve accessibility.

Expansion of Shared and White-Label ATM Networks

Another significant opportunity in the Asia Pacific ATM market is the expansion of shared and white-label ATM networks, which reduce individual bank costs while improving geographical reach. Traditionally, each bank operated its own ATM fleet, resulting in inefficiencies and uneven distribution. However, shared ATM networks where multiple banks utilize a common infrastructure are gaining traction as a cost-effective solution. White-label ATMs, which are deployed and managed by non-bank entities such as telecom companies and retail chains, are also emerging as a viable alternative. In India, the National Payments Corporation of India (NPCI) has promoted the Bharat QR and BHIM initiative alongside white-label ATM operators like Vakrangee and Tata Communications, expanding access in semi-urban and rural areas. As per the Reserve Bank of India, over 200,000 white-label ATMs were active across India in 2023, contributing to financial inclusion goals.

MARKET CHALLENGES

Regulatory Complexity and Compliance Requirements

A major challenge confronting the Asia Pacific ATM market is the diverse and evolving regulatory landscape governing cash transactions, data privacy, and financial security. Each country in the region has distinct rules regarding ATM licensing, interoperability, transaction limits, and anti-money laundering (AML) compliance, making it difficult for banks and operators to maintain uniform standards. According to the Basel Committee on Banking Supervision, regulatory scrutiny around ATM operations has intensified in recent years, particularly concerning KYC (Know Your Customer) norms and real-time monitoring of suspicious transactions. In China, the People's Bank of China mandates stringent encryption protocols for ATM transactions, increasing compliance costs for domestic and international banks. Similarly, in India, the Reserve Bank of India requires all ATMs to be EMV-compliant and mandates periodic audits for fraud prevention, adding administrative burdens. Moreover, cross-border ATM operators face additional hurdles in adhering to varying cybersecurity laws and data localization policies. In Australia, the Office of the Australian Information Commissioner (OAIC) enforces strict regulations on personal data handling, impacting foreign ATM service providers.

Declining Revenue Per ATM Due to Reduced Transaction Frequency

An emerging challenge for the Asia Pacific ATM market is the declining revenue per ATM unit due to reduced transaction frequency and falling interchange fees. As consumers increasingly rely on digital payment alternatives, traditional ATM transactions such as cash withdrawals and balance inquiries have declined, leading to lower earnings for operators. Banks are also imposing restrictions on free ATM transactions to encourage digital banking, thereby reducing footfall. In Japan, major banks have implemented policies limiting free ATM usage to account holders only, effectively pushing non-customers toward digital channels. Additionally, the rise of mobile banking and prepaid cards has diminished the necessity for frequent ATM visits. In South Korea, mobile payment app usage surpassed 90% of the population in 2023, as reported by the Korea Financial Telecommunications & Clearings Institute (KFTC), further eroding ATM transaction volumes. To counteract declining revenues, operators are exploring value-added services such as bill payments, insurance top-ups, and mobile recharges via ATMs.

SEGMENTAL ANALYSIS

By Solution Insights

The offsite ATM deployment segment was the largest and held 48.2% of the Asia Pacific ATM market share in 2024. One of the key drivers behind this segment’s dominance is the growing demand for cash accessibility in urban and semi-urban areas where foot traffic is high but proximity to a bank branch is limited. Moreover, banks and financial institutions prefer off-site deployments due to their ability to generate non-interest income through interchange fees and value-added services such as mobile top-ups and utility bill payments. Additionally, partnerships between banks and third-party operators such as telecom companies and retail chains have accelerated the rollout of offsite ATMs.

The managed services segment is projected to expand with a CAGR of 9.6% from 2025 to 2033. A major contributing factor is the rising operational complexity of ATMs with the integration of biometric authentication, AI-driven fraud detection, and cloud-based monitoring systems. Many banks, especially smaller regional institutions, lack the technical expertise and infrastructure to manage these advanced functionalities in-house. As per Deloitte, over 55% of mid-sized banks in the Philippines have transitioned to managed ATM services since 2021, which is citing cost-efficiency and improved uptime as primary benefits. Furthermore, managed service providers are leveraging digital transformation to offer predictive maintenance and remote diagnostics, reducing downtime and improving user experience.

REGIONAL ANALYSIS

India ATM Market Insights

India was the top performer in the Asia Pacific ATM sector with 32.1% of the share in 2024. A major driver of this growth is the government’s emphasis on financial inclusion through initiatives like Pradhan Mantri Jan Dhan Yojana (PMJDY), which brought over 400 million previously unbanked individuals into the formal financial system. Additionally, the proliferation of white-label ATM operators such as Vakrangee and Tata Communications has enabled broader reach in rural and semi-urban areas. As per the National Payments Corporation of India (NPCI), white-label ATMs accounted for over 200,000 active units nationwide by complementing traditional bank-owned machines. Moreover, the introduction of Aadhaar-linked biometric ATMs and interoperable payment systems has enhanced security and convenience.

China ATM Market Insights

China ranked second with 24.3% of the Asia Pacific ATM market share in 2024. A key growth factor is the continued need for cash-based transactions in smaller cities and rural regions where digital payment adoption remains uneven. Another significant driver is the expansion of smart ATMs capable of multi-functional banking services, including cardless withdrawals, QR code-based transactions, and real-time balance inquiries. Additionally, cross-border tourism and business travel continue to necessitate widespread ATM availability. As per UnionPay, over 10 million foreign tourists used Chinese ATMs in 2023, which is benefiting from expanded international interoperability.

Japan ATM Market Insights

Japan ATM market is substantially to grow substantially with the highest CAGR throughout the forecast period. One of the key factors underpinning Japan’s strong position is the country’s preference for cash transactions despite its high level of digital sophistication. Japanese banks have also prioritized the deployment of multifunctional ATMs that support a wide range of services, including foreign currency withdrawals, mobile wallet top-ups, and insurance premium payments. Mizuho Bank and Sumitomo Mitsui Banking Corporation have led efforts to integrate AI-based customer service interfaces into ATMs, enhancing the user experience. Additionally, the aging population has influenced ATM design to accommodate elderly users with features such as voice guidance, large-print displays, and emergency assistance buttons.

Australia ATM Market Insights

Australia ATM market is growing with the high consumer trust in self-service banking channels. According to the Reserve Bank of Australia, over 85% of adults use ATMs at least once a month, primarily for cash withdrawals and balance checks. This consistent usage supports a robust network of over 36,000 ATMs nationwide. Additionally, there is a growing push toward digital integration, with ATMs now supporting contactless card transactions, mobile wallet compatibility, and real-time transaction alerts. In partnership with PayID and New Payments Platform (NPP), several banks have introduced ATMs that allow instant fund transfers via mobile numbers.

South Korea ATM Market Insights

South Korea ATM market growth is due to the widespread use of cash among older demographics and small businesses. Banks and fintech firms have responded by integrating ATMs with digital services such as mobile deposit scanning, QR-based cash withdrawals, and real-time language translation for foreign users. KB Kookmin Bank and Shinhan Bank have pioneered the deployment of smart ATMs that offer personalized banking options based on user profiles. Additionally, the rise of contactless ATM transactions using NFC-enabled smartphones has revitalized interest in self-service banking.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key market players include Diebold Nixdorf, NCR Corporation, Hitachi-Omron Terminal Solutions, Fujitsu, GRG Banking, OKI Electric Industry Co., Ltd., and Triton Systems.

The competition in the Asia Pacific ATM market is marked by a dynamic mix of global technology providers, regional manufacturers, and emerging fintech-driven service companies vying for dominance in a rapidly transforming financial ecosystem. While traditional ATM vendors continue to lead with robust hardware and software solutions, new entrants are leveraging digital innovations to disrupt conventional self-service banking models. This evolving landscape is shaped by the dual forces of declining cash usage due to the rise of mobile and QR-based payments, and the increasing demand for smarter, more secure, and feature-rich ATMs in both urban and rural settings.

Market participants are differentiating themselves through advanced technology integration, localized deployment strategies, and comprehensive managed services that reduce operational burdens for banks. The competitive intensity is particularly high in countries like India and China, where large-scale ATM rollouts are driven by government-backed financial inclusion initiatives. Meanwhile, in developed markets such as Japan and Australia, the focus is shifting toward upgrading existing ATM infrastructures with AI-powered analytics, predictive maintenance, and enhanced cybersecurity measures. Strategic acquisitions, partnerships with digital payment platforms, and investments in sustainable and future-ready ATM technologies are becoming essential components of competitive strategy in the Asia Pacific ATM market.

Top Players in the Asia Pacific ATM Market

NCR Corporation (United States, with a strong presence in Asia Pacific)

NCR Corporation is a leading global provider of ATM solutions and plays a significant role in shaping the Asia Pacific ATM market. The company offers a wide range of self-service banking technologies, including smart ATMs, cash recyclers, and digital banking platforms tailored to regional needs. In the Asia Pacific, NCR collaborates closely with major banks and financial institutions to deploy secure, scalable, and integrated ATM networks that support evolving customer expectations.

NCR’s emphasis on innovation has led to the development of next-generation ATMs featuring biometric authentication, contactless transactions, and cloud-based management systems.

Diebold Nixdorf (United States, with extensive operations in Asia Pacific)

Diebold Nixdorf is a key player in the Asia Pacific ATM market, known for delivering comprehensive self-service solutions that combine hardware, software, and managed services. The company supports banks and financial institutions by offering customized ATM deployment models, including offsite and mobile ATMs, designed to enhance accessibility and convenience for end users.

In the Asia Pacific, Diebold Nixdorf has focused on integrating digital banking features into traditional ATM infrastructure, enabling customers to perform complex transactions beyond cash withdrawals. Its localized support services and proactive maintenance programs have strengthened operational efficiency for banks, particularly in emerging economies where ATM adoption is expanding rapidly.

The company’s long-standing presence in countries like India, China, and Australia promotes its deep understanding of regional banking dynamics and regulatory environments by making it a trusted partner for financial institutions aiming to modernize their ATM fleets.

Hitachi-Omron Terminal Solutions (Japan)

Hitachi-Omron Terminal Solutions is a dominant regional player in the Asia Pacific ATM market, particularly in Japan and Southeast Asia. As a joint venture between Hitachi and Omron, the company specializes in high-performance, secure, and user-friendly ATM systems that cater to both domestic and international banking requirements. This company is recognized for its advanced technological capabilities, including multi-function ATMs that support bill payments, fund transfers, and mobile top-ups. It has played a crucial role in Japan’s transition toward smart banking through the deployment of AI-enabled ATMs that offer personalized services and enhanced security protocols. Hitachi-Omron has expanded its footprint in countries such as Thailand and Indonesia, where it partners with local banks to improve financial access in rural and semi-urban areas. Its commitment to innovation and regional adaptation makes it a key contributor to the evolution of the Asia Pacific ATM landscape.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by key players in the Asia Pacific ATM market is technology integration and product innovation. Companies are continuously enhancing ATM functionalities by incorporating biometric authentication, contactless card support, mobile wallet compatibility, and real-time fraud detection mechanisms. These advancements not only improve security but also align with changing consumer preferences for seamless and intuitive banking experiences.

Another critical approach is strategic partnerships and collaborations with local banks and fintech firms. By working closely with regional financial institutions, ATM solution providers can tailor their offerings to meet specific regulatory and operational requirements. These alliances also facilitate the expansion of ATM networks into underserved areas, supporting broader financial inclusion goals across emerging economies.

Lastly, the expansion of managed services and outsourcing solutions has become a focal point for leading ATM vendors. Offering end-to-end managed services ranging from maintenance and cash logistics to software updates and cybersecurity enables banks to reduce operational costs while ensuring reliable performance. This model is gaining traction among smaller banks and credit unions that seek to modernize their ATM infrastructure without significant capital investment.

RECENT MARKET DEVELOPMENTS

- In March 2023, NCR Corporation partnered with a leading Indian bank to deploy AI-integrated ATMs capable of real-time fraud detection and personalized transaction options. This initiative aimed at improving security and enhancing user experience across urban and semi-urban locations.

- In October 2023, Diebold Nixdorf launched a new line of cloud-connected ATMs in South Korea, designed to support remote diagnostics, instant software updates, and seamless integration with mobile banking apps, strengthening its foothold in the country’s digital banking transformation.

- In January 2024, Hitachi-Omron Terminal Solutions introduced a series of energy-efficient ATMs in Japan equipped with low-power processors and eco-friendly materials by aligning with the nation's sustainability goals while maintaining high performance.

- In May 2024, Wincor Nixdorf (a subsidiary of Diebold Nixdorf) entered into a joint venture with an Indonesian fintech firm to expand white-label ATM services across the archipelago, which is focusing on improving financial access in remote regions.

- In August 2024, NCR Corporation acquired a regional ATM software provider in Australia by aiming to enhance its digital banking suite and provide banks with unified self-service platforms that integrate seamlessly with core banking systems.

MARKET SEGMENTATION

This research report on the Asia Pacific ATM market is segmented and sub-segmented into the following categories.

By Solution

- Deployment

- Managed Services

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC