Asia Pacific Beauty Devices Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By End-User, Application And By Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2025 to 2033

Market Size, 2025

$4856 MnMarket Estimate, 2026

$5625 MnMarket Forecast, 2034

$18253 MnCAGR, 2026–2034

15.85%Asia Pacific Beauty Devices Market Size

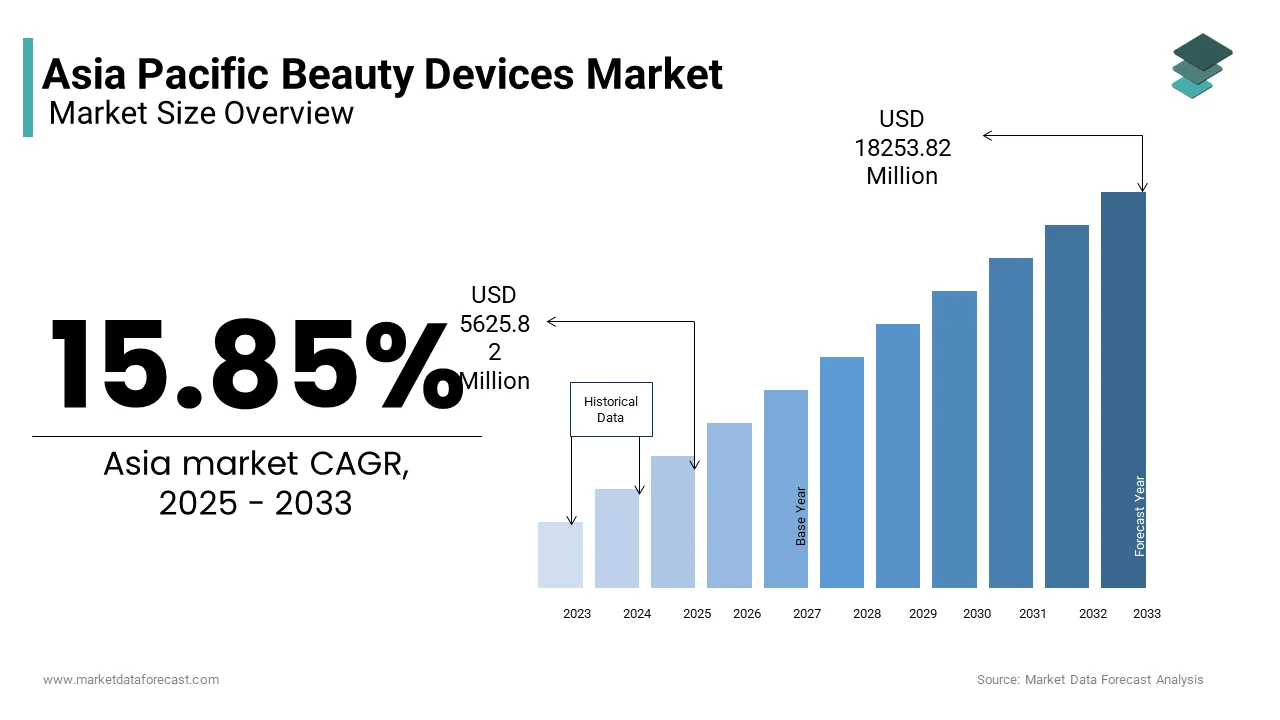

The Asia Pacific beauty devices market was valued at USD 4856.12 million in 2024 and is anticipated to reach USD 5625.82 million in 2025 from USD 18253.82 million by 2033, growing at a CAGR of 15.85% during the forecast period from 2025 to 2033.

The Asia Pacific beauty devices market covers a wide range of consumer electronic products designed for personal skincare, haircare, and body aesthetics. These include facial cleansing brushes, skin toning devices, LED masks, hair removal gadgets, epilators, microcurrent devices, and other wearable or handheld tools that apply technologies such as radiofrequency, red light therapy, ultrasonic vibrations, and iontophoresis. Unlike traditional beauty tools, modern beauty devices often integrate smart features, mobile app connectivity, and AI-based diagnostics to offer personalized treatment regimens tailored to individual skin and hair conditions.

MARKET DRIVERS

Rising Awareness of Skincare and Personal Grooming

One of the primary drivers of the Asia Pacific beauty devices market is the rising awareness of skincare and personal grooming particularly among younger and middle-class demographics. Consumers are becoming more informed about the benefits of maintaining healthy skin and managing issues such as acne, aging, pigmentation, and sensitivity through targeted treatments beyond conventional cosmetics.

In countries like South Korea and Japan, where skincare is deeply embedded in cultural norms, there is a growing preference for high-tech, at-home beauty solutions that were previously only available in professional salons or dermatology clinics. In addition, social media platforms such as Instagram, TikTok, and Xiaohongshu have played a crucial role in educating consumers and influencing purchasing behavior. Influencers and beauty experts routinely demonstrate the efficacy of devices like LED face masks, microcurrent tools, and derma rollers, making them mainstream household items. Beyond aesthetics, health concerns related to pollution-induced skin damage in megacities like Delhi, Jakarta, and Beijing have further fueled demand for advanced skincare devices. According to the United Nations Environment Programme, several Asian cities rank among the most polluted globally, prompting users to invest in anti-pollution skincare tools equipped with sensors and real-time feedback mechanisms.

Integration of Smart Technology and IoT in Beauty Devices

Another major driver of the Asia Pacific beauty devices market is the integration of smart technology and Internet of Things (IoT) capabilities, which enhance functionality, personalization, and user engagement. Modern beauty devices now feature Bluetooth connectivity, AI-powered diagnostics, mobile app synchronization, and even machine learning algorithms to tailor treatments based on individual skin analytics. South Korean and Japanese companies have been pioneers in this space, launching products like smart mirrors that analyze skin condition using facial recognition, app-connected facial cleansers that track usage patterns, and wearable beauty patches that monitor hydration levels in real time. Moreover, brands such as Panasonic, MTG, and L’Oréal’s connected beauty division are collaborating with tech firms to develop cloud-based skincare platforms that allow users to sync their beauty routines with smartphones and receive customized recommendations. This not only enhances consumer experience but also fosters brand loyalty through continuous digital interaction. Also, the expansion of e-commerce platforms and direct-to-consumer models has made it easier for consumers to access these high-tech beauty tools. Retailers like Amazon Japan, Flipkart, and Tmall have introduced dedicated sections for smart beauty devices, supported by detailed product descriptions, user reviews, and virtual try-on features.

MARKET RESTRAINT

High Cost of Advanced Beauty Devices

A key restraint affecting the growth of the Asia Pacific beauty devices market is the relatively high cost of advanced, technologically sophisticated devices, which limits accessibility for a large portion of the population. While premium beauty tools such as LED therapy masks, RF skin tightening devices, and AI-integrated smart mirrors offer enhanced performance and personalization, their price points often place them out of reach for budget-conscious consumers. However, advanced devices priced high remain largely confined to urban, high-income segments, primarily in Japan, South Korea, and Australia. In emerging markets like Indonesia, Vietnam, and the Philippines, where per capita income remains significantly lower than in developed economies, the adoption of high-end beauty devices has been sluggish. Despite rising interest in skincare, many consumers still prioritize affordability and multipurpose utility over niche technological functions. Furthermore, economic volatility and inflationary pressures in 2023 impacted discretionary spending, causing some buyers to delay purchases of non-essential beauty electronics.

Regulatory Barriers and Product Safety Concerns

Another significant constraint on the Asia Pacific beauty devices market is the increasing scrutiny from regulatory bodies regarding product safety and efficacy, particularly for devices that claim therapeutic benefits. Many beauty instruments—especially those utilizing radiofrequency, intense pulsed light (IPL), or laser-based technologies —fall into a regulatory gray area between cosmetic and medical devices, leading to inconsistent oversight across different jurisdictions.

In China and South Korea, national drug and medical device authorities have imposed stricter guidelines on beauty electronics that make clinical claims, requiring third-party testing, certification, and adverse event monitoring . Ike, As of early 2024, a significant share of newly submitted beauty device applications were rejected or delayed due to incomplete compliance documentation, impacting market entry timelines. Similarly, in India, he Central Drugs Standard Control Organization (CDSCO) has initiated investigations into whether certain beauty devices should be classified under medical equipment regulations, which would necessitate prescription-based sales and clinical validation, potentially reducing consumer accessibility. These heightened regulatory requirements not only increase the time-to-market and operational costs for manufacturers but also raise consumer skepticism about the safety and effectiveness of home-use beauty devices.

MARKET OPPORTUNITY

Expansion of E-commerce and Direct-to-Consumer Sales Channels

A major opportunity shaping the future of the Asia Pacific beauty devices market is the rapid expansion of e-commerce and direct-to-consumer (D2C) sales channels, which enable brands to reach wider audiences with improved accessibility, personalized marketing, and streamlined distribution. The proliferation of online retail platforms has eliminated traditional distribution hurdles, allowing global and regional beauty device brands to engage directly with end consumers through digital storefronts, influencer collaborations, and social commerce. In Southeast Asia, platforms such as Shopee, Tokopedia, and Lazada have introduced dedicated beauty tech categories featuring video demonstrations, customer reviews, and bundled offers, enhancing consumer trust and purchase intent. According to Google, Temasek, and Bain & Company’s 2023 e-Conomy SEA Report, online beauty and personal care sales grew by more than 30% year-over-year, with beauty devices accounting for an increasing share of this segment. Companies like ME-Smooth and JOVS, specializing in at-home hair removal and skincare devices, have capitalized on short-video content to drive impulse purchases and repeat engagement. Besides, subscription-based beauty tech services and rental models are gaining traction, especially in markets like Japan and Australia, where consumers are exploring flexible ownership options before committing to full purchases.

Growing Demand for At-Home Aesthetic Treatments Post-Pandemic

Another transformative opportunity in the Asia Pacific beauty devices market is the growing preference for at-home aesthetic treatments following the pandemic, which accelerated the shift away from salon-based services toward personal wellness and grooming solutions. With movement restrictions and hygiene concerns limiting access to professional beauty salons, consumers sought alternative ways to maintain their appearance without leaving their homes. This behavioral shift has created a surge in demand for professional-grade home devices, including RF skin lifts, phototherapy masks, and dermic pens, traditionally reserved for spa settings. Moreover, telemedicine consultations have expanded the scope of at-home beauty care, with dermatologists and aestheticians recommending specific devices as part of personalized skincare regimens. In South Korea and Singapore, several beauty brands have partnered with healthcare apps to offer AI-assisted skin analysis, followed by tailored device suggestions, thereby bridging the gap between medical advice and consumer electronics. Also, urbanization and fast-paced lifestyles have made it difficult for working professionals to schedule regular salon visits, increasing reliance on portable, easy-to-use beauty devices that fit seamlessly into daily routines. With continued advancements in miniaturization, battery efficiency, and wireless charging, at-home beauty devices are becoming more practical and appealing to a broader audience.

MARKET CHALLENGES

Lack of Consumer Awareness and Education

One of the foremost challenges facing the Asia Pacific beauty devices market is the lack of widespread consumer awareness and education regarding proper usage, benefits, and limitations of beauty devices, particularly in rural and semi-urban areas. While urban populations have embraced these tools through exposure to influencers, digital marketing, and social commerce, a large segment of the population lacks understanding of how to effectively use and maintain such devices, leading to suboptimal results or premature discontinuation. In countries like India, Indonesia, and the Philippines, where traditional beauty practices remain dominant, many consumers are unfamiliar with the concept of at-home RF treatments, LED therapy, or iontophoresis-based skincare regimes. Additionally, misinformation circulating on social media and unverified forums can lead to safety concerns or misuse of beauty devices, deterring potential buyers. For instance, improper use of IPL hair removal tools or prolonged exposure to low-quality LED masks has caused minor burns or skin irritation in isolated cases, damaging brand reputation and consumer trust.

Rapid Imitation and Market Saturation by Low-Quality Counterfeits

Another pressing challenge in the Asia Pacific beauty devices market is the proliferation of counterfeit and low-quality imitations, which undermine consumer confidence and pose potential safety risks. As demand for beauty devices grows, numerous unregulated manufacturers and small-scale producers have flooded the market with cheaply made alternatives that mimic popular designs but lack proper engineering, certifications, or quality ccontrol In China, India, and Southeast Asia, e-commerce platforms and local retailers have become hotspots for copycat versions of high-end beauty tools, often sold at a fraction of the original price. These knockoffs often fail to deliver promised results and may contain substandard components, poor insulation, or unsafe electrical circuits posing risks of overheating, electric shocks, or skin burns. Furthermore, the presence of low-cost imitations creates pricing pressure on legitimate brands, forcing them to either compete on price, which is potentially compromising quality, or risk losing market share to cheaper, inferior alternatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.72% |

| Segments Covered | By Portability, Application, Mode of Operation, End-user, Distribution Channel, and Region. |

|

Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Nu Skin, Candela Medical, Silkn, TRIA BEAUTY, Curallux LLC., Termosalud, FOREO, Tech4Beauty, Koninklijke Philips N.V., Conair Corporation, Lumenis, Cynosure, Sciton, Inc., Fotona, Procter & Gamble, Colgate-Palmolive Company, LUTRONIC, STRATA Skin Sciences, NuFACE, Spectrum Brands, Inc., Cutera, Merz North America, Inc., El. En. S.p.A., YA-MAN LTD., Panasonic Corporation, Alma Lasers, Bausch Health Companies Inc. |

SEGMENTAL ANALYSIS

By Portability Insights

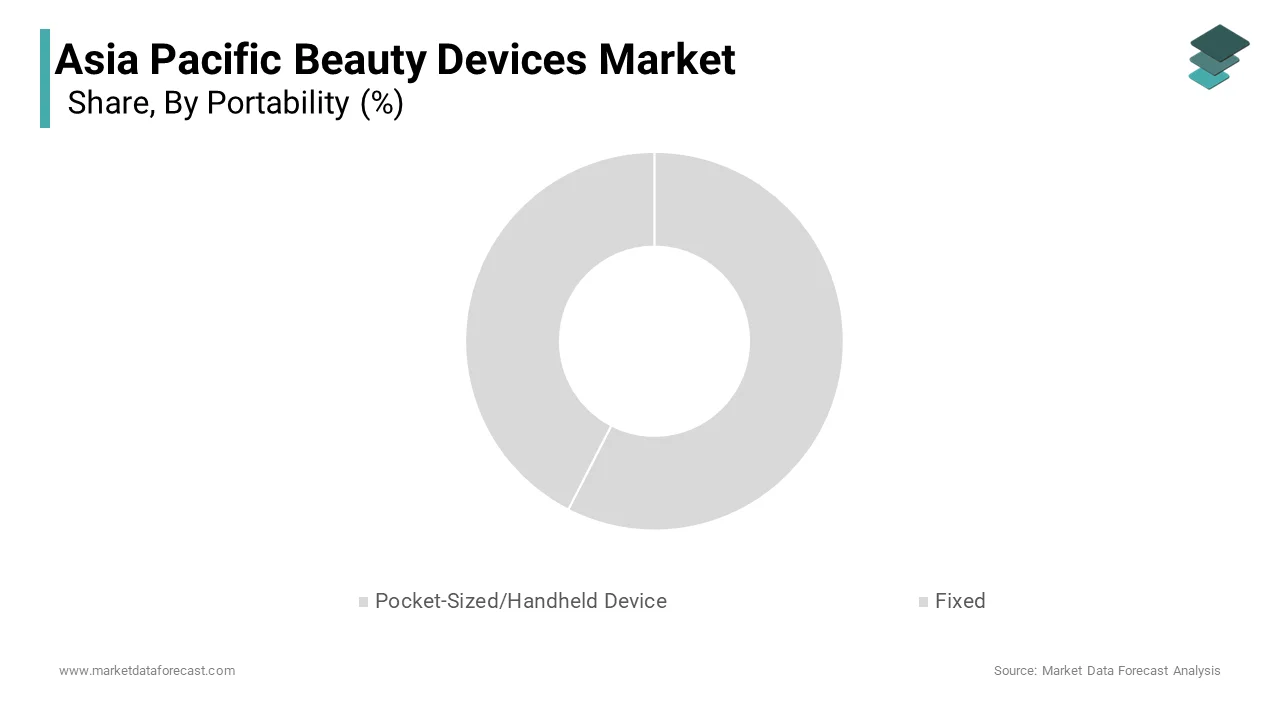

In 2024, the pocket-sized/handheld beauty devices segment accounted for 69.5% of the total Asia Pacific beauty devices market. This dominance is attributed to the growing consumer preference for compact, easy-to-use, and travel-friendly personal care gadgets. The region's increasingly mobile lifestyle and urbanization have fueled demand for on-the-go beauty solutions. One major driver is the rising adoption of at-home beauty treatments. Consumers are opting for handheld devices such as facial rollers, cleansing brushes, LED masks, and microcurrent tools due to convenience and cost-effectiveness compared to professional salon or clinic visits. The increasing integration of smart technology into handheld devices, such as Bluetooth connectivity and app-based control, has further enhanced their appeal.

On the other hand, the fixed beauty devices segment is projected to grow at the highest CAGR of 14.3% from 2025 to 2033. This rapid rise is being driven primarily by the increasing number of beauty clinics and wellness centers across the Asia Pacific region, especially in countries like Japan, South Korea, and Australia. Fixed devices include high-end technologies such as laser systems, radiofrequency machines, and cryolipolysis equipment used for professional treatments, including skin tightening, cellulite reduction, and body contouring. In 2023, the Korean Ministry of Health and Welfare reported that over 1,800 cosmetic clinics were operating nationwide, many of which invested heavily in advanced aesthetic equipment, contributing directly to this segment’s expansion. Another significant factor is the surge in medical tourism for aesthetic procedures. Countries like Thailand and Malaysia have become popular destinations for beauty treatments, attracting international clients seeking safe and affordable options. According to the Medical Council of Thailand, approximately 800,000 tourists visited Thailand for cosmetic procedures in 2022, generating an estimated USD 380 million in revenue . Moreover, government support and regulatory developments are encouraging the use of FDA-approved fixed beauty equipment, enhancing consumer confidence.

By Application Insights

The facial application devices segment held the largest share of the Asia Pacific beauty devices market, i.e., 34.7% of total revenue in 2024. This influence is associated with the widespread concern over facial aesthetics and skincare, particularly among women and increasingly among men. A key driver is the prevalence of acne and uneven skin tone, exacerbated by pollution and poor lifestyle habits. Social media influence also plays a pivotal role. Platforms like Instagram, WeChat, and TikTok have amplified beauty trends across the region. Furthermore, the rise of male grooming cannot be overlooked. Lastly, product innovation continues to stimulate growth. Brands like FOREO and Clarisonic have integrated AI and ultrasonic technology into facial cleansing and toning devices, offering real-time feedback and tailored regimens. These advancements boost both performance and consumer trust, solidifying the facial applications segment as the market leader.

Eye care beauty devices emerged as the fastest expanding segment in the Asia Pacific market, with a projected CAGR of 15.8%. This rapid ascent reflects growing awareness about premature aging around the eyes, worsened by screen exposure and stress-related fatigue. Urban populations in countries like Japan, Singapore, and Australia are increasingly adopting eye massagers, LED eye masks, and cooling jade rollers to address puffiness, dark circles, and fine lines. Consumer interest is also being amplified by celebrity endorsements and K-drama stars promoting under-eye care routines. Besides, clinical validation is driving credibility. Devices incorporating red light therapy and EMS (electrical muscle stimulation) are being marketed with dermatologist-backed claims.

By Mode of Operation Insights

The electric and battery-operated beauty devices captured a substantial share of the Asia Pacific beauty device market in 2024. This overwhelming dominance can be traced back to the increasing demand for automated, effective, and time-efficient beauty solutions, especially among urban professionals and digitally native consumers. A primary driver is the rise of smart beauty technology. Consumers are increasingly investing in electric skin cleansing brushes, LED therapy masks, and microcurrent devices that offer measurable results with minimal effort. This growth is further supported by the proliferation of e-commerce platforms such as Alibaba and Amazon, which make these products easily accessible across rural and urban areas. Moreover, the integration of IoT (Internet of Things) features into beauty devices has transformed personal care routines. Some devices now sync with smartphones via Bluetooth to track usage, provide customized recommendations, and even simulate salon-like experiences at home. According to McKinsey & Company, Asia Pacific leads the world in connected beauty spending, with consumers willing to pay a premium for intelligent, adaptive devices. Additionally, there is a cultural emphasis in markets like South Korea and Japan on achieving flawless skin through advanced technology. This has led to partnerships between electronics manufacturers and beauty companies.

Apart from holding a smaller market share, the manual beauty devices segment is expected to grow at the fastest CAGR of 12.5%. This progress is fueled by a shift toward natural skincare practices and rising concerns about electronic waste. Manual devices such as Gua Sha stones, jade rollers, and dry brushes are gaining traction due to their simplicity, affordability, and eco-friendliness. These users often cite environmental impact as a reason for choosing non-electric alternatives. The global clean beauty movement has also played a crucial role. Consumers are becoming wary of over-reliance on electricity-powered gadgets and are instead turning to age-old techniques rooted in Ayurveda and Traditional Chinese Medicine. Moreover, the post-pandemic focus on self-care and mindfulness has boosted the uptake of manual devices. Yoga studios and meditation centers in cities like Sydney, Bangkok, and Mumbai have begun offering facial massage sessions using Gua Sha tools, integrating them into wellness routines. This has helped create new customer touchpoints beyond traditional beauty retail channels.

COUNTRY LEVEL INSIGHTS

China Beauty Devices Market Analysis

China dominated the Asia Pacific beauty devices market by accounting for 28.4% of total regional revenue in 2024. As one of the most technologically advanced and digitally engaged markets, China is experiencing a boom in beauty tech thanks to rapid urbanization, rising disposable incomes, and strong e-commerce infrastructure. The country’s youth-led beauty culture, coupled with a strong KOL (Key Opinion Leader) economy, drives consumer behavior. Platforms like Xiaohongshu and Douyin (the Chinese version of TikTok) have turned beauty devices into must-have items. Government support for domestic manufacturing is another catalyst. Initiatives like the "Made in China 2025" strategy encourage local innovation, allowing firms like Xiaomi and Meidi to produce affordable yet high-tech beauty devices.

Japan Beauty Devices Market Analysis

Japan is a mature market focused on innovation. Known for its deep-rooted skincare culture and early adoption of beauty technology, Japan stands out for its emphasis on high-quality, scientifically backed products. The country’s aging population has spurred demand for anti-aging and skin-tightening devices. Devices such as galvanic face lifters and RF-based skin toners have seen a surge in popularity. Japanese consumers also prioritize ingredient transparency and brand reputation, pushing manufacturers to integrate advanced Japanese biotechnology into their offerings. Panasonic, for example, launched its nanoe-based facial steamer series in 2023, leveraging patented moisture delivery technology that gained favorable reviews for hydration benefits. Moreover, Japan's strong retail ecosystem, including chains like Tokyu Hands and Don Quijote, ensures the wide availability of beauty devices.

South Korea Beauty Devices Market Analysis

South Korea is a tech-driven growth engine in the Asia Pacific beauty devices market. The nation’s status as a global beauty innovator, known as the epicenter of K-beauty, makes it a vital player in the industry. Korea’s unique blend of skincare obsession and tech advancement fuels the popularity of devices such as LED masks, microcurrent toners, and portable ionizers. Skincare routine complexity is a major driver. Korean consumers often follow multi-step regimens, and they seamlessly incorporate beauty devices as part of their daily practice. The government’s backing of beauty tech incubators and startups has also accelerated market growth. Seoul hosts numerous beauty expos annually, including Cosmoprof Asia, where domestic brands showcase cutting-edge device innovations.

India Beauty Devices Market Analysis

India is an emerging powerhouse with strong growth potential. With a young, aspirational population and a booming middle class, India presents vast untapped potential for beauty tech. Rising disposable income and digital penetration are key drivers. A substantial number of Indians are active internet users, and platforms like Amazon, Flipkart, and Nykaa are aggressively promoting beauty devices through influencer campaigns and discounts. Nykaa reported a major increase in beauty device purchases in 2023, with LED masks and facial massagers being top-selling categories. The influence of Bollywood and social media is also pronounced. Celebrities endorsing brands like O3+ and L'Oréal have normalized the use of beauty gadgets among Indian consumers. Moreover, the growing male grooming business is fueling demand for hair removal and facial cleansing devices. Regulatory bodies like the Bureau of Indian Standards (BIS) are setting quality benchmarks, building consumer trust.

Australia Beauty Devices Market Analysis

Australia and New Zealand are premium markets with high awareness. While smaller in volume compared to China or South Korea, this region is characterized by high consumer awareness and a preference for premium, clinically tested products. The landscape is highly regulated, with the Therapeutic Goods Administration (TGA) overseeing the approval of non-invasive beauty devices. This has fostered a market environment where only high-performing and safe products thrive. In 2023, the Australian Institute of Health and Welfare reported that over 60% of adults consider skincare a regular part of their routine, driving consistent demand for facial and skin treatment tools. Eco-consciousness is another key feature. Consumers in this region favor reusable and energy-efficient devices, supporting the popularity of brands like LightStim and Perricone MD. Retail chains like Priceline and Chemist Warehouse play a critical role in distribution, often partnering with international brands to launch exclusive collections.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific beauty devices market include are

- Nu Skin, Candela Medical

- Silkn

- TRIA BEAUTY

- Curallux LLC.

- Termosalud

- FOREO

- Tech4Beauty

- Koninklijke Philips N.V.

- Conair CorporationLumenis

- Cynosure

- Sciton, Inc.

- Fotona

- Procter & Gamble

- Colgate-Palmolive Company

- LUTRONIC

- STRATA Skin Sciences

- NuFACE

- Spectrum Brands, Inc.

- Cutera

- Merz North America, Inc.

- El. En. S.p.A.

- YA-MAN LTD.

- Panasonic Corporation

- Alma Lasers

- Bausch Health Companies Inc.

MARKET SEGMENTATION

This research report on the Asia Pacific beauty devices market is segmented and sub-segmented into the following categories.

By Application

- Hair

- Facial

- Skin

- Oral

- Eye

By Portability

- Pocket-Sized/Handheld Device

- Fixed

By Mode of Operation

- Electric and Battery Operated

- Manual

By End users

- Beauty Clinics

- Spas

- Salons

- Home

- Commercial/Professional

- Domestic/Personalized/ Homecare

By Distribution Channel

- Direct Sales

- Retail

- Online

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What defines the beauty devices market in APAC, and why is it booming?

Beauty devices include at-home and professional tools like LED masks, RF tightening systems, microcurrent toners, cleansing brushes, and laser hair removers. Surging demand is driven by tech-savvy consumers, K-beauty/J-beauty influence, and the blurring line between skincare and medtech—especially among Gen Z and millennial users.

Which countries lead adoption and innovation?

South Korea and Japan set global trends with cutting-edge R&D (e.g., LG’s Pra.L line, Ya-Man’s esthetic tech), while China dominates volume via e-commerce (Tmall, Douyin livestreams); India and Southeast Asia show fastest growth, fueled by rising middle-class beauty consciousness.

How is ‘skinimalism’ reshaping device preferences?

Consumers now seek multi-functional, dermatologist-backed devices (e.g., 3-in-1 LED + RF + microcurrent) that deliver clinical results at home—prioritizing efficacy, safety certifications, and seamless integration into streamlined routines.

What technologies are gaining traction?

Red/NIR LED phototherapy, bipolar radiofrequency (RF), low-level laser therapy (LLLT), and AI-powered skin analysis (via smartphone integration) lead—while innovations like cryo-microcurrent and iontophoresis for enhanced serum delivery are emerging.

Are regulatory standards harmonizing across APAC?

Not yet—China’s NMPA classifies many devices as Class II medical devices, requiring clinical data; Japan’s PMDA uses quasi-drug and medical device pathways; ASEAN relies on local approvals. This complexity drives partnerships with local distributors for market access.

Who are the key players in the region?

Global brands like FOREO, NuFACE, and Philips dominate premium segments; Korean innovators (YA-MAN, MTG, Dr. Arrivo) lead in high-tech aesthetics; while Chinese disruptors (Amiro, Ulike, Comper) leverage DTC models, viral marketing, and aggressive pricing.

How is e-commerce and social commerce transforming sales?

Livestream demos (e.g., Douyin, Shopee Live), KOL-driven trials, and “try-before-buy” mini devices drive impulse purchases—especially in China and SEA, where 70%+ of beauty device sales occur online.

What role does men’s grooming play in market expansion?

Men’s beauty devices (e.g., beard trimmers with skin sensors, acne-clearing LEDs) are the fastest-growing sub-segment—particularly in urban India, South Korea, and Japan—reflecting shifting gender norms and workplace grooming expectations.

What challenges do brands face in APAC?

Counterfeit products undermining trust, consumer skepticism about at-home efficacy vs. clinic results, and varying electrical/safety standards (voltage, plug types) complicate pan-regional launches.

What’s the market outlook for 2025–2030?

The APAC beauty devices market is projected to grow at >12% CAGR—powered by aging populations seeking non-invasive anti-aging solutions, rising medical aesthetics literacy, and convergence with wearables and personalized skincare ecosystems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com