- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$9.30 BnMarket Estimate, 2026

$9.80 BnMarket Forecast, 2034

$14.87 BnCAGR, 2026–2034

5.35%Executive Summary: Asia Pacific Crane Market

- Market Scope: Comprehensive Asia Pacific crane market analysis covering product categories, application sectors, regional leadership frameworks, and industrial infrastructure expansion trends.

- Market Valuation: Valued at USD 9.30 billion (2025), estimated at USD 9.80 billion (2026), and projected to reach USD 14.87 billion by 2034, registering a robust CAGR of 5.35% (2026–2034).

- Primary Growth Drivers: Massive infrastructure development initiatives, rapid urbanization, industrial expansion across manufacturing and energy sectors, integration of IoT and AI-enabled smart cranes, and rising investments in renewable energy projects. Key challenges include fluctuating raw material costs and skilled labor shortages.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product Type | Mobile cranes (dominated the product segment in 2025 due to versatility in urban construction) | Fixed cranes (projected to grow at a CAGR of 7.8%) |

| By Application | Construction application (held a 44.3% market share in 2025) | Industrial sector (advancing rapidly with a projected CAGR of 8.2%) |

| By Region / Country | China (led regionally with a 40.5% market share in 2025, supported by infrastructure spending and manufacturing) | India (driven by Smart Cities Mission and National Infrastructure Pipeline investments) |

Major Market Players & Market Structure

Market Structure: Highly competitive heavy machinery landscape featuring global giants and regional manufacturers leveraging technological innovation, smart crane integration, and localization strategies.

Key Companies: Konecranes, Zoomlion, Tadano, Caterpillar, Inc., Hitachi Construction Machinery Co., Ltd., Komatsu Ltd., Liebherr-International AG, SANY Group, Terex Corporation, Zoomlion Heavy Industry Science & Technology Co., Ltd., Gorbel Inc., and The Manitowoc Company, Inc.

Asia Pacific Crane Market Size

The Asia Pacific Crane Market is projected to grow from USD 9.30 billion in 2025 to USD 9.80 billion in 2026 and reach USD 14.87 billion by 2034, registering a CAGR of 5.35% from 2026 to 2034.

The Asia Pacific crane market has emerged as a pivotal segment within the global construction and heavy machinery sector, driven by rapid urbanization and industrial expansion. As per data from the International Monetary Fund, the region accounts for over 60% of global urban development projects, creating substantial demand for cranes. China, India, and Southeast Asian nations like Indonesia and Vietnam are at the forefront of this growth, with their governments investing heavily in infrastructure. Additionally, the region's robust manufacturing sector amplifies crane demand in automotive and shipbuilding industries. Japan and South Korea lead in advanced crane technology adoption, contributing to the high-value segment of the market. Such commitments underscore the thriving conditions for crane manufacturers. However, challenges like fluctuating raw material costs and stringent environmental regulations persist is influencing market dynamics.

MARKET DRIVERS

Infrastructure Development

Infrastructure development stands as a cornerstone driving the Asia Pacific crane market, propelled by government-led initiatives and private investments. For instance, China’s Beltand Road Initiative has already allocated over 900 billion across various infrastructure projects, significantly boosting crane demand. Similarly, India’s Smart Cities Mission aims to develop 100 smart cities by requiring heavy lifting equipment for construction. Mobile cranes are witnessing heightened adoption due to their versatility in handling diverse infrastructure needs. Additionally, urban migration trends, as outlined by the United Nations, project that 68% of Asia’s population will reside in urban areas by 2050. This demographic shift amplifies the need for residential and commercial buildings, further bolstering crane utilization.

Industrial Expansion

Industrial expansion is another critical driver propelling the Asia Pacific crane market in sectors like manufacturing, energy, and logistics. According to the World Bank, the manufacturing sector in Asia Pacific contributes approximately 35% to the region’s GDP, which is necessitating advanced machinery for operational efficiency. In countries like Japan and South Korea, the demand for specialized cranes is surging due to their dominance in automotive and electronics manufacturing. For example, South Korea’s Hyundai Heavy Industries utilizes crawler cranes extensively in its shipbuilding operations.

Energy projects, including renewable energy installations, also play a significant role. The International Renewable Energy Agency reports that Asia Pacific accounted for 57% of global renewable energy capacity additions in 2022. Wind turbine installations, such as those in China and India, often require large crawler and tower cranes, contributing to market growth. Furthermore, the rise of e-commerce has spurred warehouse construction and logistics hubs, increasing crane usage.

MARKET RESTRAINTS

Fluctuating Raw Material Costs

Fluctuating raw material costs pose a significant restraint to the Asia Pacific crane market by affecting both manufacturers and end-users. Steel, a primary component in crane production, has experienced volatile pricing due to geopolitical tensions and supply chain disruptions. According to the World Steel Association, steel prices surged by nearly 25% in 2022 alone by impacting crane manufacturing costs. This volatility forces manufacturers to either absorb higher expenses or pass them on to customers by leading to reduced affordability and slower adoption rates.

Moreover, the dependency on imported raw materials exacerbates the issue for countries like India and Vietnam. For instance, as per the Federation of Indian Chambers of Commerce and Industry, India imports approximately 30% of its steel requirements by making it vulnerable to price fluctuations. These cost uncertainties create hesitancy among buyers, especially small and medium enterprises, who constitute a significant portion of the crane market. Additionally, inflationary pressures compound the problem by reducing overall purchasing power.

Stringent Environmental Regulations

Stringent environmental regulations present another major restraint for the Asia Pacific crane market as governments intensify efforts to combat climate change. According to the United Nations Environment Programme, countries like China and India have introduced strict emission norms for industrial equipment, including cranes. For instance, China’s National VI emission standards mandate the use of cleaner technologies, which is compelling manufacturers to redesign existing models or invest in new technologies. This regulatory shift increases compliance costs and extends product development timelines that is impacting profitability.

Furthermore, the push for sustainable practices influences customer preferences, favoring eco-friendly alternatives. While this benefits the environment, it creates barriers for traditional crane manufacturers struggling to adapt. Additionally, the lack of awareness about sustainable options among smaller players limits market penetration. These regulatory pressures, coupled with the need for technological upgrades are restraining the market growth by forcing stakeholders to balance innovation with affordability in an increasingly regulated environment.

MARKET OPPORTUNITIES

Adoption of Advanced Technologies

The adoption of advanced technologies presents a transformative opportunity for the Asia Pacific crane market by enabling manufacturers to enhance efficiency and cater to evolving customer demands. According to PwC, the integration of IoT and AI in heavy machinery is projected to boost productivity by up to 20%, offering a competitive edge. For instance, smart cranes equipped with sensors and real-time monitoring systems are gaining traction in countries like Japan and South Korea, where precision and safety are paramount. These technologies enable predictive maintenance by reducing downtime and operational costs.

China, a leader in digital innovation, is spearheading the adoption of autonomous cranes in ports and construction sites. Additionally, remote-controlled cranes are becoming essential in hazardous environments, such as mining and offshore oil rigs by enhancing worker safety. The proliferation of 5G networks further accelerates this trend, facilitating seamless connectivity. By embracing these advancements, manufacturers can tap into lucrative segments, such as automated logistics hubs and smart infrastructure projects is positioning themselves at the forefront of technological evolution while unlocking new revenue streams.

Rising Investments in Renewable Energy

Rising investments in renewable energy projects offer a significant growth avenue for the Asia Pacific crane market, driven by the region’s commitment to sustainability. This expansion necessitates heavy lifting equipment, particularly tower and crawler cranes, for constructing wind turbines and solar farms. For example, India’s target to achieve 500 GW of renewable energy capacity by 2030 will require extensive crane deployment by creating a robust demand pipeline.

China’s dominance in the solar panel manufacturing sector drives the need for specialized cranes in production facilities. Offshore wind projects in Vietnam and Taiwan, further amplify crane demand due to their complex installation requirements. The crane manufacturers can capitalize on these investments by fostering partnerships with energy companies and securing long-term contracts. This synergy not only diversifies revenue streams but also reinforces the market’s resilience amid shifting economic landscapes.

MARKET CHALLENGES

Intense Market Competition

Intense market competition poses a formidable challenge for the Asia Pacific crane market with the presence of numerous domestic and international players vying for market share. According to Frost & Sullivan, the region hosts over 100 crane manufacturers by ranging from small-scale enterprises to multinational corporations. This overcrowded landscape results in price wars by eroding profit margins and straining smaller players. For instance, Chinese manufacturers dominate the market with cost-effective offerings by leveraging economies of scale to undercut competitors.

India and Southeast Asia witness similar dynamics, where local players struggle to compete with established brands. A study by the Confederation of Indian Industry reveals that price sensitivity among buyers exacerbates the issue, with 60% of customers prioritizing cost over quality. Additionally, the lack of product differentiation limits growth opportunities, forcing companies to focus on aggressive marketing strategies rather than innovation. Intellectual property disputes further complicate the scenario, as highlighted by the World Intellectual Property Organization, with allegations of design infringements being common. These competitive pressures hinder profitability and stifle technological advancements, which is challenging manufacturers to strike a balance between affordability and innovation to remain relevant in the market.

Skilled Labor Shortages

Skilled labor shortages represent another pressing challenge for the Asia Pacific crane market, undermining operational efficiency and hindering growth. According to the International Labour Organization, the construction and heavy machinery sector faces a deficit of skilled operators, particularly in emerging economies like India and Indonesia. For instance, a survey by the Associated Chambers of Commerce and Industry of India reveals that nearly 40% of construction projects experience delays due to a lack of trained crane operators. This shortage is exacerbated by the rapid pace of infrastructure development, which outstrips workforce availability.

Furthermore, the complexity of modern cranes, equipped with advanced technologies, requires specialized training, which is often inaccessible to workers in rural areas. This scarcity not only impacts project timelines but also increases operational risks, as untrained personnel are more prone to accidents. To address this challenge, industry stakeholders must collaborate with educational institutions and government bodies to establish comprehensive training initiatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | Caterpillar, Inc., Hitachi Construction Machinery Co., Ltd. (Hitachi, Ltd.), Komatsu Ltd. |

SEGMENTAL ANALYSIS

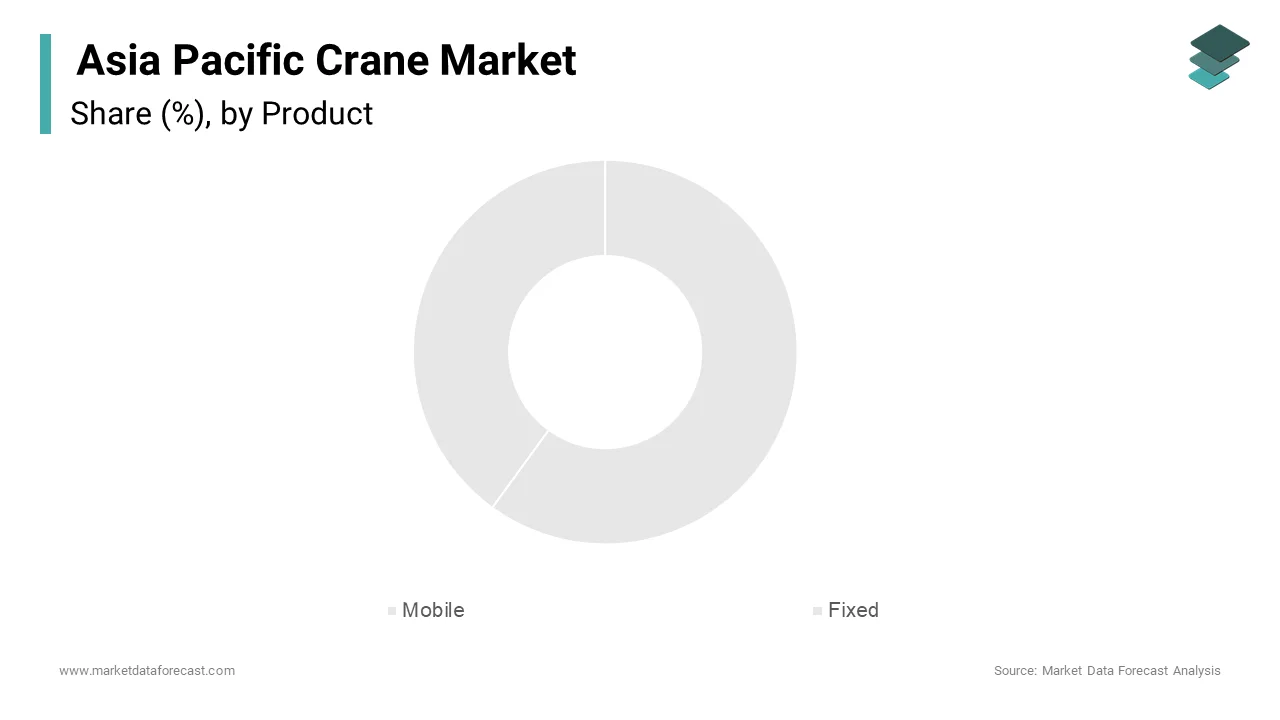

By Product Insights

The mobile cranes segment was the largest by capturing significant share of the Asia Pacific crane market in 2025 due to their versatility and adaptability across diverse applications by ranging from urban construction to heavy industrial projects. According to the United Nations, urban areas in Asia Pacific are expected to house an additional 1.2 billion people by 2050 with extensive infrastructure development. Mobile cranes, with their ability to navigate tight spaces and deliver high lifting capacities, are indispensable for such projects. Another driving factor is the proliferation of road and rail networks. Mobile cranes play a pivotal role in these projects due to their mobility and efficiency. For instance, China’s railway expansion plans, including the construction of over 30,000 kilometers of high-speed rail, rely heavily on mobile cranes. Additionally, advancements in crane technology, such as remote operation and automation that further enhance their appeal. These innovations reduce operational risks and improve productivity by making mobile cranes the preferred choice for contractors.

The fixed cranes segment is swiftly emerging with a projected CAGR of 7.8% in the next coming years. This growth is fueled by the booming construction of high-rise buildings and industrial facilities in densely populated urban centers. For example, India’s Smart Cities Mission aims to construct vertical residential and commercial spaces by creating immense demand for fixed cranes. The Confederation of Indian Industry estimates that over 100 million square meters of high-rise construction will be completed by 2025.

Another factor accelerating growth is the rise of renewable energy projects. According to the International Renewable Energy Agency, Asia Pacific accounted for 57% of global renewable energy capacity additions in 2022. Wind turbine installations, which require specialized tower cranes, are a significant contributor. For instance, Vietnam’s offshore wind projects utilize fixed cranes for turbine assembly, propelling regional demand. Additionally, stringent safety regulations favor fixed cranes, as they offer greater stability compared to mobile variants.

By Application Insights

The construction sector held 44.3% of the Asia Pacific crane market share in 2025 with the unprecedented infrastructure spending across the region. Urban migration trends also contribute significantly to this dominance. According to the World Bank, urban populations in Asia Pacific are growing at an annual rate of 2.3%, which is creating demand for residential and commercial buildings. High-rise construction relies heavily on cranes for material handling and structural assembly. For example, South Korea’s Seoul Metropolitan Government plans to construct over 500 skyscrapers by 2030 by requiring advanced crane solutions. Additionally, government initiatives like affordable housing programs amplify crane demand.

The industrial sector is lucratively growing with a projected CAGR of 8.2% in the next coming years. This growth is propelled by the region’s expanding manufacturing base in automotive, electronics, and shipbuilding industries. For instance, Japan’s automotive sector, led by companies like Toyota and Honda, utilizes overhead and gantry cranes extensively in production lines, driving demand. Similarly, South Korea’s shipbuilding industry, dominated by Hyundai Heavy Industries, relies on heavy-duty cranes for vessel assembly. Another key driver is the rise of e-commerce and logistics hubs. Countries like Singapore and Australia are investing heavily in automated warehouses, further boosting crane adoption. Additionally, technological advancements, such as IoT-enabled cranes, enhance operational efficiency in industrial settings.

COUNTRY LEVEL ANALYSIS

China was the top performer in the Asia Pacific crane market with 40.5% of share in 2025. The country’s dominance is underpinned by massive infrastructure investments and its position as a global manufacturing hub. For instance, China’s 14th Five-Year Plan allocates over $1.4 trillion for infrastructure projects, including high-speed rail and smart cities, creating robust crane demand. Additionally, the Belt and Road Initiative has spurred international projects that is amplifying domestic crane production. Technological advancements also play a crucial role. According to Deloitte, China leads in adopting AI and IoT-enabled cranes by enhancing efficiency and safety. For example, Shanghai Zhenhua Heavy Industries Co., Ltd. produces cutting-edge port cranes used globally. Moreover, the country’s focus on renewable energy drives demand for specialized cranes.

India positioned second in holding 15.4% of the Asia Pacific crane market share in 2025 due to the rapid urbanization and infrastructure push are key drivers. For example, the Smart Cities Mission aims to develop 100 smart cities by requiring extensive crane usage. Additionally, the government’s National Infrastructure Pipeline envisions investments exceeding $1.4 trillion by 2025.

Industrial growth also contributes significantly. Tata Projects and Larsen & Toubro are major consumers of cranes for large-scale projects. Furthermore, renewable energy initiatives drive demand. The Ministry of New and Renewable Energy targets 500 GW of renewable capacity by 2030, which is requiring advanced cranes for wind and solar installations.

Japan is likely to have steady growth rate in the next coming years with the advanced manufacturing sector and technological prowess are key contributors. For instance, Japan’s automotive giants, such as Toyota and Nissan, utilize state-of-the-art cranes in production lines, driving demand. Additionally, the shipbuilding industry, led by Mitsubishi Heavy Industries, relies heavily on heavy-duty cranes. Another significant factor is the government’s focus on disaster-resilient infrastructure. Urban redevelopment projects, such as Tokyo’s skyline transformation ahead of the 2020 Olympics.

South Korea crane market is likely to have the steady growth opportunities in the forecast period due to its robust shipbuilding and electronics sectors. For example, Hyundai Heavy Industries and Samsung Heavy Industries utilize advanced cranes for constructing vessels and offshore rigs. Similarly, Samsung Electronics and LG rely on cranes for manufacturing facilities. Government-led infrastructure projects also play a vital role. According to the Korean Ministry of Land, Infrastructure, and Transport, investments in smart city projects exceed $100 billions by creating substantial crane demand. Additionally, South Korea’s focus on renewable energy drives growth. The International Renewable Energy Agency reports that the country aims to achieve 20% renewable energy capacity by 2030 with specialized cranes.

Australia and New Zealand are having prominent growth opportunities in the next coming years. The region’s mining and infrastructure sectors are key drivers. For instance, Australia’s mining boom, particularly in iron ore and coal, requires heavy-duty cranes for operations. BHP and Rio Tinto are major consumers of such equipment.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Asia Pacific Crane Market are Caterpillar, Inc., Hitachi Construction Machinery Co., Ltd. (Hitachi, Ltd.), Komatsu Ltd., Liebherr-International AG, SANY Group, Terex Corporation, Zoomlion Heavy Industry Science & Technology Co., Ltd., Gorbel Inc., Tadano Ltd., The Manitowoc Company, Inc.

The Asia Pacific crane market is characterized by intense competition with the presence of both global giants and regional players vying for dominance. Established companies like Konecranes, Zoomlion, and Tadano leverage their technological expertise and extensive distribution networks to maintain its dominance. Meanwhile, local manufacturers compete aggressively on pricing, offering cost-effective solutions tailored to budget-conscious customers. The market’s competitive landscape is further shaped by rapid urbanization and industrial growth, which amplify demand but also intensify rivalry. To differentiate themselves, players focus on innovation, introducing smart cranes equipped with IoT and AI capabilities. Sustainability initiatives, such as low-emission designs, are also gaining traction amid stricter environmental regulations. Collaborations with governments and participation in mega-projects further escalates5taz wfRM; the strategic maneuvers undertaken by key participants. This dynamic environment fosters continuous advancements by ensuring the market remains vibrant yet challenging for stakeholders.

Top Players in the Market

Konecranes

Konecranes has established itself as a key player in the Asia Pacific crane market through its innovative product portfolio and commitment to sustainability. The company specializes in industrial cranes, port solutions, and service offerings tailored to meet the region's growing infrastructure and manufacturing demands. Its focus on smart technologies, such as IoT-enabled cranes, has strengthened its appeal among customers seeking efficiency and safety. In recent years, Konecranes launched its "Lifecyle Care" program, offering predictive maintenance services that reduce downtime and enhance operational reliability.

Zoomlion Heavy Industry Science & Technology Co., Ltd.

Zoomlion has emerged as a dominant force in the Asia Pacific crane market, leveraging its expertise in mobile and crawler cranes. The company’s emphasis on R&D has resulted in cutting-edge products designed for urban construction and heavy industrial applications. Zoomlion’s introduction of hybrid-powered cranes aligns with the region’s push for sustainable solutions, enhancing its competitive edge. Recently, the company expanded its production facilities in India and Thailand to cater to rising demand.

Tadano Ltd.

Tadano is renowned for its advanced crane technologies and robust presence in the Asia Pacific market. The company focuses on delivering high-performance mobile and all-terrain cranes, which are widely used in construction and mining sectors. Tadano’s commitment to innovation is evident in its development of lightweight yet durable crane models, ideal for urban environments. To bolster its position, Tadano recently entered into partnerships with e-commerce giants to supply cranes for warehouse automation projects. Furthermore, the company has invested in training programs for operators, ensuring safer and more efficient crane usage.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific crane market employ diverse strategies to maintain their competitive edge. Innovation and technology integration rank among the most prominent approaches, with companies investing heavily in IoT, AI, and automation to enhance crane efficiency and safety. Strategic partnerships and collaborations are also widely adopted, enabling firms to tap into emerging markets and secure contracts for large-scale projects. For instance, alliances with government bodies facilitate participation in infrastructure initiatives. Another critical strategy is localization, where manufacturers establish regional production hubs to reduce costs and improve supply chain resilience. Sustainability-focused measures, such as developing eco-friendly crane models, further strengthen market positioning. Lastly, after-sales services, including predictive maintenance and operator training, play a pivotal role in fostering customer loyalty and driving repeat business.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Konecranes launched its Smart Crane Technology Suite in Australia, integrating AI-driven analytics to optimize crane performance and reduce operational costs for customers.

- In June 2023, Zoomlion inaugurated a new manufacturing facility in Thailand, enhancing its production capacity to meet rising demand for mobile cranes in Southeast Asia.

- In August 2023, Tadano partnered with Singapore-based logistics firms to supply advanced cranes for automated warehousing systems, aligning with the e-commerce boom.

- In October 2023, Liebherr introduced hybrid-powered tower cranes in India by targeting renewable energy projects and addressing sustainability concerns.

- In December 2023, Sany Heavy Industry expanded its service network in Indonesia by offering comprehensive maintenance solutions to boost customer satisfaction and retention.

MARKET SEGMENTATION

This research report on the asia pacific crane market has been segmented and sub-segmented into the following.

By Product

- Mobile

- Fixed

By Application

- Construction

- Mining

- Industrial, Oil & Gas

By Country

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Indonesia

- Philippines

- Vietnam

- Singapore

- Rest of APAC