Asia Pacific Digital Advertising Market Size, Share, Trends & Growth Forecast Report By Platform (Computer, Smartphone), Format, Offering, Type, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Digital Advertising Market Size

The Asia Pacific digital advertising market size was calculated to be USD 110.58 million in 2024 and is anticipated to be worth USD 422.90 million by 2033, from USD 128.38 million in 2025, growing at a CAGR of 16.07% during the forecast period.

The Asia Pacific digital advertising market growth is driven by the rapid internet penetration and the proliferation of smartphones. According to the International Telecommunication Union, over 60% of the region’s population is now connected to the internet by creating a fertile ground for digital ad campaigns. Government initiatives promoting digital literacy further accelerate growth.

MARKET DRIVERS

Rising Internet Penetration and Smartphone Usage

The exponential rise in internet penetration and smartphone usage serves as a primary driver for the Asia Pacific digital advertising market with the region’s growing digital economy. According to the International Telecommunication Union, over 2 billion new internet users have been added in the region since 2015, which is creating immense demand for targeted advertising. Government support further amplifies this trend. As per the Ministry of Electronics and Information Technology in India, subsidies for digital infrastructure have increased by 25% since 2020 by ensuring widespread connectivity. Additionally, the proliferation of affordable smartphones in rural areas creates new opportunities for advertisers.

Growth of E-commerce Platforms

The rapid expansion of e-commerce platforms is another critical driver propelling the Asia Pacific digital advertising market. For instance, China’s Alibaba and JD.com invest heavily in programmatic advertising to enhance customer acquisition and retention. The rise of social commerce further amplifies adoption. According to the PwC, over 70% of consumers in the region discover products through social media platforms like TikTok and Instagram, which is driving demand for influencer marketing and native ads. Additionally, sectors like fashion and electronics rely on digital ads for personalized recommendations by enhancing user engagement.

MARKET RESTRAINTS

Data Privacy Concerns and Regulatory Challenges

Data privacy concerns and stringent regulatory frameworks pose significant restraints to the Asia Pacific digital advertising market by undermining advertiser confidence and hindering growth. According to the International Association of Privacy Professionals, over 70% of companies in the region cite compliance with data protection laws as a major barrier to executing effective ad campaigns. For instance, China’s Personal Information Protection Law (PIPL) mandates strict guidelines on data collection, which limits the ability of advertisers to leverage consumer insights for targeted campaigns. Similarly, India’s proposed Digital Personal Data Protection Bill imposes penalties for non-compliance by deterring smaller players from adopting advanced ad technologies. Moreover, high-profile data breaches exacerbate the issue. While larger corporations can invest in advanced encryption and consent management systems, smaller firms often lack the resources to mitigate risks effectively.

Ad Fraud and Misinformation

Ad fraud and misinformation present another major restraint for the Asia Pacific digital advertising market as brands seek transparency and authenticity in their campaigns. For instance, click farms and bot traffic in countries like Vietnam and Indonesia undermine the effectiveness of pay-per-click campaigns, which leads to wasted budgets and reduced ROI. Additionally, the spread of misinformation amplifies skepticism among consumers. As per a report by the Reuters Institute, over 60% of users in the region distrust online ads due to misleading content forcing brands to adopt stricter verification measures. While larger firms can implement AI-driven fraud detection systems, smaller advertisers often struggle to address these challenges.

MARKET OPPORTUNITIES

Expansion of Programmatic Advertising

The expansion of programmatic advertising presents a transformative opportunity for the Asia Pacific digital advertising market by enabling brands to deliver hyper-targeted campaigns with precision and efficiency. For instance, South Korea’s gaming industry utilizes programmatic platforms to target niche audiences by enhancing user acquisition and engagement. China, a leader in digital innovation, is spearheading the adoption of programmatic solutions in e-commerce. As per Deloitte, over 60% of Chinese advertisers now rely on programmatic tools to optimize ad spend and improve ROI. Additionally, industries like retail and healthcare utilize real-time bidding to deliver personalized content by driving demand for scalable ad technologies.

Rising Adoption of Video and Interactive Ads

The rising adoption of video and interactive ads offers significant growth avenues for the Asia Pacific digital advertising market, driven by the region’s preference for engaging and immersive content. According to PwC, video ad spending in the region is expected to exceed $50 billion annually by 2025, fueled by platforms like YouTube and TikTok. For example, India’s entertainment sector leverages short-form videos to capture audience attention by enhancing brand recall and conversion rates. Similarly, the proliferation of augmented reality (AR) and virtual reality (VR) creates new opportunities. Additionally, interactive ads enable consumers to engage directly with brands, fostering deeper connections. The fostering partnerships with tech firms and securing long-term contracts by aligning with these trends, advertisers can capitalize on shifting consumer preferences.

MARKET CHALLENGES

Intense Market Competition

Intense market competition poses a formidable challenge for the Asia Pacific digital advertising market by the presence of numerous domestic and international players vying for dominance. According to Frost & Sullivan, the region hosts over 500 ad tech companies ranging from small-scale startups to multinational corporations. This overcrowded landscape results in price wars, eroding profit margins, and straining smaller players. For instance, Google and Facebook dominate the market with cost-effective offerings, leveraging economies of scale to undercut competitors.

India and Southeast Asia witness similar dynamics, where local players struggle to compete with established brands. A study by the Confederation of Indian Industry reveals that price sensitivity among advertisers exacerbates the issue, with 60% of clients prioritizing cost over quality. Additionally, the lack of product differentiation limits growth opportunities, which is forcing companies to focus on aggressive marketing strategies rather than innovation. Intellectual property disputes further complicate the scenario, as per the World Intellectual Property Organization, with allegations of design infringements being common.

Skilled Labor Shortages

Skilled labor shortages represent another pressing challenge for the Asia Pacific digital advertising market by undermining operational efficiency and hindering growth. According to the International Labour Organization, the digital marketing sector faces a deficit of skilled professionals in emerging economies like India and Indonesia. For instance, a survey by the Associated Chambers of Commerce and Industry of India reveals that nearly 40% of ad campaigns experience delays due to a lack of trained personnel. This shortage is exacerbated by the rapid pace of technological advancements, which outstrips workforce availability.

Furthermore, the complexity of modern ad platforms requires specialized training, which is often inaccessible to workers in rural areas. This scarcity not only impacts campaign timelines but also increases operational risks, as untrained personnel are more prone to errors. To address this challenge, industry stakeholders must collaborate with educational institutions and government bodies to establish comprehensive training initiatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 16.07% |

| Segments Covered | By Platform, Format, Offering, Type, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of Asia-Pacific |

| Market Leaders Profiled | Google, Meta, Alibaba Group, Baidu, Tencent, ByteDance, Adobe, Dentsu Inc., Rakuten Advertising, InMobi, SEA Group, Line Corporation |

SEGMENTAL ANALYSIS

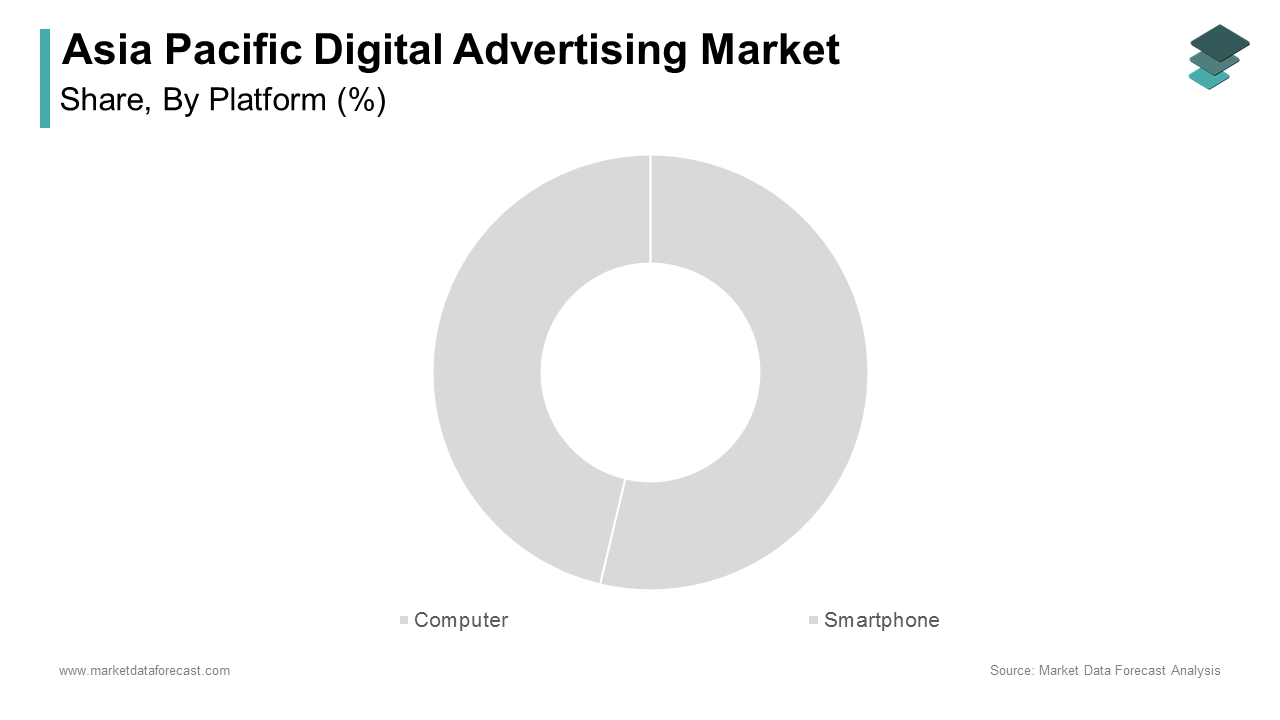

By Platform Insights

Smartphone advertising dominated the Asia Pacific digital advertising market with a significant share in 2024 with the region’s rapid smartphone adoption and mobile-first consumer behavior. According to the International Telecommunication Union, over 2 billion new smartphone users have been added in the region since 2015 creating immense demand for mobile ad campaigns. Government initiatives further amplify this trend. As per the Ministry of Electronics and Information Technology in India, subsidies for digital infrastructure have increased by 25% since 2020 by ensuring widespread connectivity. Additionally, the proliferation of affordable smartphones, particularly in rural areas, creates new opportunities for advertisers.

The computer-based advertising segment is likely to grow with a CAGR of 12.3% in the coming years. The growth of the segment is attributed to be driven by the increasing use of desktops for professional and educational purposes, particularly in urban centers. For example, South Korea’s gaming industry utilizes computer-based ads to target niche audiences by enhancing user acquisition and engagement. The rise of remote work and online education further amplifies adoption. Additionally, industries like finance and healthcare rely on computer ads for personalized recommendations by driving demand for scalable solutions.

By Format Insights

Video advertising dominated the Asia Pacific digital advertising market by holding 45.4% of the share in 2024 due to the region’s preference for engaging and immersive content among younger demographics. According to PwC, video ad spending in the region is projected to exceed $50 billion annually by 2025, fueled by platforms like YouTube and TikTok. For instance, India’s entertainment sector leverages short-form videos to capture audience attention by enhancing brand recall and conversion rates. Additionally, the proliferation of augmented reality (AR) and virtual reality (VR) creates new opportunities. AR-based ads are particularly in sectors like fashion and real estate.

The interactive ads segment is projected to witness a significant CAGR of 15.8% in the next coming years due to their ability to foster deeper connections with consumers through engagement features like quizzes, polls, and clickable elements. For example, China’s retail sector utilizes interactive ads to enhance customer experiences, driving regional demand. The rise of social commerce further amplifies adoption. Additionally, sectors like travel and hospitality rely on interactive formats to provide immersive experiences, which is driving demand for scalable technologies.

By Offering Insights

The digital advertising solutions dominated the Asia Pacific market with a dominant share in 2024 with the region’s focus on cost-effective and scalable tools to execute targeted campaigns. According to Statista, over 80% of advertisers in the region now rely on programmatic solutions to optimize ad spending and improve ROI. For instance, South Korea’s gaming industry utilizes AI-driven solutions to target niche audiences by enhancing user acquisition and engagement. Government support further amplifies this trend. Additionally, industries like retail and healthcare utilize real-time bidding to deliver personalized content with the demand for scalable technologies.

The digital advertising services segment is projected to register a CAGR of 14.5% throughout the forecast period with the increasing demand for managed services, including consulting, campaign management, and analytics, among small and medium enterprises (SMEs). The proliferation of hybrid work models further amplifies adoption. As per PwC, over 60% of companies in the region have implemented remote collaboration tools, necessitating specialized ad services. Additionally, industries like finance and manufacturing rely on data-driven insights to optimize ad performance, driving demand for tailored solutions.

By Type Insights

The search advertising segment dominated the Asia Pacific digital advertising market with 55.3% of the share in 2024 with its precision and ability to deliver highly targeted campaigns based on user intent. For instance, China’s e-commerce sector relies heavily on search ads to drive traffic and conversions by enhancing ROI for advertisers. Government initiatives further amplify this trend. Additionally, sectors like travel and education utilize search ads to capture high-intent users, driving demand for scalable solutions.

The banner advertising segment is lucratively to grow with a CAGR of 13.2% in the next coming years with the advancements in creative design and targeting capabilities by enabling brands to deliver visually appealing and contextually relevant ads. For example, Japan’s fashion industry utilizes dynamic banner ads to showcase seasonal collections. The rise of programmatic advertising further amplifies adoption. Additionally, sectors like automotive and electronics rely on banner ads for brand awareness, driving demand for innovative formats.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific digital advertising market with 40.3% of the share in 2024 with its massive digital economy and stringent localization laws. For instance, China’s Personal Information Protection Law (PIPL) mandates strict guidelines on data collection by creating robust demand for domestic ad platforms like Alibaba and Tencent. Government support further amplifies growth. According to the Ministry of Industry and Information Technology, subsidies for digital infrastructure have increased by 30% since 2020 by ensuring widespread adoption. Collaborations with global players like Google and Facebook strengthen its technological edge.

India was positioned next to China by holding 20.3% of the Asia Pacific digital advertising market share in 2024 owing to the country’s rapid digitalization and startup ecosystem drive demand for scalable ad solutions. The proliferation of affordable smartphones further amplifies adoption. For instance, Flipkart and Amazon India rely heavily on mobile ads to manage consumer data by reducing operational costs. Additionally, partnerships with domestic providers like Tata Consultancy Services bolster supply chain resilience.

Japan’s digital advertising market growth is driven by its expertise in advanced technologies, particularly in sectors like automotive and electronics manufacturing. For instance, Toyota and Sony utilize programmatic ads extensively in production lines by enhancing precision and energy efficiency. Government initiatives play a pivotal role.

South Korea digital advertising market growth is driven by its dominance in the gaming and entertainment sectors. For example, Nexon and NCSoft rely heavily on video ads for delivering seamless online experiences. Government support further amplifies growth. According to the Ministry of Science and ICT, investments in 5G infrastructure have increased by 40% since 2020 by ensuring access to advanced technologies. Collaborations with domestic players like Naver Cloud bolster supply chain resilience.

Australia and New Zealand’s growth is driven by its focus on sustainability and renewable energy projects. Government initiatives further amplify growth. Collaborations with global players like Google Cloud ensure access to cutting-edge systems.

LEADING PLAYERS IN THE ASIA PACIFIC DIGITAL ADVERTISING MARKET

Google is a dominant player in the Asia Pacific digital advertising market, renowned for its robust ad platforms like Google Ads and YouTube. The company leverages AI-driven tools to deliver hyper-targeted campaigns, catering to industries like e-commerce, travel, and entertainment. Recently, Google expanded its programmatic ad offerings in India, enabling small businesses to access cost-effective solutions. Additionally, partnerships with local agencies enhance accessibility for regional advertisers.

Facebook (Meta Platforms)

Facebook, now part of Meta Platforms, plays a pivotal role in the Asia Pacific digital advertising market, offering immersive ad formats through platforms like Instagram and WhatsApp. Meta’s focus on video and interactive ads aligns with regional consumer preferences, particularly among younger demographics. Recently, Meta introduced AR-based ad tools in South Korea, enhancing user engagement for fashion and retail brands. Collaborations with e-commerce firms further solidify its position.

Alibaba Group

Alibaba Group is a key force in the Asia Pacific digital advertising market, particularly in China, where its platforms like Taobao and Tmall dominate e-commerce advertising. Its Uni Marketing solution enables brands to execute data-driven campaigns across multiple touchpoints. Recently, Alibaba expanded its ad tech capabilities in Southeast Asia, targeting SMEs through Lazada. The company also partnered with government bodies to ensure compliance with data localization laws. Alibaba continues to expand its influence in the regional market by prioritizing scalability and localization strategies.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Asia Pacific digital advertising market employ diverse strategies to maintain their competitive edge. Innovation and R&D investments rank among the most prominent approaches, with companies developing AI-driven and programmatic ad solutions. Strategic partnerships and collaborations are also widely adopted, enabling firms to tap into emerging markets and secure contracts for large-scale projects. Localization efforts, such as creating region-specific ad formats, reduce barriers and improve accessibility. Sustainability-focused measures, such as developing eco-friendly ad platforms, further strengthen market positioning. Lastly, after-sales services, including campaign analytics and optimization support, play a pivotal role in fostering customer loyalty and driving repeat business.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific Digital Advertising Market include Google, Meta, Alibaba Group, Baidu, Tencent, ByteDance, Adobe, Dentsu Inc., Rakuten Advertising, InMobi, SEA Group, and Line Corporation.

The Asia Pacific digital advertising market is characterized by intense competition, driven by the presence of global giants and regional players vying for dominance. Established companies like Google, Meta Platforms, and Alibaba leverage their technological expertise and extensive distribution networks to maintain their dominance. Meanwhile, local manufacturers compete aggressively on pricing, offering cost-effective solutions tailored to budget-conscious customers. The market’s competitive landscape is further shaped by rapid technological advancements and government initiatives aimed at boosting digital infrastructure. To differentiate themselves, players focus on innovation, introducing cutting-edge products for AI, programmatic, and video advertising. Sustainability initiatives, such as low-emission data centers, are also gaining traction amid stricter environmental regulations. Collaborations with governments and participation in mega-projects further underscore the strategic maneuvers undertaken by key participants.

RECENT HAPPENING IN THE MARKET

- In March 2023, Google expanded its programmatic ad offerings in India by enabling small businesses to access cost-effective digital marketing solutions and enhancing regional adoption.

- In May 2023, Meta Platforms introduced AR-based ad tools in South Korea by targeting fashion and retail brands with immersive ad experiences to boost user engagement.

- In July 2023, Alibaba Group partnered with Lazada to expand its ad tech capabilities in Southeast Asia by targeting SMEs through localized ad solutions.

- In September 2023, Tencent launched its "AI-Driven Ad Optimization" platform in China, which enhances precision and efficiency for e-commerce advertisers.

- In November 2023, Naver Cloud collaborated with South Korean gaming firms to develop interactive ad formats by enhancing scalability and security for advertisers.

MARKET SEGMENTATION

This research report on the Asia Pacific digital advertising market has been segmented and sub-segmented based on platform, format, offering, type, and region.

By Platform

- Computer

- Smartphone

By Format

- Text

- Image

- Video

By Offering

- Solution

- Services

By Type

- Search Advertising

- Banner Advertising

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is driving the growth of the digital advertising market in Asia Pacific?

Rapid smartphone penetration, increased internet usage, expanding e-commerce sector, and growing social media adoption are major drivers of digital advertising in the region.

2. Which formats are most popular in digital advertising across Asia Pacific?

Display ads, video ads, search engine marketing (SEM), social media advertising, and mobile in-app advertising are among the most widely used formats.

3. Who are the key players in the Asia Pacific digital advertising market?

Major players include Google, Meta (Facebook), Alibaba Group, Tencent, ByteDance (TikTok), Baidu, Adobe, Dentsu Inc., and Rakuten Advertising.

4. How is programmatic advertising evolving in Asia Pacific?

Programmatic advertising is gaining traction with increasing automation, real-time bidding, and the use of AI and machine learning to optimize ad delivery and targeting.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com