Asia Pacific Dough Conditioners Market Size, Share, Trends & Growth Forecast Report By Ingredient Type (Enzymes [Amylases, Xylanases, Lipases], Emulsifiers [Mono-glycerides, CSL, SSL], Oxidizing Agents, Reducing Agents), Application (Bread, Pizza Crust, Cakes, Buns & Rolls), and Country (India, China, Japan, South Korea, Australia, Rest of APAC) – Industry Analysis From 2025 to 2033.

Asia Pacific Dough Conditioners Market Size

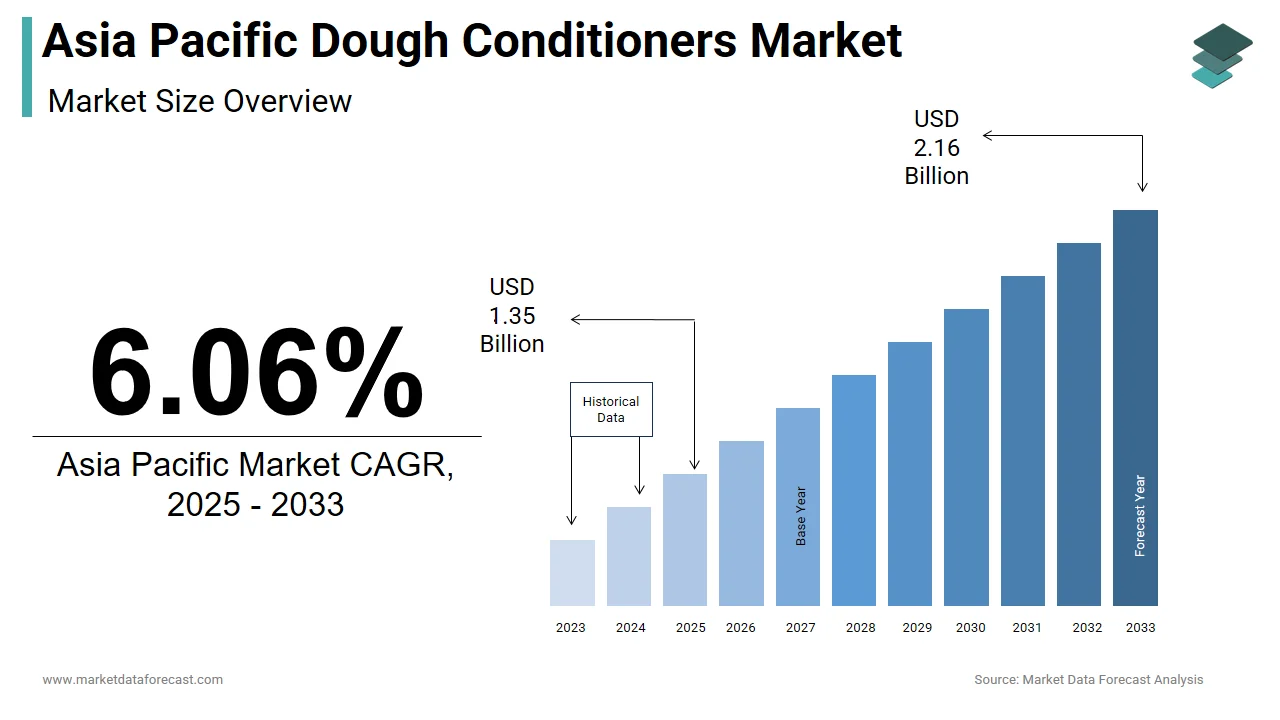

The size of the Asia Pacific dough conditioners market was worth USD 1.27 billion in 2024. The Asia Pacific market is anticipated to grow at a CAGR of 6.06% from 2025 to 2033 and be worth USD 2.16 billion by 2033 from USD 1.35 billion in 2025.

The Asia Pacific dough conditioners market refers to a specialized section within the food additives industry that focuses on enhancing the physical and functional properties of dough used in bakery and confectionery products. Dough conditioners, also known as dough improvers, are blends of enzymes, emulsifiers, oxidizing agents, and other chemical or natural substances that improve dough texture, elasticity, volume, and shelf life. As consumer demand for high-quality baked goods rises across urban and semi-urban areas, the need for processed and ready-to-use dough formulations has increased significantly. This trend is further supported by the expansion of organized retail, modern bakeries, and global fast-food chains in the region.

MARKET DRIVERS

Rising Demand for Convenience Foods in Urban Areas

One of the most influential drivers of the Asia Pacific dough conditioners market is the growing preference for convenience foods, especially among rapidly expanding urban populations. Like, over a significant share of consumers in major cities like Tokyo, Shanghai, and Jakarta now purchase pre-packaged or frozen baked goods at least once a week. This shift is attributed to changing lifestyle patterns, longer working hours, and increasing disposable incomes, which collectively encourage reliance on ready-to-eat and easy-to-bake products. Dough conditioners are essential in mass-producing these convenience items because they enhance dough stability during freezing, thawing, and mechanical processing. Given these trends, the use of dough conditioners has become indispensable in meeting industrial-scale production demands while preserving sensory attributes such as softness, crumb structure, and extended freshness.

Expansion of Bakery Chains and Commercial Baking Facilities

Another critical driver fueling the growth of the Asia Pacific dough conditioners market is the proliferation of international and regional bakery chains, along with the establishment of large-scale commercial baking facilities. Also, the number of commercial bakeries across Southeast Asia increased notably between 2020 and 2023, with Indonesia, Thailand, and Vietnam experiencing some of the highest growth rates. These establishments require standardized and efficient production processes, which depend heavily on dough conditioners to ensure uniformity in product output. For example, Domino’s Pizza, which operates a large number of outlets across Asia Pacific, relies on chemically optimized dough systems to maintain pizza crust consistency across all locations. Moreover, the entry of global brands such as Paul Lafayet and BreadTalk into emerging markets has further intensified the need for reliable dough formulation technologies. Further, in Australia and New Zealand, artisanal bakeries have started adopting enzyme-based conditioners to replicate traditional textures using mechanized production.

MARKET RESTRAINTS

Regulatory Scrutiny Over Chemical Additives

A significant restraint in the Asia Pacific dough conditioners market is the tightening regulatory environment concerning synthetic additives used in dough improvement. Across several countries in the region, including South Korea, Australia, and India, there has been a growing emphasis on clean-label and minimally processed food products. In India, for instance, the Food Safety and Standards Authority of India (FSSAI) imposed a complete ban on potassium bromate in 2022 following studies linking it to cancer in lab animals. This move disrupted supply chains and forced many small and medium-sized bakeries to reformulate their dough systems, often at higher costs. These regulatory pressures have led to delays in product approvals and reduced the availability of conventional dough conditioners, particularly in premium retail segments where consumer awareness of ingredient safety is high.

Fluctuating Prices of Raw Materials

Another pressing challenge restricting the Asia Pacific dough conditioners market is the volatility in raw material prices, particularly for key components such as enzymes, emulsifiers, and oxidizing agents. This fluctuation directly impacts the cost structure of dough conditioner manufacturers, many of whom operate on thin margins in highly competitive markets. Additionally, energy price surges in regions like Australia and New Zealand have further inflated manufacturing expenses, reducing profit margins and discouraging investment in new product development. As a result, companies are compelled to either absorb rising input costs or pass them on to end-users, both of which can dampen market growth.

MARKET OPPORTUNITIES

Growth in Health-Conscious Consumer Segments

A promising opportunity in the Asia Pacific dough conditioners market lies in the rising interest in health-conscious and functional baked goods. Consumers across the region are increasingly prioritizing nutritional value, low-calorie content, and digestive wellness in their food choices. This shift has prompted food manufacturers to explore alternative dough conditioning solutions that align with clean-label and functional nutrition goals. For instance, enzymes such as glucose oxidase and xylanase are gaining traction as natural replacements for chemical oxidants, offering improved dough strength without compromising on health labels. In response, companies like DSM and Kerry Group have introduced enzyme-based dough improvers specifically tailored for the gluten-free and whole-grain bakery markets in Asia. Moreover, in Japan, where digestive health claims are highly valued, probiotic-enriched dough conditioners are being tested in select bakery lines.

Expansion of E-commerce and Direct-to-Consumer Bakery Channels

The rapid growth of e-commerce platforms and direct-to-consumer (DTC) bakery channels presents a significant opportunity for the Asia Pacific dough conditioners market. With digital penetration accelerating across the region, online food delivery and subscription-based bakery services are gaining momentum. This transformation necessitates durable and high-performance dough formulations capable of maintaining quality through extended storage and transportation. Dough conditioners play a crucial role in ensuring that products remain fresh and structurally sound during last-mile delivery, particularly in tropical climates where humidity and heat can degrade dough integrity. Besides, in India, startups have leveraged enzyme-modified dough conditioners to offer home-baking kits that guarantee professional results without prior expertise. As digital infrastructure continues to evolve across the Asia Pacific, the demand for resilient and adaptable dough conditioners is poised to rise accordingly.

MARKET CHALLENGES

Limited Awareness Among Small-Scale Bakeries

Despite the expanding applications of dough conditioners, a significant challenge persists in the form of limited awareness and adoption among small-scale and independent bakeries across the Asia Pacific region. Many of these businesses continue to rely on traditional fermentation techniques and basic improvers due to a lack of technical knowledge and training regarding advanced dough conditioning alternatives. Furthermore, in rural parts of India and the Philippines, artisan bakers often perceive dough conditioners as unnecessary or overly complex additions to their existing recipes. This gap in education and outreach hampers market penetration and slows down the transition toward standardized, high-efficiency baking practices. To address this issue, industry stakeholders are beginning to collaborate with local governments and trade associations to conduct workshops and demonstrations. However, the fragmented nature of the bakery sector and inconsistent policy support across different countries pose persistent barriers to widespread adoption.

Supply Chain Disruptions Due to Climate Change

Climate change-induced weather anomalies are increasingly disrupting the supply chain dynamics for dough conditioners in the Asia Pacific region. Like, extreme weather events such as monsoon floods, typhoons, and droughts have damaged transportation infrastructure and delayed the movement of raw materials and finished products. Moreover, agricultural disruptions in key sourcing regions have led to shortages of primary inputs such as wheat and soy, which are integral to the production of certain dough conditioners. Such supply-side uncertainties not only elevate manufacturing costs but also force formulators to seek less optimal substitutes, potentially compromising product performance. For regional manufacturers, resilience planning has become imperative. Companies are diversifying procurement sources and investing in local production units to mitigate future climate shocks. Nevertheless, the unpredictability of environmental conditions remains a formidable challenge for sustained growth in the Asia Pacific dough conditioners market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Ingredient Type, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Watson Inc, Calpro Foods Pvt. Ltd, Caldic B.V, Puratos Group, Lallemand Inc, Lesaffre, Corbion, E.I. Du Pont De Nemours and Company, Oriental Yeast Co., Ltd, and Archer Daniels Midland Company. |

SEGMENTAL ANALYSIS

By Ingredient Type Insights

The enzymes hold the largest share i.e., 38% of the regional market in 2024. Enzymes are widely favored due to their ability to improve dough texture, enhance fermentation efficiency, and extend shelf life without altering the food label significantly. Their dominance is underpinned by a growing preference for clean-label ingredients across the bakery industry. One key driver of enzyme demand is the increasing production of frozen and par-baked goods that require extended processing stability. This trend has prompted manufacturers to adopt amylases, lipases, and proteases to maintain consistency during freezing and thawing cycles. In addition, in Japan, where artisanal baking methods are being scaled up industrially, enzyme-based systems have become crucial for preserving traditional textures with mechanized output. Another major factor supporting enzyme growth is regulatory encouragement for natural alternatives.

On the other hand, reducing agents are projected to grow at the highest CAGR of 7.9% between 2025 and 2033. This rapid expansion is primarily attributed to rising demand for soft-textured baked goods such as cakes, muffins, and sweet breads, especially among younger consumers in emerging markets like India and Indonesia. A core driver behind this growth is the increasing use of reducing agents such as L-cysteine and sodium metabisulfite in no-time dough (NTD) formulations. These agents weaken gluten structures quickly, enabling faster production cycles and energy savings. In tandem, raw material suppliers such as BASF and Novozymes have expanded their presence in South and Southeast Asia to meet surging demand. Further, in China, government-backed initiatives promoting sustainable baking practices have encouraged the use of reducing agents to minimize mechanical stress during dough mixing, thereby cutting down energy consumption in large-scale bakeries.

By Application Insights

The bread remains the dominant application by capturing a 45.6% of total market volume in 2024. Bread’s stronghold stems from its staple status across many Asian diets, particularly in countries like India, China, and the Philippines, where wheat consumption continues to rise alongside income levels and urbanization. This reflects a broader shift toward ready-to-eat breakfast and snack options in both rural and urban areas. Moreover, institutional demand—especially from schools, hospitals, and catering services—is further boosting commercial brad production, which in turn increases the need for high-performance dough conditioners. Similarly, in the Philippines, where rice dominates traditionally, retail chains report a uptick in sliced bread purchases, signaling a gradual but steady change in consumer behavior. Thus, the consistent expansion of bread consumption across diverse demographics and geographies ensures its continued leadership in the application-driven demand for dough conditioners.

While bread maintains the largest share, pizza crust is emerging as the fastest-growing application segment by registering a CAGR of 8.4%. This dramatic acceleration is fueled by the expanding footprint of international pizza franchises and the localization of Western-style fast food in Asia Pacific markets. Domino’s Pizza alone operates over 2,500 outlets across the region, with a significant portion located in India and Indonesia, where localized flavors such as tandoori chicken and shrimp tikka have boosted customer engagement. In response, bakery ingredient suppliers have developed tailored dough conditioning blends that ensure uniform crust structure, enhanced oven spring, and improved freeze-thaw resilience. Moreover, there has been a surge in home pizza baking kits, particularly in countries like Japan and Australia, where digital-savvy consumers seek premium baking experiences. Coupled with rising disposable incomes and evolving food preferences, this trend is expected to solidify pizza crust as the most rapidly expanding application segment in the region’s dough conditioners market.

COUNTRY LEVEL ANALYSIS

China held a dominant position in the Asia Pacific dough conditioners market by securing an estimated market share of 22% in 2024. As the world’s most populous country and a leading food manufacturing hub, China's robust bakery sector drives extensive demand for dough improvement technologies. The national push toward industrialized baking, supported by the Ministry of Agriculture and Rural Affairs, has led to an annual growth rate in packaged bread sales. One key driver of China’s leadership is the rapid expansion of modern retail formats such as hypermarkets, convenience stores, and online food platforms. To support this volume, domestic flour mills and additive producers have invested heavily in automated blending facilities. For instance, COFCO, one of the largest agribusiness firms in China, introduced a proprietary line of enzyme-based dough improvers in 2022 to cater to high-volume bakery chains. Simultaneously, government-led nutrition fortification programs have spurred demand for enriched flours and fortified dough products. The National Health Commission of China mandates iron and folic acid enrichment in wheat flour sold in public distribution systems, necessitating advanced conditioner blends that preserve nutrient integrity while enhancing functional properties

India’s strong cultural affinity for wheat-based foods, coupled with rising urbanization and changing dietary patterns, has made it a focal point for both domestic and global ingredient suppliers. It’s bakery sector has experienced a transformation over the past decade, transitioning from small-scale, unorganized setups to semi-automated and fully integrated production units. According to the All India Bread Manufacturers’ Association, the number of organized commercial bakeries increased between 2020 and 2023, primarily in metro and tier-2 cities. This shift has amplified the demand for standardized dough conditioners that ensure consistency in texture and leavening, especially in mass-produced items like brown bread, multigrain loaves, and burger buns. Furthermore, the government’s “Make in India” initiative has attracted foreign direct investment in food processing infrastructure, bolstering domestic production of bakery additives. With increasing health awareness, Indian consumers are also gravitating toward fortified and wholegrain bread varieties, encouraging the use of specialized enzymes and fiber-enhancing conditioners.

Japan maintains a prominent role in the Asia Pacific dough conditioners market. Despite its mature economy, Japan continues to exhibit strong demand for high-quality bakery products, underpinned by innovative formulation requirements and a culture of precision in food preparation. One of the primary drivers of Japan’s demand is the widespread adoption of enzyme-modified dough conditioners in artisanal and industrial baking. In particular, the demand for preservative-free bread has surged, with enzyme-assisted dough systems offering extended freshness without compromising on labeling. Additionally, the proliferation of convenience store bakeries, exemplified by chains like FamilyMart and Lawson, has created a need for high-throughput, quality-controlled baking operations. Moreover, Japan’s aging population has intensified demand for softer, easily digestible bread variants, which rely on specialized reducing agents to achieve optimal crumb structure.

Australia and New Zealand collectively account for a notable share of the Asia Pacific dough conditioners market. While not the largest in terms of volume, the region stands out for its high-end product adoption and stringent food safety standards, making it a critical testing ground for new ingredient innovations. Consumer demand for organic, non-GMO, and allergen-free baked goods has led to a shift toward clean-label dough improving solutions. This has prompted companies like Goodman Fielder and Fonterra to reformulate their bakery lines with enzyme-based conditioners that align with these consumer expectations. Moreover, the craft and artisanal baking movement is thriving in both countries, with independent bakeries increasingly adopting performance-enhancing yet minimally processed improvers.

Indonesia emerges as a key growth market in the Asia Pacific dough conditioners space. The country’s expanding middle class, increasing urbanization, and growing popularity of western-style baked goods are among the principal factors propelling the demand for dough conditioners. Bread and bakery consumption in Indonesia has risen steadily. This growth is particularly pronounced in Jakarta, Surabaya, and Bandung, where modern supermarkets and bakery cafes are proliferating. Additionally, the local franchise expansion of global brands such as J.CO Donuts, BreadTalk, and Domino’s Pizza has catalyzed the need for standardized dough formulations that ensure product uniformity across multiple locations. Another critical driver is the increasing availability of imported and locally produced dough conditioners tailored for tropical climates. Moreover, government efforts to boost wheat substitution and flour fortification have paved the way for enhanced dough improvers that support nutritional enrichment goals.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC dough conditioners market profiled in this report are Watson Inc, Calpro Foods Pvt. Ltd, Caldic B.V, Puratos Group, Lallemand Inc, Lesaffre, Corbion, E.I. Du Pont De Nemours and Company, Oriental Yeast Co., Ltd, and Archer Daniels Midland Company.

TOP LEADING PLAYERS IN THE MARKET

One of the leading companies in the Asia Pacific dough conditioners market is DSM (Royal DSM) . A global science-based company active in health, nutrition, and sustainable living, DSM offers a wide range of enzyme-based dough conditioners that improve dough handling, texture, and shelf life. The company’s focus on innovation and sustainability has made it a preferred partner for bakery manufacturers across Asia. Its portfolio includes natural and clean-label solutions tailored to meet evolving consumer demands, particularly in countries like China, India, and Japan.

Another major player is Kerry Group, an Irish multinational specializing in taste and nutrition. Kerry has a strong presence in the Asia Pacific region, offering customized dough conditioning systems that enhance baking efficiency and product consistency. The company invests heavily in localized R&D to cater to regional tastes while ensuring compliance with food safety standards. Kerry works closely with large-scale bakeries and fast-food chains, providing tailor-made improvers that support automation and high-volume production across diverse bakery applications.

Puratos, headquartered in Belgium, is also a key participant in the Asia Pacific dough conditioners space. Known for its expertise in bakery, patisserie, and chocolate products, Puratos provides innovative dough improvement solutions that combine traditional craftsmanship with modern functionality. The company has expanded its footprint through strategic partnerships and local manufacturing units in countries like India, Thailand, and Australia. Its commitment to sustainability and flavor excellence positions it as a trusted supplier for artisanal and industrial bakers alike.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Customization is a primary strategy employed by leading players in the Asia Pacific dough conditioners market. Companies are investing in research and development to create specialized formulations tailored to regional preferences, dietary trends, and production methods. This approach enables them to offer performance-driven solutions that align with clean-label expectations and functional benefits required by modern bakeries.

Strategic Partnerships and Collaborations are being leveraged to strengthen supply chain resilience and expand regional distribution networks. Many ingredient suppliers are forming alliances with local flour mills, bakery equipment manufacturers, and food service providers to integrate their conditioners into end-to-end baking solutions. These collaborations help in accelerating market penetration and enhancing customer engagement across the value chain.

Localized Expansion and Capacity Building is another critical tactic. Major players are establishing regional R&D centers, production facilities, and technical service teams to better serve the growing demand in emerging markets. By adapting to local regulatory environments and consumer behaviors, firms are able to deliver more relevant product offerings and ensure faster response to changing market dynamics.

COMPETITION OVERVIEW

The competition in the Asia Pacific dough conditioners market is marked by a blend of global ingredient giants and regional specialty players vying to maintain relevance amid rapidly shifting consumer preferences and technological advancements. As the bakery industry becomes increasingly industrialized, especially in emerging economies, there is a heightened need for standardized, high-performance dough improvement solutions. This has prompted established players to emphasize innovation, localization, and sustainability to differentiate themselves. At the same time, smaller domestic manufacturers are leveraging cost advantages and deep market knowledge to capture niche segments. The emphasis on clean-label, functional ingredients has intensified the race for enzyme-based and naturally derived conditioners. Additionally, the growing influence of organized retail, e-commerce, and international fast-food chains is compelling ingredient suppliers to align closely with evolving bakery formats and logistics requirements.

RECENT MARKET DEVELOPMENTS

- In March 2024, DSM launched a new line of plant-based enzymes specifically designed for tropical climates, targeting the Southeast Asian bakery sector. This product line was developed to enhance dough stability and fermentation efficiency under humid conditions, allowing local bakeries to produce higher quality bread with extended shelf life.

- In June 2024, Kerry Group announced a partnership with a leading Indian flour mill to co-develop fortified dough conditioners that support government-backed nutrition programs. This collaboration aimed at integrating essential vitamins and minerals into staple bread products without compromising taste or texture.

- In September 2024, Puratos opened a state-of-the-art bakery application center in Bangkok, focusing on customizing dough conditioning solutions for the Thai and wider ASEAN markets. The facility serves as a hub for customer training, product testing, and formulation development tailored to local bakery needs.

- In November 2024, Cargill introduced a new range of emulsifier-based dough improvers in Australia, formulated to replace synthetic additives while maintaining structural integrity in frozen dough applications. This move supported the region’s rising demand for clean-label baked goods.

- In February 2025, Bühler Group , a Swiss technology provider, collaborated with Japanese bakery equipment manufacturers to integrate real-time dough monitoring systems with optimized conditioner dosing. This initiative enhanced process efficiency and consistency for commercial bakeries across Japan.

MARKET SEGMENTATION

This Asia Pacific dough conditioners market research report is segmented and sub-segmented into the following categories.

By Ingredient Type

- Enzymes

- Amylases

- Xylanases

- Lipases

- Proteases

- Others

- Emulsifiers

- Mono-glycerides

- Calcium Stearoyl Lactylate

- Sodium Stearoyl Lactylate

- Others

- Oxidizing agent

- Azodicarbonamide

- Potassium Iodate

- Calcium Peroxide

- Potassium Bromate

- Others

- Reducing agent

- L-cysteine

- Glutathione

- Sodium Bisulphite

- Sodium Metabisulphite

- Others

- Others

By Application

- Bread

- Pizza Crust

- Tortillas

- Cakes/Pastry

- Buns & Rolls

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What drives the Asia Pacific dough conditioners market?

The Asia Pacific dough conditioners market is driven by rising demand for convenience foods, urbanization, growth of commercial bakeries, and the popularity of ready-to-eat baked goods among busy consumers

2. What challenges affect the Asia Pacific dough conditioners market?

The Asia Pacific dough conditioners market faces challenges like tightening regulations on synthetic additives, raw material price volatility, and limited awareness or adoption among small-scale bakeries

3. What opportunities exist in the Asia Pacific dough conditioners market?

The Asia Pacific dough conditioners market offers opportunities in clean-label and enzyme-based conditioners, functional and health-focused bakery products, and expansion through e-commerce and digital bakery channels

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com