Asia Pacific Dyes Market Research Report - Segmentation By Type (Dye and Pigment), End-user Industry and Region - Regional Forecast to 2026 to 2034

Market Size, 2025

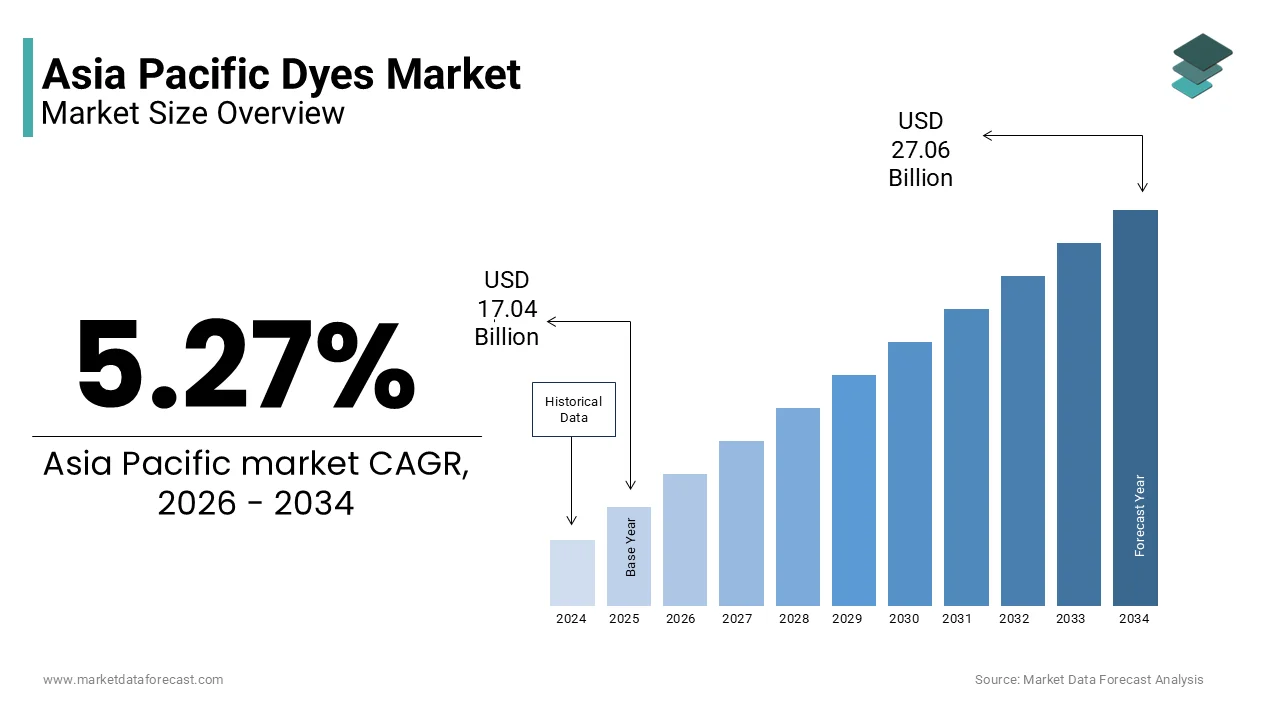

$17.04 BnMarket Estimate, 2026

$17.94 BnMarket Forecast, 2034

$27.06 BnCAGR, 2026–2034

5.27%Asia Pacific Dyes Market Size

The Asia Pacific dyes market size was valued at USD 17.04 billion in 2025 and is projected to reach USD 27.06 billion by 2034 from USD 17.94 billion in 2026, growing at a CAGR of 5.27%.

Growing call for various applications such as textiles, and clothing Se expects paints and coatings, construction, and plastics to drive market expansion. Makers of dyes and pigments are frequently venturing to enhance their goods by utilizing advanced techniques for the efficient removal of environmental and dangerous contaminants through the making procedure.

Dyes are colored substances that are applied as an aqueous solution on various substrates. These are employed as colorants in various industrial applications such as wood stains, food processing, and others. Colorants have high selective absorbency for liquids and also substrates compared to other color-imparting materials such as pigments. The high absorption characteristics of dyes help them lose their physical and structural properties during application to substrates. Low lightfastness and short shelf life are some of the other distinguishing characteristics of dyes. Therefore, they are generally employed in printing, food, and surface coating applications, which require high levels of transparency for the manufacture of finished products.

Product manufacturers are likely to experience variable production costs due to the price volatility of raw materials such as benzene. A wide distribution channel is achieved in the market both through physical retail stores and online retailing. The availability of the product online has increased the consumer base for businesses and also demonstrates greater reach, which is predicted to drive calls for the products.

MARKET DRIVERS

The worldwide market share for colorants is drastically driven by the burgeoning textile industry around the world. Improving living standards, accompanied by escalating end-user call for high-quality colored fabrics, curtains, bedding, and woolen garments will drive expansion in the industry in the coming years. The expansion of the construction industry, worldwide, has been an important factor that has contributed to the call for dyes and pigments. Countries such as the United States, the United Kingdom, China, Indonesia, India, Saudi Arabia, and the United Arab Emirates are the main countries with significant potential for worldwide expansion in the construction sector. A growing population coupled with escalating industrialization has encouraged governments to increase their spending on construction to expand infrastructure development. As a result, rising construction spending around the world is predicted to generate a massive call for dyes and pigments in the coming years. The escalating emphasis on quality and performance, together with strict government regulations on environmental pollution, will encourage the use of natural ingredients in the worldwide market. The growing awareness of the depletion of natural resources, distortion of ecological imbalance, and pollutants resulting in a disturbed environment employed by the excessive use of dangerous chemicals and especially synthetic dyes will allow sellers to launch a more sustainable and safer alternative in the market. The worldwide market for natural dyes is driven by innovations in factories and processing systems. The improvement in the standard of living and the increase in disposable income per capita will boost the call for natural dyes in the world market.

MARKET RESTRAINTS

Rising environmental concerns are driving policy changes around the world, which are predicted to slow market expansion during the foreseen period. Concern has been expressed about the excessive cost of interest. This reduction in investment in research and development activities, which are the main source of product and service innovations. In addition, high energy costs had a negative impact on the production units.

MARKET OPPORTUNITIES

The growing innovation in the textile dye industry is the vital factor accelerating the expansion of the market, along with the growing call for colored textiles and fibers, strong investment in research and development in plant-based dyes, a major The call for textile dyes and the low manufacturing cost in APAC countries are the main factors, among others, of the market for textile dyes. Furthermore, the escalating development of environmentally friendly products will create more new opportunities for the textile dye market during the foreseen period 2020-2025.

MARKET CHALLENGES

Factors such as the high water consumption in the textile industry to clarify the dye, the solubility of the product, the high content of metals in the pigments and the contamination of water during the manufacturing processes are the main environmental threats caused by the market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.27% |

| Segments Covered | By Type, End User Industry, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC |

| Market Leaders Profiled | Dow, BASF SE, Huntsman International LLC, Evonik Industries AG, INEOS Group AG, LANXESS, SABIC, Exxon Mobil Corporation, Kronos Incorporated, Kiri Industries Ltd., Archroma, Allied Industrial Corp., Ltd., Organic Dyes and Pigments, Sumitomo Chemical Co., Ltd., DayGlo Color Corporation, Anand International, SAMCO, and Vasu Chemicals LLP |

REGIONAL ANALYSIS

APAC is the largest and is predicted to be the fastest-growing market for textile dyes. The region encompasses a wide range of economies with different levels of economic development and multiple industries. With the economic downturn and saturation in Europe and North America, textile manufacturers are moving their production base to APAC. China is one of the main producers and consumers of textile dyes in the region. The strengthening of the economies of countries such as China and India attracts new investment in the APAC region. The expansion is mainly attributed to the growing call for textiles and clothing from the large population of the region. The main market players are expanding their production of textile dyes in the APAC region, especially in China and India. Asia-Pacific was the dominant regional market, accounting for more than 62% of the worldwide market share in 2019. The market is subject to strict regulations that hamper the production and use of dyes and pigments in North America and Europe.

Therefore, the production facilities are moved to the Asia-Pacific region due to favorable manufacturing conditions and lenient regulations. This is supported by the availability of raw materials, cheap labor, and skilled labor. The Asia-Pacific market dominated the worldwide market, accounting for a 50% market share of the worldwide market in 2020. It is predicted to be the leading market during the foreseen period, recording the highest CAGR due to strong expansion. of the textile industry in the economies of Southeast Asia. China, India, Bangladesh, Thailand, and South Korea are the main producers of textiles and fabrics in the Asia-Pacific. The Chinese market is the largest market domestically, and major textile producers are relocating their production base to China, due to low energy costs and the availability of skilled labor and raw materials. Also, the Indian textile sector is predicted to experience strong expansion during the foreseen period.

RECENT HAPPENINGS IN THE MARKET

- Marimekko launches its first garments, bags, and household items printed with natural dye. Marimekko Oyj is a Finnish furniture, textiles, and fashion company.

- Seven of the world's largest textile chemical companies have come together to launch a new initiative to promote sustainable chemistry and develop a worldwide harmonized "sustainability standard" for textile chemicals.

KEY MARKET PLAYERS

- Dow

- BASF SE

- Huntsman International LLC.

- Evonik Industries AG

- Ineos Group AG

- LANXESS

- SABIC

- Exxon Mobil Corporation.

- Kronos Incorporated.

- Kiri Industries Ltd

- Archroma

- ALLIED INDUSTRIAL CORP., LTD

- Organic Dyes and Pigments

- Sumitomo Chemical Co., Ltd.

- Dayglo Color Corporation

- Anand International

- SAMCO

- VASU CHEMICALS LLP

MARKET SEGMENTATION

This research report on the Asia Pacific dyes market has been segmented and sub-segmented based on categories.

By Type

- Dye

- Pigment

By End-User Industry

- Paints & Coatings

- Textile

- Printing Ink

- Plastic

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

1. What is the Asia Pacific dyes market?

The Asia Pacific dyes market comprises the production, distribution, and consumption of dyes used to impart color to textiles, plastics, paper, leather, inks, and other industrial products.

2. What factors are driving the growth of the Asia Pacific dyes market?

The market is driven by the expansion of the textile industry, growing demand for colored consumer goods, increasing industrialization, and rising manufacturing activities across the region.

3. Which countries are major contributors to the Asia Pacific dyes market?

Major contributors include China, India, Japan, South Korea, and Bangladesh due to their strong textile and manufacturing sectors.

4. What are the major types of dyes used in the market?

Common dye types include reactive dyes, disperse dyes, direct dyes, vat dyes, acid dyes, and sulfur dyes, each designed for specific applications and materials.

5. Which application segment accounts for a significant share of the market?

The textile industry holds a significant market share because dyes are extensively used in fabric coloring, garment manufacturing, and textile processing.

6. How does the apparel industry influence demand for dyes?

Growing demand for fashionable clothing, sportswear, and home textiles increases the need for high-quality dyes that provide vibrant and durable colors.

7. What role does the packaging industry play in the dyes market?

Dyes are widely used in printing inks, labels, and packaging materials to enhance product appearance and brand visibility.

8. How are environmental regulations affecting the dyes industry?

Manufacturers are increasingly developing eco-friendly and low-toxicity dyes to comply with environmental standards and reduce pollution associated with dyeing processes.

9. What challenges does the Asia Pacific dyes market face?

Challenges include fluctuating raw material prices, strict environmental regulations, wastewater treatment requirements, and intense market competition.

10. What is the future outlook for the Asia Pacific dyes market?

The market is expected to grow steadily due to rising textile production, increasing industrial applications, growing consumer demand for colored products, and advancements in sustainable dye technologies.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com