Asia Pacific Electronic Toll Collection Market Research Report – Segmented By Technology ( RFID , DSRC ) Offering, Application, Type and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis on Size, Share, Trends& Growth Forecast from 2025 to 2033

Asia Pacific Electronic Toll Collection Market Size

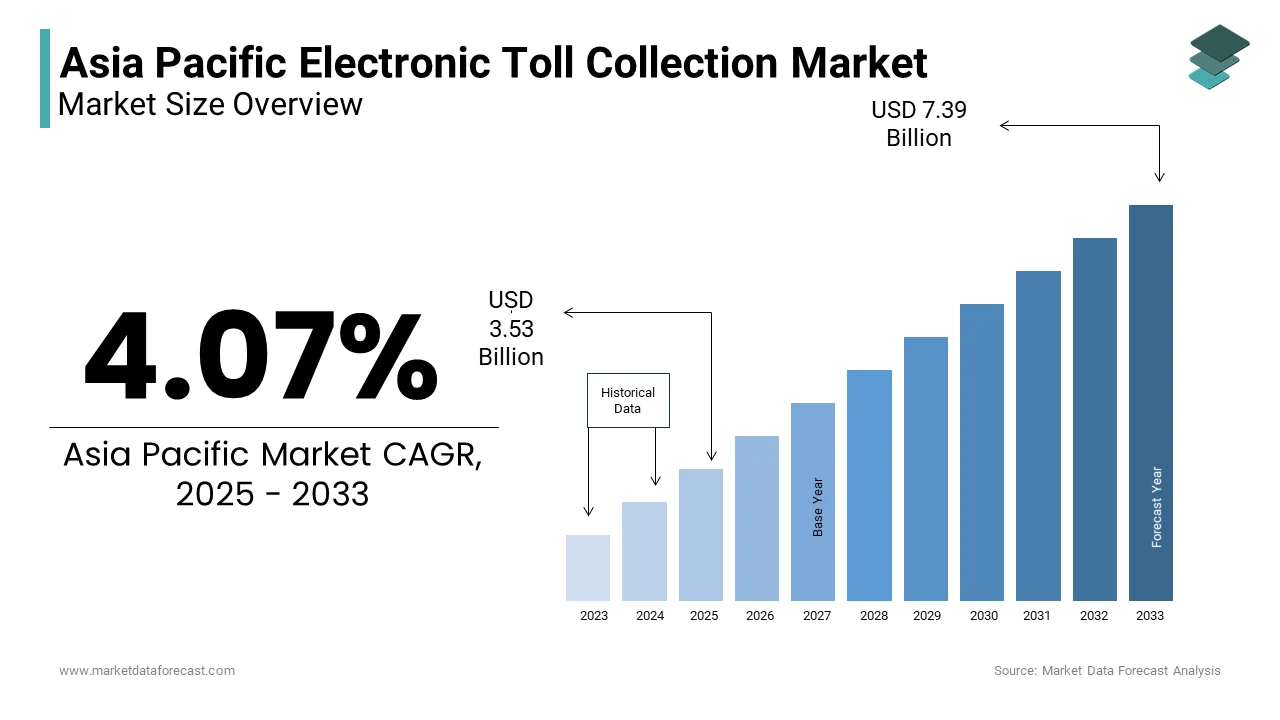

The Asia Pacific Electronic Toll Collection Market Size was valued at USD 3.22 billion in 2024. The Asia Pacific Electronic Toll Collection Market Size is expected to have 9.67% CAGR from 2025 to 2033 and be worth USD 7.39 billion by 2033 from USD 3.53 billion in 2025.

MARKET DRIVERS

Government Initiatives and Policy Mandates

A significant driver of the Asia Pacific electronic toll collection market is the proactive role of governments in mandating the adoption of ETC systems. For example, as per the Ministry of Transport in China, the government invested $5 billion in 2023 alone to integrate RFID and GPS-based tolling systems across its expressways. These policies aim to reduce congestion, minimize environmental impact, and improve revenue collection efficiency. Another key factor is the emphasis on interoperability between regions. Like, cross-border tolling agreements, such as those under the ASEAN Connectivity Master Plan, have facilitated seamless travel for commercial vehicles. This has led to a increase in inter-regional trade.

Technological Advancements and Digital Transformation

Another major driver is the rapid advancement of digital technologies that enhance the functionality and accessibility of ETC systems. For instance, as per PwC, over 80% of toll operators in Japan and South Korea have adopted AI-driven platforms to optimize traffic flow and reduce operational costs. Furthermore, the proliferation of mobile payment gateways has expanded the reach of ETC systems. These innovations not only cater to tech-savvy users but also address the growing demand for cashless ecosystems. Additionally, as per the International Road Federation, the deployment of solar-powered toll booths has reduced energy consumption, aligning with sustainability goals. These technological strides are propelling the adoption of ETC systems across the region.

MARKET RESTRAINTS

High Initial Investment Costs

A significant restraint in the Asia Pacific electronic toll collection market is the high initial investment required for deploying advanced infrastructure. Additionally, maintenance costs pose a further challenge. Without adequate funding or international aid, these financial barriers hinder widespread adoption, particularly in rural areas where infrastructure development is already lagging. This disparity limits the market’s inclusivity, creating uneven progress across the region.

Cybersecurity Vulnerabilities and Data Privacy Concerns

Another major restraint is the rising concern over cybersecurity vulnerabilities and data privacy issues associated with ETC systems. For example, a breach in a major toll system in Thailand exposed the personal data of over 2 million users, eroding public trust in digital tolling solutions. Governments and private stakeholders must invest in robust encryption protocols and compliance frameworks to mitigate these threats. However, as per Deloitte, the additional costs of implementing cybersecurity measures can deter adoption, particularly among small-scale operators. These concerns pose a significant barrier to the seamless expansion of ETC systems in the region.

MARKET OPPORTUNITIES

Integration with Smart City Initiatives

A significant opportunity in the Asia Pacific electronic toll collection market lies in its integration with broader smart city initiatives. According to the United Nations Economic and Social Commission for Asia and the Pacific, over 60% of the region’s population will reside in urban areas by 2030, driving the need for intelligent transportation solutions. These integrations not only enhance urban connectivity but also reduce carbon emissions by optimizing traffic flow. Furthermore, as per the Asian Development Bank, investments in IoT-enabled infrastructure have enabled ETC systems to communicate with other smart utilities, such as parking systems and public transit networks. This interconnected ecosystem fosters greater convenience for commuters while generating valuable data for urban planners.

Expansion into Tier-II and Rural Areas

Another promising opportunity is the expansion of ETC systems into tier-II cities and rural areas, where infrastructure development is gaining momentum. According to the World Bank, over 50% of road networks in countries like India and Indonesia are located in semi-urban and rural regions, presenting untapped potential for ETC adoption. For example, as per Deloitte, the Indian government’s Bharatmala Project aims to install ETC systems across 26,000 kilometers of freight and passenger movement across the country, improving accessibility and revenue generation. Additionally, the introduction of low-cost ETC solutions, such as battery-powered tags and satellite-based tolling, has made it feasible to deploy systems in remote areas with limited power and communication infrastructure. These innovations not only bridge the urban-rural divide but also support regional economic growth by facilitating smoother movement of goods and people.

MARKET CHALLENGES

Interoperability Issues Across Borders

A pressing challenge for the Asia Pacific electronic toll collection market is the lack of interoperability between tolling systems across borders. According to the Asian Development Bank, over 60% of cross-border toll transactions in the ASEAN region face delays due to incompatible technologies and fragmented regulatory frameworks. For instance, as per Deloitte, trucks traveling between Thailand and Malaysia often encounter multiple toll systems requiring separate payments, disrupting supply chains and increasing operational costs. Furthermore, as per the World Economic Forum, the absence of unified standards for ETC protocols complicates efforts to create seamless travel corridors. While initiatives like the ASEAN Single Window aim to address these gaps, progress remains slow due to varying levels of technological readiness among member states.

Resistance to Behavioral Change Among Users

Another critical challenge is the resistance to behavioral change among users unfamiliar with digital tolling systems. According to the International Transport Forum, numerous drivers in rural areas of countries like Indonesia and Vietnam prefer manual toll payments due to mistrust or lack of awareness about ETC benefits. Additionally, the transition from cash-based systems to digital platforms requires extensive public education campaigns, which many governments struggle to implement effectively. Without clear communication and incentives, such as discounts for early adopters, user engagement remains low, limiting the scalability of ETC systems.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.67% |

| Segments Covered | By Technology ,Offering, Application, Type and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | Thales Group S.A., Raytheon Technologies Corporation, Kapsch TrafficCom AG. |

SEGMENTAL ANALYSIS

By Technology Insights

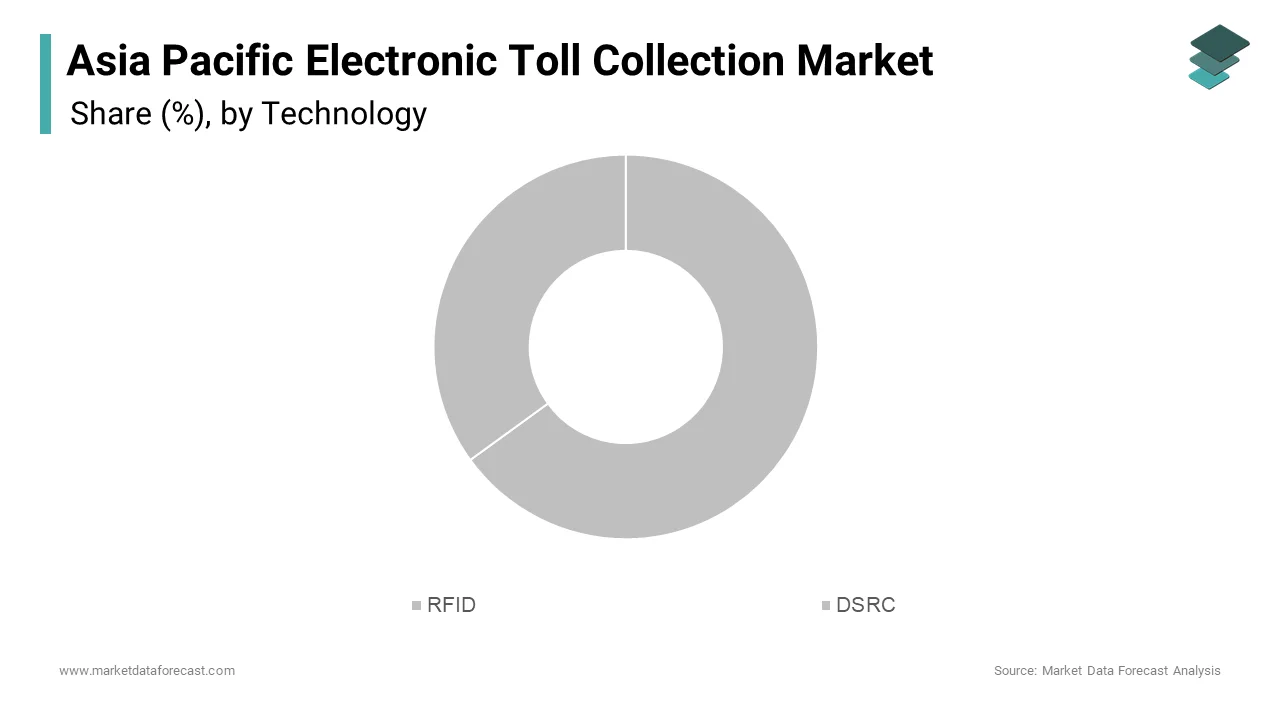

The RFID technology segment led the Asia Pacific electronic toll collection market by commanding a 65% share in 2024. This lead position is due to its cost-effectiveness and widespread adoption across highways and urban corridors. Similarly, RFID systems are favored for their ability to process transactions quickly and accurately, reducing congestion at toll plazas. For instance, in countries like India and China, a significant percentage of toll booths have transitioned to RFID-based systems, enabling seamless cashless payments. A key driver is the integration of RFID with mobile payment platforms. Additionally, as per the Asian Development Bank, governments are investing heavily in RFID infrastructure, with projects like India’s FASTag initiative achieving near-universal adoption.

The DSRC (Dedicated Short-Range Communication) is moving ahead quickly in the Asia Pacific electronic toll collection market, with a CAGR of 14.8%. This acceleration is credited to the increasing demand for high-speed, low-latency communication systems. For instance, as per the World Economic Forum, DSRC is being adopted for smart highway projects in Japan and South Korea, where real-time data exchange is critical for traffic management. A significant factor is the rise of autonomous vehicles, which rely on DSRC for seamless tolling. According to the International Transport Forum, over 50% of new vehicles in urban areas are equipped with DSRC-enabled systems, facilitating interoperable toll payments.

By Offering Insights

The hardware segment has the biggest share of the Asia Pacific electronic toll collection market in 2024. This prominence is driven by the extensive deployment of RFID tags, gantry systems, and onboard units (OBUs). Also, hardware accounts for the majority of upfront investments in ETC systems, particularly in large-scale projects like China’s national highway network upgrades. For instance, as per the Asian Development Bank, hardware installation costs exceed $5 billion annually in the region, underscoring its critical role in system functionality. A key driver is the growing emphasis on durability and reliability. Also, advancements in materials and engineering have extended the lifespan of hardware components, reducing long-term maintenance costs.

The Back office solutions segment is seeing an impressive rise in the Asia Pacific electronic toll collection market, with a CAGR of 16.2%. This is propelled by the increasing complexity of tolling operations and the need for centralized data management. For example, back office systems are being deployed to analyze transaction data, optimize pricing models, and ensure compliance with regulatory standards. A significant factor is the integration of AI and cloud computing into back office platforms. Additionally, as per the World Bank, the shift toward cloud-based solutions has reduced infrastructure costs, accelerating adoption rates.

By Application Insights

The highways segment prevailed in the Asia Pacific electronic toll collection market by accounting for 60.7% of the total application segment in 2024. This leading position is attributed to the region’s extensive highway networks and the critical need for efficient tolling systems to manage heavy traffic volumes. For instance, as per the Ministry of Transport in China, the implementation of ETC systems on highways has reduced congestion since 2020. A key driver is the focus on revenue generation and environmental sustainability. As per the World Economic Forum, toll revenues from highways exceed $20 billion annually in the region, funding further infrastructure development.

The urban areas segment represent the swiftest expanding application segment in the Asia Pacific electronic toll collection market, with a CAGR of 18.5%. This growth is caused by the increasing adoption of congestion pricing and smart city initiatives. For example, as per the United Nations Economic and Social Commission for Asia and the Pacific, cities like Singapore and Seoul have implemented dynamic pricing models to regulate traffic flow and reduce pollution. A significant factor is the integration of ETC systems with urban mobility frameworks. According to Deloitte, over 70% of tolling systems in urban areas are now linked to public transit networks, fostering seamless multimodal travel.

By Type Insights

The transponders/tag-based tolling systems segment commanded the Asia Pacific market by holding a 55% share in 2024. This influence is credited to their widespread adoption across highways and urban corridors. Like, transponders are favored for their accuracy and ease of use, processing a vast portion of toll transactions in countries like India and Japan. For instance, as per the Asian Development Bank, India’s FASTag system achieved near-universal adoption, with over 100 million tags issued by 2023. A key driver is the affordability and scalability of tag-based systems. As per PwC, the average cost of deploying transponders is 30% lower than alternative technologies, making them accessible for emerging economies.

The GPS-based tolling systems segment is the fastest-growing type in the Asia Pacific electronic toll collection market, with a CAGR of 20.3% from 2025 to 2033. This is driven by the increasing demand for location-based services and flexible pricing models. For example, GPS systems are being adopted for congestion pricing in cities like Bangkok and Jakarta, where traditional tolling methods are impractical. A significant factor is the rise of smart highways and autonomous vehicles. According to the International Transport Forum, over 60% of GPS-based systems are integrated with vehicle navigation platforms, facilitating seamless toll payments.

COUNTRY LEVEL ANALYSIS

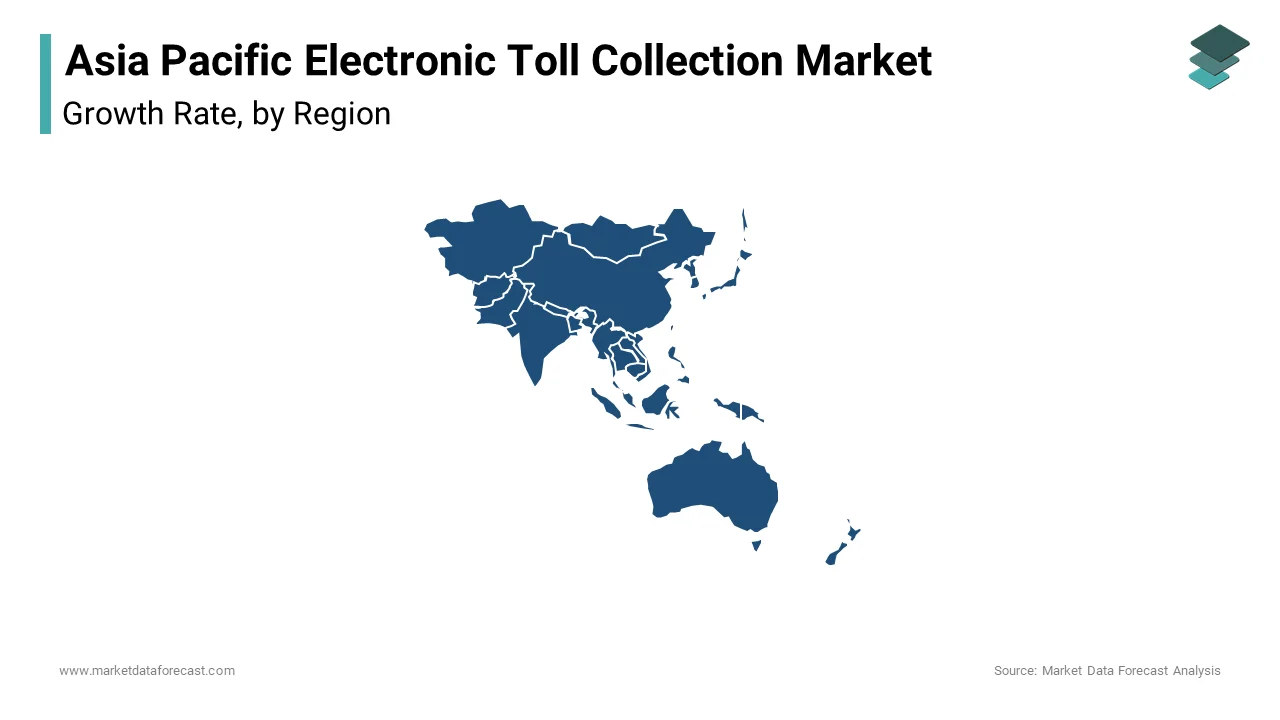

China remains at the lead position in the Asia Pacific electronic toll collection market by contributing 35.3% to the regional share in 2024. This control is supported by the country’s vast highway network and aggressive investments in smart transportation. Like, China spent over $15 billion on ETC infrastructure in 2023, enabling seamless tolling across a vast network of expressways. The government’s push for cashless tolling has resulted in universal adoption, with a large number of vehicles equipped with ETC tags.

India is an emerging player in this market. This is attributable to the success of the FASTag initiative, which has transformed toll collection across the country. According to the Asian Development Bank, over 90% of toll transactions in India are now handled through FASTag, generating $5 billion in annual revenue. The government’s focus on digitalization and interoperability has further strengthened the market.

Japan holds a major position in the market. Its growt is underpinned by advanced DSRC systems and widespread adoption of ETC2.0 technology. Like, Japan’s ETC penetration rate is high, supported by subsidies and user-friendly policies.

South Korea continues to advance ahead in this market and is fueled by smart city initiatives and investments in DSRC technology. A large number of toll transactions in urban areas like Seoul are processed through DSRC-enabled systems, enhancing operational efficiency.

Singapore is a key player in the market. It is driven by congestion pricing and smart mobility frameworks. Also, Singapore’s ETC systems have reduced traffic congestion, setting a benchmark for urban tolling solutions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Asia Pacific Electronic Toll Collection Market are Thales Group S.A., Raytheon Technologies Corporation, Kapsch TrafficCom AG (Datax Handels Gmbh), Conduent, Incorporated, Cubic Corporation, Siemens AG, TransCore (ST Engineering), Efkon GmbH (STRABAG SE), FEIG ELECTRONIC GmbH.

The Asia Pacific electronic toll collection market is characterized by intense competition, driven by the presence of global giants like Thales Group, Kapsch TrafficCom, and Siemens Mobility, alongside regional players striving to carve out their niche. The competitive landscape is shaped by innovation, customization, and strategic collaborations, with companies vying to offer scalable and interoperable solutions. A key differentiator is the focus on sustainability, with firms adopting green technologies to align with environmental goals. Additionally, partnerships with local stakeholders and investments in digital tools are critical for addressing the unique demands of the region. Regulatory mandates promoting cashless transactions and interoperability further intensify competition, requiring participants to adopt agile strategies. Despite challenges like high initial costs and cybersecurity concerns, the market fosters innovation and drives continuous improvement, benefiting both operators and end-users.

Top Players in the Market

Thales Group

Thales Group is a leading player in the Asia Pacific electronic toll collection market, renowned for its expertise in advanced RFID and DSRC technologies. The company’s contribution to the global market lies in its ability to deliver scalable and interoperable solutions tailored to regional needs. Its focus on cybersecurity ensures secure data exchange, addressing growing concerns about privacy. Through innovation and collaboration, Thales continues to drive the adoption of smart tolling solutions across the region.

Kapsch TrafficCom

Kapsch TrafficCom stands out for its comprehensive portfolio of end-to-end ETC solutions, ranging from hardware to back-office systems. The company’s global influence is evident in its ability to integrate cutting-edge technologies like AI and cloud computing into tolling frameworks. In the Asia Pacific market, Kapsch has strengthened its presence by offering customized solutions for highways and urban areas, aligning with smart city initiatives. Its emphasis on sustainability and operational efficiency has earned it a reputation as a trusted partner for modern transportation networks.

Siemens Mobility

Siemens Mobility is a key player in the Asia Pacific electronic toll collection market, known for its innovative approach to intelligent transportation systems. The company’s global impact stems from its ability to leverage IoT and big data analytics to optimize tolling operations. In the region, Siemens has differentiated itself by focusing on interoperability and seamless integration with existing infrastructure. Its commitment to sustainability and digital transformation aligns with the growing demand for smart mobility solutions.

Top Strategies Used by Key Market Participants

Focus on Technological Innovation

A major strategy adopted by key players is the continuous investment in technological innovation to enhance system capabilities. Companies are leveraging advancements in IoT, AI, and cloud computing to improve transaction speeds, data accuracy, and user experience. For instance, integrating predictive analytics into back-office systems allows operators to optimize pricing models and reduce congestion.

Strategic Partnerships and Collaborations

Another significant strategy is forming strategic partnerships with governments, financial institutions, and technology providers. These collaborations enable companies to access funding, share expertise, and develop localized solutions that align with regulatory requirements. For example, partnering with banks facilitates prepaid tolling models, enhancing user convenience. Additionally, alliances with global tech firms ensure access to cutting-edge innovations, strengthening competitive positioning.

Emphasis on Sustainability and User-Centric Solutions

The third key strategy involves prioritizing sustainability and user-centric design to meet evolving customer expectations. Companies are developing eco-friendly systems that minimize energy consumption and carbon emissions, aligning with global environmental goals. Simultaneously, they are focusing on enhancing user convenience through features like mobile payment integration and real-time notifications.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, SS8 Networks, a provider of lawful interception solutions, partnered with European cybersecurity firm CyberShield to enhance its data monitoring capabilities. This collaboration is anticipated to strengthen SS8’s position in the European market by offering more robust compliance tools.

- In June 2023, Utimaco, a leading provider of encryption solutions, acquired a German-based lawful interception software developer. This acquisition enabled Utimaco to expand its portfolio and address growing demand for secure interception technologies.

- In September 2022, Verint Systems launched a new AI-driven analytics platform for lawful interception in Europe. This move was aimed at improving real-time data processing and enhancing investigative accuracy for law enforcement agencies.

- In January 2023, Cisco Systems integrated advanced lawful interception features into its networking solutions, targeting European telecom operators. This initiative reinforced Cisco’s leadership in providing secure communication infrastructure.

- In November 2022, Aqsacom, a provider of regulatory compliance solutions, signed a strategic agreement with a European government agency to deploy a nationwide lawful interception system. This project is expected to bolster Aqsacom’s presence in the region and set new standards for data security.

MARKET SEGMENTATION

This research report on the asia pacific electronic toll collection market has been segmented and sub-segmented into the following.

By Technology

- RFID

- DSRC

By Offering

- Hardware

- Back Office

By Application

- Highways

- Urban Areas

By Type

- Transponders/Tag-Based Tolling Systems

- GPS-Based Tolling Systems

By Country

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Indonesia

- Philippines

- Vietnam

- Singapore

- Rest of APAC

Frequently Asked Questions

Which countries in the Asia Pacific are leading in ETC adoption?

Countries like Japan, South Korea, China, Singapore, and India are among the leaders, with robust ETC infrastructure and growing adoption of smart mobility systems.

How big is the Asia Pacific ETC market?

As of recent estimates, the market is valued in billions of USD, with double-digit CAGR growth expected through 2030, driven by urbanization and infrastructure investment.

Who are the key players in the Asia Pacific ETC market?

Major players include are Kapsch TrafficCom TransCore Toshiba Corporation Mitsubishi Heavy Industries Siemens AG 3M Thales Group.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com