Asia Pacific Empty Capsules Market Size, Share, Trends & Growth Forecast Report By Product, Therapeutic Application, End User & Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of Asia-Pacific), Industry Analysis From 2026 to 2034

Asia Pacific Empty Capsules Market Report Summary

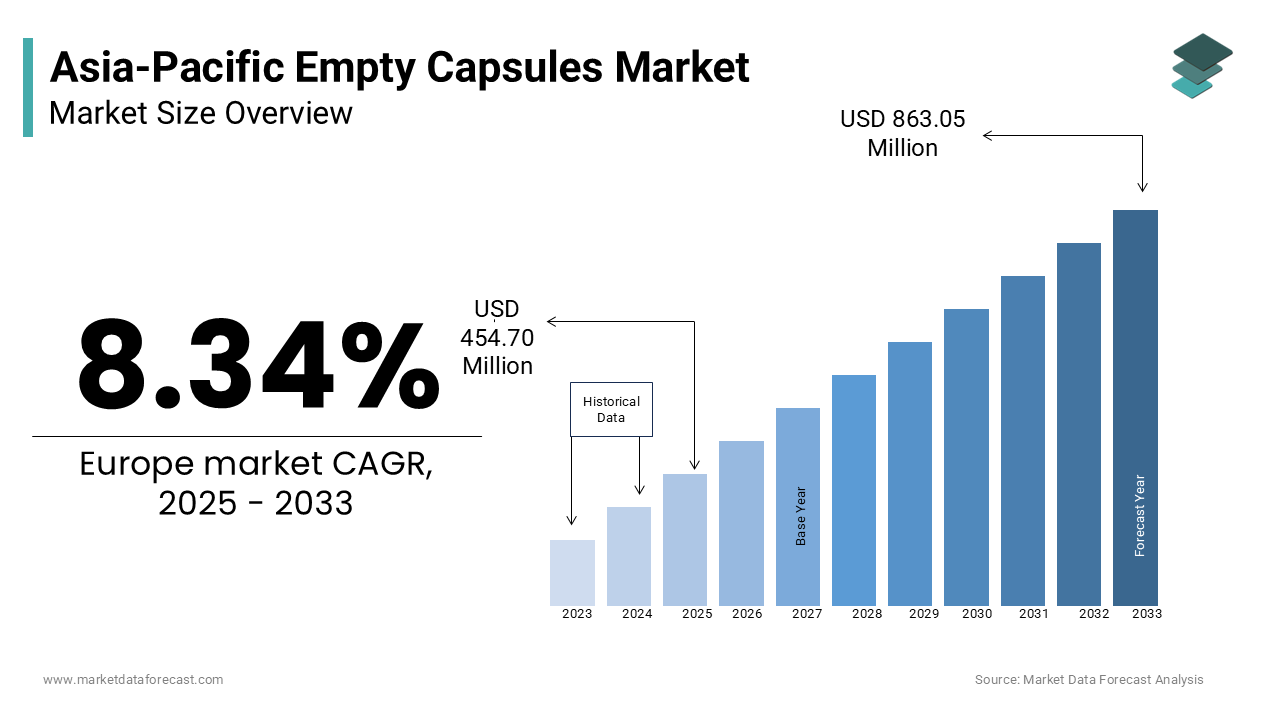

The Asia Pacific empty capsules market was valued at USD 454.70 million in 2025, is estimated to reach USD 492.62 million in 2026, and is projected to reach USD 935.02 million by 2034, growing at a CAGR of 8.34% during the forecast period from 2026 to 2034. The growth of the Asia Pacific empty capsules market is driven by the expansion of the generic pharmaceutical industry, rising demand for nutraceuticals and dietary supplements, and increasing preference for patient-friendly oral dosage forms. Additionally, growing health awareness, regulatory emphasis on quality standards, and the shift toward vegetarian and plant-based capsules are further accelerating market growth across the region.

Key Market Trends

- Increasing demand for nutraceuticals and dietary supplements driven by preventive healthcare trends.

- Rising adoption of vegetarian (HPMC and pullulan) capsules due to ethical and cultural preferences.

- Growing focus on personalized nutrition and customized supplement formulations.

- Advancements in modified-release and targeted drug delivery capsule technologies.

- Expansion of generic pharmaceutical manufacturing hubs in Asia Pacific.

Segmental Insights

- Based on product, the gelatin capsules segment dominated the market in 2025 due to cost-effectiveness, widespread availability, and strong pharmaceutical adoption.

- The non-gelatin capsules segment is expected to grow at a faster rate, driven by increasing demand for vegan, halal, and clean-label products.

- Based on therapeutic application, the vitamins and dietary supplements segment held the largest share, supported by the booming wellness industry and rising consumer health awareness.

- The cardiovascular therapy segment is projected to grow steadily due to increasing prevalence of heart diseases and lifestyle disorders.

- Based on end user, the pharmaceutical industry segment dominated the market due to large-scale generic drug production in countries like India and China.

- The nutraceutical segment is expected to witness strong growth driven by rising consumer focus on preventive healthcare and wellness products.

Regional Insights

- China was the largest contributor, driven by strong pharmaceutical manufacturing capacity, growing health awareness, and expanding nutraceutical sector.

- India is a key growth market due to its dominance in generic drug production and increasing demand for herbal and Ayurvedic supplements.

- Japan holds a significant share, supported by high-quality standards, aging population, and demand for advanced drug delivery systems.

- South Korea and Australia are witnessing steady growth due to regulatory advancements and rising health-conscious consumers.

Competitive Landscape

The Asia Pacific empty capsules market is highly competitive, with both global leaders and regional manufacturers focusing on innovation, cost efficiency, and product diversification. Companies are investing in vegetarian capsules, advanced drug delivery technologies, and sustainable sourcing practices to gain a competitive edge. Strategic partnerships with pharmaceutical and nutraceutical companies, along with capacity expansion and regulatory compliance, are key growth strategies. Key players in the market include Capsugel, ACG Worldwide, Suheung Co Ltd., Bright Pharmacaps Inc., Capscanada Corporation, Medi-Caps Ltd., Qualicaps, Roxlor LLC, Snail Pharma Industry Co. Ltd., and Sunil Healthcare Limited.

Asia Pacific Empty Capsules Market Size

The size of the empty capsules market in the Asia Pacific was valued at USD 454.70 million in 2025. The regional market is predicted to experience a CAGR of 8.34 % from 2026 to 2034 and be worth USD 935.02 million by 2034 from USD 492.62 million in 2026.

Empty capsules are hollow shells primarily used as dosage forms for pharmaceuticals, nutraceuticals, and dietary supplements. These capsules are predominantly made from gelatin, hydroxypropyl methylcellulose (HPMC), or pullulan, and serve as critical delivery systems that mask unpleasant tastes and odors while ensuring precise drug release. The region is experiencing a robust transformation in oral solid dosage formulations, driven by the expanding generic pharmaceutical industry and the surging demand for herbal and natural supplements. According to the United States Pharmacopeia, India and China now account for a combined 61% share of total active pharmaceutical ingredient filings, which is indicating their status as key manufacturing hubs. Furthermore, as per the International Diabetes Federation, over 75% of adults with diabetes live in low and middle income countries, which include many developing nations in the Asia Pacific where lifestyle related diseases are rising sharply. The shift towards patient centric drug delivery systems has amplified the preference for capsules due to their ease of swallowing and rapid disintegration properties. Regulatory bodies in countries like Japan, Australia, and South Korea are enforcing stringent quality standards for excipients, prompting manufacturers to adopt advanced production technologies. This regulatory landscape, coupled with the growing health consciousness among consumers, creates a fertile ground for market expansion. The integration of sustainable sourcing practices and the development of vegetarian alternatives further align with regional preferences, thereby driving the adoption of diverse empty capsule types across the Asia Pacific healthcare ecosystem.

MARKET DRIVERS

Surging Demand for Nutraceuticals and Dietary Supplements

The escalating demand for nutraceuticals and dietary supplements is primarily propelling the growth of the empty capsules market in Asia-Pacific. Rising health awareness, coupled with an aging population, has led consumers to prioritize preventive healthcare through the regular intake of vitamins, minerals, and herbal extracts. According to the Global Wellness Institute, India and Australia are among the top markets experiencing strong growth in the wellness economy, with India seeing an annual growth rate of 11.5% from 2019 to 2024. In China, according to the Global Wellness Institute, the national wellness market reached $950 billion in 2024, reflecting a strong consumer inclination towards wellness products. Capsules are the preferred delivery format for these supplements due to their ability to protect sensitive ingredients from oxidation and moisture, while facilitating easy ingestion. In India, the Ministry of Ayush has promoted the global acceptance of traditional medicine, leading to a surge in the export of herbal formulations which are predominantly encapsulated. According to the Indian Drug Manufacturers Association, the production of herbal capsules has increased by 15% annually to meet both domestic and international demand. The convenience of capsules compared to tablets, particularly for elderly patients who struggle with swallowing, further drives their adoption. Additionally, the trend towards personalized nutrition has spurred the development of customized supplement blends often packaged in capsule form. This sustained consumer interest in health and wellness ensures a steady and growing demand for high quality empty capsules across the region.

Expansion of the Generic Pharmaceutical Industry

The rapid expansion of the generic pharmaceutical industry in the Asia Pacific significantly propels the demand for empty capsules as a cost effective and efficient drug delivery system, which is further aiding the regional market expansion. Countries such as India and China are major global suppliers of generic medicines, catering to both domestic needs and export markets in developed nations. According to the United States Pharmacopeia, India accounts for 48% of total active pharmaceutical ingredient filings globally, relying heavily on oral solid dosage forms. The National Medical Products Administration in China has streamlined approval processes for generic drugs, encouraging local manufacturers to increase production capacities. According to the World Health Organization, over 50 Chinese manufacturing sites are now pre-qualified, supporting an industry where generic drugs fuel the bulk of the volume. Empty capsules are favored in generic drug formulation due to their versatility in accommodating various powder and pellet fills, and their relatively low manufacturing costs compared to other dosage forms. The patent cliffs of several blockbuster drugs have further accelerated the entry of generic versions, many of which utilize capsule technology for bioequivalence. In Southeast Asian nations like Vietnam and Indonesia, the growing middle class is increasing access to affordable medicines, boosting the local pharmaceutical sector. The Association of Southeast Asian Nations has harmonized regulatory standards for pharmaceuticals, facilitating cross border trade and stimulating production. This robust growth in generic drug manufacturing creates a substantial and consistent demand for empty capsules, reinforcing their critical role in the regional pharmaceutical supply chain.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices, particularly for gelatin and hydroxypropyl methylcellulose is a significant restraint on the growth of the empty capsules market in the Asia Pacific. Gelatin derived from animal collagen is subject to fluctuations in livestock prices and availability, while HPMC depends on the pulp and chemical industries which are influenced by global economic conditions. According to the Food and Agriculture Organization of the United Nations, African Swine Fever has been reported in over 20 countries in the Asia Pacific since 2018, leading to potential disruptions in the supply of porcine materials. In China, which is a major producer of gelatin, any disturbance in the agricultural sector directly impacts the cost structure of capsule manufacturers. According to the China Gelatin Manufacturers Association, price volatility has forced many small and medium sized enterprises to operate with thin margins, affecting their competitiveness. Similarly, the price of HPMC is linked to the cotton linter and wood pulp markets, which have experienced instability due to trade tensions and logistical bottlenecks. In India, the reliance on imported raw materials for certain specialty capsules exposes manufacturers to currency exchange risks and import duties. The Asian Development Bank notes that supply chain inefficiencies in the region can lead to prolonged lead times and increased inventory costs. These financial pressures compel manufacturers to pass on costs to customers, potentially reducing demand from price sensitive segments. The inability to predict raw material costs accurately hinders long term planning and investment in capacity expansion, thereby restraining market growth.

Stringent Regulatory Compliance and Quality Standards

The imposition of stringent regulatory compliance and quality standards poses a substantial challenge for empty capsule manufacturers in the Asia Pacific region. Regulatory authorities are increasingly demanding higher levels of purity, consistency, and traceability for pharmaceutical excipients to ensure patient safety. As per the World Health Organization, pharmaceutical quality systems require rigorous testing for contaminants, which inherently increases production costs. In Japan, the Pharmaceuticals and Medical Devices Agency enforces strict standards for capsule quality, requiring extensive documentation and validation processes. According to the Japanese Ministry of Health, Labour and Welfare, non compliance can result in product recalls and significant financial penalties, deterring smaller players from entering the market. In Australia, the Therapeutic Goods Administration mandates that all medicinal products, including empty capsules, meet high quality benchmarks which often exceed international norms. The complexity of navigating diverse regulatory frameworks across different countries in the Asia Pacific creates administrative burdens for multinational manufacturers. In China, the National Medical Products Administration has intensified inspections of pharmaceutical excipient manufacturers, leading to the closure of facilities that fail to meet updated standards. According to reports from the National Medical Products Administration, the enforcement of consistency evaluations for generic drugs has pressured manufacturers to invest heavily in quality. These regulatory hurdles raise barriers to entry and limit the speed at which new products can be launched. Consequently, manufacturers must invest heavily in quality assurance infrastructure, which can strain resources and slow down market expansion, particularly for smaller regional producers.

MARKET OPPORTUNITIES

Growing Preference for Vegetarian and Vegan Capsule Alternatives

The increasing consumer preference for vegetarian and vegan capsule alternatives presents a lucrative opportunity for market expansion in the Asia Pacific region. Religious, cultural, and ethical considerations drive a significant portion of the population in countries like India and Indonesia to avoid animal derived products such as gelatin. According to the Pew Research Center, India has the largest population of vegetarians in the world, creating an inherent demand for plant based dosage forms. Hydroxypropyl methylcellulose (HPMC) and pullulan capsules are gaining traction as ideal substitutes, offering similar performance characteristics without animal origins. In China, the rises of the middle class and greater exposure to global wellness trends have fueled interest in plant based supplements. According to the Global Wellness Institute, China and Japan are among the top five largest wellness markets globally, with consumers increasingly favoring natural ingredients. Manufacturers are responding by expanding their portfolios of HPMC and starch based capsules to cater to this niche but rapidly growing segment. In Southeast Asian nations with significant Muslim populations, halal certified vegetarian capsules offer a competitive advantage. The Indonesian Ulema Council emphasizes the importance of halal certification for pharmaceutical products, further driving the adoption of non-animal capsules. Additionally, the perception of plant based capsules as cleaner and more natural aligns with the broader clean label movement in the food and beverage industry. By investing in the production of high quality vegetarian alternatives, manufacturers can tap into a dedicated customer base willing to pay a premium for ethically sourced products. This shift towards plant based options opens new avenues for growth and differentiation in the competitive empty capsules market.

Advancements in Modified Release and Targeted Delivery Technologies

Technological advancements in modified release and targeted delivery systems offer significant opportunities for innovation in the Asia Pacific empty capsules market. Pharmaceutical companies are increasingly seeking specialized capsules that can control the release of active ingredients to improve efficacy and reduce side effects. As per the Journal of Controlled Release, enteric coated and delayed release capsules are becoming essential for drugs that need to bypass the stomach acid or target specific intestinal regions. In Japan, leading pharmaceutical firms are collaborating with capsule manufacturers to develop innovative formulations for chronic disease management. According to the Japanese Society for the Study of Diabetes, novel delivery systems are crucial for improving patient adherence and therapeutic outcomes. The development of capsules with enhanced barrier properties against moisture and oxygen extends the shelf life of sensitive biologics and probiotics. In India, the growing biosimilar sector requires advanced encapsulation techniques to maintain protein stability. The Indian Institute of Chemical Technology is actively researching smart capsule technologies that respond to physiological triggers. Furthermore, the integration of digital health markers into capsules for patient monitoring is an emerging trend. Manufacturers who invest in research and development to create specialized functional capsules can command higher margins and establish long term partnerships with pharmaceutical innovators. The ability to offer customized solutions for complex drug formulations positions companies at the forefront of technological progress. This focus on value added products transforms empty capsules from simple containers into integral components of advanced drug delivery strategies, driving market growth.

MARKET CHALLENGES

Competition from Alternative Dosage Forms

The intense competition from alternative dosage forms such as tablets, softgels, and liquids poses a challenge to the empty capsules market expansion in the Asia-Pacific. Tablets remain the most widely used oral dosage form due to their lower manufacturing costs, stability, and ease of mass production. According to the Global Market Insights report on the Asia Pacific over the counter drugs market, the tablets segment dominated the market in 2024 with 63.6% of the market share. In China, the dominance of traditional Chinese medicine often in tablet or liquid form limits the penetration of capsules in certain therapeutic areas. According to the Chinese Pharmaceutical Association, the output of various medication forms continues to grow, with tablets maintaining a high volume due to established manufacturing infrastructure. Softgels are also gaining popularity for lipid based formulations and a vitamin, providing a seamless alternative for liquid fills. In Australia, the Therapeutic Goods Administration notes that softgels are preferred for certain supplements due to their aesthetic appeal and perceived potency. The flexibility of tablets in terms of shape, size, and branding allows pharmaceutical companies to differentiate their products effectively. Additionally, the development of orally disintegrating tablets offers convenience for patients with swallowing difficulties, a key advantage traditionally held by capsules. The cost efficiency of tablet compression compared to capsule filling machines makes tablets more attractive for generic manufacturers operating on tight margins. This competitive pressure forces capsule manufacturers to continuously innovate and justify their value proposition. Without distinct advantages in performance or patient preference, the market share of empty capsules faces constant threat from these versatile and cost effective alternatives.

Environmental Concerns and Waste Management Issues

Growing environmental concerns regarding the disposal of pharmaceutical packaging and capsule materials present a significant challenge for the Asia Pacific market. While gelatin is biodegradable, the industrial production process involves significant water and energy consumption, raising sustainability issues. As per the United Nations Environment Programme, the pharmaceutical industry is under increasing pressure to reduce its environmental footprint, including waste generated from excipient manufacturing. In India, the Central Pollution Control Board has tightened regulations on industrial effluent discharge, affecting gelatin production facilities. According to the Indian Green Building Council, sustainable sourcing and waste reduction are becoming critical criteria for corporate procurement. Plastic based blister packs commonly used for capsule packaging contribute to non-biodegradable waste, exacerbating the environmental impact. In Japan, the Ministry of the Environment promotes circular economy principles, encouraging companies to adopt eco-friendly packaging solutions. The challenge lies in balancing the need for protective packaging with environmental responsibility. Consumers are increasingly aware of ecological issues and may prefer brands with sustainable practices. However, transitioning to green manufacturing processes and biodegradable packaging requires substantial investment and technological innovation. In Southeast Asia, inadequate waste management infrastructure in some regions leads to improper disposal of medical waste. Manufacturers face the dual challenge of optimizing production efficiency while minimizing environmental harm. Failure to address these sustainability concerns can damage brand reputation and lead to regulatory restrictions. Thus, environmental stewardship remains a complex and ongoing challenge for the empty capsules market in the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.34% |

| Segments Covered | By Product, Therapeutic Application, End User and Region |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the Rest of APAC. |

| Market Leaders Profiled | Capsugel, ACG Worldwide, Suheung Co Ltd., Bright Pharmacaps Inc., Capscanada Corporation, Medi-Caps Ltd., Qualicaps, Roxlor, LLC, Snail Pharma Industry Co.Ltd, and Sunil Healthcare Limited. |

SEGMENTAL ANALYSIS

By Product Insights

The gelatin capsules segment commanded the dominant position in the Asia Pacific empty capsules market by holding 71.6% of the regional market share in 2025. The dominance of gelatin capsules segment in this regional market is primarily driven by their cost effectiveness, superior mechanical properties, and widespread acceptance in the pharmaceutical industry. The lower production cost and the well-established manufacturing infrastructure across the Asia Pacific region is further contributing to the dominance of gelatin capsules segment in this regional market. Gelatin derived from bovine and porcine collagen is abundantly available and less expensive to process compared to plant based alternatives like HPMC. According to the Food and Agriculture Organization of the United Nations, global meat and livestock production supports a stable supply of materials for gelatin, with Asia serving as a major processing hub. In China, which is the largest producer of gelatin in the region, the economies of scale allow manufacturers to offer competitive pricing. According to the China Gelatin Manufacturers Association, the domestic production capacity has expanded significantly, ensuring a steady supply chain for capsule manufacturers. The mature technology for gelatin capsule production requires less capital investment compared to newer alternatives, making it the preferred choice for generic drug manufacturers who operate on thin margins. In India, the vast generic pharmaceutical sector relies heavily on gelatin capsules due to their affordability. According to the Indian Drug Manufacturers Association, the pharmaceutical sector's reliance on cost effective oral solid dosage forms is a cornerstone of its manufacturing strategy. The familiarity of formulation scientists with gelatin properties, such as dissolution rates and stability, further cements its position. The extensive network of suppliers and standardized quality control protocols reduce operational risks for pharmaceutical companies. This economic advantage, combined with technical reliability, ensures that gelatin capsules remain the backbone of the empty capsules market in the region.

However, the non-gelatin capsules segment is estimated to record a CAGR of 10.5% over the forecast period in this regional market owing to the rising demand for vegetarian and vegan friendly options and religious considerations. The increasing consumer preference for vegetarian and vegan friendly products is further supporting the expansion of the non-gelatin capsules segment in the Asia Pacific region. Health consciousness and ethical considerations are driving individuals to avoid animal derived ingredients in their medications and supplements. According to the Pew Research Center, India has the largest vegetarian population globally, creating a substantial inherent demand for plant based dosage forms. Hydroxypropyl methylcellulose (HPMC) capsules made from plant cellulose are gaining popularity as they align with these lifestyle choices. In China, the rising middle class is increasingly adopting wellness trends that favor natural and plant based products. According to the Global Wellness Institute, China is a top global market for healthy eating and nutrition, growing at a pace that supports plant based encapsulation. HPMC capsules offer similar performance to gelatin but without the animal origin, making them ideal for this segment. In Australia, the Therapeutic Goods Administration reports a steady increase in the registration of complementary medicines, many of which utilize vegetarian certified formats. The clean label movement, which emphasizes transparency and natural ingredients, further supports this trend. Manufacturers are investing in HPMC production facilities to meet this growing need. The ability to market products as vegetarian or vegan provides a competitive edge in the crowded supplement market. As awareness of dietary preferences grows, the adoption of non-gelatin capsules is accelerating across various therapeutic areas.

By Therapeutic Application Insights

The vitamins and dietary supplements segment led the market by holding 41.4% of the Asia-pacific market share in 2025. The dominance of vitamins and dietary supplements segment in this regional market is primarily attributed to the widespread use of capsules for delivering nutrients and the booming wellness industry. The booming wellness industry and the shifting focus towards preventive healthcare in the Asia Pacific region are also propelling the growth of the vitamins and dietary supplements segment in this regional market. Consumers are increasingly proactive about managing their health through regular intake of multivitamins, minerals, and herbal extracts. According to the Global Wellness Institute, the Asia Pacific region hosts some of the largest wellness markets, including China at $950 billion and Japan at $262 billion. In China, the State Administration for Market Regulation reported that the health food market has expanded significantly, with capsules being a preferred format for premium supplements. Capsules offer advantages such as odor masking and protection of sensitive ingredients from oxidation, which is crucial for vitamins like C and E. According to the Global Wellness Institute, healthy eating and nutrition is a leading sector in the region's wellness economy. In India, the Ministry of Ayush promotes traditional herbal remedies, many of which are now packaged in capsules for modern convenience. The Indian Drug Manufacturers Association notes a surge in the production of herbal capsules catering to both domestic and export markets. The aging population in Japan and South Korea also contributes to high demand for joint health and cognitive support supplements often delivered via capsules. The convenience of capsules compared to powders or liquids makes them ideal for daily routines. This strong consumer preference for convenient and effective nutrient delivery sustains the leading position of this segment.

However, the cardiovascular therapy drugs segment is estimated to witness a CAGR of 9.1% over the forecast period in this regional market owing to the rising prevalence of heart diseases and the need for effective drug delivery systems. The escalating prevalence of cardiovascular diseases (CVD) in the Asia Pacific region is further favouring the expansion of the cardiovascular therapy drugs segment in this regional market. Lifestyle changes, including poor diet, sedentary behavior, and smoking, have led to a surge in hypertension and coronary artery disease. As per the World Health Organization, cardiovascular diseases cause 17.9 million deaths annually worldwide, with over 75% of these occurring in low and middle income countries. In China, the National Center for Cardiovascular Diseases reports that over 330 million people suffer from some form of cardiovascular condition. This massive patient pool requires long term medication management often involving multiple drugs. Capsules are increasingly used for delivering antihypertensives and lipid lowering agents due to their ability to improve patient compliance. According to the Chinese Medical Journal, recent clinical trials involving traditional capsules for heart function have shown significant improvements in patient compliance and health outcomes. In India, the Indian Heart Association highlights that cardiovascular diseases affect younger populations, necessitating early and consistent treatment. The ease of swallowing capsules is particularly beneficial for elderly patients who often suffer from dysphagia. The growing awareness of heart health is driving regular check ups and subsequent medication adherence. Governments are launching national programs to combat CVDs, increasing access to affordable medicines. The sustained demand for effective and compliant drug delivery systems positions cardiovascular therapy as a high growth area for empty capsules.

By End User Insights

The pharmaceutical segment dominated the market by holding 61.6% of the regional market share in 2025. This dominance is attributed to the massive scale of drug production and the critical role of capsules in generic medicine manufacturing. The massive scale of generic drug production in the Asia Pacific region, particularly in India and China is also boosting the dominance of pharmaceutical segment in the regional market. These countries are known as the pharmacy of the world, supplying a significant portion of global generic medicines. According to the United States Pharmacopeia, India leads in essential API manufacturing and maintains a dominant lead in total active pharmaceutical ingredient filings. The National Medical Products Administration in China has facilitated the rapid approval of generic drugs, leading to a surge in manufacturing volumes. According to the Chinese Pharmaceutical Association, the output value of traditional medicine and generic medications remains a cornerstone of the $160 billion industry. Empty capsules are a preferred dosage form for many generic drugs due to their cost effectiveness and ease of manufacturing. The ability to quickly switch between different drug fills on the same production line enhances operational efficiency. In Southeast Asia, the growing local pharmaceutical sectors in Vietnam and Indonesia are also increasing their reliance on capsules for domestic drug supply. The Association of Southeast Asian Nations harmonizes regulatory standards, facilitating regional trade and production scaling. The sheer volume of prescriptions filled with generic drugs ensures a consistent and high demand for empty capsules. This industrial scale consumption cements the pharmaceutical industry as the leading end user in the market.

On the other end, the nutraceutical segment is expected to exhibit a CAGR of 10.6% over the forecast period in the Asia-pacific empty capsules market owing to the expanding wellness market and increased consumer health awareness. Individuals are increasingly taking charge of their health through supplements and functional foods. According to the Global Wellness Institute, India is among the top countries for annual wellness market growth, exceeding 10% between 2019 and 2024. In China, the State Administration for Market Regulation reports a surge in the registration of health food products, many of which are encapsulated. According to the Global Wellness Institute, China's wellness market is the second largest in the world, valued at $950 billion. Capsules are perceived as more potent and professional than gummies or tablets. In India, the Ministry of Ayush promotes the integration of traditional herbs into modern supplement forms, boosting the nutraceutical sector. The Indian Drug Manufacturers Association notes a significant increase in the launch of new nutraceutical brands. The aging population in Japan and South Korea drives demand for anti-aging and cognitive health supplements. The convenience of capsules fits well with busy urban lifestyles. As health consciousness becomes a mainstream value, the consumption of nutraceuticals continues to rise. This trend fuels the rapid adoption of empty capsules by nutraceutical manufacturers seeking to meet consumer expectations.

REGIONAL ANALYSIS

China Empty Capsules Market Analysis

China stood as the largest market for empty capsules in the Asia Pacific region by capturing 35.4% of the regional market share in 2025. The massive manufacturing capacity, a booming domestic healthcare sector, the expansion of the generic pharmaceutical industry and rising health consciousness are propelling the dominance of China in the Asia-Pacific empty capsules market. According to the National Medical Products Administration, China has surpassed other regions in new active pharmaceutical ingredient filings, accounting for 45% of new filings in 2024. As per the Chinese Pharmaceutical Association, while generic drugs fuel the bulk of the volume, the industry is shifting toward high innovation. The government’s Healthy China 2030 initiative promotes preventive care, boosting the nutraceutical market. According to the State Administration for Market Regulation, the health food industry is expanding rapidly, with capsules being a preferred format. Local manufacturers are upgrading technologies to meet international quality standards. The presence of major gelatin producers ensures a stable supply chain. The rising middle class is demanding higher quality healthcare products, driving innovation. The regulatory environment is becoming more stringent, ensuring product safety. These factors combined with the sheer scale of the population make China the dominant force in the regional empty capsules market. Continued investment in healthcare infrastructure supports sustained growth.

India Empty Capsules Market Analysis

India is predicted to occupy a prominent share of the Asia-Pacific empty capsules market during the forecast period. The Indian market is defined by its role as a global hub for generic pharmaceuticals and traditional medicine. The primary driving factors are the robust export oriented pharmaceutical sector and the growing domestic nutraceutical market. According to the United States Pharmacopeia, India holds 48% of total active pharmaceutical ingredient filings, a share that did not decrease from 2021 levels. The Indian Drug Manufacturers Association notes that the production of herbal capsules is increasing due to global demand for Ayurvedic products. The Ministry of Ayush supports the standardization and modernization of traditional medicines. According to the World Health Organization, over 75% of cardiovascular deaths occur in low and middle income countries, highlighting the disease burden driving therapeutic demand in India. The cost competitiveness of Indian manufacturing attracts global partnerships. Local capsule manufacturers are expanding capacity to meet domestic and international needs. The government’s focus on affordable healthcare ensures steady demand for generic medicines. The growing awareness of wellness among the urban population boosts the nutraceutical sector. These dynamics position India as a critical growth engine in the regional market.

Japan Empty Capsules Market Analysis

Japan is anticipated to account for a notable share of the Asia-Pacific empty capsules market during the forecast period owing to the high quality standards and an aging population. The driving factors include the demand for advanced drug delivery systems and the preference for easy to swallow medications. According to the Global Wellness Institute, Japan has the fourth largest wellness market in the world, valued at $262 billion in 2024. The elderly population requires medications that are easy to administer. The Japanese Pharmaceutical Society reports a steady demand for capsule based therapies for chronic conditions. The regulatory framework enforced by the Pharmaceuticals and Medical Devices Agency ensures high product quality. According to the Japanese Ministry of Economy, Trade and Industry, the pharmaceutical industry is investing in innovation. The preference for natural and safe ingredients drives the use of high quality capsules.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific Empty Capsules Market is characterized by the presence of established global leaders and emerging regional manufacturers. Leading multinational corporations leverage their extensive distribution networks technological expertise and brand reputation to maintain dominance. However local players in countries like India and China are gaining traction by offering cost effective alternatives and flexible customization options. The market witnesses intense competition based on product quality price and innovation capabilities. Companies are increasingly focusing on developing vegetarian and vegan friendly capsules to cater to changing consumer preferences. Strategic collaborations with pharmaceutical and nutraceutical firms are common tactics to secure long term contracts. Regulatory compliance and certification play a crucial role in differentiating competitors in this highly regulated industry. Price wars are prevalent in the generic segment prompting manufacturers to optimize production efficiencies. Innovation in capsule coatings and delivery mechanisms serves as a key differentiator for premium segments. The entry of new participants with specialized technologies further intensifies the competitive landscape. This dynamic environment drives continuous improvement in product offerings and service quality across the region.

KEY MARKET PLAYERS

A few of the notable companies in the APAC Empty Capsules Market include

- Capsugel

- ACG Worldwide

- Suheung Co. Ltd.

- Bright Pharmacaps Inc.

- Capscanada Corporation

- Medi-Caps Ltd.

- Qualicaps

- Roxlor, LLC

- Snail Pharma Industry Co. Ltd.

- Sunil Healthcare Limited

Top Players in the Market

ACG World

ACG World is a leading global provider of integrated pharmaceutical solutions with a strong presence in the Asia Pacific empty capsules market. The company contributes significantly to the global market by offering high quality gelatin and HPMC capsules that meet international regulatory standards. Recent actions include expanding its manufacturing facilities in India and China to enhance production capacity and reduce lead times for regional customers. ACG World actively invests in research and development to innovate sustainable capsule materials and advanced coating technologies. The company collaborates with major pharmaceutical manufacturers to provide customized drug delivery solutions. By focusing on operational excellence and customer centric services ACG World strengthens its position as a trusted partner in the healthcare industry. Its commitment to quality and innovation ensures consistent growth and reinforces its leadership in the dynamic Asia Pacific region.

Lonza Group AG

Lonza Group AG is a prominent supplier of specialty ingredients and pharmaceutical technologies including empty capsules through its Capsugel brand. The company plays a pivotal role globally by setting benchmarks for quality and reliability in capsule manufacturing. In the Asia Pacific region Lonza has strengthened its market position by launching innovative vegetarian capsule options such as Vcaps Plus. Recent strategies involve expanding its technical support centers in Singapore and Shanghai to better serve local clients. Lonza focuses on sustainability by implementing eco friendly manufacturing processes and sourcing raw materials responsibly. The company partners with leading nutraceutical and pharmaceutical firms to develop tailored encapsulation solutions. By leveraging its global expertise and local presence Lonza enhances its competitive edge. Its dedication to scientific excellence and customer collaboration drives continuous improvement and solidifies its reputation in the Asia Pacific empty capsules market.

Qualicaps Co Ltd

Qualicaps Co Ltd is a key player in the Asia Pacific empty capsules market known for its high quality gelatin and HPMC capsules. The company contributes to the global market by delivering consistent and reliable products that adhere to strict quality standards. Recent actions include upgrading its production facilities in Japan and Thailand to increase efficiency and meet growing demand. Qualicaps focuses on innovation by developing specialized capsules for modified release applications and sensitive active ingredients. The company engages in strategic partnerships with regional distributors to expand its reach in emerging markets. Qualicaps emphasizes sustainability by reducing waste and energy consumption in its operations. By prioritizing product quality and customer satisfaction Qualicaps maintains a strong competitive position. Its commitment to technological advancement and environmental responsibility ensures sustained growth and reinforces its leadership in the Asia Pacific region.

Top Strategies Used by the Key Market Participants

Key players in the Asia Pacific Empty Capsules Market primarily employ strategies such as capacity expansion and facility upgrades to meet rising demand. Companies frequently invest in research and development to innovate new capsule materials including vegetarian and sustainable options. Strategic partnerships with local distributors and pharmaceutical manufacturers help enhance market penetration and customer reach. Focus on quality assurance and regulatory compliance ensures adherence to international standards and builds trust. Sustainability initiatives such as reducing carbon footprints and optimizing resource usage are increasingly prioritized. Digital transformation through automated manufacturing processes improves efficiency and reduces costs. These multifaceted approaches enable companies to strengthen their competitive positions and address the evolving needs of the healthcare and nutraceutical industries in the Asia Pacific region effectively.

MARKET SEGMENTATION

This research report on the APAC Empty Capsules Market has been segmented and sub-segmented into the following categories

By Product

- Gelatin Capsules

- Non-Gelatin Capsules

By Therapeutic Application

- Antibiotic And Antibacterial Drugs

- Vitamins And Dietary Supplements

- Antacid And Antiflatulent Preparations

- Antianemic Preparations

- Anti-Inflammatory Drugs

- Cardiovascular Therapy Drugs

- Cough And Cold Preparations

- Other Therapeutic Application

By End User

- Pharmaceutical Industry

- Nutraceutical Industry

- Cosmetics Industry

- Research Laboratories

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com