Asia Pacific Energy Management System (EMS) Market Research Report – Segmented By Type of Ems (BEMS (Building EMS), IEMS (Industrial EMS), HEMS (Home EMS)), End-Use, Component, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2026 to 2034

Market Size, 2025

$15.14 BnMarket Estimate, 2026

$17.33 BnMarket Forecast, 2034

$51.05 BnCAGR, 2026–2034

14.46%Asia Pacific Energy Management System (EMS) Market Size

The Asia Pacific energy management system (EMS) market size was valued at USD 15.14 billion in 2025 and is anticipated to reach USD 17.33 billion in 2026 from USD 51.05 billion by 2034, growing at a CAGR of 14.46% during the forecast period from 2026 to 2034.

Energy management system (EMS) refers to a sophisticated network of digital platforms and control technologies designed to monitor, optimize, and regulate energy consumption across industrial, commercial, and residential infrastructures. These systems integrate real-time data analytics, automation, and machine learning to enhance energy efficiency, reduce operational costs, and support sustainability mandates. In recent years, rapid urbanization and industrial expansion across the region have intensified energy demand, prompting governments and private entities to adopt EMS solutions for improved energy governance.

As per the International Energy Agency, energy consumption in the Asia Pacific region grew by 3.5% in 2023, outpacing global averages, driven primarily by economic growth in India and Southeast Asia. Countries such as Japan and South Korea have institutionalized energy audits and smart grid integration, while emerging economies like Vietnam and Indonesia are advancing regulatory frameworks for energy efficiency. The proliferation of smart cities, further underscores the systemic need for intelligent energy oversight. These developments position EMS not merely as a technological upgrade but as a strategic imperative in balancing energy security, economic growth, and decarbonization across one of the world’s most dynamic regions.

MARKET DRIVERS

Rising Industrial Energy Demand and Regulatory Pressure for Efficiency

The industrial sector in the Asia Pacific region accounts for nearly 55% of total final energy consumption, as per the International Energy Agency in 2023, making it the largest energy-consuming segment. This substantial demand is amplified by the expansion of manufacturing hubs in countries like China, India, and Thailand, where energy-intensive industries such as steel, cement, and chemicals dominate. To manage escalating energy costs and comply with tightening environmental regulations, enterprises are increasingly deploying energy management systems to optimize production processes. For instance, China’s 14th Five-Year Plan mandates a 13.5% reduction in energy intensity by 2025 compared to 2020 levels. Similarly, India’s Perform, Achieve, and Trade (PAT) scheme, which covers over 1,500 designated industrial units, has driven a 7.8% improvement in energy efficiency between 2012 and 2022, according to the Bureau of Energy Efficiency. These regulatory frameworks incentivize the integration of EMS to meet compliance targets and capitalize on energy savings. Additionally, the rise of green manufacturing standards, such as Japan’s Top Runner Program and South Korea’s Energy Efficiency Labeling Scheme, further accelerates EMS adoption. As industries face growing pressure to decarbonize, EMS serves as a critical tool for aligning operational efficiency with national climate goals, ensuring sustained competitiveness in a carbon-constrained economy.

Urbanization and the Expansion of Smart Infrastructure

Asia Pacific is undergoing the most rapid urban transformation in human history. This demographic shift is driving unprecedented demand for intelligent infrastructure capable of managing energy loads efficiently. Cities such as Singapore, Sydney, and Seoul are pioneering integrated EMS platforms to regulate energy use in buildings, transportation, and public utilities. Singapore’s Smart Nation initiative, for example, has deployed city-wide energy management systems. Moreover, the region is witnessing a surge in green building certifications; Australia alone recorded over 2,800 Green Star-rated buildings by 2023, according to the Green Building Council of Australia. These structures rely heavily on EMS for HVAC optimization, lighting control, and renewable energy integration. The proliferation of smart grids further amplifies this trend—Japan has installed over 80 million smart meters as of 2023, enabling bidirectional energy data flow essential for demand-side management. As urban centers grapple with energy reliability and sustainability, EMS becomes indispensable in orchestrating decentralized energy resources and enhancing grid resilience. The convergence of digital infrastructure, municipal climate targets, and rising electricity demand positions urban development as a pivotal catalyst for EMS market expansion across the region.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks and Policy Implementation Gaps

The Asia Pacific region suffers from inconsistent regulatory enforcement and divergent policy priorities across jurisdictions. While countries like Japan and South Korea have established comprehensive energy efficiency mandates, others such as Indonesia and the Philippines lack standardized compliance mechanisms for energy management systems. According to the Asian Development Bank, only few regional economies have fully implemented mandatory energy efficiency codes for buildings. In India, although the Energy Conservation Act of 2001 established the legal foundation for energy audits, enforcement remains weak in smaller industrial clusters. Moreover, cross-border disparities in certification standards—such as varying interpretations of ISO 50001—hinder interoperability and discourage multinational firms from uniform EMS deployment. The absence of harmonized incentives further exacerbates the issue; while China offers subsidies covering a portion of EMS installation costs in pilot cities. This regulatory asymmetry increases compliance complexity and raises operational costs for enterprises operating across multiple markets. As a result, many organizations delay investment in EMS due to uncertainty over long-term policy stability. Without coordinated regional frameworks and stronger institutional capacity, the full potential of energy management systems will remain constrained, particularly in emerging economies where institutional infrastructure is still evolving.

High Upfront Costs and Limited Access to Financing Mechanisms

The deployment of advanced energy management systems often requires significant initial capital, including expenses for sensors, control hardware, software licensing, and system integration. For small and medium-sized enterprises (SMEs), which constitute over 90% of businesses in the Asia Pacific region as per the United Nations Industrial Development Organization, these costs present a formidable barrier. The average payback period for EMS installations in manufacturing facilities ranges from 2.5 to 4 years, discouraging risk-averse operators, particularly in economies with volatile interest rates. Even in more developed markets, budget constraints persist. Additionally, the lack of standardized performance metrics makes it difficult to secure loans based on projected energy savings. While energy service companies (ESCOs) offer performance-based contracts, their presence remains limited outside major urban centers. Without accessible leasing models, government-backed credit enhancement, or scalable pay-as-you-save schemes, the financial burden continues to stifle widespread EMS penetration, particularly among the very sectors that stand to benefit most from energy optimization.

MARKET OPPORTUNITIES

Integration of Renewable Energy and Grid Modernization Initiatives

The aggressive expansion of renewable energy capacity across Asia Pacific is creating a compelling opportunity for energy management systems to play a central role in grid stability and energy balancing. This rapid influx of variable generation sources necessitates advanced EMS platforms capable of forecasting generation, managing demand response, and optimizing storage utilization. In Australia, where rooftop solar penetration exceeds 30% in some states, distribution networks are deploying EMS to mitigate voltage fluctuations and prevent grid congestion. Beyond utility-scale applications, microgrids in remote areas of the Philippines and Indonesia are leveraging EMS to integrate solar-diesel hybrids, improving energy access for substantial number of people. Furthermore, national grid modernization programs, such as India’s Revamped Distribution Sector Scheme, allocate substantial funding for digital control systems that rely on EMS for loss reduction and load forecasting. As renewable penetration surpasses in countries like Vietnam and Thailand, the technical complexity of managing bidirectional energy flows intensifies, elevating the strategic value of EMS. This transition positions energy management systems not merely as efficiency tools but as foundational components of a decentralized, resilient, and low-carbon energy architecture across the region.

Growth of Industrial Internet of Things and Data-Driven Energy Optimization

The convergence of Industrial Internet of Things (IIoT) and artificial intelligence is unlocking transformative potential for energy management systems in Asia Pacific’s industrial landscape. IIoT enables granular energy monitoring through thousands of connected sensors, feeding real-time data into EMS platforms for predictive analytics and anomaly detection. The rise of digital twins, virtual replicas of physical plants, further enhances EMS capabilities; Tata Steel’s Jamshedpur facility in India reduced energy waste by 12% in 2023 using a digital twin synchronized with its EMS, as per the company’s sustainability division. Cloud-based EMS platforms are also gaining traction, allowing SMEs to access enterprise-grade analytics without heavy infrastructure investment. Alibaba Cloud’s Energy Brain platform, deployed across 200 Chinese industrial sites, has demonstrated energy savings of up to 15% through machine learning-driven load optimization. As data becomes a strategic asset, the synergy between IIoT and EMS is redefining energy governance, enabling proactive decision-making, and setting new benchmarks for operational excellence across Asia Pacific’s industrial ecosystem.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Networked Energy Systems

As energy management systems become increasingly interconnected and reliant on cloud-based architectures, they are exposed to escalating cybersecurity threats. These systems, which often interface with building automation, industrial control systems, and smart grids, present a broad attack surface for malicious actors seeking to disrupt operations or steal sensitive data. Furthermore, legacy systems in countries like Indonesia and Bangladesh remain incompatible with modern security protocols, creating systemic risks. The decentralized nature of renewable integration compounds the issue, as distributed energy resources often operate on less-secured edge devices. Without robust encryption standards, continuous threat monitoring, and workforce training, the digitalization of energy management could inadvertently undermine grid reliability and national energy security, particularly as geopolitical tensions heighten the risk of state-sponsored cyber operations.

Workforce Skill Gaps and Technical Expertise Shortages

The effective deployment and maintenance of energy management systems requires a specialized workforce proficient in data analytics, control engineering, and energy modeling—skills that remain in short supply across much of the Asia Pacific. According to the International Labour Organization, the region faces a deficit of over 1.2 million energy efficiency professionals, particularly in emerging economies where technical education lags behind technological adoption. In India, only 18% of engineering graduates possess the competencies needed for smart energy system integration, as reported by the All India Council for Technical Education. This gap is further exacerbated by the rapid evolution of EMS technologies, which demand continuous upskilling in AI, cybersecurity, and IoT protocols. In Vietnam, a 2023 survey by the Ministry of Industry and Trade found that 74% of industrial facilities lacked in-house personnel capable of operating advanced EMS platforms, forcing reliance on external vendors and increasing operational delays. Similarly, in Australia, the Clean Energy Council identified a 30% shortfall in certified energy auditors, hindering the commissioning of new EMS installations. The scarcity of certified professionals also affects system performance; poorly configured EMS can result in suboptimal energy savings or even increased consumption due to algorithmic errors. While governments are launching training initiatives, such as Japan’s Green Talent Program, scaling these efforts to match deployment rates remains a challenge. Without a coordinated strategy involving academia, industry, and policymakers to build a skilled workforce, the region risks underutilizing its energy management infrastructure, undermining both economic and environmental objectives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 14.46% |

| Segments Covered | By Type of Ems, End-Use, Component and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, the Philippines, Indonesia, Singapore, and the rest of APAC. |

| Market Leaders Profiled | Schneider Electric, Siemens, Honeywell International, ABB, Johnson Controls, General Electric (GE), IBM, Cisco Systems, Rockwell Automation, Emerson Electric, Eaton, Yokogawa Electric, Mitsubishi Electric, Azbil Corporation, Toshiba Corporation, Daikin Industries, C3.ai, ENGIE Impact, eSight Energy, Optimum Energy, Enel X, and Uplight.. |

SEGMENTAL ANALYSIS

By Type of EMS Insights

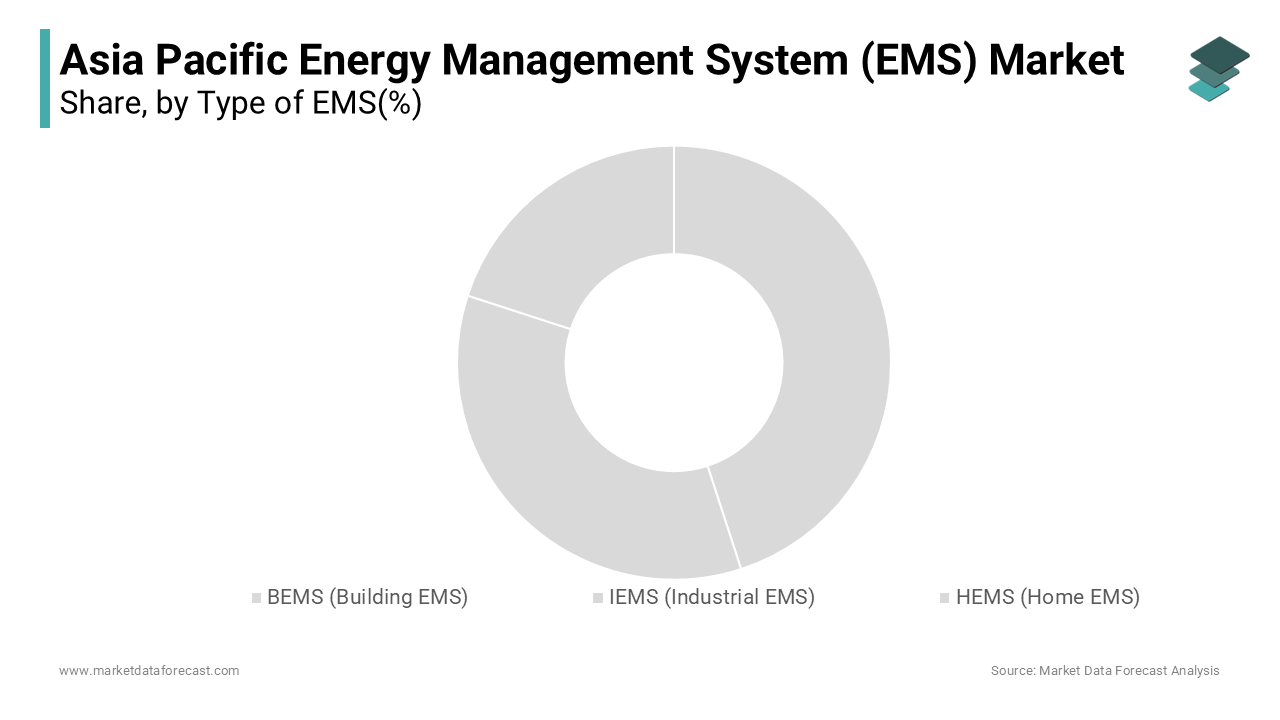

The Building Energy Management Systems (BEMS) segment commanded the largest share of the Asia Pacific energy management system market at 52.5% of total revenue in 2025. This dominance is primarily fueled by the region’s accelerating urbanization and the proliferation of commercial and high-rise residential infrastructure. These systems are now integral to managing HVAC, lighting, and power distribution in large office complexes, shopping malls, and airports. Moreover, Australia’s Commercial Building Disclosure program requires energy efficiency ratings for office spaces over 2,000 square meters, compelling property owners to deploy BEMS for compliance. The convergence of regulatory mandates, rising electricity tariffs in urban centers, and corporate sustainability goals—such as net-zero pledges by companies like Mitsubishi and DBS Bank—is reinforcing BEMS as a strategic asset. Hence, the economic and operational imperative for intelligent building control continues to solidify BEMS’ market leadership.

The Home Energy Management System (HEMS) segment is expanding at an unprecedented compound annual growth rate of 18.7% from 2026 to 2034. This surge is driven by the rapid adoption of smart home technologies and the increasing integration of distributed energy resources at the residential level. The rise of time-of-use electricity pricing in markets like Australia and New South Wales is further incentivizing consumers to manage consumption patterns through HEMS. Additionally, utility-led programs such as Singapore’s PowerSaver initiative offer rebates for HEMS installation, accelerating uptake. As battery storage costs decline, residential energy systems are becoming more complex, necessitating HEMS for coordination between solar, storage, and grid supply. This shift transforms households from passive consumers to active energy participants, positioning HEMS at the forefront of the decentralized energy revolution in Asia.

By End-User Industry Insights

The manufacturing sector held a commanding share of the Asia Pacific energy management system market in 2025. Manufacturing facilities, from semiconductor fabs in Taiwan to textile mills in Bangladesh, are under mounting pressure to reduce energy costs and meet sustainability benchmarks. The semiconductor industry, concentrated in South Korea and Taiwan, exemplifies this trend. Additionally, multinational corporations like Toyota and Panasonic enforce global energy standards across their Asian plants, requiring real-time monitoring and reporting capabilities. With energy costs representing a notable share of operational expenses in industries such as steel and cement, EMS adoption is no longer optional but a strategic necessity for competitiveness. As industrial automation and digital twin technologies gain traction, the integration of EMS into production ecosystems is deepening, reinforcing manufacturing’s dominance in the regional EMS landscape.

The IT and telecommunication sector is experiencing the fastest growth in EMS adoption across the Asia Pacific, with a CAGR of 19.3% from 2026 to 2034. This acceleration is rooted in the exponential expansion of data centers and 5G infrastructure, both of which are extraordinarily energy-intensive. The rollout of 5G networks further amplifies demand; each 5G base station consumes up to three times more power than its 4G predecessor. Telecom operators like Singtel and Reliance Jio are integrating EMS to manage site-level energy use and integrate renewable microgrids. Regulatory pressures are also mounting. As digitalization intensifies, the need for resilient, low-carbon IT infrastructure ensures that EMS will remain a cornerstone of the sector’s operational strategy.

By Component Insights

The software segment constituted the prominent component in the Asia Pacific energy management system market by capturing 44.3% of total revenue in 2025. This position reflects a fundamental shift from hardware-centric monitoring to intelligent, analytics-driven energy governance. Modern EMS software platforms leverage artificial intelligence, machine learning, and cloud computing to deliver predictive insights, anomaly detection, and automated control strategies. The growing complexity of energy ecosystems spanning renewables, storage, and demand response necessitates advanced software to coordinate operations. Furthermore, subscription-based licensing models (SaaS) are gaining traction, particularly among SMEs, offering lower entry barriers and continuous updates. As energy systems become more dynamic and data-rich, software is no longer a supporting component but the central intelligence layer, solidifying its dominance in the EMS value chain.

The services segment is expanding at a CAGR of 20.1% from 2026 to 2034. This surge is propelled by the increasing complexity of EMS deployment and the growing demand for lifecycle support, including system integration, energy auditing, cybersecurity, and performance verification. In Thailand, the Energy Conservation Promotion Act mandates energy audits for large industrial consumers, creating a robust market for EMS consulting services. Moreover, managed EMS services are also gaining traction. Moreover, performance contracting models—where service providers guarantee energy savings are becoming prevalent, particularly in public infrastructure. With digital transformation accelerating, the need for specialized, ongoing support ensures that services will remain the fastest-growing pillar of the EMS ecosystem.

REGIONAL ANALYSIS

China Energy Management System (EMS) Market Insights

China stood as the dominant force in the Asia Pacific energy management system market by commanding a 34.4% share of regional revenue in 2025. Its lead position is anchored in a comprehensive national strategy to achieve carbon peak by 2030 and carbon neutrality by 2060. Under its 14th Five-Year Plan, China has mandated energy efficiency improvements across industrial enterprises and committed a substantial amount to smart grid and digital energy infrastructure. The country leads globally in BEMS deployment. Additionally, China’s dominance in manufacturing drives extensive EMS adoption in sectors like electronics, steel, and chemicals. The rise of domestic tech giants such as Huawei and Alibaba, which offer integrated EMS platforms, further accelerates market penetration. Thus, China’s EMS market is poised for sustained expansion, solidifying its position as the region’s technological and policy leader.

Japan Energy Management System (EMS) Market Insights

Japan is also a key player in the Asia Pacific energy management system market. Despite its mature industrial base, Japan remains a pioneer in advanced EMS integration, driven by energy security concerns and post-Fukushima policy reforms. The country’s Smart Community initiative, led by the Ministry of Economy, Trade and Industry, has established several integrated energy management zones where EMS coordinates power between households, businesses, and utilities. Japan also leads in industrial EMS adoption. The country’s Top Runner Program sets progressively stricter energy efficiency standards, compelling continuous upgrades. Furthermore, Japan’s widespread deployment of Ene-Farm units, residential fuel cells linked to HEMS. Thus, Japan continues to innovate in EMS, particularly in hydrogen-integrated energy networks and digital twin applications, maintaining its status as a high-value, technology-driven market.

India Energy Management System (EMS) Market Insights

India is positioning it as a significant national market. Its growth is fueled by rapid industrialization, urban expansion, and a robust policy framework for energy efficiency. The Bureau of Energy Efficiency points out that over 1,500 industrial units under the Perform, Achieve, and Trade scheme have collectively saved 127 million tonnes of oil equivalent since 2012, driving EMS adoption in cement, textiles, and aluminum sectors. The government’s Revamped Distribution Sector Scheme allocates $33 billion for smart metering and grid modernization, directly benefiting EMS deployment. As of 2023, over 40 million smart meters have been installed, enabling real-time data exchange for demand-side management. In the commercial sector, the Energy Conservation Building Code now applies to all new structures over 1,000 square meters, covering 85% of new urban construction. The Indian Green Building Council confirms that over 7,500 projects are registered under green certification, most incorporating BEMS. Additionally, rising solar penetration, 12.5 gigawatts added in 2023 alone, as per the Ministry of New and Renewable Energy, necessitates EMS for grid stability. Thus, India’s EMS market is on a steep growth trajectory, supported by both public policy and private investment.

South Korea Energy Management System (EMS) Market Insights

South Korea is distinguished by its advanced technological integration and strong government backing. The country’s Green New Deal allocates notable funds to digital and energy infrastructure, including nationwide EMS deployment in public buildings and industrial complexes. As per the Korea Energy Agency, over 90% of government-owned facilities are now equipped with centralized energy management systems, achieving an average 18% reduction in energy use. South Korea leads in smart factory adoption, with the Ministry of Trade, Industry and Energy reporting that 40,000 factories are connected to the Smart K-Factory platform, which integrates EMS for real-time monitoring and AI-based optimization. In the semiconductor sector, Samsung and SK Hynix employ proprietary EMS to manage energy-intensive fabrication processes, reducing power consumption by up to 20%. The country also excels in residential EMS; the Korea Smart Grid Institute confirms that over 1.2 million homes are linked to HEMS through the national smart meter rollout. With a national goal to cut emissions by 40% by 2030 and a thriving domestic tech ecosystem, South Korea’s EMS market is characterized by high innovation, strong public-private collaboration, and deep integration with Industry 4.0 initiatives.

Australia Energy Management System (EMS) Market Insights

Australia accounts for a small share of the Asia Pacific energy management system market, with growth driven by stringent regulatory frameworks and a mature commercial real estate sector. The country’s Commercial Building Disclosure program requires energy efficiency ratings for office spaces, affecting properties and compelling BEMS adoption. As per the Clean Energy Regulator, over 2,800 facilities are registered under the National Energy Productivity Plan, driving demand for energy auditing and management services. In the industrial sector, the Energy Efficiency Opportunities program has identified potential savings of 12 terawatt-hours annually, equivalent to powering 2.5 million homes. Additionally, Australia’s rooftop solar penetration is the highest globally, with over 3.4 million installations, as per the Clean Energy Council, necessitating HEMS for load management and grid interaction. EMS adoption is becoming essential for both cost control and compliance, positioning Australia as a leader in policy-driven energy optimization.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific energy management system market is intensifying as global technology leaders and regional players vie for dominance across diverse regulatory and economic landscapes. The market is characterized by rapid innovation, with companies differentiating through AI integration, cybersecurity robustness, and cloud-native architectures. Multinational corporations such as Schneider Electric, Honeywell, and Siemens leverage their global expertise and extensive portfolios to secure large-scale infrastructure projects, while local firms capitalize on regulatory familiarity and cost advantages. Strategic collaborations with government bodies, utilities, and real estate developers are critical for market access and credibility. The rise of performance-based contracting and energy-as-a-service models is reshaping customer engagement, shifting focus from product sales to outcome-based solutions. Cybersecurity, interoperability, and data sovereignty are emerging as key decision factors, especially in public sector deployments. Smaller players are focusing on niche applications such as SME-focused EMS or renewable integration in off-grid areas. Continuous product upgrades, regional R&D investments, and talent acquisition are essential to maintain a competitive edge. As urbanization and decarbonization mandates accelerate, the competitive landscape is evolving from hardware provision to holistic energy intelligence, requiring agility, scalability, and deep ecosystem integration to succeed.

KEY MARKET PLAYERS

The key players in the Asia Pacific Energy Management System (EMS) market include

- Schneider Electric

- Siemens

- Honeywell International

- ABB

- Johnson Controls

- General Electric (GE)

- IBM

- Cisco Systems

- Rockwell Automation

- Emerson Electric

- Eaton

- Yokogawa Electric

- Mitsubishi Electric

- Azbil Corporation

- Toshiba Corporation

- Daikin Industries

- C3.ai

- ENGIE Impact

- eSight Energy

- Optimum Energy

- Enel X

- Uplight

Top Players in the Asia Pacific Energy Management System Market

Schneider Electric has established a dominant presence in the Asia Pacific energy management system market through its EcoStruxure platform, which integrates IoT-enabled hardware, software, and services for industrial, commercial, and residential applications. The company has deepened its regional footprint by launching localized R&D centers in India, China, and Singapore to tailor solutions for diverse regulatory and climatic conditions. It has also partnered with government agencies in Thailand and Vietnam to support national energy efficiency programs. By expanding its ecosystem of certified system integrators and launching cloud-based EMS subscriptions, Schneider is accelerating adoption among SMEs. Its acquisition of a majority stake in Indian energy analytics firm Grid7 in early 2025 strengthened its data intelligence capabilities. The company continues to invest in green financing models, enabling performance-based contracts across public infrastructure projects, reinforcing its role as a technology and sustainability enabler in the region’s energy transition.

Honeywell plays a pivotal role in shaping the Asia Pacific energy management system landscape, particularly in smart buildings and industrial automation. The company’s Forge Energy Optimization platform leverages AI to deliver real-time insights across commercial and manufacturing facilities, with deployments spanning over 10,000 sites in the region. The company has strengthened its position through strategic collaborations with local utilities. Honeywell also expanded its manufacturing footprint in Malaysia to produce smart sensors and controllers for regional distribution. By embedding cybersecurity protocols into its EMS offerings and launching digital twin solutions for industrial clients in China and India, the company addresses critical operational and safety concerns. Its focus on hybrid workspaces and resilient infrastructure has driven adoption in airports, hospitals, and high-tech campuses, positioning Honeywell as a leader in intelligent, future-ready energy management.

Siemens is a key innovator in the Asia Pacific energy management system market, delivering integrated solutions across urban infrastructure, industry, and power networks. Its Spectrum Power and Desigo CC platforms are widely deployed in smart cities and industrial parks across China, Singapore, and Australia, enabling centralized monitoring and adaptive control. The company also initiated a digitalization partnership with Indonesia’s state utility PLN to modernize distribution systems using EMS-driven analytics. Siemens strengthened its regional services arm by opening a digital energy hub in Bangalore, focusing on cloud-based EMS for manufacturing clients. By collaborating with universities in Japan and South Korea on smart grid research and participating in government-led net-zero city projects, Siemens is advancing scalable, interoperable energy management frameworks. Its commitment to open standards and cybersecurity ensures long-term adaptability, solidifying its reputation as a trusted partner in the region’s sustainable energy evolution.

Top Strategies Used by the Key Market Participants

Key players in the Asia Pacific energy management system market are deploying multi-pronged strategies to consolidate their positions. Strategic partnerships with local utilities and government agencies enable seamless integration into national energy programs. Companies are increasingly investing in AI and cloud-based platforms to enhance predictive analytics and remote monitoring capabilities. Mergers and acquisitions targeting regional software firms strengthen data intelligence and domain-specific expertise. Expanding service offerings particularly energy auditing, cybersecurity, and performance contracting allows firms to deliver end-to-end solutions. Localization of R&D and manufacturing ensures compliance with regional standards and reduces deployment costs. Digital twin and simulation technologies are being adopted to optimize industrial energy use. Furthermore, firms are leveraging green financing models and ESCO partnerships to lower entry barriers for SMEs. Training programs and certification initiatives are being rolled out to address workforce skill gaps. Cloud-native SaaS platforms are gaining traction, offering scalable, subscription-based access. Finally, participation in smart city and net-zero district projects positions companies as strategic enablers of urban energy transformation, ensuring long-term market relevance.

RECENT MARKET DEVELOPMENTS

- In June 2023, Schneider Electric launched its AI-powered Energy Advisor platform in Singapore, enhancing real-time energy optimization for commercial buildings and data centers across Southeast Asia.

- In September 2023, Honeywell partnered with Tokyo Electric Power Company to deploy demand response-enabled building energy management systems in over 500 commercial facilities across Japan.

- In November 2023, Siemens inaugurated a digital energy solutions hub in Bangalore, India, to accelerate cloud-based EMS development and support manufacturing clients across South and Southeast Asia.

- In February 2025, Honeywell acquired a majority stake in South Korea-based energy analytics startup Enervate, strengthening its AI-driven optimization capabilities for industrial clients in the region.

- In April 2025, Schneider Electric acquired Grid7, an Indian energy data analytics firm, to enhance its predictive modeling and grid integration services for renewable-heavy markets in the Asia Pacific.

MARKET SEGMENTATION

This research report on the Asia Pacific Energy Management System (EMS) Market is segmented and sub-segmented into the following categories.

By Type of Ems

- BEMS (Building EMS)

- IEMS (Industrial EMS)

- HEMS (Home EMS)

By End-User Industry

- Manufacturing

- Power and Energy

- IT and Telecommunication

- Healthcare

- Other End-user Industries

By Component

- Hardware

- Software

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the Asia Pacific Energy Management System (EMS) market?

The growth is driven by rapid urbanization, rising energy costs, government initiatives for energy efficiency, and increasing adoption of smart grid technologies across the region.

Which industries are adopting energy management systems the most in Asia Pacific?

Industries such as manufacturing, commercial buildings, IT & telecom, healthcare, and utilities are among the leading adopters of EMS solutions.

What are the major challenges faced by the Asia Pacific EMS market?

High initial investment costs, lack of skilled professionals, integration issues with legacy systems, and cybersecurity risks are some of the key challenges.

What is the future outlook for the Asia Pacific EMS market?

The market is expected to witness significant growth due to increasing renewable energy integration, advancements in IoT and AI-based EMS solutions, and strong demand for energy optimization in both industrial and commercial sectors.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com