Asia Pacific Enterprise Mobility Market Research Report – Segmented By Component (Mobile Device Management (MDM), Mobile Application Management (MAM)), Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2025 to 2033

Asia Pacific Enterprise Mobility Market Size

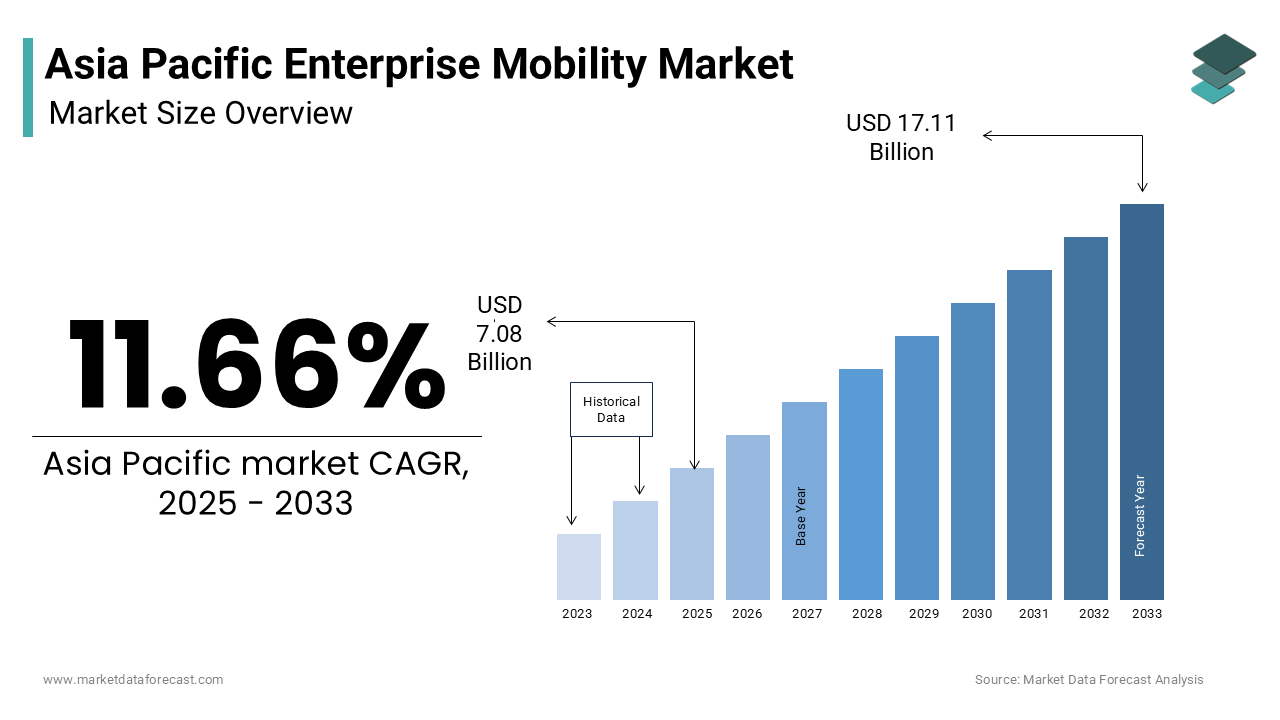

The Asia Pacific Enterprise Mobility Market was worth USD 6.34 billion in 2024. The Asia Pacific market is expected to reach USD 17.11 billion by 2033 from USD 7.08 billion in 2025, rising at a CAGR of 11.66% from 2025 to 2033.

The Asia Pacific enterprise mobility market refers to the deployment and management of mobile technologies, applications, and services within corporate environments to enhance productivity, streamline operations, and improve workforce engagement. Enterprises across sectors such as banking, healthcare, logistics, and government are increasingly adopting mobility solutions to support remote work models, field operations, and real-time decision-making. Moreover, initiatives such as Digital India, Smart Nation Singapore, and Industry 4.0 Japan have catalyzed the integration of mobility into both public and private sector workflows. Additionally, as reported by McKinsey, over 60% of enterprises in Southeast Asia have either implemented or are piloting mobile-first business applications to improve customer engagement and internal collaboration.

MARKET DRIVERS

Proliferation of Smartphones and Improved Network Infrastructure

One of the primary drivers fueling the growth of the Asia Pacific enterprise mobility market is the rapid proliferation of smartphones and the continuous enhancement of network infrastructure, especially with the rollout of 4G and 5G technologies. According to GSMA Intelligence, as of 2023, smartphone adoption in the Asia Pacific exceeded 75%, with countries like China, India, and Indonesia witnessing exponential growth in mobile internet usage.

This widespread smartphone availability enables enterprises to deploy mobile-first strategies for employee engagement, customer interaction, and operational efficiency. In India, for instance, the Department of Telecommunications reported that mobile broadband subscriptions surpassed 900 million in 2023, driven largely by low-cost data plans and improved rural connectivity.

In addition, telecom operators across the region are aggressively expanding 5G networks, allowing for faster and more reliable mobile access. South Korea, Japan, and Australia lead in this regard, with commercial 5G coverage now reaching over 80% of urban areas. As per Dell'Oro Group, these developments have enabled enterprises to adopt bandwidth-intensive mobility applications such as real-time video conferencing, AI-driven analytics, and IoT-based monitoring systems.

Rise of Remote Workforce and Field Operations Digitization

Another significant driver contributing to the growth of the Asia Pacific enterprise mobility market is the increasing reliance on remote and hybrid work models, along with the digitization of field operations. The post-pandemic shift towards flexible working arrangements has necessitated robust mobile infrastructures that support secure access to enterprise resources from diverse locations. This transition has spurred demand for enterprise-grade mobile applications, unified communications, and cloud-based collaboration tools. Additionally, industries such as logistics, utilities, and healthcare are aggressively digitizing field operations through mobile workforce management solutions. For example, in China, state-backed smart city projects have incorporated mobile dispatch systems for municipal services, enhancing service delivery efficiency.

MARKET RESTRAINTS

Data Security and Privacy Concerns Across Mobile Platforms

A key restraint affecting the growth of the Asia Pacific enterprise mobility market is the growing concern around data security and privacy risks associated with mobile device usage in corporate settings. As enterprises expand their use of smartphones, tablets, and personal devices for business functions, the potential for data breaches, unauthorized access, and malware attacks increases significantly. According to Kaspersky, the Asia Pacific accounted for over 30% of global mobile cyberattacks in 2023, with India and Indonesia experiencing sharp rises in phishing attempts and ransomware targeting enterprise endpoints. These threats have prompted companies to delay or scale back mobility deployments due to fears of regulatory non-compliance and reputational damage. Furthermore, varying national laws regarding data protection complicate cross-border enterprise mobility strategies. While countries like Australia and Singapore have stringent cybersecurity regulations, others such as Vietnam and Thailand are still in the process of formalizing comprehensive frameworks. As per PwC’s Asia Pulse Report, nearly half of the surveyed enterprises cited regulatory uncertainty as a major impediment to scaling their mobility programs.

High Deployment and Integration Costs for SMEs

Another significant challenge impeding the expansion of the Asia Pacific enterprise mobility market is the high cost of deploying and integrating mobility solutions for small and medium-sized enterprises (SMEs). While large corporations can afford sophisticated mobile device management (MDM), enterprise mobility management (EMM), and secure app development platforms, many SMEs struggle with budget constraints and a lack of technical expertise. According to the Asian Development Bank, nearly 60% of SMEs in Southeast Asia lack the financial capacity to invest in end-to-end enterprise mobility ecosystems. These costs include software licensing, device procurement, cloud hosting, and ongoing maintenance, making it difficult for smaller firms to justify expenditure, especially in emerging economies. In India, despite government incentives for digital transformation under the Digital India initiative, only 22% of SMEs have adopted mobile-first business applications due to affordability issues. Similarly, in the Philippines, where micro-enterprises dominate the economy, limited access to financing options further hinders mobility adoption.

MARKET OPPORTUNITIES

Expansion of AI-Powered Mobile Applications in Enterprises

One of the most promising opportunities emerging in the Asia Pacific enterprise mobility market is the rapid expansion of AI-powered mobile applications designed to enhance business intelligence, automate workflows, and improve user experience. Enterprises are increasingly leveraging artificial intelligence to personalize mobile interfaces, optimize resource allocation, and provide real-time insights through predictive analytics. According to ABI Research, AI-integrated mobile apps in enterprise settings across Asia Pacific grew by over 25% in 2023, driven by advancements in natural language processing and computer vision. Companies in China, South Korea, and Japan are at the forefront of deploying AI-driven chatbots, virtual assistants, and intelligent scheduling tools within mobile enterprise platforms. In healthcare, mobile AI applications are being used for diagnostics, patient engagement, and telehealth consultations, particularly in rural areas of India and Indonesia where access to medical professionals remains limited. Financial institutions in Australia and Singapore are also integrating AI-powered fraud detection mechanisms into mobile banking apps to enhance security and compliance.

Surge in Cloud-Based Enterprise Mobility Solutions Adoption

The increasing adoption of cloud-based enterprise mobility solutions represents a transformative opportunity for the Asia Pacific enterprise mobility market. Unlike traditional on-premises mobility infrastructure, cloud-native approaches offer greater scalability, flexibility, and cost-efficiency, making them ideal for contemporary enterprises aiming to support remote work, mobile workforce management, and real-time collaboration.

According to IDC, approximately 65% of enterprises in the Asia Pacific are expected to adopt cloud-managed mobility services by 2026, driven by digital transformation imperatives and the need for agile IT infrastructure. Public and hybrid cloud platforms are being widely deployed to facilitate mobile access to enterprise applications, data storage, and identity management without requiring heavy upfront capital investment. Small and medium-sized enterprises (SMEs) are also embracing Software-as-a-Service (SaaS)-based mobility tools due to their subscription-based pricing models. As per Synergy Research Group, Asia Pacific emerged as the fastest-growing region for cloud infrastructure services in Q3 2023, with year-over-year revenue growth exceeding 21%.

MARKET CHALLENGES

Talent Shortage and Lack of Skilled Mobility Professionals

A pressing challenge confronting the Asia Pacific enterprise mobility market is the acute shortage of skilled professionals capable of designing, deploying, and managing advanced mobile enterprise solutions. As enterprises embrace AI-driven mobility applications, zero-trust security frameworks, and cloud-native architectures, the demand for experienced mobility specialists has surged exponentially. However, educational institutions and training programs across much of the region have struggled to keep pace with evolving technological requirements. According to a 2023 report by Cisco’s Networking Academy, nearly 50% of IT decision-makers in the Asia Pacific identified a significant skills gap in their mobility teams, particularly concerning mobile app development, endpoint security, and enterprise mobility management (EMM). In countries like Vietnam and the Philippines, universities produce fewer than 10,000 certified mobility developers annually—far below industry demand. Furthermore, experienced mobility architects and consultants are increasingly migrating to developed markets such as Australia and Singapore, exacerbating talent shortages in less mature economies. As per Hays’ Asia Salary Guide, the average time to fill senior mobility roles in Malaysia and Thailand rose by 35% in 2023 compared to the previous year. This labor crunch not only delays project rollouts but also increases recruitment and training costs for enterprises. Unless addressed through industry-academia partnerships and upskilling initiatives, the talent deficit will continue to constrain the market’s growth potential.

Interoperability Issues Across Multi-Vendor Mobility Environments

Interoperability issues present a formidable challenge in the Asia Pacific enterprise mobility market, particularly as businesses deploy multi-vendor mobility equipment and software to meet diverse operational needs. Enterprises often combine products from vendors such as Microsoft, VMware, Samsung, and SAP, each offering proprietary hardware and software ecosystems that do not seamlessly integrate. This heterogeneity complicates device management, hampers automation implementation, and increases the risk of performance bottlenecks. As per a 2023 survey conducted by Enterprise Management Associates (EMA), 58% of enterprises in the Asia Pacific reported difficulties in managing multi-vendor mobility environments, citing compatibility concerns and inconsistent management interfaces as primary obstacles. In India, where enterprises frequently procure mobility gear from multiple suppliers to optimize costs, integration complexities have led to extended deployment cycles and higher operational expenditures. In addition, the absence of standardized APIs and open mobility protocols further intensifies interoperability concerns. For example, in Japan, despite strong domestic adoption of enterprise mobility solutions, many firms struggle to coordinate functionalities across legacy and next-gen systems. As per Omdia, the average enterprise in the region spends an additional USD 80,000 annually on third-party integration tools and consultancy services to mitigate these compatibility gaps.

SEGMENTAL ANALYSIS

By Component Insights

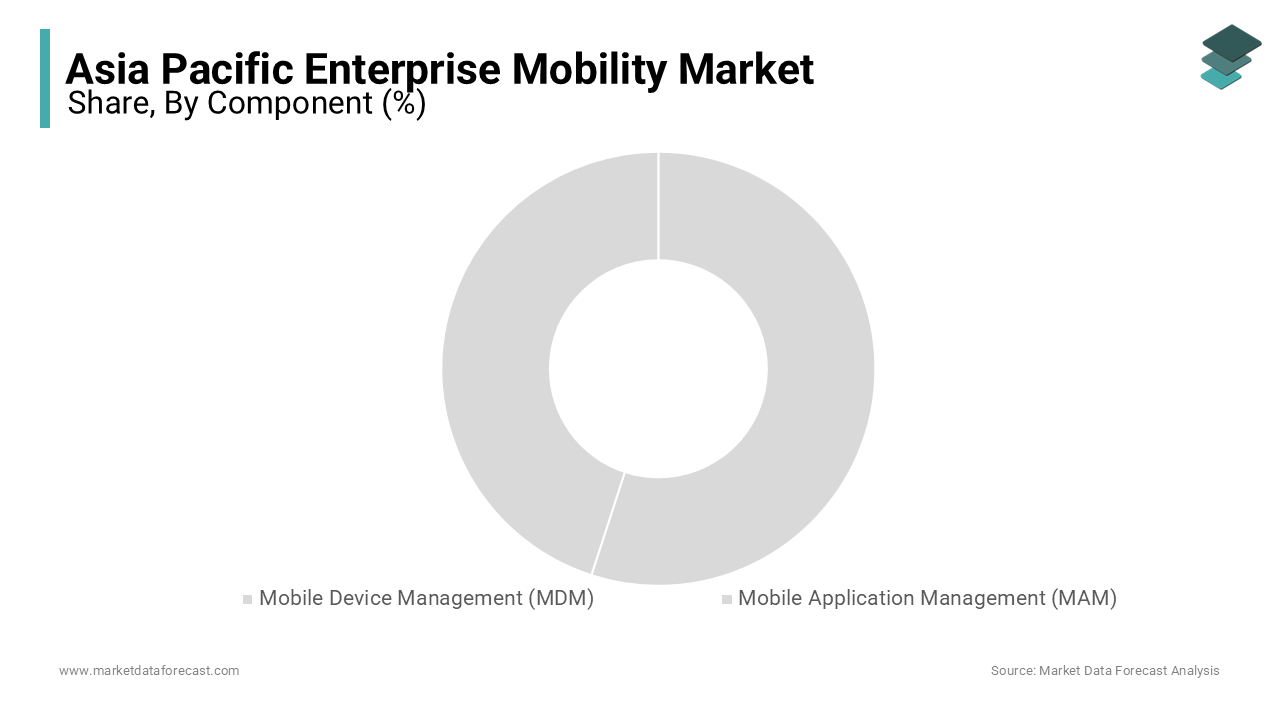

The Mobile Device Management (MDM) segment was the largest and held 54.5% of the Asia Pacific enterprise mobility market share in 2024 due to the increasing proliferation of mobile endpoints across enterprises and the heightened need for centralized control over device security, compliance, and lifecycle management.

A key driver is the widespread adoption of Bring Your Device (BYOD) policies in countries like India, Australia, and Singapore, where organizations are allowing employees to use personal devices for work purposes. Additionally, regulatory mandates in sectors such as finance, healthcare, and government require strict device monitoring and encryption protocols. In Japan, for instance, financial institutions must comply with stringent cybersecurity guidelines from the Financial Services Agency (FSA), compelling them to deploy advanced MDM frameworks.

The Mobile Application Management (MAM) segment is swiftly emerging with a CAGR of 19.3% from 2025 to 2033. One major catalyst is the shift toward application-centric security models, where enterprises focus on protecting sensitive corporate data at the app level instead of locking down entire devices. In South Korea, for example, financial services firms have increasingly adopted containerized MAM solutions that allow employees to securely access banking apps on personal devices without exposing company data. According to Samsung SDS, this approach has improved both employee satisfaction and operational efficiency. Moreover, the rise of cloud-native mobile applications and Software-as-a-Service (SaaS) platforms has intensified the need for real-time app management, policy enforcement, and remote updates that MAM tools excel at delivering. Frost & Sullivan estimates that SaaS-based enterprise app usage in Southeast Asia increased by 30% in 2023, directly influencing MAM adoption.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific enterprise mobility market with 28.4% of the share in 2024. The Chinese government has been instrumental in promoting enterprise mobility through national programs such as Made in China 2025 and Digital China. These initiatives encourage industries to adopt mobile-enabled automation, real-time data analytics, and intelligent logistics tracking systems. According to the Ministry of Industry and Information Technology (MIIT), more than 2,000 smart factories were deployed nationwide by mid-2023, all requiring enterprise-grade mobility infrastructure for field personnel and asset tracking. In addition, the presence of domestic tech giants such as Huawei, Tencent, and Alibaba has bolstered homegrown innovation in mobile enterprise platforms. Huawei alone reported that over 150,000 enterprises had deployed its MDM and MAM solutions in 2023.

India was positioned second by holding 15.4% of the Asia Pacific enterprise mobility market share in 2024, with a growing hub due to its large workforce, increasing smartphone penetration, and proactive government digitization efforts. The country is witnessing strong momentum in mobility adoption among SMEs and public sector organizations.

One of the primary drivers is the Digital India initiative, which has significantly expanded broadband connectivity and encouraged mobile-first business models across Tier 2 and Tier 3 cities. According to the Telecom Regulatory Authority of India (TRAI), enterprise internet subscriptions surged by 22% in FY 2023, with mobility being a core component of IT investment. Moreover, the rise of startup ecosystems and co-working spaces has intensified demand for flexible and secure mobility solutions. RedSeer Consulting reports that India’s SaaS industry alone saw $14 billion in funding in 2023, spurring corresponding demand for mobile application management and secure BYOD frameworks.

Japan was the top performer in the Asia Pacific enterprise mobility market with its mature digital ecosystem and deep integration of mobility in enterprise operations. According to Fujitsu’s 2023 Digital Transformation Outlook, over 70% of Japanese enterprises have incorporated some form of mobility into their IT infrastructure by ranging from mobile workforce management to secure communication apps.

A key contributing factor is Japan’s early adoption of advanced mobility solutions in manufacturing, logistics, and healthcare sectors. The Ministry of Economy, Trade and Industry (METI) reported that over 150 private 5G trials were underway in industrial settings in 2023, aimed at improving factory-floor mobility and reducing downtime.

Australian enterprise mobility market is likely to be driven by the progressive economy with a strong focus on cybersecurity, cloud integration, and workforce digitization. The Australian government’s Digital Economy Strategy 2030 has emphasized the importance of secure and resilient mobile connectivity, prompting widespread adoption of zero-trust mobility frameworks and cloud-managed MDM services. Additionally, the mining, healthcare, and education sectors have been investing heavily in high-capacity mobile workforce management tools and encrypted communication apps. Telstra and Optus have launched several enterprise-grade 5G private networks tailored for industrial use cases. Singapore's enterprise mobility market growth is growing lucratively with a regional innovation hub due to its advanced digital infrastructure and forward-looking policies. According to the Infocomm Media Development Authority (IMDA), Singapore recorded the highest enterprise broadband penetration rate in Southeast Asia in 2023, with 98% of businesses having access to gigabit-speed networks.

The Smart Nation initiative has driven heavy investment in enterprise mobility, particularly in AI-integrated mobile apps, IoT-linked field operations, and secure BYOD frameworks. In 2023, the Economic Development Board (EDB) reported that over 40 multinational tech firms established regional R&D centers in Singapore focused on next-gen mobility technologies.

Top Players in the Asia Pacific Enterprise Mobility Market

Samsung Electronics (South Korea)

Samsung plays a pivotal role in shaping enterprise mobility across the Asia Pacific through its Knox security platform, ruggedized devices, and integration with enterprise IT ecosystems. The company offers comprehensive mobile device management solutions tailored for industries such as healthcare, logistics, and manufacturing.

Samsung contributes to the global market by setting benchmarks in secure Android-based enterprise mobility, influencing how OEMs design hardware and software for business use. Its partnerships with leading MDM vendors and government agencies have helped standardize mobile security protocols across APAC countries, enhancing trust in mobile-first enterprise strategies.

Huawei Technologies (China)

Huawei is a key player in the Asia Pacific enterprise mobility market, offering customized mobility platforms that integrate seamlessly with its cloud and networking infrastructure. The company provides end-to-end enterprise mobility solutions including mobile device management, secure app containers, and enterprise-grade smartphones and tablets. Huawei's contribution to the global enterprise mobility landscape lies in its ability to offer cost-effective, scalable mobility ecosystems that cater to both large corporations and SMEs. With a strong regional presence and government-backed digital transformation initiatives, Huawei continues to drive the adoption of mobile-enabled smart workflows in the public and private sectors across China and Southeast Asia.

VMware (United States – Strong APAC Presence)

VMware maintains a dominant position in the Asia Pacific enterprise mobility market through its Workspace ONE platform, which combines mobile device and application management into a unified digital workspace solution. It enables enterprises to deploy secure, zero-trust mobility frameworks across distributed workforces.

Its global dominance in virtualization and cloud computing translates into a strong influence on enterprise mobility trends worldwide. In Asia Pacific, VMware collaborates extensively with local telecom operators, cloud providers, and system integrators to enhance deployment efficiency, making it a preferred platform for large-scale enterprise mobility rollouts across multiple industry verticals.

Top Strategies Used by Key Market Participants

Product Innovation and AI Integration

Leading players are continuously innovating their enterprise mobility offerings by incorporating artificial intelligence, automation, and advanced analytics. These enhancements help enterprises optimize workforce productivity, improve endpoint security, and deliver personalized mobile experiences that align with evolving business demands.

Strategic Partnerships and Ecosystem Development

To strengthen their foothold, key players are forming strategic alliances with telecom operators, cloud service providers, and managed services firms. These collaborations enable seamless integration of mobility solutions within broader enterprise IT infrastructures and accelerate time-to-market for new capabilities.

Expansion into Emerging Markets and Vertical-Specific Solutions

Market leaders are expanding their reach into high-growth economies across Southeast Asia and tailoring their mobility solutions for specific industry verticals such as healthcare, education, and logistics. This approach allows vendors to address unique regulatory, operational, and security requirements while capturing untapped demand in digitally transforming sectors.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

VMware, IBM Corporation, Microsoft Corporation, Citrix Systems, Cisco Systems, SAP SE, MobileIron (now part of Ivanti), BlackBerry Limited, SOTI Inc., Samsung SDS, Sophos Ltd., 42Gears Mobility Systems, ManageEngine (a division of Zoho Corporation), and Baramundi Software AG are some of the key market players.

The competitive environment in the Asia Pacific enterprise mobility market is characterized by a diverse mix of global technology leaders, regional telecom providers, and emerging software vendors striving to meet the evolving needs of enterprises. While established players leverage their global expertise and robust product portfolios to maintain dominance, smaller firms focus on niche functionalities and localized deployment models to carve out market share. The region’s vast digital transformation agenda has intensified competition, prompting vendors to differentiate themselves through enhanced security features, cloud-native architectures, and industry-specific mobility applications.

A key battleground is innovation speed, with companies racing to integrate AI-driven analytics, zero-trust security frameworks, and real-time data synchronization into mobility platforms. At the same time, pricing competitiveness remains crucial, especially in markets where small and medium-sized enterprises form a significant portion of potential customers. Regulatory diversity across countries further complicates market entry, requiring vendors to adapt their offerings to meet varying compliance standards.

Collaborations and acquisitions are also shaping the landscape, as vendors seek to expand their ecosystem reach and technological capabilities. As enterprises increasingly prioritize agility, scalability, and secure access across dispersed workforces, the competition will continue to intensify, driving rapid evolution in the Asia Pacific enterprise mobility sector.

RECENT MARKET DEVELOPMENTS

- In January 2024, Samsung launched an upgraded version of its Knox Platform for Enterprise, integrating AI-powered threat detection and adaptive authentication features designed to enhance mobile security for businesses operating in highly regulated industries across the Asia Pacific.

- In March 2024, Huawei expanded its enterprise mobility footprint in Southeast Asia by introducing a localized Mobile Device Management (MDM) suite tailored for SMEs in Thailand and Malaysia, aiming to simplify secure device provisioning and remote management for resource-constrained IT teams.

- In June 2024, VMware partnered with SoftBank to deploy its Workspace ONE platform across Japanese enterprises, enabling seamless integration with 5 G-enabled private networks and supporting next-generation mobile workforce strategies in manufacturing and logistics.

- In August 2024, Kyocera Corporation announced a collaboration with Microsoft Intune to develop ruggedized Android-based enterprise mobility solutions optimized for field workers in critical infrastructure sectors across Australia and New Zealand.

- In October 2024, Wipro integrated its AI-driven mobility analytics tool with leading MAM platforms in India, which is allowing enterprises to monitor mobile app usage patterns, detect anomalies, and enforce contextual security policies without compromising user experience.

MARKET SEGMENTATION

This research report on the Asia Pacific enterprise mobility market is segmented and sub-segmented into the following categories.

By Component

- Mobile Device Management (MDM)

- Mobile Application Management (MAM)

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the Asia Pacific enterprise mobility market?

The market is being driven by the widespread adoption of mobile devices, BYOD (Bring Your Own Device) policies, and the increasing need for secure remote access and workforce productivity tools.

What are the primary solutions offered in the enterprise mobility market?

Key solutions include Mobile Device Management (MDM), Mobile Application Management (MAM), Unified Endpoint Management (UEM), and mobile security platforms.

What challenges does the Asia Pacific enterprise mobility market face?

Key challenges include data security concerns, high initial investment costs, and the complexity of integrating mobility solutions with legacy systems.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com