Asia-Pacific Feed Phytogenics Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Ingredients, Animal Type, Application, And By Region (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2025 to 2033

Asia-Pacific Feed Phytogenics Market Size

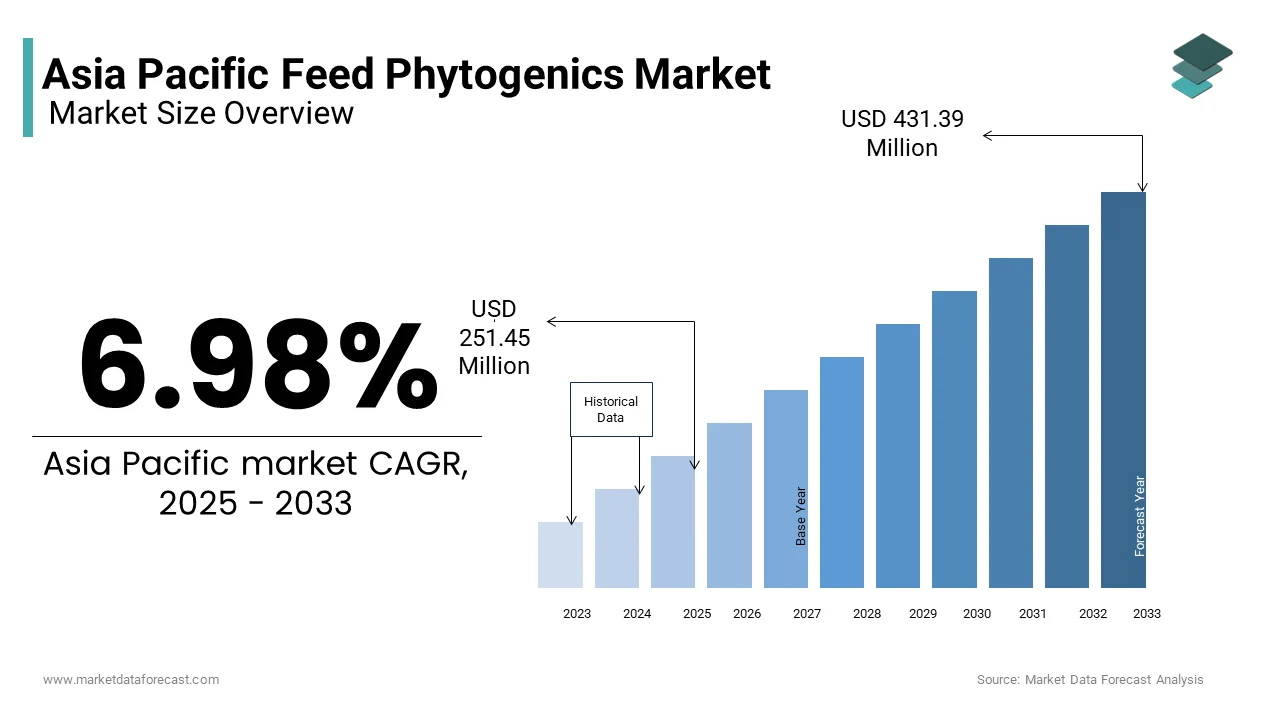

The Asia-Pacific feed phytogenics market was valued at USD 235.04 million in 2024 and is anticipated to reach USD 251.45 million in 2025 from USD 431.39 million by 2033, growing at a CAGR of 6.98%, from 2025 to 2033.

Feed phytogenics refer to plant-derived bioactive compounds used in animal feed formulations to enhance digestion, improve immunity, and promote overall livestock performance. These natural additives—extracted from herbs, spices, essential oils, and other botanical sources—are increasingly replacing synthetic growth promoters and antibiotics in the livestock industry. The Asia Pacific feed phytogenics market is witnessing growing traction due to shifting consumer preferences toward antibiotic-free meat and increasing regulatory scrutiny on livestock health practices.

According to the Food and Agriculture Organization (FAO), the region accounts for more than half of global livestock production, driven by strong demand from countries like China, India, and Thailand. With rising concerns over antimicrobial resistance and food safety, governments across the region are implementing policies to encourage the use of natural feed additives. In China, the Ministry of Agriculture and Rural Affairs launched a nationwide campaign in 2023 to phase out the routine use of in-feed antibiotics in poultry and swine farming.

Like, feed manufacturers in the country have begun integrating phytogenic blends into dairy cattle diets to enhance rumen efficiency without chemical additives.

MARKET DRIVERS

Regulatory Push Against Antibiotic Use in Livestock

The tightening regulatory environment around the use of antibiotics in animal feed is a key accelerator of the Asia Pacific feed phytogenics market. Governments and health organizations have raised alarms over the rise of antimicrobial resistance (AMR) linked to excessive antibiotic use in livestock, prompting policy reforms that favor natural alternatives such as phytogenics.

In China, the Ministry of Agriculture and Rural Affairs implemented a comprehensive ban on the use of medically important antibiotics in feed starting January 2023. This directive, known as the "No Antibiotics, High Yield" initiative, has led to a surge in demand for botanical feed additives.

Similarly, in India, the National Action Plan on Antimicrobial Resistance, updated in 2023, emphasized reducing antibiotic dependency in farm animals. As per the Indian Council of Agricultural Research, poultry producers adopting phytogenic blends experienced a 12% improvement in feed conversion ratios without compromising growth rates.

These regulatory shifts underscore a systemic transformation in livestock management, positioning feed phytogenics as a critical component of sustainable animal nutrition in the Asia Pacific.

Rising Consumer Demand for Organic and Natural Meat Products

Consumer awareness regarding food safety, animal welfare, and environmental sustainability has significantly influenced the adoption of feed phytogenics in the Asia Pacific. A growing segment of consumers prefers meat and dairy products derived from animals raised without synthetic additives or antibiotics, creating a ripple effect across the supply chain.

As per India's Food Safety and Standards Authority (FSSAI), organic meat exports grew by 19% in FY 2023–24, primarily driven by Middle Eastern and European markets requiring residue-free certification. This evolving consumer-driven landscape is reinforcing the momentum of the feed phytogenics market across the Asia Pacific.

MARKET RESTRAINT

Limited Awareness and Technical Knowledge Among Farmers

The lack of awareness and technical understanding among smallholder farmers is one of the primary constraints limiting market expansion in the Asia Pacific. Many livestock producers, particularly in rural parts of India, Indonesia, and the Philippines, continue to rely on traditional feeding practices and remain skeptical about the efficacy of plant-based additives.

Moreover, misinformation and inconsistent product labeling create confusion among end-users. As per the Asian Feed Industry Federation, a significant portion of surveyed farmers in Vietnam and Thailand believed that phytogenic feed additives were either too expensive or ineffective compared to conventional options. This knowledge gap hinders widespread adoption and limits the ability of manufacturers to penetrate lower-tier markets effectively.

To address this challenge, several governments and private sector players are launching farmer education initiatives. For instance, in China, the Ministry of Agriculture and Rural Affairs partnered with universities to conduct field demonstrations on phytogenic integration in swine diets.

High Cost and Supply Chain Challenges of Raw Materials

The elevated cost of raw materials and logistical complexities involved in sourcing high-quality botanical extracts pose a significant restraint to the Asia Pacific feed phytogenics market. Unlike synthetic additives, which are often mass-produced and standardized, phytogenic ingredients require specific climatic conditions, extensive processing, and stringent quality control measures, all of which contribute to higher production costs.

In India, as per the Spices Board of India, export prices of black pepper—a commonly used phytogenic ingredient—rose by 25% in 2023 due to erratic monsoon patterns affecting yield.

Moreover, the fragmented nature of herb and spice cultivation in the region complicates supply chain efficiency. In Indonesia, the Directorate General of Estate Crops found that only 20% of local spice growers followed Good Agricultural Practices (GAP), leading to inconsistencies in potency and contamination risks. This variability forces manufacturers to invest heavily in quality assurance and supplier audits.

Furthermore, transportation and storage requirements for sensitive plant extracts add to operational costs. These economic barriers are limiting their penetration in cost-sensitive markets across the Asia Pacific.

MARKET OPPORTUNITY

Expansion of Organic Livestock Farming and Certification Programs

The rapid expansion of organic livestock farming and the proliferation of certification programs that emphasize natural feed inputs is a significant opportunity for the Asia Pacific feed phytogenics market. Governments and agricultural bodies across the region are promoting organic farming models to reduce chemical dependence and ensure food safety, creating a favorable environment for phytogenic adoption.

Like, in India, the Paramparagat Krishi Vikas Yojana (PKVY) scheme encourages farmers to adopt organic practices, including the use of natural feed additives. As per the Ministry of Agriculture, over 1.2 million hectares were brought under organic farming in FY 2023–24, with poultry and dairy sectors showing particular interest in phytogenic supplementation.

In Australia, the Australian Certified Organic (ACO) program mandates the use of plant-based feed components in certified livestock operations. As per the Department of Agriculture, Fisheries and Forestry, organic meat exports grew by 20% in 2023, further reinforcing the need for compliant feed solutions. These developments indicate a clear pathway for sustained growth in the feed phytogenics market across the Asia Pacific.

Integration of Phytogenics in Precision Livestock Farming Technologies

The convergence of feed phytogenics with precision livestock farming technologies presents a transformative opportunity for the Asia Pacific market. As digitalization reshapes agriculture, smart feeding systems, data analytics, and automated monitoring tools are enabling more targeted and efficient use of feed additives, including plant-based solutions.

As per the ASEAN Smart Agriculture Forum, investments in agtech solutions in the region surged by 28% in 2023, signaling a shift toward data-driven, sustainable livestock production models. These advancements position feed phytogenics as a strategic element in the future of intelligent farming ecosystems across the Asia Pacific.

MARKET CHALLENGES

Standardization and Regulatory Divergence Across Countries

Lack of harmonized regulatory frameworks governing the approval, labeling, and usage of botanical feed additives is one of the foremost challenges confronting the Asia Pacific feed phytogenics market. Unlike in the European Union, where the European Food Safety Authority (EFSA) provides a centralized evaluation system, the Asia Pacific comprises diverse jurisdictions with varying levels of scientific validation and registration requirements.

India’s Feed Registration Committee under the Department of Animal Husbandry and Dairying has been working on draft regulations for phytogenic feed additives since 2022, but finalization has been delayed due to conflicting stakeholder opinions on efficacy testing protocols. Similarly, in Australia, the Australian Pesticides and Veterinary Medicines Authority (APVMA) treats certain phytogenic compounds as veterinary medicines rather than feed additives, subjecting them to more stringent compliance procedures.

These inconsistencies not only slow down product approvals but also complicate marketing strategies for multinational companies. As per the Asia-Pacific Economic Cooperation (APEC) Food Regulatory Forum, efforts to align feed additive standards across member economies are ongoing, but progress remains gradual.

Limited Scientific Validation and Efficacy Data

The scarcity of robust scientific validation and standardized efficacy data is a critical obstacle impeding the widespread acceptance of feed phytogenics in the Asia Pacific. While anecdotal evidence and preliminary studies suggest beneficial effects on digestion, immunity, and growth performance, the absence of large-scale clinical trials and peer-reviewed research limits confidence among regulators, feed formulators, and livestock producers. This disparity reflects a broader gap in investment in agritech R&D within the region, particularly in emerging markets such as Vietnam and Bangladesh.

In India, as per the Indian Council of Agricultural Research in 2023, while numerous indigenous plants possess potential phytogenic properties, very few had undergone systematic evaluation for inclusion in commercial feed applications.

Moreover, the complex interactions between different plant compounds and animal physiology make it challenging to establish universally applicable dosage recommendations. As per the Australian Centre for International Agricultural Research, even widely used extracts like garlic and cinnamon showed variable efficacy depending on species, diet composition, and rearing conditions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.98% |

| Segments Covered | By Ingredients, Animal Type, Application, Feedstock |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, etc |

| Market Leaders Profiled | Cargill Inc., DuPont, Biomin, Pancosma SA, and Delacon Biotechnik. |

SEGMENTAL ANALYSIS

By Ingredients Insights

Herbs and Spices

The herbs and spices segment represented the largest ingredient in the Asia Pacific feed phytogenics market by holding 43.2% of total share in 2024. The widespread use of herbs such as garlic, turmeric, ginger, and fenugreek in livestock diets to enhance digestion and immunity is one key driver of this segment. Similarly, in China, as per the Ministry of Agriculture and Rural Affairs, more than 45% of commercial swine feed formulations included herbal extracts to replace antibiotics post the national ban on in-feed antibiotic use in 2023. The dominance of herbs and spices segment is also attributed to the region’s long-standing agricultural heritage and abundant availability of indigenous medicinal plants that are traditionally used for their health-promoting properties.

The integration of traditional Ayurvedic and Chinese medicinal knowledge into modern animal nutrition is another contributing factor. In Thailand, the Department of Livestock Development has actively promoted lemongrass and holy basil in ruminant feed to improve rumen efficiency and reduce methane emissions.

Essential Oils

The essential oils segment is projected to register the highest CAGR of 11.3% during the forecast period, which is driven by growing scientific validation and targeted application in high-value livestock segments such as poultry and dairy cattle. Unlike herbs and spices, essential oils offer concentrated bioactive compounds that can be precisely dosed to achieve desired physiological effects.

The increasing incorporation of essential oils like thymol, carvacrol, and eugenol into precision feeding systems that optimize gut health and nutrient absorption is also a major growth catalyst. According to the Australian Centre for International Agricultural Research, controlled trials demonstrated a 15–20% improvement in feed conversion ratios when essential oil blends were administered to broiler chickens under heat stress conditions.

Besides, advancements in microencapsulation technology have enhanced the stability and bioavailability of essential oils in feed formulations. As per the Journal of Animal Physiology and Nutrition, studies conducted in Japan and South Korea revealed that encapsulated essential oils improved intestinal morphology and reduced pathogenic bacterial load in pigs without altering feed palatability.

By Application Insights

Feed Intake and Digestibility

The feed intake and digestibility segment accounted for the largest application with 52% share in the Asia Pacific feed phytogenics industry in 2024. The increasing need to optimize feed efficiency in response to rising feed costs and resource constraints is the key driver behind this growth of the segment. This segment's dominance is also due to the primary function of phytogenics in enhancing nutrient absorption, improving gut health, and boosting overall livestock productivity. According to the Food and Agriculture Organization (FAO), feed accounts for a significant portion of total livestock production costs in the Asia Pacific, making it critical to adopt additives that enhance utilization of nutrients. Phytogenic compounds such as saponins, flavonoids, and alkaloids have been shown to stimulate digestive enzymes and improve microbial balance in the gastrointestinal tract. In China, the Ministry of Agriculture and Rural Affairs mandated improvements in feed conversion ratios under its Green Feeding Program, prompting large-scale adoption of phytogenic premixes in poultry and swine operations.

Stress Reduction and Energy Effectiveness

The stress reduction and energy effectiveness segment is expected to grow at the fastest CAGR of 10.8% and is reflecting the evolving role of feed phytogenics beyond basic digestion support toward holistic animal wellness and performance optimization. The rising incidence of environmental and physiological stressors affecting livestock, particularly in tropical climates where heat stress significantly impacts productivity, is a key growth driver. According to the University of Melbourne’s School of Agriculture and Food, prolonged exposure to temperatures above 30°C reduces weight gain in broilers by up to 25%. To counteract this, phytogenic blends containing adaptogens like ashwagandha, ginseng, and licorice root are being increasingly adopted in poultry and dairy farming. Moreover, regulatory changes restricting the use of synthetic stimulants and beta-agonists have created an opening for natural alternatives that enhance energy metabolism without compromising animal welfare. Apart from these, the aquaculture sector is leveraging phytogenics for stress mitigation in high-density fish farming environments. As per the Southeast Asian Fisheries Development Center, shrimp farms in Vietnam and Thailand have started using ginger and garlic-based feed additives to reduce oxidative stress and enhance survival rates during disease outbreaks.

By Animal Insights

Poultry

The poultry segment was the commanding animal type with 39.4% share in the Asia Pacific feed phytogenics market in 2024. The rapid expansion of commercial poultry farming, coupled with stringent regulations against antibiotic use, has made this segment the most prominent consumer of botanical feed additives. The sheer scale of poultry production in the region, particularly in countries like China, India, and Thailand, is among the key drivers. According to the Food and Agriculture Organization (FAO), Asia Pacific accounted for over 65% of global chicken meat output in 2023, with China alone producing 15 million metric tons annually. Given the intensive nature of poultry farming, feed efficiency, disease prevention, and growth promotion are critical concerns, making phytogenics an attractive alternative to antibiotics. In India, the Indian Poultry Association noted that more than 60% of organized poultry farms had transitioned to phytogenic-based feed supplements following the implementation of the National Action Plan on Antimicrobial Resistance in 2023. Similarly, in Thailand, the Department of Livestock Development mandated reductions in antibiotic usage, prompting leading feed manufacturers like Betagro Group to reformulate their poultry feed with oregano and cinnamon extracts. Furthermore, the growing demand for organic and antibiotic-free poultry products has reinforced the adoption of phytogenics.

Aquaculture

The aquaculture segment is anticipated to exhibit the highest CAGR of 12.5% in the Asia Pacific feed phytogenics market. The intensification of fish and shrimp farming practices and increasing awareness of sustainable feed ingredients are driving the growth of the aquaculture segment. The rising prevalence of disease outbreaks in densely stocked aquaculture systems, which has prompted a shift toward natural immune boosters and antimicrobial agents, is also a major growth factor. In these environments, phytogenic compounds such as garlic extract, curcumin, and neem leaf powder are being used to enhance disease resistance and improve water quality tolerance. Besides, governments and export certification bodies are enforcing stricter residue limits on aquafeeds, pushing processors to eliminate synthetic additives. Technological advancements in feed delivery mechanisms are also accelerating adoption. In Japan, companies like Nippon Suisan Kaisha have developed microencapsulated phytogenic blends tailored for fishmeal replacement in carnivorous species.

COUNTRY-LEVEL ANALYSIS

China

China spearheaded the Asia Pacific feed phytogenics market by commanding 31.4% of total share in 2024. As the world’s top livestock producer, the country is undergoing a significant transformation in animal nutrition strategies due to tightening regulations on antibiotic use and a push toward sustainable agriculture. According to the Ministry of Agriculture and Rural Affairs, China implemented a nationwide ban on medically important antibiotics in animal feed starting January 2023. This policy, part of the broader "No Antibiotics, High Yield" initiative, has led to a surge in demand for natural feed additives, including phytogenics. As per the Chinese Feed Industry Association, over 50% of commercial feed mills had integrated phytogenic premixes into their formulations within a year of the regulation update. Moreover, the government’s Green Feeding Program encourages the use of plant-derived feed enhancers to improve gut health and feed efficiency. Leading domestic players such as New Hope Liuhe and COFCO Agri have partnered with international suppliers to develop customized phytogenic blends tailored for poultry, swine, and aquaculture applications.

India

India is another major player in the Asia Pacific feed phytogenics market. The country’s vast livestock population, rising consumer demand for organic meat, and proactive government policies are collectively driving the adoption of natural feed additives. Like, India is home to over 530 million livestock and poultry, making it one of the largest producers of eggs, milk, and buffalo meat globally. The National Action Plan on Antimicrobial Resistance, updated in 2023, mandates reductions in antibiotic use in farm animals, prompting feed manufacturers to incorporate phytogenic blends into their formulations.

As per the Indian Poultry Association, more than 60% of organized poultry farms had transitioned to phytogenic-based feed supplements by early 2024 to comply with new food safety norms. Moreover, the Paramparagat Krishi Vikas Yojana (PKVY) scheme encourages organic livestock farming, further reinforcing the use of plant-derived feed ingredients.

Japan

Japan is a mature region in the Asia Pacific feed phytogenics market, which is characterized by advanced agricultural practices, strict food safety standards, and a strong emphasis on animal welfare. The country’s focus on premium livestock products has positioned phytogenics as a core component of modern feed formulation strategies. Besides, Japanese researchers are at the forefront of evaluating phytogenic efficacy through clinical trials and academic collaborations. As per the National Institute of Livestock and Grassland Science, studies demonstrated that citrus peel extract and other botanicals improved thermoregulation and reduced stress markers in pigs and poultry. With leading retailers such as Itoham Yusoki Co. Ltd. and Maruha Nichiro promoting antibiotic-free meat lines, feed manufacturers are increasingly integrating phytogenic solutions. Companies like Ajinomoto and Kemin Industries have expanded their presence in Japan, leveraging scientific validation and digital livestock monitoring tools to enhance product adoption.

Australia

Australia contributes a significant share of the regional market and is driven by its strong commitment to organic farming, food traceability, and sustainable livestock production. The country’s rigorous feed safety regulations and growing consumer demand for clean-label meat products have accelerated the uptake of phytogenics. According to the Australian Pesticides and Veterinary Medicines Authority (APVMA), import restrictions on antibiotic-laced feed additives were tightened in 2023, prompting domestic producers to seek natural alternatives. As per the Australian Chicken Meat Federation, over 35% of broiler farms in Victoria and Queensland had incorporated phytogenic blends into their feed regimens to meet retailer sustainability targets. Leading brands such as Baiada and Ingham’s have publicly committed to sourcing only antibiotic-free poultry, directly influencing feed formulation trends.

Vietnam

Vietnam is emerging as a key player in the Asia Pacific feed phytogenics market. The country’s rapidly expanding livestock and aquaculture sectors, combined with increasing regulatory scrutiny on antibiotic use, are fueling demand for natural feed additives. According to the Department of Livestock Production, Vietnam issued a directive in 2023 urging feed manufacturers to phase out non-therapeutic antibiotics in poultry and swine feed. As a result, leading domestic firms such as CP Vietnam and ANOVA have begun incorporating phytogenic blends into their formulations to ensure compliance with export standards. The aquaculture industry, which accounts for a significant portion of Vietnam’s agricultural exports, is also adopting phytogenics to enhance disease resistance and improve water quality tolerance.

KEY MARKET PLAYERS

The major players in the market are fixated on broadening their distribution networks to cater to the wider market. The major companies dominating the Feed Phytogenics market in this region are Cargill Inc., DuPont, Biomin, Pancosma SA, and Delacon Biotechnik.

Top Players In The Market

One of the leading companies in the Asia Pacific feed phytogenics market is Delacon Biotechnik, an Austrian-based firm with a strong regional presence. The company specializes in plant-derived feed additives that enhance livestock performance through natural means. Delacon has built a reputation for scientific rigor, conducting extensive research on the efficacy of phytogenics in improving digestion, immunity, and stress resistance in animals. Its product portfolio includes blends derived from herbs, spices, and essential oils tailored to regional livestock needs.

Another key player is Pancosma S.A., a Swiss company known for its expertise in botanical extracts and functional feed ingredients. Pancosma focuses on developing sustainable solutions that support animal health without reliance on antibiotics. The company has expanded its footprint across Asia by collaborating with local feed manufacturers and adapting formulations to suit tropical climatic conditions and diverse livestock species.

Kemin Industries is also a dominant force in the market, offering a wide range of phytogenic feed additives designed to improve gut health and overall productivity. With a strong R&D foundation, Kemin integrates advanced formulation technologies into its products, ensuring high bioavailability and effectiveness. The company actively engages in farmer education programs and collaborates with academic institutions to validate the benefits of phytogenics, strengthening its influence in the Asia Pacific region.

Top Strategies Used By Key Market Participants

One of the primary strategies employed by leading players in the Asia Pacific feed phytogenics market is localized product development and customization. Companies are tailoring their formulations to match regional livestock breeds, dietary habits, and climate conditions, ensuring greater efficacy and acceptance among farmers and feed producers.

Another crucial approach is strategic partnerships with regional distributors and agricultural cooperatives. By forming alliances with local stakeholders, global manufacturers can navigate regulatory landscapes more efficiently and ensure widespread availability of their products across both commercial and smallholder farming segments.

Lastly, investment in research and knowledge dissemination is gaining momentum. Companies are collaborating with universities and research institutions to conduct clinical trials and publish findings that validate the benefits of phytogenics. This not only enhances credibility but also supports policy advocacy and consumer awareness, reinforcing long-term market positioning.

COMPETITION OVERVIEW

The Asia Pacific feed phytogenics market is characterized by a dynamic and evolving competitive environment, where both global and regional players coexist and vie for dominance. As the demand for antibiotic-free livestock production grows, companies are intensifying their focus on innovation, sustainability, and market accessibility. While multinational corporations bring technological expertise and established brand recognition, domestic firms leverage local insights and cost advantages to capture niche markets. The industry is witnessing increased collaboration between feed additive manufacturers, livestock producers, and government bodies to align with evolving food safety regulations. Apart from these, there is a growing emphasis on scientific validation and product differentiation based on efficacy, dosage precision, and application-specific formulations. Distribution networks are expanding through strategic alliances and localized supply chains to reach both large-scale agribusinesses and rural farming communities. Furthermore, digital integration in livestock management is influencing how feed additives are marketed and applied, pushing companies to incorporate data-driven solutions into their offerings. Overall, competition is shifting from mere product availability to value-added services, technical support, and regulatory compliance, shaping a more sophisticated and performance-oriented market landscape.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Delacon Biotechnik launched a new line of climate-adapted phytogenic blends specifically formulated for poultry in tropical environments, targeting major markets such as Thailand and Indonesia.

- In June 2024, Pancosma expanded its regional presence by establishing a dedicated technical service center in Vietnam, aimed at supporting feed mills with formulation guidance and on-site consultation for phytogenic integration.

- In August 2024, Kemin Industries introduced a proprietary microencapsulation technology in Japan to enhance the stability and efficacy of essential oil-based feed additives, particularly for swine and aquaculture applications.

- In October 2024, Nutriad formed a strategic alliance with a leading Indian livestock nutrition company to strengthen distribution channels and increase access to smallholder farmers across South Asia.

- In December 2024, DSM Animal Nutrition partnered with a Singapore-based agritech startup to develop AI-powered feeding recommendations that optimize phytogenic usage based on real-time animal health metrics.

MARKET SEGMENTATION

This research report on the Asia Pacific phytogenics market is segmented and sub-segmented into the following categories.

By Ingredients

- Essential oils

- Oleoresins

- Herbs and Species

- Others

By Animal Type

- Poultry

- Aquaculture

- Swine

- Ruminant

- Others

By Application

- Flavouring and Aroma

- Organic Trace minerals

- Anti-Parasitic

- Feed Intake

- Digestibility

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What are feed phytogenics?

Feed phytogenics are plant-derived natural compounds—such as essential oils, herbs, spices, and extracts—used in animal feed to improve digestion, boost immunity, and support growth. They are increasingly adopted as alternatives to antibiotic growth promoters in livestock and poultry farming.

Why is the Asia Pacific region seeing growth in feed phytogenics?

Rising awareness of animal health, stricter regulations on antibiotic use, and growing demand for safe meat and dairy products are driving interest in natural feed additives. Countries like India, China, Thailand, and Vietnam are leading the shift due to expanding commercial farming and export-focused animal production.

How do phytogenics benefit livestock and poultry?

They enhance nutrient absorption, reduce gut inflammation, and help maintain a balanced intestinal microbiome, leading to better feed efficiency and weight gain. Their antimicrobial and antioxidant properties also support overall animal resilience and performance.

Are phytogenics replacing antibiotics in animal feed?

While not a complete replacement, they are playing a major role in reducing reliance on antibiotics, especially in countries phasing out growth promoters. Farmers are combining phytogenics with probiotics and organic acids to maintain animal health without overusing drugs.

What types of animals are fed phytogenic additives?

Poultry, swine, and aquaculture species are the primary users due to high-intensity farming and sensitivity to gut health issues. Dairy and beef cattle are also increasingly receiving phytogenic supplements to improve digestion and milk or meat quality.

What challenges exist in adopting phytogenics across the region?

Variability in raw material quality, inconsistent potency, and lack of standardized dosing can affect performance and farmer confidence. Additionally, higher costs compared to synthetic additives make adoption slower among small-scale producers.

How are governments influencing the phytogenics market?

Some countries are tightening rules on antibiotic residues in food, indirectly promoting the use of natural alternatives like phytogenics. While direct regulations on phytogenics are still limited, food safety standards are encouraging safer, residue-free animal production.

Who are the main suppliers of phytogenic feed additives in Asia Pacific?

Global feed additive companies operate in the region, but local manufacturers and regional agri-tech firms are gaining ground by offering cost-effective, locally adapted formulations. Partnerships with research institutes are helping improve product consistency and efficacy.

What trends are shaping the future of this market?

There’s growing interest in combining different phytogenic compounds for synergistic effects and using encapsulation technology to improve stability and release in the gut. Digital farming tools are also helping farmers track performance and justify the investment in premium feed additives.

How is consumer demand affecting the phytogenics industry?

Consumers are increasingly seeking meat and dairy products labeled as “antibiotic-free” or “naturally raised,” pushing producers to adopt cleaner farming practices. This shift in preference is creating a strong downstream pull for phytogenic solutions across the supply chain.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com