Asia Pacific Fertility Test Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Product (Ovulation Predictor Kits, Fertility Monitors (Urine, Saliva, Blood)), Mode of Purchase, Application, End-User, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Market Size, 2025

$133 MnMarket Estimate, 2026

$143 MnMarket Forecast, 2034

$258 MnCAGR, 2026–2034

7.62%Asia Pacific Fertility Test Market Size

Asia Pacific Fertility Test market size was valued at USD 133.25 million in 2025, and is expected to reach USD 258.04 million by 2034 from USD 143.40 million in 2026. The market's promising CAGR for the predicted period is 7.62%.

The Asia Pacific fertility tests range from over-the-counter (OTC) home fertility kits to advanced clinical diagnostics performed in laboratories and fertility clinics. The primary objective of fertility testing is to evaluate hormonal levels, ovarian reserve, sperm count, and other biological indicators that influence conception potential. As awareness around infertility issues increases across the region, so does the demand for early diagnosis and intervention.

According to the World Health Organization, infertility affects approximately 15% of couples globally, with rising prevalence observed in urban centers across China, India, Japan, and Australia. Moreover, changing lifestyle factors such as delayed childbearing, increased stress levels, obesity, and environmental pollutants are contributing to declining fertility rates. Governments and private healthcare providers are responding by expanding access to reproductive health services, including fertility assessments, which is further propelling market growth.

MARKET DRIVERS

Rising Incidence of Infertility and Delayed Parenthood

One of the most significant drivers of the Asia Pacific fertility test market is the increasing incidence of infertility among couples, coupled with the trend of delayed parenthood. In recent years, there has been a noticeable shift in family planning patterns, with more individuals choosing to have children later in life due to career priorities, financial stability, and evolving social norms. According to the International Federation of Fertility Societies, infertility rates in major metropolitan areas of China and India have increased by nearly 20% over the past decade. Individuals are increasingly seeking early diagnosis through fertility tests to understand their reproductive status with greater public awareness and media attention on reproductive health. This growing health consciousness, combined with an aging population is significantly boosting the adoption of fertility tests across the Asia Pacific region.

Technological Advancements and Availability of Home-Based Testing Kits

Another key driver fueling the growth of the Asia Pacific fertility test market is the rapid advancement in diagnostic technologies and the increasing availability of user-friendly home-based fertility testing kits. Unlike traditional laboratory assessments, these kits offer convenience, privacy, and faster results, which is encouraging more individuals to proactively monitor their reproductive health. Companies such as Modern Fertility and LetsGetChecked have expanded into markets like Singapore and Australia, offering hormone-level assessments via simple blood or urine samples. In India, startups like Cloudnine and Indira IVF have introduced affordable at-home fertility test packages tailored for local consumers. Additionally, technological improvements in digital health platforms have enabled real-time tracking and interpretation of fertility markers. As per the Asia Pacific Digital Health Association, fertility apps integrated with test results are gaining popularity, especially among tech-savvy millennials who prefer personalized health insights.

MARKET RESTRAINTS

Cultural Stigma and Lack of Awareness in Rural Areas

A major restraint affecting the widespread adoption of fertility tests in the Asia Pacific region is the persistent cultural stigma surrounding infertility and the lack of awareness, particularly in rural and semi-urban communities. In many parts of India, Indonesia, the Philippines, and Vietnam, infertility remains a deeply sensitive issue, often linked to social shame and familial pressure, discouraging open discussion and proactive health-seeking behavior. Moreover, in countries like Thailand and Malaysia, misconceptions about fertility such as attributing conception difficulties solely to female factors persist are leading to underutilization of male fertility tests. Without targeted educational initiatives and community outreach programs, these cultural barriers will continue to hinder the expansion of the fertility test market across large segments of the Asia Pacific population.

High Cost of Advanced Diagnostic Tests and Limited Insurance Coverage

Another critical barrier to the growth of the Asia Pacific fertility test market is the high cost associated with advanced diagnostic procedures and the limited extent of insurance coverage for fertility-related assessments. While basic hormone tests and ovulation prediction kits are relatively affordable, more sophisticated evaluations such as AMH (Anti-Müllerian Hormone) testing, semen analysis, and genetic screenings can be prohibitively expensive for a significant portion of the population. According to Deloitte’s 2023 healthcare report, out-of-pocket expenses account for more than 70% of fertility-related healthcare costs in India, where public health insurance schemes rarely cover diagnostic fertility testing. Even in developed economies like Australia, where some level of insurance support exists, private fertility clinic fees remain high, deterring routine testing.

MARKET OPPORTUNITIES

Expansion of Telehealth and Online Fertility Platforms

The rapid expansion of telehealth services and online fertility platforms presents a substantial opportunity for the Asia Pacific fertility test market. With the increasing penetration of smartphones and internet connectivity, consumers are now able to access fertility education, virtual consultations, and home-based testing solutions without visiting clinics in remote and underserved regions.

According to the Asia Pacific Telehealth Alliance, the number of digital health startups offering fertility tracking and testing services in Southeast Asia has doubled since 2021. In India, companies like Fitterfly and Ela Women's Health have introduced mobile applications that guide users through self-testing processes and connect them with certified specialists for result interpretation.

In China, where e-commerce and digital health are highly developed, platforms such as JD Health and Ping An Good Doctor have integrated fertility assessments into their telemedicine offerings, enabling millions of users to order test kits online and receive expert guidance remotely.

Growing Demand for Male Fertility Testing

The increasing recognition of male infertility as a significant contributor to couple infertility presents a promising opportunity for the Asia Pacific fertility test market. Traditionally, fertility discussions have predominantly focused on women, but recent shifts in awareness and medical understanding have led to a surge in demand for male-specific fertility assessments.

According to the Asian Journal of Andrology, male infertility accounts for nearly 50% of all infertility cases in the region, yet it remains underdiagnosed due to lower participation in routine fertility screening. In Japan, the Japanese Society of Andrology has launched awareness campaigns emphasizing the importance of sperm quality testing, which is resulting in a notable increase in male engagement in fertility assessments.

MARKET CHALLENGES

Regulatory Heterogeneity Across Countries

One of the most pressing challenges facing the Asia Pacific fertility test market is the presence of diverse and inconsistent regulatory frameworks across different countries. According to a 2023 report by the Asia-Pacific Economic Cooperation (APEC) Health Forum, the time required to obtain regulatory clearance for fertility diagnostics varies significantly, which is ranging from 12 months in Australia to over 24 months in certain ASEAN nations. Additionally, differences in labeling, data submission protocols, and device classification create complexities for companies attempting to scale their offerings across multiple markets.

Limited Access to Specialized Fertility Clinics in Rural Areas

Limited access to specialized fertility clinics in rural and semi-urban areas poses a significant challenge to the expansion of the Asia Pacific fertility test market. A large proportion of the population in countries like India, Indonesia, and the Philippines lacks proximity to well-equipped diagnostic centers or reproductive health specialists. According to the Indian Council of Medical Research, less than 15% of fertility clinics in India are located outside major metropolitan areas, leaving vast rural populations underserved. As per the World Health Organization, improving access to reproductive health services in low-resource settings remains a priority, but progress has been slow due to infrastructural limitations and workforce shortages.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.62% |

| Segments Covered | By Product, Mode of Purchase, Application, End-User, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Prestige Consumer Healthcare Inc., Procter & Gamble, Geratherm Medical AG, Abbott, Church & Dwight Co., Inc., Fairhaven Health, Babystart, bioZhena Corporation, and Fertility Focus Limited, and others |

SEGMENTAL ANALYSIS

By Product Insights

The ovulation predictor kits (OPKs) segment was accounted in holding prominent share of the holds Asia Pacific fertility test market in 2025. According to Frost & Sullivan, over 75% of home-based fertility testing in the region involves OPKs due to their affordability, ease of use, and availability without a prescription.

The fertility monitors segment is esteemed to register a CAGR of 14.2% in the next coming years owing to the technological advancements that offer greater accuracy compared to traditional dipstick tests, making them particularly appealing to tech-savvy consumers. In South Korea, where digital health adoption is high, companies like Ava Health and Lady-Comp have launched localized versions of their fertility trackers, integrating AI-driven insights to enhance cycle prediction capabilities.

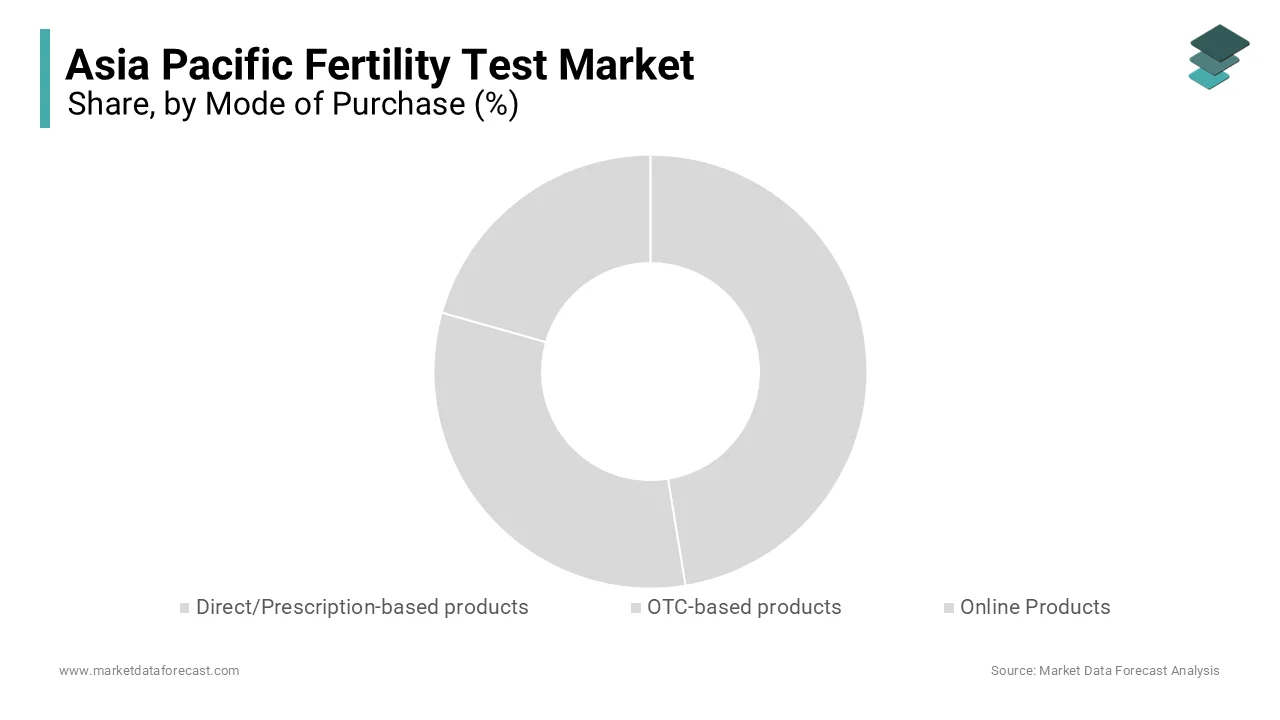

By Mode of Purchase Insights

The over the counter (OTC) was accounted in holding 54.3% of the Asia Pacific fertility test market share in 2025. According to Deloitte’s 2023 healthcare report, nearly 80% of fertility test users in India and Indonesia prefer purchasing ovulation kits directly from pharmacies or retail stores, citing privacy concerns and immediate availability as key reasons. In Australia, where public health initiatives promote preventive care, the Therapeutic Goods Administration has approved several OTC fertility tests, encouraging broader adoption.

The online segment is likely to grow with a CAGR of 16.8% throughout the forecast period. According to Frost & Sullivan, online sales of fertility tests in the Asia Pacific region grew by over 40% in 2023, with platforms like Amazon, Flipkart, and JD Health expanding their range of fertility-related products. In Singapore, where digital health adoption is highly developed, government-backed initiatives like Smart Nation Healthcare have facilitated seamless access to fertility diagnostics via online portals.

By Application Insights

The female fertility test segment was the largest by occupying dominant share of the Asia Pacific fertility test market due to the higher awareness and social acceptance surrounding female reproductive health, along with the wider availability of hormone-based diagnostic kits targeting ovulation and ovarian reserve assessment.

According to the Asian Journal of Medical Sciences, nearly 90% of fertility clinics in India recommend hormone-level testing, including AMH (Anti-Müllerian Hormone) and LH (luteinizing hormone), as part of initial infertility evaluations. Female fertility tests remain the most widely adopted category in the Asia Pacific fertility test market.

The male fertility testing segment is likely to grow with a CAGR of 13.4% during the forecast period owing to the increasing recognition of male factor infertility as a critical component in couple infertility cases and the development of non-invasive, easy-to-use sperm analysis tools. According to the Asian Journal of Andrology, male infertility now accounts for nearly 50% of all infertility cases in the region, yet it remains underdiagnosed due to lower participation in routine fertility screening.

By End-User Insights

The home care setting segment was the largest with 58.6% of the Asia Pacific fertility test market share in 2025. According to Frost & Sullivan, over 70% of fertility test purchases in India and Indonesia occur outside clinical settings, with couples opting for home-based ovulation kits and hormone level tests. The home care segment continues to dominate fertility test consumption across the Asia Pacific with ongoing product innovation and greater digital health integration.

The fertility clinics segment is projected to expand at a CAGR of 12.6% throughout the forecast period with the increasing number of specialized fertility centers offering comprehensive diagnostic services as part of assisted reproductive technology (ART) treatment protocols. In South Korea, where ART procedures are highly regulated and technologically advanced, institutions such as Seoul National University Hospital and CHA Medical Group have integrated sophisticated fertility testing workflows, attracting both domestic and international patients.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific fertility test market with 25.3% of share in 2025. According to the National Health Commission of China, infertility affects nearly 12% of married couples, prompting increased demand for early diagnosis and intervention. In response, digital health platforms such as JD Health and Ping An Good Doctor have expanded fertility test offerings, integrating teleconsultations and AI-powered cycle tracking to improve user experience.

India was positioned second in leading the Asia Pacific fertility test market with 19.8% of share with the escalating infertility rates, increasing healthcare expenditure, and expanding access to affordable diagnostic tools. The country has witnessed a notable rise in lifestyle-induced fertility issues, which is prompting a surge in demand for early detection methods.

According to the Indian Society for Assisted Reproduction, one in six Indian couples experiences infertility, with hormonal imbalances and stress-related conditions being primary contributors.

Japan fertility test market growth is likely to be driven by the advanced healthcare system, high-tech medical devices, and strong emphasis on reproductive health research. The country has one of the highest rates of fertility treatment utilization globally, largely due to demographic trends and declining birth rates.

According to the Japan Society of Obstetrics and Gynecology, more than 1.5 million fertility assessments were conducted in 2023, with hormone-based tests and digital fertility monitors witnessing significant adoption.

South Korea fertility test market is likely to grow with an emerging powerhouse in reproductive diagnostics. The country’s growth is primarily driven by rising infertility rates, progressive healthcare policies, and strong government backing for reproductive medicine.

Australia fertility test market growth is gearing up with the presence of well-developed healthcare system, high patient awareness, and strong regulatory environment. The country maintains some of the highest clinical standards in the region by ensuring safe and reliable fertility testing options for consumers.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific fertility test market is intensifying as global diagnostics giants and regional startups vie for market share in a rapidly expanding sector. Established multinational corporations dominate due to their technological expertise, regulatory experience, and established supply chains, offering high-precision fertility tests used in laboratories and fertility clinics. At the same time, local players are gaining traction by introducing affordable, user-friendly, and digitally connected fertility testing solutions tailored to the specific needs of Asian consumers. The growing influence of e-commerce and direct-to-consumer sales models has further diversified the competitive landscape, allowing new entrants to reach wider audiences without relying heavily on traditional distribution networks. Additionally, increasing collaboration between technology firms and medical device manufacturers is driving innovation in digital fertility tracking, making the market more dynamic and fragmented.

KEY MARKET PLAYERS

Prestige Consumer Healthcare Inc., Procter & Gamble, Geratherm Medical AG, Abbott, Church & Dwight Co., Inc., Fairhaven Health, Babystart, bioZhena Corporation, and Fertility Focus Limited are the key players in the Asia Pacific fertility test market.

TOP PLAYERS IN THE MARKET

- Roche is a global leader in diagnostics and plays a significant role in the Asia Pacific fertility test market through its advanced hormone testing solutions and automated immunoassay systems. The company offers highly accurate fertility-related diagnostic tests used in laboratories and fertility clinics across Japan, Australia, and China. Roche’s commitment to innovation ensures that its fertility assays meet the highest clinical standards by supporting early detection of hormonal imbalances and reproductive health issues.

- Abbott is a major player in the fertility diagnostics space, offering a broad range of hormone-based tests used for assessing ovarian reserve and male fertility factors. In the Asia Pacific region, Abbott provides both point-of-care and centralized laboratory fertility testing solutions, enabling efficient patient management in hospitals and clinics. The company's strong distribution network and focus on affordability help expand access to fertility diagnostics in emerging markets such as India and Southeast Asia.

- Quidel, now integrated into Ortho Clinical Diagnostics, is well-known for its over-the-counter fertility test kits, including ovulation predictor kits widely available in pharmacies and online platforms across the Asia Pacific. These products are designed for ease of use and reliability, making them popular among women seeking to track their fertility cycles at home. The company contributes to raising awareness about reproductive health by providing accessible and cost-effective fertility monitoring tools tailored for diverse consumer needs.

TOP STRATEGIES USED BY KEY PLAYERS

One of the primary strategies employed by leading players in the Asia Pacific fertility test market is product innovation and digital integration , where companies develop smart, AI-enabled fertility monitors and mobile-connected test kits to enhance user engagement and accuracy. Another crucial approach is strategic partnerships and collaborations , wherein manufacturers work closely with healthcare providers, telemedicine platforms, and fertility clinics to improve product adoption and service delivery.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, Roche launched a new line of automated fertility hormone assays in Japan aimed at improving diagnostic accuracy and reducing turnaround time for fertility assessments in hospital laboratories.

- In September 2023, Abbott expanded its partnership with a leading Indian e-pharmacy platform to increase the availability of its branded ovulation predictor kits and male fertility test strips in Tier I and Tier II cities.

- In April 2025, Quidel introduced a localized version of its digital fertility monitor in South Korea, integrating AI-based cycle prediction features and compatibility with local health apps to enhance consumer engagement.

- In November 2023, Danaher Corporation acquired a minority stake in an Australian fertility diagnostics startup to gain access to next-generation biomarker testing technologies for early fertility screening applications.

- In May 2025, Mindray Medical entered the fertility diagnostics segment by launching a suite of reproductive hormone test kits in China, leveraging its existing presence in clinical labs to drive rapid adoption.

MARKET SEGMENTATION

This research report on the Asia Pacific Fertility Test market has been segmented and sub-segmented based on the following categories.

By Application

- Female Fertility Products

- Male Fertility Products

By Mode of Purchase

- Direct/Prescription-based products

- OTC-based products

- Online Products

By Product

- Ovulation Prediction Kits

- Fertility Monitors

- Male Fertility Testing Products

By End-User

- Home Care Settings

- Hospitals and Fertility Clinics

- Other End Users

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is the Asia Pacific fertility test market?

The Asia Pacific fertility test market comprises diagnostic products and services used to assess male and female fertility, including ovulation tests, sperm analysis kits, hormone testing, and fertility monitoring devices.

2. What factors are driving the growth of the Asia Pacific fertility test market?

The market is driven by rising infertility rates, increasing awareness of reproductive health, delayed pregnancies, growing adoption of home-based testing kits, and advancements in fertility diagnostics.

3. Which countries lead the Asia Pacific fertility test market?

China, Japan, India, South Korea, and Australia are the leading markets due to their large populations, improving healthcare infrastructure, and growing demand for fertility care.

4. What are the major types of fertility tests available in the market?

The market includes ovulation prediction kits, pregnancy-related fertility tests, hormone testing, sperm analysis tests, ovarian reserve tests, and digital fertility monitoring devices.

5. Who are the primary end users of fertility tests?

Hospitals, fertility clinics, diagnostic laboratories, home healthcare users, and research institutions are the primary end users.

6. Why are fertility tests important?

Fertility tests help identify reproductive health issues, determine the most fertile period for conception, support early diagnosis of infertility, and guide appropriate treatment decisions.

7. What challenges does the Asia Pacific fertility test market face?

Challenges include high diagnostic costs, limited awareness in rural areas, social stigma surrounding infertility, and unequal access to specialized fertility services.

8. How is the trend toward home-based testing influencing the fertility test market?

The increasing availability of easy-to-use and accurate home fertility test kits is improving convenience, privacy, and early fertility monitoring for consumers.

9. How are technological advancements shaping the fertility test market?

Innovations such as digital fertility monitors, smartphone-connected devices, AI-powered fertility tracking, and advanced biomarker testing are improving diagnostic accuracy and user experience.

10. What is the future outlook for the Asia Pacific fertility test market?

The market is expected to experience strong growth during the forecast period, supported by rising infertility prevalence, increasing healthcare expenditure, continuous technological advancements, and greater awareness of reproductive health across the Asia Pacific region.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com