Asia Pacific Flexographic Printing Inks Market Research Report – Segmented By Type ( Water-Based Inks, UV-Cured Inks ) Resin Type and Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis( 2026 to 2034).

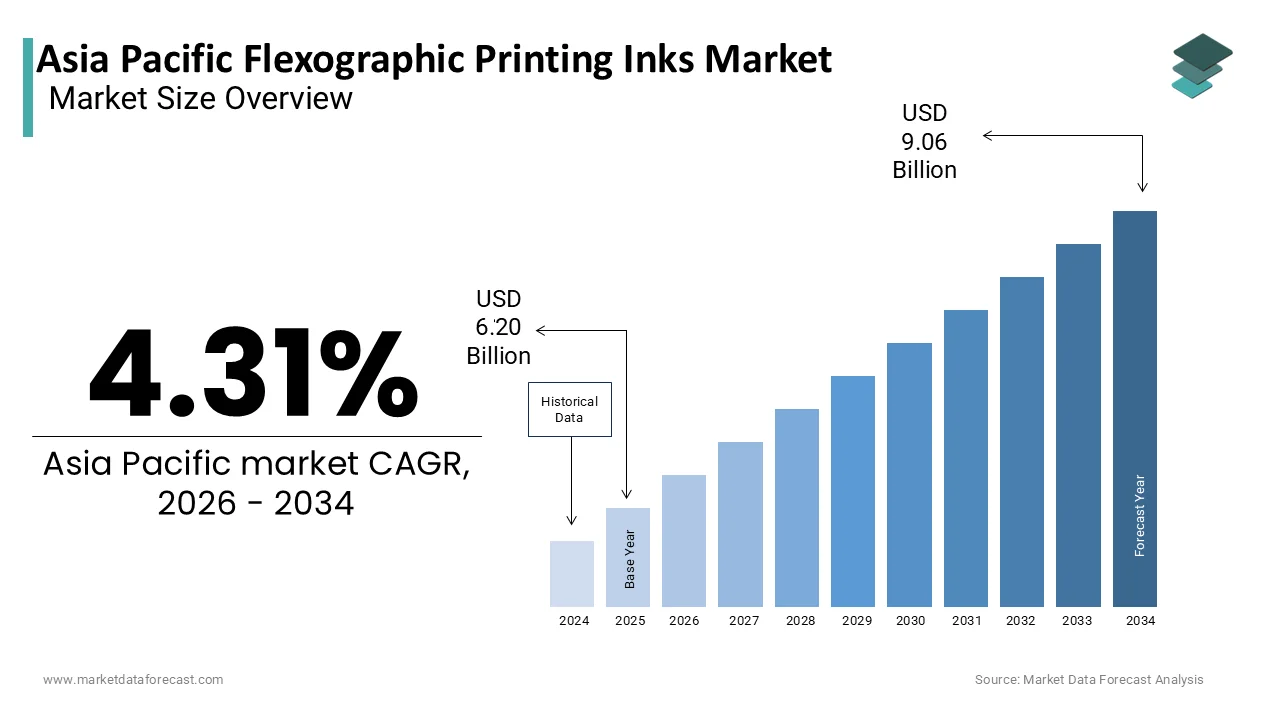

Market Size, 2025

$6.20 BnMarket Estimate, 2026

$6.46 BnMarket Forecast, 2034

$9.06 BnCAGR, 2026–2034

4.31%Asia Pacific Flexographic Printing Inks Market Size

The Asia Pacific Flexographic Printing Inks Market Size was valued at USD 6.20 billion in 2025, is expected to have 4.31 % CAGR from 2026 to 2034 and be worth USD 9.06 billion by 2034 from USD 6.46 billion in 2026.

Flexographic printing inks are fluid substances specifically formulated for use in flexographic printing a method that utilizes flexible relief plates to transfer ink onto various substrates such as paper, plastic, and metallic films. This form of printing is widely adopted across packaging industries due to its efficiency, cost-effectiveness, and ability to print on a wide range of materials. In the Asia Pacific region, the market for flexographic printing inks has evolved significantly, driven by the expanding consumer goods sector and rising demand for sustainable packaging solutions.

The Asia Pacific region holds a substantial share in the global packaging industry, with countries like China, India, Japan, and South Korea playing pivotal roles in shaping production and consumption trends.

Moreover, regulatory shifts toward eco-friendly inks especially water-based and UV-curable variants are influencing formulations and driving innovation among local manufacturers. With rapid urbanization and changing consumer preferences, the demand for high-quality, visually appealing packaging continues to rise across food & beverage, pharmaceuticals, and personal care sectors in the region.

MARKET DRIVERS

Growth of the Flexible Packaging Industry

One of the primary drivers fueling the Asia Pacific flexographic printing inks market is the rapid expansion of the flexible packaging industry. This surge is largely attributed to the increasing consumption of packaged food, beverages, and personal care products across emerging economies such as India, Indonesia, and Vietnam.

Flexible packaging requires high-performance printing solutions that offer durability, clarity, and resistance to moisture and heat qualities that flexographic inks effectively provide. The dominance of flexography in this segment stems from its compatibility with a variety of substrates including polyethylene, polypropylene, and aluminum foil. Moreover, the adoption of lightweight and recyclable packaging materials aligns with sustainability goals, further boosting the demand for eco-formulated flexographic inks.

In China alone, the China National Light Industry Council reported that flexible packaging production surpassed 15 million metric tons in 2025, representing a year-on-year increase. Given that flexographic printing accounts for more than 70% of all flexible packaging print jobs as noted by the Indian Institute of Packaging the correlation between flexible packaging growth and ink consumption becomes evident. This sustained momentum in packaging applications is a key catalyst for the ongoing expansion of the flexographic printing inks market in the Asia Pacific.

Rising Demand for Sustainable and Low-VOC Inks

Environmental concerns surrounding volatile organic compound (VOC) emissions have prompted a significant shift toward sustainable ink solutions in the Asia Pacific region. Water-based and UV-curable flexographic inks, which emit lower levels of VOCs compared to solvent-based alternatives, are increasingly preferred across industrial applications.

Governments across the region have introduced stricter environmental regulations to curb industrial pollution. For instance, the Ministry of Ecology and Environment in China mandated a reduction in VOC emissions from the printing sector under its 14th Five-Year Plan, pushing manufacturers to adopt greener alternatives. Similarly, in India, the Central Pollution Control Board (CPCB) has enforced emission standards that encourage the use of eco-friendly inks in packaging operations.

This regulatory push, combined with growing corporate emphasis on green branding, has spurred demand for bio-based and renewable resource-derived inks.

MARKET RESTRAINTS

Fluctuating Raw Material Prices

A significant restraint impacting the Asia Pacific flexographic printing inks market is the volatility in raw material prices, particularly petrochemical derivatives such as resins, solvents, and pigments. These components constitute a major portion of ink formulation costs.

For example, resin prices an essential ingredient in both water-based and solvent-based inks rose notably in China and India during the first half of 2025 due to supply chain disruptions and increased feedstock costs. This volatility places financial pressure on ink manufacturers, many of whom operate on narrow margins. Smaller regional players, especially in Southeast Asia, often struggle to absorb these cost increases without passing them on to end-users, potentially slowing adoption rates.

Also, geopolitical tensions and trade restrictions have disrupted the availability of critical raw materials. Such fluctuations not only hinder production consistency but also create uncertainty in pricing strategies, thereby acting as a key constraint on market growth in the Asia Pacific region.

Stringent Regulatory Compliance and Certification Requirements

Regulatory scrutiny regarding food safety and chemical usage in packaging has intensified across the Asia Pacific, posing a challenge to flexographic ink manufacturers. Countries such as Australia, Japan, and South Korea enforce strict compliance standards for inks used in food packaging, requiring extensive testing and certification processes. According to the Food Safety Standards Authority of Australia (FSANZ), any packaging material intended for direct food contact must undergo rigorous migration testing to ensure no harmful substances leach into food products.

These requirements significantly increase time-to-market and operational costs for ink producers. For instance, in Japan, the Ministry of Health, Labour and Welfare mandates adherence to the Japan Hygienic Olefin Plastics Association (JHOPA) guidelines, which necessitate specialized formulations and third-party validation.

Furthermore, multinational companies operating across multiple Asia Pacific markets face the added complexity of navigating diverse regulatory landscapes. This fragmentation hinders small and medium enterprises from scaling their operations efficiently.

MARKET OPPORTUNITIES

Expansion of E-commerce and Labeling Requirements

The burgeoning e-commerce sector in the Asia Pacific presents a compelling opportunity for the flexographic printing inks market. As online retail expands, so does the need for durable, informative, and visually appealing product labels and packaging.

E-commerce packaging demands differ from traditional retail packaging, emphasizing scannability, traceability, and damage resistance. Flexographic printing meets these needs by offering high-speed application capabilities and excellent print quality on corrugated boxes, flexible pouches, and adhesive labels. In particular, the requirement for barcodes, QR codes, and batch numbers has led to increased reliance on high-resolution flexo inks that ensure clear and consistent print output.

This trend underscores a robust growth avenue for flexographic ink suppliers catering to the evolving logistics and fulfillment needs of the digital commerce ecosystem in the Asia Pacific.

Technological Advancements in Ink Formulations

Technological innovation in ink chemistry is opening new avenues for growth in the Asia Pacific flexographic printing inks market. Manufacturers are increasingly focusing on developing advanced formulations that offer enhanced performance characteristics such as faster drying times, improved substrate adhesion, and superior color vibrancy.

According to a white paper released by the Society of Manufacturing Engineers (SME), recent developments in hybrid UV and electron beam (EB)-curable inks have significantly boosted print quality while reducing energy consumption.

One of the most promising advancements is the integration of nanotechnology in ink formulations. Companies in South Korea and Japan have pioneered the use of nano-pigments that improve opacity and reduce ink usage per print job. The Korea Institute of Industrial Technology (KITECH) found that nano-enhanced flexographic inks can cut down ink consumption without compromising print resolution.

Moreover, digital flexography an emerging technique combining digital imaging with conventional flexo presses is gaining traction in the region. This innovation allows for variable data printing and shorter run lengths, making it ideal for personalized packaging applications.

MARKET CHALLENGES

Competition from Alternative Printing Technologies

One of the foremost challenges confronting the Asia Pacific flexographic printing inks market is the increasing competition from alternative printing technologies such as gravure, offset, and digital printing. While flexography remains dominant in flexible packaging, digital printing is rapidly gaining ground due to its ability to support short-run, customizable, and on-demand print jobs.

Gravure printing, known for its superior print quality and long-run efficiency, continues to be a preferred choice for high-end packaging applications in Japan and South Korea. Despite its higher setup costs, gravure maintains a strong presence in luxury goods and magazine printing segments. Meanwhile, offset printing remains entrenched in label and carton production, especially in Australia and New Zealand, where brand owners prioritize high-resolution graphics.

The entry of digital inkjet technologies into the flexible packaging domain further intensifies the competition. Companies like HP and Canon have introduced industrial-scale digital presses capable of producing complex designs without the need for plate changes.

Skilled Labor Shortage and Technical Expertise Gap

A persistent challenge in the Asia Pacific flexographic printing inks market is the shortage of skilled labor and technical expertise required for efficient ink formulation, press operation, and color management. The complexity of flexographic printing demands trained professionals who understand substrate behavior, ink rheology, and drying mechanisms skills that are currently in short supply across several regional markets.

Moreover, in Southeast Asia, where labor-intensive manufacturing is still prevalent, automation in flexographic printing is advancing faster than workforce readiness.

This deficiency in skilled personnel leads to inconsistencies in print quality, longer setup times, and inefficient ink usage issues that ultimately affect productivity and profitability. Addressing this challenge will require collaborative efforts between governments, educational institutions, and industry stakeholders to develop targeted training programs and certifications tailored to the evolving demands of the flexographic printing sector in the Asia Pacific.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Resin Type and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | China, India, Japan, South Korea, Australia, New Zealand, Thailand, Indonesia, Philippines, Vietnam, Singapore, Rest of APAC. |

| Market Leader Profiled | DIC CORPORATION, SAKATA INX CORPORATION, Siegwerk Druckfarben AG & Co. |

SEGMENTAL ANALYSIS

By Type Insights

Water-based inks represented the largest segment in the Asia Pacific flexographic printing inks market, accounting for over 45% of total market volume as of 2025. This dominance is primarily attributed to their environmental advantages and increasing regulatory support across the region. Its consumption in the Asia Pacific grew at a steady pace, driven by stringent VOC emission norms introduced by environmental agencies in China, India, and Japan.

The shift toward sustainable packaging solutions has been particularly strong in India, where the Central Pollution Control Board mandated a reduction in solvent emissions from industrial printing operations.

Beyond regulatory compliance, cost-efficiency also plays a crucial role. Water-based inks require less complex ventilation systems and offer lower fire hazards compared to solvent-based counterparts. These combined factors reinforce the leading position of water-based inks in the Asia Pacific market.

UV-cured inks are emerging as the fastest-growing segment in the Asia Pacific flexographic printing inks market, projected to expand at a CAGR of 9.2%. This rapid growth stems from the superior performance characteristics and sustainability benefits offered by UV technology, which aligns with evolving industry needs.

One key driver is the increasing demand for high-speed printing in the flexible packaging sector. UV-cured inks dry instantly upon exposure to ultraviolet light, eliminating the need for lengthy drying tunnels and reducing energy consumption.

Moreover, UV inks emit negligible volatile organic compounds (VOCs), making them an attractive alternative in regions with tightening environmental regulations.

Technological advancements such as LED-UV curing have further accelerated adoption. Compared to conventional mercury lamps, LED-UV systems consume less power and generate minimal heat, preserving sensitive substrates.

By Resin Type Insights

Polyamide resins held the largest share in the Asia Pacific flexographic printing inks market, commanding 38.3% of total resin-based ink formulations as of 2025. This is largely due to their excellent adhesion properties on non-porous substrates such as polyethylene and polypropylene films materials widely used in food packaging applications.

Also, polyamide-based inks are preferred for retortable pouches and boil-in-bag packaging, which require resistance to high temperatures and moisture.

Moreover, polyamide resins offer superior printability and rub resistance, making them ideal for multi-layered laminated structures.

Also, ease of formulation compatibility with both solvent-based and water-based systems enhances their versatility. These attributes continue to drive their dominance in the regional flexographic ink resin market.

Polyurethane resins are witnessing the highest growth among resin types in the Asia Pacific flexographic printing inks market, expanding at a CAGR of 10.5%. This rapid ascent is fueled by the rising demand for high-performance inks capable of delivering superior abrasion resistance and substrate adhesion critical requirements in industrial and pharmaceutical packaging.

One major growth driver is the expansion of the medical and healthcare packaging sector. Polyurethane-based inks are extensively used in blister packs and sterilizable pouches due to their chemical resistance and ability to withstand gamma radiation and ethylene oxide sterilization processes.

In addition, the growing use of flexible electronics and smart packaging applications in countries like South Korea and Singapore is boosting demand for conductive and durable ink formulations.

Furthermore, manufacturers are increasingly formulating water-dispersible polyurethane inks to comply with environmental regulations. These factors collectively contribute to the robust growth trajectory of polyurethane resins in the Asia Pacific flexographic inks landscape.

COUNTRY LEVEL ANALYSIS

China held the largest share of the Asia Pacific flexographic printing inks market, contributing 32.5% of total regional consumption in 2025. As the world’s largest producer and consumer of packaging materials, China’s dominance is underpinned by its vast manufacturing ecosystem and continuous investment in advanced printing technologies.

The government’s emphasis on upgrading the printing sector through automation and digital workflows has further bolstered ink consumption.

Environmental regulations have also played a pivotal role in shaping market dynamics. With ongoing investments in smart packaging and e-commerce fulfillment infrastructure, China remains a central hub for flexographic ink demand in the Asia Pacific.

India is a key player in the market. The country's rapid industrialization, coupled with supportive regulatory policies, has positioned it as a key growth engine for flexographic ink suppliers.

The Indian packaging industry is expanding at a significant pace, driven by rising disposable incomes and urbanization. A significant share of flexible packaging units in the country rely on flexographic inks, particularly in food, beverage, and pharmaceutical sectors.

Government initiatives such as the Production-Linked Incentive (PLI) scheme for packaging industries have encouraged local ink manufacturers to invest in R&D and adopt sustainable practices. With a growing number of ink producers setting up domestic production facilities, India is poised to maintain its upward trajectory in the flexographic ink market.

Japan is maintaining a mature yet technologically advanced position within the region. While growth is moderate compared to emerging economies, Japan continues to lead in innovation and high-end ink formulation development.

A major driver in the Japanese market is the widespread adoption of UV-curable and LED-UV inks. Additionally, the country’s aging workforce has spurred automation in printing operations, favouring ink systems that reduce manual intervention.

Environmental regulations also play a critical role. This has led to increased research into low-migration and bio-based ink formulations by companies such as DIC Corporation and Toyo Ink.

Despite a saturated market, Japan remains a key innovator in the flexographic ink space.

South Korea is distinguished by its advanced manufacturing base and growing demand for high-performance packaging solutions. The country’s strong presence in the electronics and e-commerce sectors has significantly influenced ink consumption patterns.

The rise of cross-border logistics hubs in cities like Seoul and Busan has further boosted demand for scannable, durable, and visually appealing packaging.

Another key growth factor is the integration of smart packaging technologies. Companies such as LG Household & Health Care and Samsung C&T have adopted flexographic inks for printed electronics and anti-counterfeit labels.

These developments underline South Korea’s strategic role in driving innovation and sustainable practices in the regional flexographic ink market.

Australia and New Zealand is characterized by a strong preference for environmentally compliant products and high-quality packaging. Both nations have well-established regulatory frameworks that prioritize sustainability and food safety, directly influencing ink formulation trends. New Zealand mirrors this trend, with the Environmental Protection Authority (EPA) enforcing strict guidelines on industrial emissions.

In both markets, there is a growing interest in circular economy models, prompting brands to adopt recyclable and compostable substrates compatible with flexographic inks. This regulatory and consumer-driven environment positions Australia and New Zealand as niche but influential players in the Asia Pacific flexographic inks market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Overview of Competition in the Asia Pacific Flexographic Printing Inks Market

- DIC Corporation

- Sakata INX Corporation

- Siegwerk Druckfarben AG & Co. KGaA

- Toyo Ink SC Holdings Co., Ltd.

- Hubergroup Deutschland GmbH

- Flint Group

- Kao Collins Corporation

- SICPA Holding SA

- T&K TOKA Corporation

- Tokyo Printing Ink Mfg. Co., Ltd.

The competition in the Asia Pacific flexographic printing inks market is characterized by a mix of global leaders and regional players striving to capture market share through differentiation in product quality, sustainability credentials, and localized service capabilities. While multinational corporations dominate due to their extensive R&D resources and established distribution networks, domestic manufacturers in countries like India and China are gaining traction by offering cost-effective alternatives. The market landscape is further shaped by the increasing emphasis on green chemistry, regulatory compliance, and the need for high-performance ink solutions tailored to flexible packaging applications. As demand for sustainable and high-quality packaging grows, companies are intensifying their focus on innovation, customer engagement, and strategic expansion across emerging economies. This competitive environment fosters continuous improvement in ink technology, formulation adaptability, and application versatility, ensuring that the market remains dynamic and responsive to evolving industry needs.

Top Players in the Market

DIC Corporation (Japan)

DIC Corporation is a leading global manufacturer of printing inks, with a strong presence in the Asia Pacific flexographic inks segment. The company offers a diverse portfolio of eco-friendly and high-performance inks tailored for food packaging, labels, and industrial applications. DIC's commitment to innovation and sustainability has positioned it as a preferred supplier across key markets such as China, India, and Southeast Asia. Its strategic collaborations with local converters and investment in R&D have enabled the development of advanced ink technologies that align with evolving regulatory and consumer demands.

Toyo Ink S.C. Holdings Co., Ltd. (Japan)

Toyo Ink is a major player known for its cutting-edge ink solutions, including water-based, UV-curable, and low-migration formulations suitable for flexographic printing. The company has a robust footprint across the Asia Pacific region, particularly in Japan, South Korea, and ASEAN countries. Toyo Ink focuses on providing customized ink systems that meet the needs of food safety regulations and sustainable packaging trends. Its expertise in color science and substrate compatibility has made it a trusted partner among brand owners and packaging converters seeking high-quality print results.

Siegwerk Druckfarben AG & Co. KGaA (Germany, with strong APAC presence)

Siegwerk maintains a significant influence in the Asia Pacific flexographic printing inks market through its regional production facilities and dedicated technical service centers. The company emphasizes circular packaging solutions and has developed a range of recyclable and compostable ink systems compatible with flexographic processes. Siegwerk’s localized approach enables it to respond swiftly to market-specific requirements in countries like India, Australia, and Thailand. By integrating sustainability into product development and strengthening customer partnerships, Siegwerk continues to expand its relevance in the APAC region.

Top Strategies Used by Key Market Participants

One of the primary strategies employed by key players is product innovation and formulation customization. Companies are investing heavily in R&D to develop inks that meet evolving environmental regulations and performance standards. This includes formulating bio-based, low-VOC, and recyclable ink options that cater to specific substrates and end-use applications across the packaging industry.

Another critical strategy is expanding regional manufacturing and technical support infrastructure. Leading ink manufacturers are setting up local production units and application labs in high-growth Asia Pacific markets to reduce lead times, comply with local regulations, and offer tailored technical assistance to printers. These localized efforts help strengthen customer relationships and improve supply chain efficiency.

Lastly, companies are focusing on strategic partnerships and collaboration with converters and raw material suppliers. By working closely with packaging producers and resin manufacturers, ink suppliers can co-develop solutions that enhance print quality, durability, and sustainability. These alliances also enable faster adoption of new technologies and ensure alignment with industry-wide sustainability goals.

RECENT HAPPENINGS IN THE MARKET

- In March 2025, DIC Corporation expanded its production capacity at its Shanghai facility to better serve growing demand in China and neighboring markets. This move was aimed at enhancing supply chain resilience and supporting increased adoption of eco-friendly ink solutions in the region.

- In August 2025, Toyo Ink launched a new line of low-migration UV flexographic inks designed specifically for food packaging applications. The introduction was part of the company’s broader effort to align with stringent food safety regulations and support converters in transitioning toward safer and more sustainable printing practices.

- In January 2025, Siegwerk opened a state-of-the-art technical service center in Bangkok to provide localized support for customers in Southeast Asia. The facility focuses on ink testing, substrate compatibility assessments, and training programs aimed at improving print performance and operational efficiency.

- In May 2025, Sun Chemical, a key player in the ink industry, partnered with an Indian packaging firm to co-develop water-based flexographic inks suited for multilayer films. This collaboration reflects the growing trend of joint innovation between ink suppliers and packaging converters to address sustainability challenges.

- In September 2025, INX International Ink Co. announced the establishment of a regional distribution hub in Melbourne, Australia. This initiative was designed to streamline logistics, reduce delivery times, and enhance customer service for flexographic ink users across Australia and New Zealand.

MARKET SEGMENTATION

This research report on the asia pacific flexographic printing inks market has been segmented and sub-segmented into the following.

By Type

- Water-Based Inks

- UV-Cured Inks

By Resin Type

- Polyamide Resins

- Polyurethane Resins

By Country

- China

- India

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Indonesia

- Philippines

- Vietnam

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the Asia Pacific flexographic printing inks market?

Growth is driven by increasing demand for flexible packaging, rising e-commerce, advancements in printing technology, and eco-friendly inks.

Which countries in Asia Pacific are leading in the adoption of flexographic printing inks?

China, India, Japan, and South Korea are key markets due to their strong manufacturing and packaging sectors.

What environmental regulations impact the flexographic inks market in Asia Pacific?

Governments are promoting the use of low-VOC and biodegradable inks, pushing companies toward water-based and UV-curable alternatives.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com