Asia Pacific Food Antioxidants Market Size, Share, Trends & Growth Forecast Report By Source (Oils, Fruits & Vegetables, Spices & Herbs, Botanical Extracts, Gallic Acid, Petroleum), Application, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest Of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Food Antioxidants Market Size

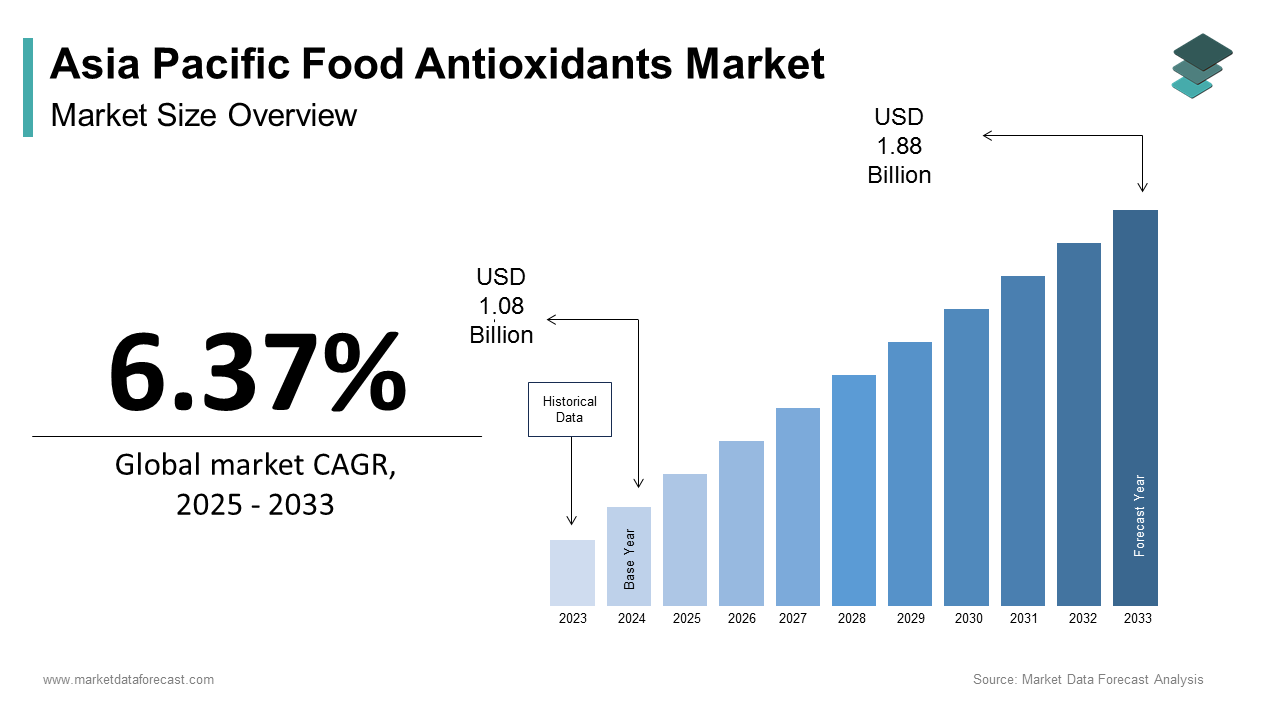

The Asia Pacific Food Antioxidants Market Size is estimated to grow from USD 1.08 billion in 2024 to USD 1.88 billion in 2033, representing a CAGR of 6.37% during the forecast period

Food antioxidants are compounds that inhibit oxidation in food products, thereby extending shelf life and preserving flavour, colour, and nutritional value. In the Asia Pacific region, these additives have become integral to the food and beverage industry due to rising concerns over food spoilage and increasing consumer awareness about health benefits linked with antioxidant-rich diets. The market includes a wide range of natural and synthetic antioxidants such as tocopherols, ascorbates, butylated hydroxyanisole (BHA), and butylated hydroxytoluene (BHT).

With rapid urbanization and changing dietary patterns across countries like China, India, Japan, and Australia, demand for processed and packaged foods has surged, directly boosting the need for effective preservatives. Moreover, regulatory bodies such as Food Standards Australia New Zealand (FSANZ) and the National Health Commission of China have implemented stringent food safety standards, further influencing the adoption of approved antioxidants. These aspects position the Asia Pacific food antioxidants market as a key player in the global landscape, driven by both industrial needs and health-conscious consumers.

MARKET DRIVERS

Rising Demand for Processed and Ready-to-Eat Foods

The growing consumption of processed and ready-to-eat (RTE) foods is one of the most significant drivers of the Asia Pacific food antioxidants market. As urbanization accelerates and disposable incomes rise, especially in emerging economies such as India, Indonesia, and Vietnam, there has been a marked shift toward convenience-based diets. This trend necessitates the use of antioxidants to prevent rancidity and maintain product integrity during extended storage periods. Natural antioxidants like vitamin E and rosemary extract are increasingly preferred over synthetic variants due to shifting consumer perceptions around clean-label products. Moreover, government initiatives promoting food fortification such as India's FSSAI guidelines encouraging nutrient enrichment have indirectly supported the use of antioxidants in staple food items. This convergence of lifestyle changes, regulatory support, and evolving consumer preferences collectively reinforces the upward trajectory of the food antioxidants market in the region.

Increasing Health Awareness and Functional Food Consumption

The growing health consciousness among consumers and the subsequent rise in demand for functional foods is another pivotal driver of the Asia Pacific food antioxidants market. Functional foods, which offer additional health benefits beyond basic nutrition, often contain bioactive compounds such as polyphenols, flavonoids, and carotenoids which act as antioxidants. This trend is particularly pronounced in developed markets like Japan and South Korea, where the concept of "functional foods" is well-established. Similarly, in China, there is a year-over-year increase in sales of fortified foods, many of which incorporated antioxidant ingredients to appeal to health-conscious buyers. Apart from these, public health campaigns emphasizing the role of antioxidants in disease prevention have played a crucial role in shaping consumer behavior.

MARKET RESTRAINTS

Regulatory Hurdles and Stringent Approval Processes

Complex regulatory frameworks and lengthy approval procedures for food additives is a significant restraint for the Asia Pacific food antioxidants market. Each country in the region has its own set of food safety laws, leading to fragmented compliance requirements that can delay product launches and increase operational costs for manufacturers. For example, according to the ASEAN Food Safety Regulatory Framework, harmonization efforts have made progress, but differences still exist between national standards, particularly concerning permissible levels of synthetic antioxidants like BHA and BHT. In China, the National Health Commission mandates rigorous testing and documentation before approving any new antioxidant ingredient, a process that can take up to two years. Similarly, in India, the Food Safety and Standards Authority of India (FSSAI) frequently revises its list of permitted additives, creating uncertainty for suppliers. Moreover, consumer skepticism toward synthetic additives has prompted regulators to impose stricter limits on their usage. Such developments, inadvertently slow down innovation and market expansion in the food antioxidants segment across the Asia Pacific region.

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices, particularly for natural antioxidants derived from agricultural sources is an addition restraining factor for the Asia Pacific food antioxidants market . Ingredients such as rosemary extract, green tea polyphenols, and vitamin E depend heavily on crop yields, which are influenced by climatic conditions, geopolitical tensions, and trade policies. These fluctuations directly impact production costs for antioxidant manufacturers, especially in countries like China and India, where a large portion of raw materials are sourced domestically. Apart from these, logistical bottlenecks exacerbated by pandemic-related restrictions and port congestion have further delayed raw material procurement and finished product distribution. Furthermore, geopolitical instability in regions like Eastern Europe and Central Asia has disrupted the supply of essential oils and plant extracts used in natural antioxidant formulations. These factors hinder market growth and limit the scalability of natural antioxidant solutions in the Asia Pacific region.

MARKET OPPORTUNITIES

Expansion of Clean Label and Organic Food Trends

The growing preference for clean label and organic food products is one of the potential opportunities in the Asia Pacific food antioxidants market. Consumers across the region are increasingly scrutinizing ingredient lists and favouring products with recognizable, naturally derived components. This shift aligns with rising health consciousness and environmental awareness, prompting manufacturers to reformulate their products using natural antioxidants such as tocopherols, ascorbic acid, and plant-based extracts. Governments in the region have also recognized this trend, offering policy incentives to promote organic farming and sustainable food production. As a result, food and beverage companies are investing heavily in R&D to develop innovative antioxidant blends that meet clean label demands without compromising on shelf life or sensory attributes.

Growth in Functional Beverages and Fortified Drinks

The expanding market for functional beverages and fortified drinks presents another substantial opportunity for the Asia Pacific food antioxidants industry. With rising health awareness and an increasing focus on preventive healthcare, consumers are gravitating toward beverages that offer added nutritional benefits, including immune support, energy enhancement, and digestive wellness. Many of these functional beverages incorporate antioxidants to improve oxidative stability and deliver perceived health advantages. Notably, sports drinks, herbal infusions, and antioxidant-rich juices have seen robust growth, driven by younger demographics seeking performance-boosting and wellness-oriented options. In India, for example, the Ayurveda-inspired beverage category has gained traction, with products containing ingredients like amla (Indian gooseberry) and tulsi (holy basil)—both rich in natural antioxidants. Moreover, multinational beverage giants such as Coca-Cola and PepsiCo have launched antioxidant-fortified product lines tailored to Asian markets. This trend is expected to continue as manufacturers leverage scientific research linking antioxidants to cellular protection and anti-aging benefits, further embedding these compounds into mainstream beverage formulations across the region.

MARKET CHALLENGES

Consumer Misconceptions About Synthetic Antioxidants

The widespread consumer misconception regarding synthetic antioxidants is a serious challenge for the Asia Pacific food antioxidants market. Despite their proven efficacy and regulatory approval, synthetic variants such as butylated hydroxyanisole (BHA) and butylated hydroxytoluene (BHT) are often viewed negatively due to misinformation and media-driven narratives linking them to health risks. This perception gap has led to a growing demand for natural alternatives, pressuring manufacturers to reformulate products even when synthetic antioxidants may be more cost-effective and stable under processing conditions. Moreover, social media platforms and online forums have amplified these concerns, often citing outdated or misinterpreted studies. Regulatory bodies such as the U.S. FDA and the European Food Safety Authority (EFSA) reaffirmed the safety of these compounds within prescribed limits still the damage to consumer trust persists.

Technological Limitations in Natural Antioxidant Extraction and Stability

The technological limitations associated with extracting and stabilizing natural antioxidants for commercial food applications is another pressing challenge confronting the Asia Pacific food antioxidants market. Unlike synthetic counterparts, which offer consistent performance and longer shelf life, natural antioxidants derived from plant sources often exhibit variability in potency, solubility, and thermal stability. This inconsistency complicates their integration into diverse food matrices, particularly in high-heat processing environments such as baking and frying. Furthermore, extraction techniques such as solvent-based methods and supercritical fluid extraction remain costly and energy-intensive, limiting scalability for smaller manufacturers. Besides, maintaining the bioactivity of natural antioxidants during long-term storage remains a concern.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.37% |

| Segments Covered | By Source, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, And the Rest Of Asia-Pacific |

| Market Leaders Profiled | Kemin Industries, Archer Daniels Midland Company, BASF SE, Koninklijke DSM N.V., Barentz Group, Camlin Fine Sciences Ltd, DuPont de Nemours Inc., Eastman Chemical Company, Vitablend Nederland B.V., BTSA Biotecnologías Aplicadas |

SEGMENTAL ANALYSIS

By Source Insights

The oils segment commanded the Asia Pacific food antioxidants market by accounting for 32.4% of total consumption in 2024. The surge in edible oil production and consumption in the region is one of the key driving factors behind the growth of the oils segment. This dominance is also primarily attributed to the extensive use of antioxidants in edible oil processing and preservation across major economies such as China, India, and Indonesia. These oils are highly susceptible to oxidation, necessitating the addition of antioxidants like tocopherols and synthetic variants such as BHT to extend shelf life and maintain quality. Besides, government initiatives aimed at reducing food waste have further reinforced the demand for antioxidants in oil formulations.

The botanical extracts segment is anticipated to grow at the fastest rate and is likely registering a CAGR of 11.2% during the forecast period. The rising application of botanical extracts such as green tea polyphenols, rosemary extract, and curcumin in functional foods and beverages is a primary growth catalyst for the botanical extracts segment. This rapid expansion is driven by shifting consumer preferences toward natural and clean-label ingredients, particularly in health-conscious markets such as Japan, South Korea, and Australia. The increasing investment in R&D for bioactive extraction technologies is another significant factor contributing to this growth. As per research bulletin by the National University of Singapore, advancements in supercritical fluid extraction and microencapsulation have significantly enhanced the stability and efficacy of botanical antioxidants, making them more viable for industrial-scale applications. The botanical extracts segment is poised to outpace other categories in the Asia Pacific food antioxidants market as consumers are demanding safer and more sustainable alternatives.

By Application Insights

The fats & oils application segment led the Asia Pacific food antioxidants market by capturing 35.2% of total demand in 2024. The high susceptibility of fats and oils to oxidative rancidity, which necessitates the widespread use of antioxidants to preserve freshness, flavor, and nutritional integrity is driving the leading position of the fats & oils application segment. These oils often require antioxidant additives such as tocopherols, TBHQ, and BHA to enhance oxidative stability during transportation, storage, and usage. Moreover, regulatory bodies such as the Food Safety and Standards Authority of India (FSSAI) and Food Standards Australia New Zealand (FSANZ) mandate the use of approved antioxidants in packaged oils, reinforcing their market penetration. Also, growing awareness about heart health has led to increased fortification of oils with natural antioxidants like vitamin E, further strengthening this segment’s dominance in the regional food antioxidants market.

The bakery & confectionery segment is emerging as the fastest-growing application area in the Asia Pacific food antioxidants market and is projected to expand at a CAGR of 9.8% between 2025 and 2033. The expanding bakery industry and the increasing incorporation of antioxidants to enhance the shelf life and sensory properties of baked goods is fuelling the rapid growth of the bakery & confectionery segment. Baked products such as cookies, crackers, and pastries often contain fats and oils that are prone to oxidation, making antioxidants essential for maintaining texture, flavor, and appearance over time. Furthermore, there is a growing trend toward functional bakery products fortified with natural antioxidants. Besides, manufacturers are increasingly using rosemary extract, ascorbic acid, and tocopherols to meet clean-label expectations while ensuring product longevity. With rising disposable incomes and evolving consumer preferences, the bakery & confectionery sector is set to drive substantial demand for antioxidants in the coming decade.

LEADING PLAYERS IN THE ASIA PACIFIC FOOD ANTIOXIDANTS MARKET

BASF SE

BASF is a global leader in food antioxidants and holds a strong presence in the Asia Pacific region. The company offers a wide portfolio of synthetic and natural antioxidants, including butylated hydroxytoluene (BHT) and tocopherols. BASF's commitment to innovation and sustainability has enabled it to cater to diverse food applications while maintaining regulatory compliance across key markets like China, India, and Japan. Its technical expertise and long-standing partnerships with regional food manufacturers make it a dominant player.

Kerry Group plc

Kerry Group is a major contributor to the Asia Pacific food antioxidants market due to its focus on natural and clean-label solutions. The company provides plant-based antioxidant extracts tailored for the region’s growing demand for functional foods and beverages. Kerry invests heavily in R&D to develop customized antioxidant blends that enhance product stability without compromising taste or nutrition, making it a preferred partner among leading F&B brands in Southeast Asia and Australia.

Cargill, Incorporated

Cargill plays a crucial role in the Asia Pacific food antioxidants sector by integrating sustainable sourcing and advanced formulation technologies. The company supplies antioxidants derived from oils and botanical extracts, supporting the preservation needs of edible oils, bakery products, and processed meats. With its extensive supply chain network and localized production facilities, Cargill ensures efficient delivery of high-quality antioxidant solutions across the region.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by key players in the Asia Pacific food antioxidants market is product innovation focused on natural and clean-label ingredients . Companies are investing in research to develop plant-based antioxidants that align with consumer preferences for transparency and health benefits.

Another critical approach is strategic partnerships and collaborations with local manufacturers , enabling multinational companies to better understand regional regulatory landscapes and consumer behavior while accelerating product development and distribution.

Lastly, firms are increasingly adopting expansion through localized production facilities and acquisitions , allowing them to reduce costs, improve supply chain efficiency, and strengthen their foothold in high-growth Asian markets such as India, Indonesia, and Vietnam.

KEY MARKET PLAYERS AND COMPETITIVE OVERVIEW

Major Players of the Asia Pacific food antioxidants market include Kemin Industries, Archer Daniels Midland Company, BASF SE, Koninklijke DSM N.V., Barentz Group, Camlin Fine Sciences Ltd, DuPont de Nemours Inc., Eastman Chemical Company, Vitablend Nederland B.V., BTSA Biotecnologías Aplicadas

The competition in the Asia Pacific food antioxidants market is intensifying as both global and regional players strive to capture a larger share of the expanding food and beverage industry. The market features a mix of established multinational corporations and emerging local manufacturers, all vying to meet the rising demand for shelf-stable and nutritious food products. Companies are differentiating themselves through innovation, particularly in the area of natural antioxidants, which aligns with the region’s growing preference for clean-label and organic ingredients. Strategic investments in R&D have become a priority, enabling firms to develop customized antioxidant blends tailored to specific food applications. Additionally, partnerships with food processors and ingredient suppliers are becoming more common, helping companies secure long-term contracts and gain insights into evolving consumer preferences. At the same time, regulatory dynamics vary significantly across countries, prompting firms to adopt flexible compliance strategies. As competition heats up, brand reputation, product efficacy, and sustainability initiatives are playing an increasingly important role in shaping market positioning across the Asia Pacific region.

RECENT HAPPENINGS IN THE MARKET

- In June 2023, Kerry Group launched a new line of plant-based antioxidant extracts specifically formulated for Southeast Asian food manufacturers. This move was aimed at meeting the growing demand for natural preservatives in ready-to-eat meals and functional beverages.

- In September 2023 , Cargill expanded its production facility in Indonesia to increase its capacity for producing oil-derived antioxidants, strengthening its supply chain presence in one of the region’s fastest-growing edible oil markets.

- In January 2024 , BASF partnered with a Japanese biotech firm to co-develop next-generation antioxidant formulations using fermentation-based technology, enhancing performance and stability in processed foods.

- In March 2024 , ADM (Archer Daniels Midland) entered into a joint venture with an Indian spice manufacturer to extract antioxidants from traditional herbs, targeting the growing health-conscious consumer base in South Asia.

- In May 2024 , Koninklijke DSM N.V. introduced a digital platform to assist food manufacturers in selecting the most suitable antioxidant blends based on application, regulatory requirements, and desired shelf life, improving customer engagement and technical support across the region.

MARKET SEGMENTATION

This research report on the Asia Pacific Food Antioxidants Market has been segmented and sub-segmented based on source, application and region.

By Source

- Oils

- Fruits & Vegetables

- Spices & Herbs

- Botanical Extracts

- Gallic Acid

- Petroleum

By Application

- Fats & Oils

- Bakery & Confectionery

- Prepared Meat & Poultry

- Others

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of Asia-Pacific

Frequently Asked Questions

1. What are the major types of food antioxidants used in this market?

Common antioxidants include natural antioxidants (such as vitamin C, vitamin E, rosemary extract, and green tea extract) and synthetic antioxidants (such as BHA, BHT, TBHQ, and propyl gallate).

2. Which countries are the largest consumers of food antioxidants in the Asia Pacific region?

Key countries include China, India, Japan, South Korea, and Australia, driven by large populations, expanding food industries, and rising awareness of food preservation.

3. What are the main applications of food antioxidants in the Asia Pacific market?

Food antioxidants are widely used in bakery & confectionery, fats & oils, meat products, beverages, and dairy to maintain freshness and prevent spoilage.

4. What is driving the growth of the Asia Pacific food antioxidants market?

Growth is fueled by rising processed food consumption, increasing health awareness, urbanization, and the demand for clean-label and shelf-stable products.

5. What are the challenges faced by the market?

Key challenges include stringent food safety regulations, limited awareness in rural areas, and consumer concerns over synthetic additives.

6. Which segment is growing faster: natural or synthetic antioxidants?

Natural antioxidants are witnessing faster growth due to the clean-label trend and increasing consumer demand for natural and organic food additives.

7. Who are the key market players in the Asia Pacific food antioxidants market?

Leading players include BASF SE, Archer Daniels Midland Company, DuPont, Eastman Chemical Company, Kemin Industries, Barentz International, Camlin Fine Sciences, and Kalsec Inc.

8. How are food safety regulations impacting the market?

Governments in countries like China, India, and Japan are tightening regulations on food additives, encouraging manufacturers to adopt safe, approved antioxidants and natural alternatives.

9. What is the future outlook for the Asia Pacific food antioxidants market?

The market is expected to grow steadily due to increased investment in food processing, R&D in natural antioxidants, and rising consumer preference for healthier, longer-lasting food options.

10. Who are the leading players in the Asia Pacific food antioxidants market?

Major companies include BASF SE, DuPont, Eastman Chemical Company, Archer Daniels Midland Company, Kemin Industries, Camlin Fine Sciences, Kalsec Inc., Barentz International

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com