Asia Pacific Greenhouse Equipment Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Equipment, Type, Crop Type, and By Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis 2024 to 203

Asia Pacific Greenhouse Equipment Market Size

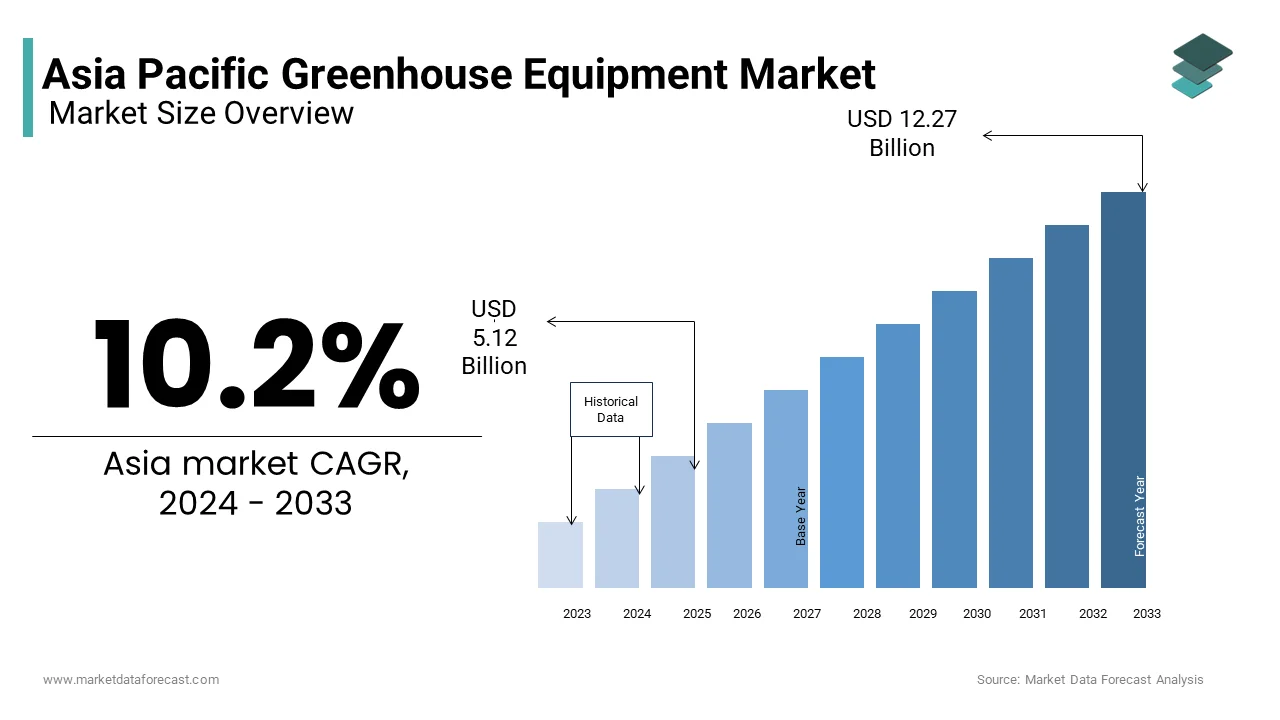

The Asia Pacific greenhouse equipment market is anticipated to expand from USD 5.12 billion in 2024 to USD 12.27 billion by 2033, growing at a CAGR of 10.2%.

The Asia Pacific greenhouse equipment market covers different technologies and systems designed to enhance controlled-environment agriculture, including structures such as glass, plastic, and polycarbonate greenhouses, along with climate control mechanisms like heating, ventilation, irrigation, lighting, and shading systems. These facilities enable year-round cultivation of crops by regulating temperature, humidity, light exposure, and nutrient supply, critical in regions facing erratic weather patterns and land scarcity.

With rising population pressures and shrinking arable land in several countries across the region, greenhouse farming is gaining traction as a sustainable alternative to conventional agriculture. Also, according to the Food and Agriculture Organization (FAO), over 40% of global agricultural production now faces risks from climate change, making controlled environment agriculture an essential adaptation strategy. In China and India, government-backed initiatives are promoting greenhouse adoption among smallholder farmers to boost productivity and reduce post-harvest losses.

Japan and South Korea have been early adopters of high-tech vertical farming integrated with greenhouse systems, while Australia has seen growth in commercial hydroponic farms using advanced environmental controls. As per the United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP), greenhouse farming can yield up to five times more produce per hectare than open-field farming, reinforcing its strategic importance in food security planning across the region.

MARKET DRIVERS

Rising Demand for Food Security Amid Climate Change Pressures

A main driver of the Asia Pacific greenhouse equipment market is the growing need for food security in the face of increasingly unpredictable climate conditions. Countries like India, Thailand, and the Philippines have experienced significant disruptions in traditional farming cycles due to monsoon irregularities, droughts, and extreme temperatures.

Like, according to the Asian Development Bank (ADB), crop yields in South and Southeast Asia could decline by up to 30% by 2050 if current climatic trends continue.

Moreover, greenhouse technology offers a viable solution by enabling stable, year-round production regardless of external weather fluctuations. In response, governments across the region have introduced subsidies and training programs to encourage farmers to adopt greenhouse-based cultivation.

For instance, under India’s National Horticulture Mission, over 150,000 small-scale farmers received financial assistance for setting up low-cost polyhouses between 2020 and 2023.

Apart from these, urbanization and changing dietary habits are increasing demand for fresh fruits and vegetables, which greenhouse systems can efficiently supply through localized production. This combination of climate resilience and enhanced productivity is fueling robust market expansion across the Asia Pacific region.

Government Support and Investment in Agricultural Modernization

An additional key driver of the Asia Pacific greenhouse equipment market is strong governmental backing and investment in modernizing agricultural practices. Many national governments in the region have recognized the potential of greenhouse farming to improve food self-sufficiency and rural livelihoods.

Similarly, in China, the Ministry of Agriculture and Rural Affairs has allocated over USD 3 billion since 2020 to promote protected horticulture, including subsidies for greenhouse construction materials and drip irrigation systems.

Similarly, in India, the state governments of Punjab, Haryana, and Maharashtra have launched special schemes offering up to 75% capital cost subsidies for greenhouse installation under the Rashtriya Krishi Vikas Yojana (RKVY). These incentives have led to a rise in greenhouse adoption among progressive farmers in the last three years.

In Japan and South Korea, public-private partnerships have accelerated the development of smart greenhouses equipped with AI-driven climate control systems and automated harvesting solutions. These policy-level interventions and targeted investments are playing a crucial role in expanding the regional greenhouse equipment market.

MARKET RESTRAINTS

High Initial Capital Investment and Limited Access to Credit

One of the major restraints hindering the growth of the Asia Pacific greenhouse equipment market is the high initial capital outlay required for setting up advanced greenhouse systems. Traditional farming remains significantly cheaper, making it difficult for small- and medium-scale farmers to transition without financial support.

As per the International Fund for Agricultural Development (IFAD), the cost of constructing a fully equipped greenhouse can be up to ten times higher than that of conventional open-field farming.

Access to credit also poses a challenge, particularly in rural areas where banking infrastructure is limited. In countries like Indonesia and Vietnam, less than 30% of smallholder farmers have access to formal financing channels, according to the World Bank. Even when subsidies are available, bureaucratic delays and lack of awareness often prevent timely implementation.

Besides, maintenance costs for climate control systems, irrigation equipment, and energy consumption further add to the financial burden. For example, in India, the operational expenses of a high-tech greenhouse can be twice as much as those of a basic polyhouse, as per the Indian Council of Agricultural Research (ICAR).

Hence, these economic barriers hinder widespread adoption, especially among resource-constrained farmers.

Lack of Technical Expertise and Skilled Labor

An important barrier to the expansion of the Asia Pacific greenhouse equipment market is the shortage of skilled labor and technical expertise required to operate and maintain sophisticated greenhouse systems. Unlike conventional farming, greenhouse management demands knowledge of climate control, nutrient delivery, pest management, and automation systems. As per the Food and Agriculture Organization (FAO), only a small share of farmers in South and Southeast Asia receive formal training in greenhouse techniques.

This skills gap limits the effectiveness of government subsidy programs, as many beneficiaries struggle to optimize greenhouse productivity. In the Philippines, the Department of Agriculture indicates that approximately 40% of subsidized greenhouses remain underutilized due to poor maintenance and improper crop selection.

Moreover, there is a lack of extension services and on-site advisory support to guide farmers through the complexities of greenhouse farming. In India, despite government-funded training centers, a notable portion of participants do not apply the learned techniques effectively, as noted by the Indian Institute of Horticultural Research (IIHR). Without adequate education and continuous support, the adoption of greenhouse equipment will continue to lag behind its full potential.

MARKET OPPORTUNITY

Expansion of Smart Farming and IoT Integration

A major opportunity driving the Asia Pacific greenhouse equipment market is the rapid advancement of smart farming technologies and Internet of Things (IoT) integration. The deployment of sensors, cloud-based monitoring, and automated control systems enables real-time data collection and precise environmental adjustments within greenhouses.

According to McKinsey & Company, digital agriculture technologies have the potential to increase farm profitability by up to 25%, encouraging wider adoption of smart greenhouse solutions.

Countries like Japan and South Korea are leading this transformation, with companies developing AI-powered climate controllers and remote monitoring applications for greenhouse operations.

Also, startups in India and Indonesia are introducing affordable smart greenhouse kits tailored for small-scale farmers. With increased connectivity and digital literacy, the integration of smart technologies presents a substantial growth avenue for the regional greenhouse equipment industry.

Urban Agriculture and Vertical Farming Trends

One more promising opportunity for the Asia Pacific greenhouse equipment market is the growing trend of urban agriculture and vertical farming, particularly in densely populated cities. As urbanization accelerates across the region, traditional farmland is diminishing, prompting interest in space-efficient farming alternatives. According to the United Nations Department of Economic and Social Affairs (UN DESA), 68% of the world's population is expected to reside in urban areas by 2050.

Vertical farming, which is often conducted within a controlled-environment greenhouse, offers a solution by utilizing stacked layers and LED grow lights to maximize yield per square meter. In Singapore, where arable land is virtually nonexistent, the government has actively supported the development of rooftop and indoor greenhouses.

Similarly, in Tokyo and Seoul, commercial greenhouse operators are adopting hydroponic and aeroponic systems to grow high-value crops near consumer hubs. These developments underscore a growing shift toward localized, high-yield greenhouse farming, creating new market opportunities across the Asia Pacific region.

MARKET CHALLENGES

Regional Disparities in Adoption Rates

A critical challenge for the Asia Pacific greenhouse equipment market is the significant disparity in adoption rates across different countries and even within regions of the same country. While developed economies like Japan, South Korea, and Australia have embraced high-tech greenhouse systems, many parts of South and Southeast Asia still rely on traditional farming methods.

Like, less than 5% of cultivated land in Bangladesh and Cambodia uses any form of protected cultivation.

These disparities stem from variations in economic development, access to funding, and levels of agricultural modernization. For example, in India, states like Punjab and Maharashtra have high adoption rates due to better infrastructure and government support, whereas eastern and central regions lad because of lower farmer awareness and inadequate extension services, as per the Indian Council of Agricultural Research (ICAR).

Moreover, cultural preferences for open-field farming persist in certain communities, slowing the transition to greenhouse-based agriculture.

Energy Costs and Sustainability Concerns

One more growing concern affecting the Asia Pacific Greenhouse Equipment Market is the high energy consumption associated with climate-controlled greenhouse operations. Heating, cooling, artificial lighting, and irrigation systems require significant power inputs, particularly in tropical and temperate climates where ambient conditions must be carefully regulated. According to the International Renewable Energy Agency (IRENA), energy costs can account for up to 40% of total operating expenses in high-tech greenhouses.

This dependency on electricity or fossil fuels raises sustainability concerns, especially in countries where the grid relies heavily on coal. Similarly, in China, greenhouse operators in northern provinces face seasonal energy shortages during winter months due to increased heating demand, as reported by the National Development and Reform Commission (NDRC).

To mitigate these issues, some companies are exploring renewable energy integration, such as solar-powered greenhouses and biomass-fueled heating systems. However, initial investment costs and technological limitations slow widespread adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 10.2% |

| Segments Covered | By Equipment, Greenhouse, Crop, And Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | Richel Group SA, Argus Control Systems Ltd, Certhon, Logiqs B.V, Lumigrow, Inc, Agra Tech, Inc, Rough Brothers, Inc, Nexus Corporation, Hort Americas, LLC, Heliospectra AB. |

SEGMENTAL ANALYSIS

By Equipment Insights

Heating Systems

Heating systems depicted the largest segment in the Asia Pacific greenhouse equipment market, capturing 38.6% of total market revenue in 2024. This dominance is primarily attributed to the critical role heating equipment plays in maintaining optimal growing conditions across temperate and subtropical regions where seasonal temperature variations can severely impact crop yield.

In countries like China and Japan, where winter temperatures often fall below plant tolerance levels, greenhouse operators rely heavily on heating systems such as radiant heaters, boiler-based hot water systems, and geothermal heat exchangers.

Moreover, government-backed agricultural modernization programs are accelerating the adoption of climate control technologies. With rising demand for off-season produce and increasing investments in controlled-environment agriculture, the heating systems segment remains a cornerstone of the regional greenhouse equipment industry.

Cooling Systems

Cooling systems are projected to register the highest CAGR of 9.7% from 2025 to 2033. This rapid expansion is driven by the need to regulate internal temperatures in tropical and semi-arid regions where ambient heat can hinder photosynthesis and damage sensitive crops.

Countries such as Thailand, Vietnam, and Malaysia experience high humidity and intense solar radiation, making evaporative cooling pads, fogging systems, and ventilation fans essential components of greenhouse infrastructure.

Besides, advancements in smart climate control technologies—such as AI-powered temperature sensors and automated shading mechanisms—are enhancing the efficiency of cooling systems. These factors collectively contribute to the segment’s accelerated growth trajectory within the Asia Pacific greenhouse equipment landscape.

By Greenhouse Insights

Plastic Greenhouses

Plastic greenhouses commanded the market, accounting for 62.3% of the Asia Pacific greenhouse equipment market in 2024. The widespread adoption of plastic-covered structures is largely due to their cost-effectiveness, ease of installation, and adaptability to diverse climatic conditions.

These greenhouses, typically made using polyethylene films or UV-stabilized sheets, offer an economical solution for smallholder farmers seeking to enhance productivity without heavy capital investment. In India, China, and Vietnam, where a majority of farming operations are conducted on small plots of land, plastic greenhouses provide a practical alternative to glass structures that are expensive and complex to maintain.

According to the Indian Council of Agricultural Research (ICAR), the cost of setting up a basic plastic greenhouse is nearly half that of a glass greenhouse, making it accessible to a broader demographic. Besides, governments in these countries have been promoting polyhouse cultivation through subsidies and training initiatives.

The flexibility of plastic materials also allows for customization based on local weather patterns, enabling farmers to optimize light transmission and ventilation. As a result, plastic greenhouses remain the preferred choice for a wide range of horticultural applications across the region.

Glass Greenhouses

Glass greenhouses are expected to grow at the fastest CAGR of 8.9% during the forecast period. This growth is primarily fueled by increasing investments in high-tech, climate-controlled agriculture in developed economies such as Japan, South Korea, and Australia.

Unlike plastic alternatives, glass greenhouses offer superior durability, better insulation, and enhanced aesthetic appeal, making them ideal for commercial and research-oriented applications. In Japan, where urban farming is gaining traction, companies like Mirai Co. Ltd. have deployed multi-tiered glass greenhouses equipped with LED lighting and automated nutrient delivery systems, significantly boosting output per square meter.

Moreover, the integration of Internet of Things (IoT)-enabled climate control systems has improved operational efficiency in glass greenhouses.

Government-led initiatives in Australia are also supporting the sector, with the Department of Agriculture and Fisheries funding pilot projects that combine renewable energy with glass greenhouse operations. These developments underscore the strong momentum behind this premium segment.

By Crop Insights

Fruits & Vegetables

Fruits & Vegetables led the Asia Pacific Greenhouse Equipment Market, capturing 58.5% of the total market value in 2024. This segment’s progress is due to the growing demand for fresh, pesticide-free produce and the increasing reliance on greenhouse cultivation to ensure a consistent supply throughout the year.

With rapid urbanization and changing dietary preferences, consumers across the region are shifting toward organic and locally grown fruits and vegetables. Countries like China, India, and Thailand have seen a surge in greenhouse-based cultivation of high-value crops such as tomatoes, cucumbers, bell peppers, and strawberries.

Besides, government-backed initiatives aimed at improving food security are encouraging farmers to adopt greenhouse technology. In India, the National Horticulture Board reports that over 200,000 hectares of farmland have been converted to protected cultivation since 2020, primarily for vegetable production. Similarly, in Japan, vertical farms integrated with greenhouse systems are supplying urban centers with fresh produce, reducing dependency on imports.

The ability of greenhouse farming to extend growing seasons and protect crops from extreme weather events further reinforces its importance in ensuring stable fruit and vegetable supplies. These factors collectively sustain the dominance of this segment in the regional market.

Flowers & Ornamentals

Flowers & Ornamentals are projected to witness the highest CAGR of 10.2% in the Asia Pacific greenhouse equipment market. This rapid expansion is driven by the rising demand for decorative plants, cut flowers, and exotic foliage in both domestic and international markets.

Countries like Thailand, Malaysia, and Indonesia have emerged as key exporters of ornamental plants, leveraging favorable climatic conditions and advanced greenhouse technology to boost production.

Moreover, the growing popularity of indoor gardening and home décor trends in urban centers like Singapore, South Korea, and Australia has stimulated demand for high-quality ornamental plants. In response, commercial growers are investing in automated irrigation, LED grow lights, and climate monitoring systems to improve yield consistency and aesthetic quality.

Also, floriculture cooperatives in India’s Karnataka and Tamil Nadu states have adopted greenhouse-based rose and jasmine cultivation, leading to higher export volumes to Europe and the Middle East. As per the International Trade Centre (ITC), India’s floriculture exports grew by 18% in 2023, largely attributed to improved greenhouse infrastructure. These dynamics are propelling the segment’s robust growth trajectory.

COUNTRY ANALYSIS ANALYSIS

China

China prevailed in the Asia Pacific greenhouse equipment market, contributing 28.5% of total regional revenue in 2024. As the world’s most populous country with vast agricultural needs, China has prioritized greenhouse farming to enhance food security and meet rising domestic demand for fresh produce.

According to the Chinese Academy of Agricultural Sciences (CAAS), the country’s greenhouse area expanded to over 13,000 square miles, making it the global leader in greenhouse cultivation.

Furthermore, technological advancements in controlled-environment agriculture, particularly in provinces like Shandong and Hebei, have led to the development of large-scale commercial greenhouses equipped with IoT-enabled monitoring systems. These innovations support high-yield, resource-efficient farming practices, reinforcing China’s dominant position in the regional greenhouse equipment market.

India

India is emerging as one of the fastest-growing segments in recent years. The country’s expanding middle class, coupled with government incentives, has spurred interest in greenhouse-based farming among small and medium-scale farmers.

The Indian government has actively promoted greenhouse adoption through schemes such as the National Horticulture Mission (NHM) and Rashtriya Krishi Vikas Yojana (RKVY), offering subsidies covering up to 75% of capital costs for polyhouse construction.

Besides, private sector participation has intensified, with companies like Jain Irrigation Systems and Netafim India introducing cost-effective greenhouse kits tailored for local conditions. States like Maharashtra, Punjab, and Haryana have witnessed a surge in greenhouse farming, particularly for high-value crops such as capsicum, cucumber, and exotic tomatoes.

Japan

Japan is distinguished by its focus on high-tech, precision-driven greenhouse farming. The Japanese government supports greenhouse expansion through policies promoting urban farming and digital agriculture. In Tokyo and Osaka, vertical farms integrated with glass greenhouses are increasingly common, utilizing LED grow lights and automated nutrient delivery systems to maximize output in limited spaces.

Moreover, companies like Fujitsu and Panasonic have entered the agritech space, developing AI-driven climate control systems that optimize temperature, humidity, and CO₂ levels for maximum plant growth. These technological advancements position Japan as a leader in next-generation greenhouse solutions within the Asia Pacific region.

Australia

Australia contributes a notable share to the Asia Pacific greenhouse equipment market, driven by a strong emphasis on sustainable agriculture and commercial greenhouse operations.

The country’s arid climate and limited arable land have necessitated the adoption of climate-controlled greenhouses equipped with hydroponic and aquaponic systems.

Besides, the government has launched initiatives such as the Smart Farms Program to encourage greenhouse-based agriculture. Private companies like AustCherry and Snowy Hydro are investing in high-tech greenhouse complexes that integrate renewable energy and automated harvesting. These efforts reflect Australia’s strategic shift toward resource-efficient, high-yield farming models.

South Korea

South Korea is characterized by its early adoption of digital technologies in greenhouse operations. The country’s Ministry of Agriculture, Food and Rural Affairs (MAFRA) has been instrumental in promoting smart greenhouse systems that incorporate artificial intelligence, IoT-based monitoring, and autonomous climate control.

Moreover, South Korean conglomerates such as LG and Samsung have developed proprietary software platforms that enable real-time crop monitoring and remote adjustments to irrigation and lighting. This convergence of technology and agriculture positions South Korea as a key player in the evolving greenhouse equipment landscape.

KEY MARKET PLAYERS

Richel Group SA, Argus Control Systems Ltd, Certhon, Logiqs B.V, Lumigrow, Inc, Agra Tech, Inc, Rough Brothers, Inc, Nexus Corporation, Hort Americas, LLC, Heliospectra AB. These are the market players that are dominating the Asia Pacific greenhouse equipment market.

Top Players In the Market

Netafim India

Netafim, a global leader in precision irrigation and greenhouse solutions, has a strong presence in the Asia Pacific region through its Indian subsidiary. The company offers end-to-end greenhouse systems integrated with drip irrigation, fertigation, and climate control technologies tailored for diverse crop types. Netafim’s focus on sustainable farming practices and water-efficient solutions has made it a preferred partner for governments and agricultural cooperatives across South and Southeast Asia.

Lumigro (A part of Signify N.V.)

Lumigro specializes in horticultural LED lighting solutions that enhance plant growth in controlled-environment greenhouses. As a division of Signify, Lumigro plays a pivotal role in advancing indoor farming by providing customized light recipes that optimize photosynthesis and yield quality. In the Asia Pacific market, Lumigro collaborates with agritech firms and research institutions to support vertical farming and greenhouse-based cultivation in urban settings.

Jain Irrigation Systems Ltd. (JISL)

Jain Irrigation Systems is a leading Indian agri-tech company offering comprehensive greenhouse equipment packages, including structures, irrigation systems, sensors, and automation tools. Known for its farmer-centric approach, JISL provides scalable and affordable greenhouse solutions suited for small- and medium-scale farmers. The company also promotes training and financing models that facilitate wider adoption of greenhouse technology across rural communities in Asia.

Top Strategies Used By Key Market Participants

Localized Product Development and Customization

Key players are focusing on designing greenhouse equipment tailored to regional climatic conditions, soil types, and crop preferences. This strategy allows manufacturers to offer cost-effective and efficient solutions that align with local farming practices, enhancing adoption among diverse user groups across the Asia Pacific region.

Partnerships with Government and Research Institutions

Collaborating with government bodies and agricultural universities helps companies gain insights into policy directions, receive funding support, and pilot innovative technologies. These partnerships also assist in promoting greenhouse farming through demonstration projects and capacity-building programs.

Integration of Smart Technologies and Digital Platforms

To meet the growing demand for precision agriculture, leading firms are embedding IoT-enabled sensors, automated climate controls, and data analytics platforms into greenhouse systems. This digital transformation enables real-time monitoring and decision-making, improving productivity and resource efficiency for commercial growers.

COMPETITION OVERVIEW

The competition in the Asia Pacific Greenhouse Equipment Market is intensifying as both global and regional players strive to capture a larger share of a rapidly evolving industry. The market is characterized by a mix of established multinational corporations and agile local enterprises, each leveraging distinct strengths to gain a competitive edge. Multinational firms bring advanced technologies, extensive R&D capabilities, and global expertise, while domestic players emphasize affordability, localized service networks, and a deep understanding of regional farming dynamics.

Innovation remains a key battleground, with companies investing heavily in smart greenhouse systems, energy-efficient climate control mechanisms, and integrated digital platforms that enable remote monitoring and automation. Besides, strategic collaborations with governments and agricultural institutions are becoming common, helping firms align their offerings with national food security initiatives and subsidy-driven adoption programs.

Market participants are also expanding their distribution channels and after-sales support infrastructure to ensure seamless installation and maintenance services, particularly in rural areas where technical assistance is limited. As consumer awareness grows and regulatory support strengthens, competition is expected to shift further toward sustainability, scalability, and ease of integration, making differentiation increasingly dependent on technological advancement and customer engagement strategies.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Jain Irrigation Systems launched an exclusive line of modular greenhouse kits designed for smallholder farmers in Southeast Asia. These pre-engineered structures aimed at simplifying installation and reducing initial investment barriers, making greenhouse farming more accessible in rural areas.

- In May 2024, Netafim India announced a partnership with a major Indian state agricultural university to establish demonstration greenhouses across several districts. The initiative focused on training farmers in modern greenhouse techniques and promoting the benefits of protected cultivation.

- In August 2023, Lumigro introduced a new range of tunable LED grow lights specifically adapted for tropical greenhouse environments. The product was developed in collaboration with agronomists to optimize light spectra for high-yield vegetable and herb cultivation in hot and humid conditions.

- In November 2023, a leading Chinese greenhouse equipment manufacturer expanded its manufacturing facility in Guangdong province to increase production capacity for climate control systems. The expansion aimed to cater to rising domestic and export demand from neighboring Asian countries.

- In January 2024, a prominent Australian agritech firm collaborated with a solar energy provider to develop an off-grid greenhouse model powered entirely by renewable energy. The solution targeted remote and island communities seeking sustainable food production alternatives.

MARKET SEGMENTATION

This research report on the Asia Pacific greenhouse equipment market is segmented and sub-segmented into the following categories.

By Equipment

- Heating Systems

- Cooling Systems

- Others

By Greenhouse Type

- Glass Greenhouse

- Horticulture Glass

- And Other Greenhouse Glass

- Plastic Greenhouse

- Polyethylene

- Polycarbonate

- Polymethyl Methacrylate (PMMA)

By Crop Type

- Fruits & Vegetables

- Flowers & Ornamentals

- Nursery Crops

- Other Crop Types

COUNTRY ANALYSIS

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is driving the growth of the greenhouse equipment market in the Asia Pacific region?

The Asia Pacific greenhouse equipment market is growing due to increasing food demand, rapid urbanization, and limited arable land in many countries. Governments across the region are promoting controlled environment agriculture (CEA) to improve crop yields and ensure food security. Additionally, rising awareness about sustainable farming practices, coupled with advancements in technology like smart greenhouses and IoT-enabled systems, is accelerating adoption.

Which countries are leading the adoption of greenhouse equipment in Asia Pacific?

China leads the market in terms of volume due to large-scale government-backed agricultural modernization programs. India is also emerging rapidly, driven by private sector investments and subsidies for farmers adopting protected cultivation. Japan and South Korea focus on high-tech, climate-controlled greenhouses, while Australia and New Zealand emphasize precision horticulture and export-oriented farming.

How do climatic conditions influence the need for greenhouse equipment in this region?

The Asia Pacific region experiences diverse and often extreme weather patterns, including monsoons, typhoons, droughts, and heatwaves. These conditions make open-field farming increasingly unpredictable. Greenhouse structures provide a controlled environment that protects crops from adverse weather, pests, and diseases, making them an attractive solution for stable year-round production.

What types of greenhouse structures are most commonly used in Asia Pacific?

In this region, both polyhouse structures and glass greenhouses are widely used. Polyhouses are more common in countries like India and Indonesia due to their lower cost and ease of installation. Glass and semi-glass greenhouses are gaining traction in wealthier markets such as Japan and South Korea, where there’s a preference for advanced climate control and integration with automation.

How important is automation and technology in the APAC greenhouse equipment market?

Automation is becoming increasingly important, especially in developed markets like Japan and Singapore, where labor costs are high. Technologies such as automated irrigation, climate control systems, LED grow lights, and remote monitoring via mobile apps are being adopted to enhance efficiency, reduce manual labor, and optimize resource use like water and energy.

Are smallholder farmers in the region adopting greenhouse equipment?

While initial adoption was concentrated among large commercial farms, efforts by governments and NGOs to promote greenhouse farming through subsidies, training programs, and financing schemes are enabling smallholder farmers to participate. In countries like Thailand, Vietnam, and the Philippines, cooperative farming models are helping smaller growers access greenhouse technologies collectively.

What role does sustainability play in the greenhouse equipment market in Asia Pacific?

Sustainability is a key consideration. Many greenhouse systems now incorporate solar-powered ventilation, rainwater harvesting, and organic pest control methods. There's also a shift toward biodegradable materials and energy-efficient lighting solutions. Consumers and regulators alike are pushing for greener agricultural practices, which is influencing equipment design and usage.

What challenges are faced by the greenhouse equipment industry in Asia Pacific?

High initial investment remains a major barrier, especially for small-scale farmers. Lack of technical knowledge, limited after-sales support in rural areas, and inconsistent electricity supply in some regions also pose challenges. However, increasing partnerships between local manufacturers and international suppliers are helping to address these issues through localized service networks and affordable packages.

How is the market responding to the rise in vertical farming and indoor agriculture?

With the rise of urban farming and space constraints in densely populated cities like Tokyo, Seoul, and Singapore, there’s growing interest in integrating greenhouse equipment into vertical farming setups. Modular greenhouse designs, retractable roofs, and compact hydroponic systems are being developed to suit these new-age farming models.

Who are the key players in the Asia Pacific greenhouse equipment market?

Major global players like Netafim , Ridder Group , and Lumigrow have a presence in the region, particularly in high-tech segments. However, local manufacturers and startups are gaining momentum by offering cost-effective, region-specific solutions. Companies based in China and India are playing a growing role in supplying affordable polyhouse kits and modular structures tailored for small to medium-sized farms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com