Asia Pacific Heat Meters Market Research Report – Segmented By Type-((Mechanical) (Multi-Jet Meters, Turbine Meters)),Type, Connectivity End-User, Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC) - Industry Analysis From 2025 to 2033

Asia Pacific Heat Meters Market Size

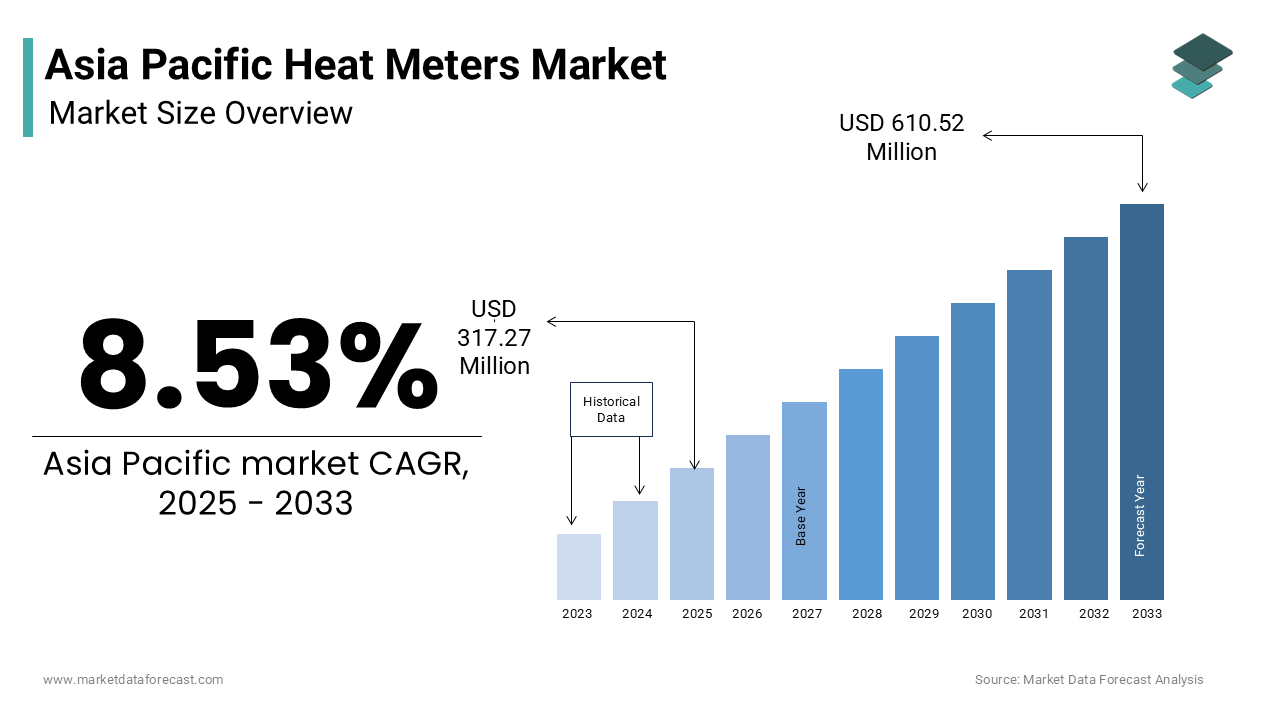

The Asia Pacific Heat Meters Market was worth USD 292.28 million in 2024. The Asia Pacific market is expected to reach USD 610.52 million by 2033 from USD 317.27 million in 2025, rising at a CAGR of 8.53% from 2025 to 2033.

The Asia Pacific heat meters market is an integral segment of the broader energy management and smart infrastructure landscape, designed to measure the thermal energy consumed in heating systems. Heat meters are sophisticated devices that monitor and quantify energy usage in district heating, industrial applications, and residential complexes, enabling efficient energy distribution and cost management. The region’s growing urbanization and increasing emphasis on sustainable energy solutions have positioned heat meters as a critical tool for optimizing resource utilization.

MARKET DRIVERS

Growing Urbanization and Smart City Initiatives

The rapid pace of urbanization in the Asia Pacific region is one of the primary drivers propelling the heat meters market. As cities expand and populations grow, there is an increasing need for efficient energy management systems to support heating infrastructure in residential, commercial, and industrial sectors. Heat meters play a crucial role in monitoring energy consumption in district heating systems, which are widely used in densely populated urban centers. For example, in South Korea, the government’s Smart City Initiative has prioritized the deployment of energy-efficient technologies, including heat meters, to optimize resource utilization and reduce carbon emissions. Similarly, in India, the Smart Cities Mission aims to integrate smart grid technologies into urban infrastructure, fostering the adoption of heat meters in heating applications.

Stringent Energy Efficiency Regulations

Another significant driver of the heat meters market in the Asia Pacific is the implementation of stringent energy efficiency regulations aimed at reducing energy wastage and promoting sustainable practices. Governments across the region have introduced policies to encourage the adoption of smart metering technologies in heating systems. Heat meters enable accurate measurement of thermal energy consumption, allowing for better monitoring and control of energy usage. This aligns with regional initiatives such as Japan’s Green Growth Strategy, which emphasizes the transition to low-carbon technologies. Furthermore, the increasing focus on circular economy principles has encouraged businesses to adopt resource-efficient processes like heat metering, which minimize energy losses.

MARKET RESTRAINTS

High Initial Investment Costs

One of the most significant restraints hindering the growth of the Asia Pacific heat meters market is the high initial investment required for procurement and installation. Heat meters are sophisticated devices that incorporate advanced technologies such as ultrasonic and electromagnetic sensors, making them expensive compared to traditional energy measurement tools. Like, small and medium-sized enterprises (SMEs) in the construction and real estate sectors often face financial constraints, limiting their ability to adopt capital-intensive solutions. For instance, businesses operating in emerging economies like Vietnam and Indonesia may find it challenging to justify the upfront costs associated with retrofitting existing heating systems with heat meters. Also, the operational expenses related to maintenance and calibration further exacerbate the financial burden. While modern heat meters are designed to be durable and accurate, the initial outlay remains a deterrent for many organizations, particularly smaller players.

Lack of Awareness and Technical Expertise

Another major restraint is the lack of awareness and technical expertise regarding the optimal use of heat meters among end-users. Many stakeholders, particularly in rural or semi-urban areas, remain unfamiliar with the benefits of advanced metering technologies and their role in enhancing energy efficiency. In countries like Bangladesh and Myanmar, where traditional methods of energy measurement are still prevalent, the adoption of heat meters is hindered by a lack of understanding about their functionality and advantages. Moreover, the absence of skilled personnel trained in operating and maintaining these systems further complicates the issue. This knowledge deficit not only limits the effective utilization of heat meters but also increases the risk of operational inefficiencies.

MARKET OPPORTUNITIES

Expansion of District Heating Systems

The expansion of district heating systems presents a lucrative opportunity for the Asia Pacific heat meters market. District heating, which involves centralized production and distribution of thermal energy, is gaining traction in the region due to its ability to provide cost-effective and sustainable heating solutions. Heat meters play a pivotal role in this context by enabling accurate measurement and billing of energy consumption, ensuring transparency and accountability. Similarly, in countries like South Korea and Japan, the push for renewable energy integration has amplified the need for advanced metering solutions to monitor and optimize district heating operations.

Integration with Smart Grid Technologies

Another promising opportunity lies in the integration of heat meters with smart grid technologies, which are increasingly being adopted across the Asia Pacific region. Smart grids leverage digital communication and IoT-enabled devices to enhance the efficiency, reliability, and sustainability of energy distribution systems. For example, in Australia, the rollout of smart grid infrastructure has spurred the adoption of advanced metering solutions to monitor and manage energy usage in heating applications. Similarly, in India, the government’s Smart Grid Vision Plan emphasizes the importance of integrating smart meters into energy networks, offering new avenues for heat meter manufacturers.

MARKET CHALLENGES

Energy Consumption Concerns

A significant challenge facing the Asia Pacific heat meters market is the concern over energy consumption and its environmental impact. Heat meters rely on a continuous power supply to function effectively, which can strain energy grids, especially in regions with limited resources. Moreover, the environmental implications of high energy usage cannot be overlooked. As per the United Nations Environment Programme, the carbon footprint of industrial processes is a growing concern, prompting calls for more sustainable alternatives. While manufacturers are working to develop energy-efficient models, the current generation of heat meters still poses a challenge in terms of balancing performance with environmental responsibility.

Logistical Barriers in Remote Areas

Another pressing challenge is the logistical difficulty of deploying heat meters in remote and underdeveloped areas. The Asia Pacific region is characterized by diverse geographical landscapes, ranging from densely populated urban centers to vast rural expanses with limited infrastructure. This disparity creates significant barriers to the widespread adoption of heat meters, particularly in agricultural communities that could benefit from their use. For example, in Papua New Guinea, where road connectivity is limited, transporting and installing heavy equipment like heat meters becomes a daunting task. Similarly, in parts of Nepal and Bhutan, the lack of a stable power supply hinders the effective operation of these systems. Even when heat meters are successfully deployed, maintaining them in such environments poses additional challenges. Also, the cost of servicing and repairing equipment in remote locations can be up to three times higher than in urban areas, further deterring businesses from investing in these technologies.

SEGMENTAL ANALYSIS

By Type(Mechanical) Insights

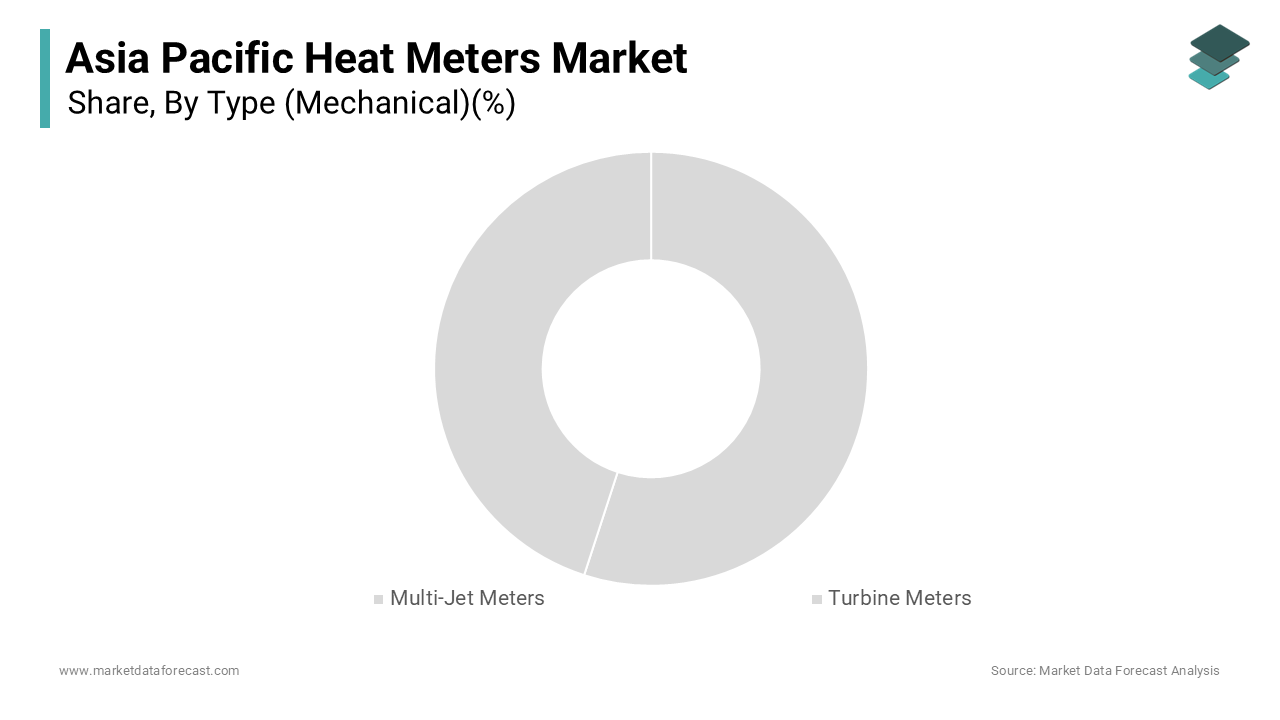

The Multi-jet meters segment commanded the mechanical heat meters segment in the Asia Pacific market by capturing 60.8% of the total market share in 2024. This dominance is driven by their reliability and cost-effectiveness, making them a preferred choice for residential and small-scale commercial applications. According to the International Water Association, multi-jet meters are widely adopted due to their ability to provide accurate measurements even at low flow rates, which is critical for heating systems in densely populated urban areas. A key factor behind their prominence is their robust design, which ensures durability and minimal maintenance requirements. Another driving factor is the growing emphasis on retrofitting existing heating infrastructure with advanced metering solutions. Multi-jet meters, with their compatibility with older systems and ease of installation, are well-suited for such projects.

The turbine meters segment is emerging as the fastest-growing in the mechanical heat meters market, with a projected CAGR of 8.5%. This rapid surge is fueled by their suitability for large-scale industrial and district heating applications, where high flow rates and precision are paramount. Another significant factor propelling the growth of turbine meters is their integration with smart grid technologies. Turbine meters, equipped with IoT-enabled features, align perfectly with this trend by enabling real-time monitoring and data analytics. This technology is particularly beneficial in countries like Japan and South Korea, where precision and efficiency are critical to industrial operations. Additionally, advancements in materials and design have improved the accuracy and lifespan of turbine meters.

By Type Insights

Electromagnetic meters dominate the static heat meters segment in the Asia Pacific market, accounting for 55% of the total market share. Their leadership is attributed to their high accuracy, reliability, and ability to handle a wide range of flow conditions, making them ideal for both residential and industrial applications. According to the International Society of Automation, electromagnetic meters are widely used in district heating systems due to their non-intrusive design and resistance to impurities in water, which ensures long-term performance. Another key factor contributing to their dominance is the increasing focus on sustainability and energy conservation. Electromagnetic meters play a crucial role in optimizing energy usage by providing precise measurements, aligning with regional initiatives to achieve carbon neutrality. Also, their compatibility with smart grid technologies enhances their appeal.

Ultrasonic meters are the rapidly advancing segment in the static heat meters market, with a CAGR of 9.2%. This growth is driven by their ability to provide highly accurate measurements without requiring physical contact with the fluid, making them ideal for applications where hygiene and minimal maintenance are critical. For example, in Japan, the adoption of ultrasonic meters has surged due to their ability to meet stringent quality standards and support renewable energy integration. Another significant factor is the growing emphasis on digital transformation in the energy sector. Ultrasonic meters, equipped with advanced sensors and data analytics capabilities, align perfectly with this trend by enabling predictive maintenance and energy optimization. This technology is particularly beneficial in countries like Australia and Singapore, where smart city initiatives are driving the adoption of cutting-edge solutions. Additionally, advancements in ultrasonic technology have improved their affordability and scalability, making them accessible to a wider range of applications.

By Connectivity Insights

Wired meters dominated the connectivity segment of the Asia Pacific heat meters market by capturing 65.5% of the total market share. Their leadership is driven by their reliability and cost-effectiveness, particularly in regions with stable power grids and established infrastructure. Another key factor contributing to their dominance is the widespread availability of wired infrastructure in urban areas. Wired meters, with their proven track record and compatibility with existing systems, remain the preferred choice for many stakeholders. Additionally, their lower initial costs compared to wireless alternatives make them accessible to smaller players, further strengthening their place in the connectivity segment.

Wireless meters are the fastest-rising segment in the connectivity category of the Asia Pacific heat meters market, with a CAGR of 10.5%. This progress is fueled by their ability to provide flexible and scalable solutions, particularly in remote or underserved areas where wired infrastructure is limited. Another significant factor is the growing emphasis on smart grid technologies and digital transformation. This technology is particularly beneficial in countries like Australia and India, where smart city initiatives are driving the adoption of advanced metering solutions. Also, advancements in wireless communication technologies, such as 5G, have improved the reliability and speed of data transmission, further enhancing their appeal.

By End-User Insights

The residential sector represented the largest end-user segment in the Asia Pacific heat meters market by accounting for 45.1% of the total market share in 2024. This dominance is driven by the growing urbanization and increasing adoption of district heating systems in residential complexes. Heat meters play a pivotal role in this context by enabling accurate measurement and billing of energy consumption, ensuring transparency and accountability. Another key factor contributing to the segment’s growth is the implementation of government policies aimed at promoting energy conservation. Similarly, in India, the Smart Cities Mission emphasizes the importance of integrating advanced metering technologies into urban infrastructure, fostering the adoption of heat meters in residential applications.

The industrial sector is the quickest expanding end-user segment in the Asia Pacific heat meters market, with a CAGR of 11.2%. This development is caused by the increasing demand for energy-efficient solutions in manufacturing and processing industries, where thermal energy consumption is a significant cost factor. Another significant factor is the growing emphasis on sustainability and regulatory compliance. Additionally, advancements in heat meter technology, such as IoT-enabled features, have enhanced their appeal in industrial applications by enabling real-time monitoring and predictive maintenance.

REGIONAL ANALYSIS

China stood as the largest contributor to the Asia Pacific heat meters market by commanding a 35.5% market share in 2024. The country’s dominance is underpinned by its extensive use of district heating systems, which are integral to its urban infrastructure. Heat meters play a critical role in this context by enabling accurate measurement and billing of energy consumption, ensuring transparency and accountability. In addition, the government’s push for smart city development has spurred the adoption of advanced metering solutions.

Japan remains a significant player in the market. The country’s position is bolstered by its advanced industrial and residential sectors, which rely heavily on precise energy management solutions. The government’s Green Growth Strategy emphasizes the importance of integrating advanced technologies to reduce carbon emissions, making heat meters indispensable. Also, Japan’s expertise in smart grid technologies has enabled seamless integration of heat meters with IoT platforms, enhancing their functionality and appeal.

South Korea accounts for a key share of the Asia Pacific heat meters market and is supported by its thriving industrial and residential sectors. Apart from these, South Korea’s focus on smart city initiatives has fostered the adoption of IoT-enabled heat meters, which provide real-time monitoring and predictive maintenance capabilities.

India holds a considerable market share in the Asia Pacific heat meters market and is driven by its rapidly expanding urban infrastructure and government initiatives to promote energy efficiency. Heat meters play a crucial role in ensuring transparency and accountability in energy billing, aligning with the country’s energy-saving targets. In addition, the growing emphasis on renewable energy integration has amplified the need for accurate and reliable metering solutions, further boosting the adoption of heat meters in India.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Siemens AG, Danfoss A/S, Kamstrup A/S, Diehl Stiftung & Co. KG, Landis+Gyr AG, Itron Inc., Wasion Group Holdings Limited, Zenner International GmbH & Co. KG, Apator S.A., and Secure Meters Ltd are some of the key market players.

The Asia Pacific heat meters market is characterized by intense competition, driven by the presence of established global brands and emerging regional players. Companies are vying for market leadership by leveraging their technological expertise, extensive distribution networks, and customer-centric strategies. The competitive landscape is shaped by rapid advancements in metering technologies, increasing demand for energy-efficient solutions, and stringent regulatory frameworks. To maintain their edge, key players are continuously innovating and expanding their product portfolios to cater to diverse applications across residential, commercial, and industrial sectors. Additionally, the growing emphasis on sustainability and digital transformation has prompted companies to adopt smart features and green technologies. Strategic initiatives such as mergers, acquisitions, and partnerships are prevalent, enabling players to consolidate their positions and tap into new opportunities.

Top Players in the Asia Pacific Heat Meters Market

Kamstrup A/S

Kamstrup A/S is a global leader in the heat meters market, renowned for its innovative and reliable metering solutions tailored to both residential and industrial applications. The company’s advanced ultrasonic and smart heat meters have set industry benchmarks for accuracy and efficiency. Kamstrup’s commitment to sustainability is evident in its development of energy-efficient products that align with global environmental standards. By leveraging IoT-enabled technologies, Kamstrup provides real-time monitoring and predictive maintenance capabilities, enhancing the user experience. Its strong presence in the Asia Pacific region is reinforced by strategic partnerships with local distributors and governments, ensuring widespread adoption of its solutions.

Diehl Metering

Diehl Metering is a prominent player in the Asia Pacific heat meters market, offering cutting-edge solutions for district heating, industrial, and residential applications. The company’s electromagnetic and ultrasonic heat meters are widely recognized for their precision and durability, making them a preferred choice for energy management systems. Diehl Metering’s focus on digital transformation is reflected in its integration of smart grid technologies, enabling seamless data analytics and remote monitoring. By prioritizing sustainability and energy conservation, the company aligns with regional initiatives to reduce carbon emissions. Its robust distribution network and localized manufacturing capabilities ensure timely delivery and superior customer support.

Itron Inc.

Itron Inc. is a key contributor to the Asia Pacific heat meters market, known for its high-performance and scalable metering solutions. The company specializes in advanced heat meters that cater to diverse applications, including smart city projects and industrial energy management. Itron’s focus on delivering customizable and eco-friendly solutions has enabled it to establish a strong foothold in the region. By integrating IoT platforms and data analytics into its products, Itron enhances operational efficiency and supports sustainable energy practices. Its ability to adapt to evolving market needs ensures its continued leadership in the heat meters industry.

Top Strategies Used by Key Market Participants

Investment in Research and Development

Key players in the Asia Pacific heat meters market are heavily investing in research and development to introduce innovative products that meet evolving consumer demands. By focusing on advancements such as ultrasonic technology, IoT-enabled features, and predictive maintenance capabilities, companies aim to enhance the accuracy and functionality of their heat meters. These innovations not only improve user experience but also align with global sustainability goals, appealing to environmentally conscious customers. Additionally, R&D efforts enable manufacturers to develop cost-effective solutions that cater to diverse applications, from residential complexes to industrial facilities. This focus on innovation ensures that companies remain competitive while addressing emerging trends in the energy management sector.

Strategic Partnerships and Collaborations

Strategic partnerships and collaborations are pivotal strategies used by market players to expand their reach and enhance their offerings. Companies are teaming up with local governments, utility providers, and technology firms to strengthen supply chains and improve market penetration. These alliances enable players to leverage complementary strengths, access new customer bases, and address logistical challenges. For instance, collaborations with regional energy authorities help companies develop tailored solutions for district heating networks.

Expansion of Manufacturing and Distribution Networks

Expanding manufacturing and distribution networks is another key strategy adopted by leading players to strengthen their market position. By establishing production facilities in strategic locations across the region, companies can reduce costs, improve supply chain efficiency, and better serve local markets. Localized manufacturing also allows for greater customization and quicker response to customer needs, enhancing brand loyalty. Additionally, expanding distribution networks ensures wider availability of products, particularly in remote and underserved areas. This approach not only boosts sales but also reinforces the company’s reputation as a reliable and accessible provider of heat metering solutions.

REGIONAL ANALYSIS

- In February 2023, Kamstrup A/S launched a new line of IoT-enabled heat meters designed for smart city projects across Southeast Asia. This move aimed to support urban infrastructure development while enhancing the company’s reputation as a leader in smart energy solutions.

- In June 2023, Diehl Metering announced a partnership with a leading utility provider in Japan to integrate advanced heat meters into district heating networks. This collaboration focused on optimizing energy usage and reducing carbon emissions through real-time monitoring.

- In September 2023, Itron Inc. expanded its manufacturing facility in India to meet the rising demand for residential heat meters. This expansion underscored the company’s commitment to supporting regional energy conservation initiatives.

- In November 2023, Zenner International acquired a mid-sized distributor in Indonesia to strengthen its distribution network across the Asia Pacific region. This acquisition enabled Zenner to improve market access and enhance customer service in emerging markets.

- In March 2024, Landis+Gyr introduced a modular heat meter system tailored for industrial applications in Vietnam. This initiative addressed the growing.

MARKET SEGMENTATION

This research report on the Asia Pacific heat meters market is segmented and sub-segmented into the following categories.

By Type(Mechanical)

- Multi-Jet Meters

- Turbine Meters

By Type

- Electromagnetic Meters

- Ultrasonic Meters

By Connectivity

- Wired Connection

- Wireless Connection

By End-User

- Residential

- Commercial & Public

- Industrial

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What drives the growth of the Asia Pacific heat meters market?

The market is driven by increasing demand for energy efficiency, rapid urbanization, growing district heating systems, and government initiatives promoting smart metering infrastructure.

What are the major challenges facing this market?

Challenges include high initial installation costs, retrofit difficulties in older buildings, and lack of awareness or regulation in some developing regions.

What is the future outlook of the Asia Pacific heat meters market?

The market is expected to witness substantial growth due to expanding urban infrastructure, rising investments in smart energy systems, and increasing focus on carbon emission reduction through efficient energy use.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]