Asia Pacific High Purity Alumina Market Size, Share, Growth, Trends, And Forecasts Research Report, Segmented By Product, Application And By Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From 2026 to 2034

Market Size, 2025

$1.46 BnMarket Estimate, 2026

$1.81 BnMarket Forecast, 2034

$10.08 BnCAGR, 2026–2034

23.95%Executive Summary: Asia Pacific High Purity Alumina Market

- Market Scope: Comprehensive regional high purity alumina (HPA) market analysis covering purity grades, application sectors, country-specific leadership frameworks, and key strategic developments.

- Market Valuation: Valued at USD 1.46 billion (2025), estimated at USD 1.81 billion (2026), and projected to reach USD 10.08 billion by 2034, registering a robust CAGR of 23.95% (2026–2034).

- Primary Growth Drivers: Rapid expansion of LED lighting and display technologies, surging demand for high-performance lithium-ion batteries in electric vehicles, and synthetic sapphire applications. Opportunities include solid-state battery electrolytes, 6N purity quantum computing components, and alumina-coated separators.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Purity Grade & Application | 4N HPA segment (held 52.3% share for LEDs/ceramics); LED segment (held largest share at 41.2%) | 6N HPA segment (CAGR of 14.8% for semiconductors/quantum tech); Li-ion battery segment (fastest application CAGR of 17.3%) |

| By Region / Country | China (led regional market with a dominant 38.4% share in 2025 via electronics manufacturing and EV production) | Advanced Asian technology hubs expanding high-purity material production and battery component supply chains |

Major Market Players & Market Structure

Market Structure: Highly competitive Asia-Pacific high purity alumina landscape featuring global chemical manufacturers and specialty producers competing intensely on production line expansions, long-term supply agreements, and joint ventures for coated battery separators.

Key Companies: Almatis, Inc., Altech Chemicals Ltd., Alpha HPA, Baikowski, CoorsTek Inc., FYI RESOURCES, HONGHE CHEMICAL, Shandong Aluminium Industry Science & Technology Co., Ltd., Sasol Limited, Nippon Light Metal Holdings Co., Ltd., Orbite Technologies Inc., Polar Sapphire Ltd., and Sumitomo Chemical Co., Ltd.

Asia Pacific High Purity Alumina Market Size

The Asia Pacific high-purity alumina market size was valued at USD 1.46 billion in 2025 and is anticipated to reach a valuation of USD 1.81 billion in 2026 and USD 10.08 billion by 2034, growing at a CAGR of 23.95%, from 2026 to 2034.

High purity alumina (HPA), defined as aluminum oxide with a purity level exceeding 99.99%, is a critical material used in various high-technology applications, including LED manufacturing, semiconductor substrates, lithium-ion batteries, and synthetic sapphire production. The Asia Pacific region has emerged as a dominant force in the global HPA market due to its robust electronics industry, increasing investments in clean energy technologies, and expanding industrial infrastructure.

MARKET DRIVERS

Growth in LED Lighting and Display Technologies

One of the primary drivers of the Asia Pacific high-purity alumina market is the rapid expansion of LED lighting and display technologies. High-purity alumina serves as a crucial raw material in the production of sapphire substrates used in light-emitting diodes (LEDs). These substrates are essential for manufacturing energy-efficient lighting solutions and high-resolution displays used in smartphones, televisions, and automotive lighting systems.

According to the Japan Electronics and Information Technology Industries Association, the production of LED components in Japan alone increased by 14% in 2023 compared to the previous year, largely supported by domestic HPA supply chains. In South Korea, companies like Samsung and LG continue to invest heavily in OLED technology, which relies on sapphire-based components derived from high-purity alumina. As per the Korea Semiconductor Industry Association, over 30 new display manufacturing lines were commissioned in 2023, significantly boosting HPA demand.

Expansion of the Lithium-Ion Battery Industry

The growing lithium-ion battery industry is another significant driver of the Asia Pacific high-purity alumina market. High-purity alumina plays a vital role in battery manufacturing, particularly as a coating material for separators and electrodes, where it enhances thermal stability, prevents short circuits, and improves overall battery safety. A substantial portion of this output utilized high-purity alumina-coated separators to meet international safety standards. According to the China Chemical Industry Association, HPA consumption in the battery sector grew by approximately 18% year-over-year. Similarly, in Japan, major battery manufacturers such as Panasonic and GS Yuasa have integrated high-purity alumina into their cell designs to enhance performance and longevity.

MARKET RESTRAINTS

Complex and Cost-Intensive Production Processes

One of the primary restraints affecting the Asia Pacific high-purity alumina market is the complexity and high cost associated with its production. Unlike conventional alumina, high-purity alumina requires highly specialized refining techniques such as the ammonium aluminum carbonate hydroxide (AACH) process or the sulfate route, which involve multiple purification steps to achieve ultra-low impurity levels. These processes demand significant capital investment in advanced equipment, stringent quality control measures, and skilled labor.

According to the Australian Mineral Foundation, the production cost of high-purity alumina can be up to three times higher than that of standard metallurgical-grade alumina. In countries like India and Thailand, where access to high-purity raw materials and refining expertise is limited, local manufacturers face challenges in scaling production efficiently. Additionally, the Japanese Industrial Standards Committee noted that maintaining consistent product quality across batches remains a persistent issue, requiring continuous process optimization. These technical and financial barriers limit the number of viable producers in the region and hinder smaller players from entering the market. As a result, despite rising demand, the high entry costs and operational complexities pose a significant restraint on the broader adoption of high-purity alumina across the Asia Pacific.

Supply Chain Vulnerabilities and Raw Material Constraints

Another significant restraint in the Asia Pacific high-purity alumina market is the vulnerability of its supply chain and constraints related to raw material availability. High-purity alumina is derived from high-grade bauxite through an energy-intensive refining process, but only a small fraction of global bauxite reserves meet the required purity standards for HPA production. Countries such as China and Japan rely heavily on imported bauxite from Australia, Guinea, and Indonesia, making them susceptible to geopolitical disruptions and trade policy changes. Moreover, environmental regulations in key producing nations have led to periodic shutdowns of mining operations, further straining the supply chain. In Australia, stricter emissions norms introduced by the Department of Climate Change, Energy, the Environment, and Water in early 2023 resulted in temporary halts at several bauxite processing facilities. These supply-side pressures create uncertainty for manufacturers and hinder the steady growth of the high-purity alumina market in the Asia Pacific.

MARKET OPPORTUNITIES

Increasing Demand for Synthetic Sapphire Applications

An emerging opportunity in the Asia Pacific high-purity alumina market lies in the expanding use of synthetic sapphire for high-tech applications such as smartphone camera covers, fingerprint sensors, LED substrates, and aerospace components. Synthetic sapphire is manufactured using the Verneuil or Czochralski method, both of which require high-purity alumina as the primary raw material.

In addition, the Indian Defence Research and Development Organisation has been investing in sapphire-based armor windows and sensor covers, citing enhanced durability under extreme conditions. The demand for high-purity alumina in synthetic sapphire production is poised for substantial growth across the Asia Pacific as these industries scale up and new application areas emerge.

Integration in Solid-State Battery Technologies

The development and commercialization of solid-state batteries represent a promising opportunity for the Asia Pacific high-purity alumina market. Solid-state batteries utilize ceramic electrolytes instead of liquid ones, offering improved safety, higher energy density, and longer cycle life—attributes that are highly desirable for electric vehicles, consumer electronics, and grid-scale energy storage. High-purity alumina is a key component in the synthesis of lithium-stabilized alumina (LLZO), a ceramic electrolyte material currently being explored for next-generation battery systems.

According to the Toyota Central R&D Laboratories, Japan-based automakers are accelerating their solid-state battery R&D efforts, with pilot production scheduled to begin in late 2024. As part of this initiative, several joint ventures between battery manufacturers and material suppliers have been formed to secure a stable supply of high-purity alumina. In South Korea, the Korea Institute of Science and Technology indicated that LLZO-based electrolytes showed a 30% improvement in ionic conductivity compared to conventional polymer electrolytes. Furthermore, in China, the State Key Laboratory of Advanced Batteries has initiated multiple projects aimed at optimizing alumina-based solid electrolytes for mass production.

MARKET CHALLENGES

Technological Barriers in Alternative Material Development

A significant challenge facing the Asia Pacific high-purity alumina market is the ongoing development and adoption of alternative materials that could potentially replace HPA in key applications. Researchers and manufacturers are exploring substitutes such as yttria-stabilized zirconia, silicon carbide, and aluminum nitride, which offer comparable performance characteristics in certain high-temperature and electronic applications while being more cost-effective or easier to produce.

According to the Korea Institute of Materials Science, recent advancements in ceramic composites have enabled the partial substitution of high-purity alumina in semiconductor manufacturing and thermal barrier coatings. In Japan, the University of Tokyo’s Department of Materials Engineering reported that some next-generation LED substrates are being developed using gallium oxide, which may reduce reliance on sapphire-based structures. Companies operating in the region must continuously innovate and enhance the value proposition of high-purity alumina to maintain their relevance amid evolving material science trends.

Environmental and Regulatory Pressures on Mining and Processing

Environmental concerns and tightening regulatory frameworks surrounding mining and refining activities present a major challenge for the Asia Pacific high-purity alumina market. The extraction and processing of bauxite to produce high-purity alumina generate significant waste, including red mud and greenhouse gas emissions, prompting governments to impose stricter environmental compliance measures. These regulations increase production costs and create operational hurdles for existing and new entrants in the market.

As per the Australian Department of Climate Change, Energy, the Environment, and Water, new emission reduction targets introduced in 2023 required alumina refineries to implement carbon capture and storage technologies, adding to capital expenditures. In China, the Ministry of Ecology and Environment mandated stricter effluent discharge limits for alumina refineries, resulting in temporary plant closures and reduced output. Additionally, the Indonesian Ministry of Environment and Forestry announced tighter oversight of bauxite mining operations in environmentally sensitive regions, limiting raw material availability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 23.95% |

| Segments Covered | By Product, Application, and Region. |

|

Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Almatis, Inc., Altech Chemicals Ltd., Alpha HPA, Baikowski, CoorsTek Inc., FYI RESOURCES, HONGHE CHEMICAL, Nippon Light Metal Holdings Co., Ltd., Orbite Technologies Inc., Polar Sapphire Ltd., Sumitomo Chemical Co., Ltd |

SEGMENTAL ANALYSIS

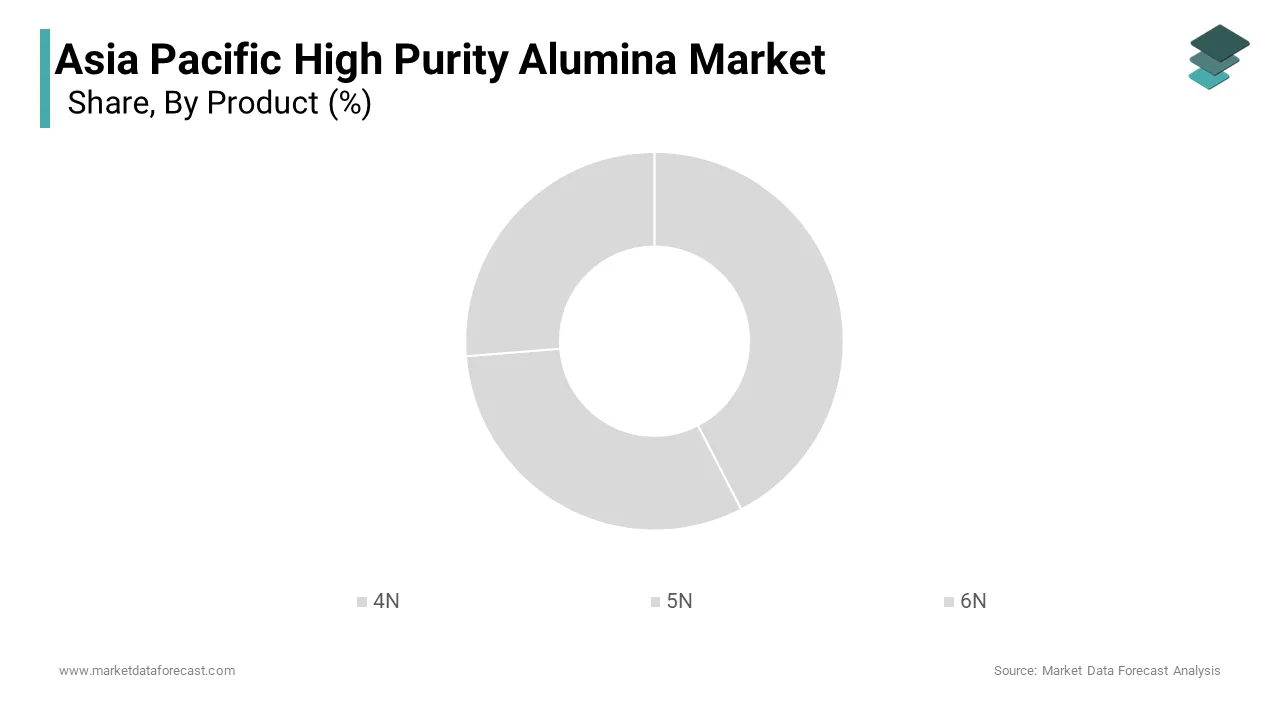

By Product Insights

The 4N high-purity alumina segment dominated the Asia Pacific market with a share of 52.3% in 2025. According to the China Nonferrous Metals Industry Association, over 60% of domestic HPA consumption in the lighting sector is attributed to 4N-grade alumina, primarily due to its compatibility with YAG (Yttrium Aluminum Garnet) phosphors used in white LEDs. In Japan, the Japan Institute of Metals reported that 4N alumina remains the preferred material for producing sintered ceramics used in industrial furnace linings and crucibles, owing to its balance between performance and cost-efficiency. In India, the Indian Institute of Minerals and Materials noted a 20% year-over-year increase in the procurement of 4N alumina for refractory applications in steel and glass manufacturing. As industries across the region seek cost-effective yet reliable materials for mid-tier technological applications, the demand for 4N high-purity alumina continues to outpace other purity grades.

The 6N high-purity alumina segment is expected to register a CAGR of 14.8% from 2025 to 2033. This ultra-high purity variant, containing at least 99.9999% aluminum oxide, is increasingly being utilized in advanced semiconductor manufacturing, quantum computing components, and next-generation optical devices where even trace impurities can compromise performance. Additionally, in China, the Shanghai Institute of Ceramics reported that research institutions are exploring 6N alumina for use in cryogenic superconducting circuits, further driving demand.

By Application Insights

The LED application segment was the largest and held 41.2% of the Asia Pacific high-purity alumina market share in 2025. High-purity alumina serves as a critical raw material in the production of sapphire substrates used in gallium nitride (GaN)-based LEDs, which dominate modern lighting and display technologies. According to the Japan Electronics and Information Technology Industries Association, Japan’s LED production capacity increased by 13% in 2023, with most manufacturers sourcing HPA from domestic and regional suppliers to meet growing demand. South Korea’s Korea Semiconductor Industry Association also noted that OLED panel producers are increasingly integrating sapphire-based components into flexible display designs to enhance durability and optical clarity. With governments promoting energy-efficient lighting solutions and consumer electronics companies advancing display technologies, the LED segment remains the dominant driver of high-purity alumina demand across the Asia Pacific.

The Li-ion battery segment is lucratively to grow with a CAGR of 17.3% during the forecast period. High-purity alumina is widely used as a coating material for separators and electrodes in lithium-ion cells, enhancing thermal stability, preventing internal short circuits, and improving overall battery safety. According to the China Chemical Industry Association, HPA consumption in the battery sector grew by nearly 19% in 2023, driven by the rapid expansion of electric vehicle production and renewable energy storage projects. South Korean firms such as LG Energy Solution and Samsung SDI have also intensified their R&D efforts into HPA-coated separators to improve battery longevity and efficiency. The Indian Department of Heavy Industry noted a surge in domestic battery manufacturing investments, with several new gigafactories planning to integrate high-purity alumina into their production lines.

COUNTRY LEVEL ANALYSIS

China High Purity Alumina Market Analysis

China led the Asia Pacific high purity alumina market with a dominant share of 38.4% in 2025, with the country's strong presence in electronics manufacturing, LED production, and battery technologies underpinning its dominance in HPA consumption. According to the National Development and Reform Commission, China’s installed LED production capacity reached over 150 million lumens per month in 2023, significantly boosting demand for sapphire substrates derived from high-purity alumina.

Simultaneously, the China Automotive Engineering Research Institute reported that domestic electric vehicle sales surpassed 9 million units in 2023, fueling demand for alumina-coated battery separators. Additionally, the Ministry of Science and Technology allocated USD 500 million in nanomaterials funding, supporting advancements in alumina-based components for semiconductors and optical devices.

Japan High Purity Alumina Market Analysis

Japan was positioned second by holding 21.3% of the Asia Pacific high-purity alumina market share in 2025 within semiconductor manufacturing, synthetic sapphire production, and advanced electronic components. According to the Japan Institute of Metals, Japanese firms accounted for over 30% of global sapphire substrate exports in 2023, largely sourced from high-purity alumina inputs.

The Ministry of Economy, Trade, and Industry reported that semiconductor production in Japan rose by 14% in 2023, with major players like Sony and Toshiba incorporating HPA-based materials in wafer polishing and chamber linings. Additionally, the National Institute for Materials Science emphasized the role of 6N-grade alumina in emerging applications such as quantum computing and photonics. With sustained investment in high-tech industries and a focus on precision manufacturing, Japan maintains a strong foothold in the regional high-purity alumina market.

South Korea High Purity Alumina Market Analysis

South Korea's high-purity alumina market growth is driven by its globally recognized electronics and semiconductor industries. Companies such as Samsung and LG play a pivotal role in shaping regional demand for HPA through their advanced display technologies and integrated circuit manufacturing processes. Additionally, the Korea Institute of Industrial Technology reported that OLED display manufacturers are increasingly adopting sapphire-based substrates coated with high-purity alumina to enhance screen durability and optical performance.

India High Purity Alumina Market Analysis

India's high-purity alumina market is likely to grow due to increasing investments in LED manufacturing, solar power infrastructure, and battery technology. The Department of Electronics and Information Technology reported that domestic LED production surged by 25% in 2023, supported by government initiatives such as UJALA (Unnat Jyoti by Affordable LEDs for All).

The Indian Renewable Energy Development Agency also noted a 20% rise in solar panel installations nationwide, many of which utilize alumina-based ceramics for photovoltaic module encapsulation. Furthermore, the Ministry of Heavy Industries announced the establishment of six new lithium-ion battery gigafactories in 2025, each planning to incorporate high-purity alumina in separator coatings to enhance battery safety.

Australia High Purity Alumina Market Analysis

Australia's high-purity alumina market growth is leveraging its abundant bauxite reserves and strong refining capabilities. The country is one of the world’s top producers of metallurgical high-purity alumina, supplying both domestic and international markets with raw materials essential for electronics, ceramics, and aerospace applications. Additionally, the Department of Climate Change, Energy, the Environment, and Water indicated that several mining firms are investing in sustainable extraction methods to align with global ESG standards. With ongoing advancements in refining technologies and environmental stewardship, Australia plays a crucial role in supporting the Asia Pacific high-purity alumina supply chain.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific high-purity alumina market is shaped by a mix of established chemical and materials companies, specialized refineries, and emerging regional players striving to capture market share in a rapidly evolving industry. As demand surges from high-tech sectors like semiconductors, LEDs, and lithium-ion batteries, companies are under pressure to scale production while maintaining stringent quality standards. The market remains highly fragmented, with a few dominant firms controlling significant portions of supply, particularly in Japan, Australia, and China.

Innovation plays a crucial role in distinguishing competitors, as advancements in purification methods and production efficiency can provide substantial advantages. Additionally, sustainability concerns and regulatory pressures are pushing firms to adopt greener refining practices and invest in cleaner technologies. Smaller players are increasingly forming alliances or entering contract manufacturing agreements to remain competitive against larger corporations. Overall, the landscape is marked by continuous technological evolution, strategic positioning, and an intense focus on securing reliable feedstock sources amid rising global demand.

KEY MARKET PLAYERS

These are the market players that are dominating the Asia Pacific high-purity alumina market:

- Almatis, Inc.

- Altech Chemicals Ltd.

- Alpha HPA

- Baikowski

- CoorsTek Inc.

- FYI RESOURCES

- HONGHE CHEMICAL

- Shandong Aluminium Industry Science & Technology Co., Ltd. (China)

- Sasol Limited – Australian Subsidiary (Australia)

- Nippon Light Metal Holdings Co., Ltd.

- Orbite Technologies Inc.

- Polar Sapphire Ltd.

- Sumitomo Chemical Co., Ltd.

Top Players in the Market

- Sumitomo Chemical is a leading manufacturer of high-purity alumina in Japan and plays a vital role in supplying ultra-pure materials for semiconductor, LED, and electronic applications. The company has developed proprietary refining technologies that enable consistent production of 5N and 6N grade alumina. Its products are widely used by major electronics and chipmakers across Asia.

- Sasol’s Australian operations have become a cornerstone in the production of high-purity alumina, particularly through its advanced purification processes derived from coal-based feedstock. This unique approach allows the company to offer competitive pricing while maintaining product quality. Sasol supplies to both domestic and international markets, supporting industries such as synthetic sapphire manufacturing and ceramic components. Its strategic focus on sustainable alumina extraction strengthens its position in the Asia Pacific region.

- A subsidiary of China (Chalco), this company is one of China's largest producers of high-purity alumina, catering to the country’s booming LED, battery, and refractory sectors. It has invested heavily in R&D to develop new purification techniques and expand production capacity. With government backing and extensive distribution networks, the company plays a central role in meeting China’s growing demand and exporting to Southeast Asian markets.

Top Strategies Used By Key Market Participants

One of the key strategies employed by market participants in the Asia Pacific high-purity alumina market is vertical integration, where companies control multiple stages of the supply chain—from raw material sourcing to refining and end-product manufacturing. This helps ensure a stable supply of high-quality input materials and reduces dependency on external suppliers.

Another critical approach is investment in research and development to improve purification technologies and explore alternative production routes that enhance efficiency and reduce environmental impact. Companies are also focusing on developing higher-grade alumina variants tailored for niche applications such as quantum computing and solid-state batteries.

RECENT MARKET NEWS

- In March 2024, Sumitomo Chemical announced the expansion of its HPA production line at its Osaka facility, aiming to enhance its capacity to meet rising demand from the semiconductor industry.

- In June 2024, Sasol’s Australian division entered into a long-term supply agreement with a South Korean sapphire substrate manufacturer to ensure a dedicated channel for its itshigh-puritya output, which is strengthening its foothold in the electronics materials sector.

- In August 2024, Shandong Aluminium launched a new R&D center focused exclusively on next-generation purification techniques for high-purity alumina by targeting improved yield and lower processing costs, especially for battery and optical applications.

- In October 2024, Mitsubishi Materials formed a joint venture with a Japanese battery materials firm to co-develop alumina-coated separators for lithium-ion cells by aligning with the growing demand for safer and more efficient energy storage solutions.

- In December 2024, Baikowski, a French company with significant operations in Japan, expanded its local logistics network to improve delivery times and service reliability for semiconductor manufacturers across the Asia Pacific, which is reinforcing its presence in the region.

MARKET SEGMENTATION

This research report on the Asia Pacific high-purity alumina market is segmented and sub-segmented into the following categories.

By Product

- 4N

- 5N

- 6N

By Application

- LED

- Semiconductor

- Phosphor

- Sapphire

- Lithium-ion Batteries

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is high purity alumina (HPA), and why is it critical in advanced industries?

HPA refers to aluminum oxide (Al₂O₃) refined to ≥99.99% (4N) or higher purity—essential for applications demanding extreme thermal stability, optical clarity, and electrical insulation. In APAC, it’s a strategic material for LEDs, lithium-ion batteries, and semiconductors.

Which end-use sectors drive HPA demand in the region?

LED sapphire substrates remain the largest application, but lithium-ion battery separators (coated with HPA for thermal shutdown safety) are the fastest-growing segment—fueled by EV and energy storage expansion across China, Japan, and South Korea.

How is the EV boom reshaping HPA consumption?

As EV makers prioritize battery safety, HPA-coated ceramic separators are becoming standard in premium cells (e.g., CATL, LG Energy Solution, Panasonic); just 1 kg of HPA can coat separators for ~5–10 EV battery packs—scaling demand rapidly with gigafactory output.

What purity grades are most commercially relevant?

4N (99.99%) dominates LED and general ceramics; 4N5–5N (99.995–99.999%) is required for semiconductor components and advanced battery applications—where trace sodium or iron impurities can cause device failure.

Which countries lead in HPA production and consumption?

Japan (Sumitomo Chemical, Baikowski Japan) and China (Dongying HPA, Orbite China JV) lead manufacturing; South Korea and China are top consumers—driven by Samsung, LG, BOE, and CATL’s supply chains. Australia is emerging as a key feedstock (bauxite/alunite) and producer (e.g., Altech Chemicals’ Malaysian plant).

Who are the major HPA suppliers in APAC?

Global leaders: Sumitomo Chemical (Japan), Baikowski (France, strong APAC presence); Regional players: Orbite Technologies (Canada/China JV), Dongying HPA New Material (China), Altech Chemicals (Australia/Malaysia project), and Showa Denko (now Resonac, Japan)—investing in chloride and hydrothermal process scale-up.

What production technologies dominate, and how are they evolving?

Traditional sulfate and Bayer modifications are being replaced by chloride hydrolysis and hydrothermal synthesis for higher purity and lower contamination—though capital intensity and chemical handling remain challenges for new entrants.

How do supply chain security concerns affect the market?

Geopolitical tensions and export controls on critical minerals are pushing Japanese and Korean battery makers to secure long-term HPA contracts and support local/regional production—reducing reliance on single-source suppliers.

What challenges hinder broader adoption?

High production costs (up to 10× smelter-grade alumina), energy-intensive refining, limited number of certified suppliers for 5N+ grades, and competition from alternative ceramic coatings (e.g., silica, boehmite) constrain margin expansion.

What’s the market outlook for 2025–2030?

The APAC HPA market is projected to grow at a robust CAGR—driven by EV battery safety mandates, micro-LED display development, and 5G/6G semiconductor packaging—positioning HPA as a mission-critical enabler of the region’s high-tech manufacturing sovereignty.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com