Asia Pacific Hospital-Acquired Disease Testing Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Indication (UTI (Urinary Tract Infection), SSI (Surgical Site Infection), Pneumonia, Bloodstream Infections, MRSA (Methicillin-Resistant Staphylococcus Aureus), and Others), and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Market Size, 2025

$3.68 BnMarket Estimate, 2026

$4.24 BnMarket Forecast, 2034

$13.26 BnCAGR, 2026–2034

15.32%Asia Pacific Hospital-Acquired Disease Testing Market Size

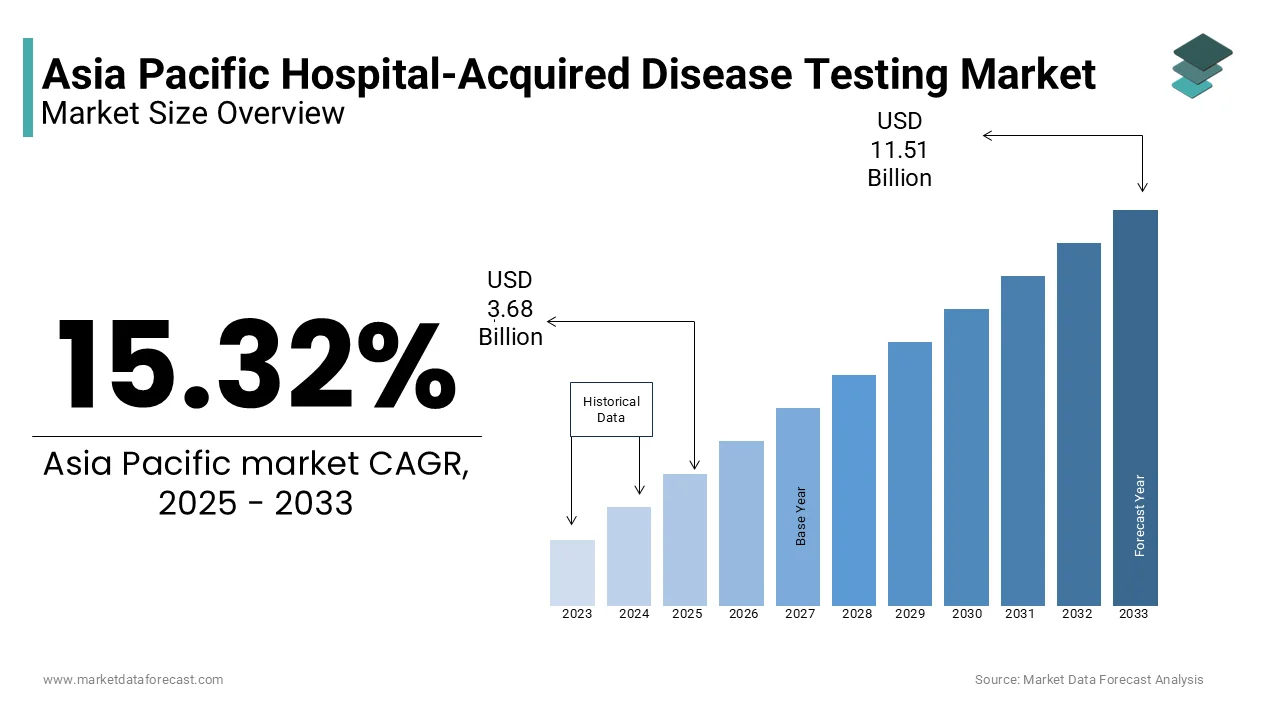

Asia Pacific hospital-acquired disease testing market size was valued at USD 3.68 billion in 2025, and the market size is expected to reach USD 13.26 billion by 2034 from USD 4.24 billion in 2026. The market's promising CAGR for the predicted period is 15.32%.

The Hospital-Acquired Disease Testing Market growth is driven by the growing need for diagnostic procedures that can quickly and accurately detect infections contracted during a patient’s stay in healthcare settings such as hospitals and long-term care facilities. These infections are commonly known as healthcare-associated infections (HAIs) including conditions like ventilator-associated pneumonia, surgical site infections and hospital-acquired bacterial pneumonia. Early and accurate diagnosis is critical in preventing transmission, reducing mortality and minimizing prolonged hospitalization.In the Asia Pacific region, the demand for hospital acquired disease testing has surged due to rising nosocomial infection rates as well as increased awareness among healthcare professionals and the expansion of intensive care infrastructure. HAIs affect nearly 10.18% of hospitalized patients in low and middle-income Asian countries which is significantly higher than the global average. Over 200,000 HAIs occur annually in Australia alone thereby emphasizing the pervasive nature of these infections even in high-income nations within the region.

MARKET DRIVERS

Rising Incidence of Multidrug-Resistant Infections

The increasing prevalence of multidrug-resistant (MDR) pathogens in healthcare settings is a major driver of the Asia Pacific hospital acquired disease testing market. Infections caused by organisms such as MRSA (Methicillin-resistant Staphylococcus aureus), VRE (Vancomycin-resistant Enterococcus) and carbapenem-resistant Enterobacteriaceae (CRE) have become alarmingly common across hospitals in the region. Nearly 40.72% of ICU-acquired infections in India are now attributed to MDR bacteria thereby necessitating advanced diagnostic tools for accurate detection and targeted treatment. In Vietnam, a 2023 study published in Antimicrobial Resistance and Infection Control found that CRE incidence had tripled over the past five years thus prompting hospitals to adopt rapid molecular assays for early identification. Australia has implemented mandatory screening protocols for MDR organisms in high-risk wards and aligning with guidelines from the Australian Society for Antimicrobials. This proactive approach has led to increased utilization of PCR-based diagnostics for real-time pathogen detection. Similarly, Japan has introduced automated susceptibility testing systems in major hospitals to streamline antibiotic selection.

Expansion of Infection Prevention and Control Programs

Governments and healthcare institutions in the Asia Pacific region are increasingly prioritizing infection prevention and control (IPC) programs which directly boost the demand for hospital acquired disease testing. These initiatives aim to reduce the burden of healthcare-associated infections through improved surveillance, staff training and implementation of rapid diagnostic workflows. Indonesia had launched a nationwide IPC improvement project in 2022 while mandating all secondary and tertiary hospitals to adopt real-time microbial tracking systems.China’s National Health Commission has also strengthened its regulatory framework by requiring compulsory HAI monitoring in all public hospitals. Over 600 hospitals adopted point-of-care testing devices between 2022 and 2025 to expedite infection reporting and isolation decisions. In South Korea, the Korea Disease Control and Prevention Agency has mandated quarterly HAI audits thus leading to increased procurement of culture and molecular diagnostics.

MARKET RESTRAINTS

Lack of Standardized Testing Protocols Across the Region

Lack of standardized diagnostic protocols across different countries is one of the most significant constraints hindering the growth of the Asia Pacific hospital acquired disease testing market. North America and Europefollow unified guidelines from bodies such as CLSI and EUCAST whereas the Asia Pacific region exhibits substantial variability in testing methodologies, specimen handling practices and interpretation criteria. Less than 40.72% of laboratories in the ASEAN region adhere to international standards for antimicrobial susceptibility testing. This inconsistency leads to discrepancies in pathogen identification and antibiotic sensitivity reporting, complicating clinical decision-making and undermining infection control efforts. For example, a 2023 audit conducted by the Philippine Department of Health revealed significant variations in blood culture processing times between urban and rural hospitals thus affecting sepsis diagnosis accuracy. In India, many smaller hospitals continue using outdated manual techniques resulting in delayed or false-negative results. Additionally, the absence of region-specific breakpoints for antimicrobial resistance further complicates therapy selection.

Limited Healthcare Budgets and Infrastructure Gaps

Financial limitations and inadequate healthcare infrastructure pose a persistent challenge to the widespread adoption of hospital acquired disease testing in the Asia Pacific region. Many low and middle-income countries struggle to allocate sufficient funds for advanced diagnostics in rural and semi-urban hospitals where basic laboratory services remain underdeveloped. Healthcare expenditure as a percentage of GDP in countries like Indonesia and the Philippines remains below 3.5% constraining investments in modern diagnostic equipment and consumables. In Nepal, only 12 out of 77 districts have functional biosafety level-2 laboratories capable of performing standard HAI diagnostics. Thailand is a relatively developed market but faces budgetary constraints that restrict the use of molecular diagnostics to large teaching hospitals thereby leaving community clinics dependent on conventional methods with lower sensitivity. Funding disparities result in uneven quality of care and contribute to high HAI-related morbidity.

MARKET OPPORTUNITIES

Integration of Digital Health Technologies

The integration of digital health technologies presents a transformative opportunity for the Asia Pacific hospital acquired disease testing market. Healthcare providers can enhance real-time surveillance of hospital-acquired infections (HAIs) and improve outbreak response capabilities with advancements in electronic health records (EHRs), artificial intelligence and cloud-based diagnostics. Over 50.23% of hospitals in Australia and New Zealand have already adopted AI-powered infection tracking systems thereby enabling faster detection and containment of nosocomial pathogens. Japan's Ministry of Health has promoted the use of RFID-enabled hand hygiene compliance monitoring and linking it with diagnostic data to assess the impact on infection rates. In India, tele-lab platforms are emerging as viable solutions for remote sample analysis which allows smaller hospitals to access centralized microbiology expertise without investing in full-scale labs.

Rise of Point-of-Care Diagnostics in Hospitals

The emergence and adoption of point-of-care (POC) diagnostics offer a significant growth avenue for the Asia Pacific hospital acquired disease testing market. These compact and rapid-testing platforms enable bedside or near-patient diagnosis thereby facilitating quicker clinical decisions and reducing turnaround time for infection detection. POC testing adoption in the Asia Pacific region is expected to grow at a CAGR of 14.17% through 2027 and is driven by demand for prompt HAI diagnosis in intensive care units and emergency departments. In South Korea, Samsung Medical Center has deployed fully automated rapid molecular diagnostic systems in ICUs by cutting sepsis identification time from 48 hours to under three hours.In Malaysia, the Ministry of Health has initiated a pilot program integrating handheld PCR devices in selected government hospitals to expedite detection of methicillin-resistant Staphylococcus aureus (MRSA). In Australia, Sonic Healthcare has introduced mobile POC labs in regional hospitals while improving access to urgent infection diagnostics.

MARKET CHALLENGES

Shortage of Trained Healthcare Personnel

Acute shortage of trained healthcare personnel is a major critical challenge impeding the expansion of the Asia Pacific hospital acquired disease testing market . Effective management of healthcare-associated infections (HAIs) requires skilled laboratory technicians, clinical microbiologists and infection control officers who can accurately interpret diagnostic results and guide antimicrobial stewardship. However, many countries in the region face a severe workforce deficit in these specialized areas.Fewer than 15.27% of biomedical science graduates in the Philippines pursue careers in clinical microbiology due to limited training opportunities and career progression challenges. In India ,less than half of government hospitals have dedicated microbiology departments. In China, there remains a significant disparity in staffing levels between Tier I cities and rural provinces despite heavy investment in diagnostics infrastructure. This shortage results in diagnostic delays and suboptimal infection control measures thereby undermining efforts to combat hospital-acquired diseases across the region.

Delayed Diagnostic Reporting and Workflow Inefficiencies

Delayed diagnostic reporting and inefficient laboratory workflows pose a persistent challenge in the Asia Pacific hospital acquired disease testing market. The timely identification of hospital-acquired infections (HAIs) is crucial for effective intervention yet many healthcare facilities still rely on traditional culture-based methods that can take several days to yield results. Over 40.18% of hospitals in Southeast Asia experience diagnostic delays exceeding 72 hours for bloodstream infections and ventilator-associated pneumonia. Such inefficiencies lead to prolonged empiric antibiotic use along with increasing the risk of antimicrobial resistance and poor patient outcomes. In Vietnam, nearly 60.18% of ICU patients received broad-spectrum antibiotics prior to confirmed pathogen identification due to slow lab turnaround times. In Bangladesh, only 12.9% of district hospitals have access to automated blood culture systems which force reliance on outdated manual techniques with lower sensitivity. Similarly, in Papua New Guinea, logistical limitations and lack of connectivity hinder real-time data sharing between laboratories and clinical teams. As per the Pacific Island Health Directors Forum, this fragmentation contributes to inconsistent infection tracking and delayed outbreak responses.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.32% |

| Segments Covered | By Indication, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Abbott Laboratories, F. Hoffmann-La Roche Ltd., Becton, Dickinson and Company (BD), bioMérieux SA, Cepheid, Siemens Healthineers, Hologic Inc., NG Biotech, Daiichi Sankyo Co., Ltd., AstraZeneca, and others |

SEGMENTAL ANALYSIS

By Indication Insights

The bloodstream infections segment held the leading share of 28.33% of the Asia Pacific hospital acquired disease testing market share in 2025. This dominance is primarily driven by the high mortality and economic burden associated with healthcare-associated bloodstream infections (BSIs) in intensive care units (ICUs) and post-surgical wards. A key driver behind this segment’s growth is the rising incidence of sepsis in hospitals across the region. Over 10 million cases of sepsis are reported annually in Asia with a case fatality rate exceeding 30.12% in low and middle-income countries. In India bloodstream infections account for nearly 45.49% of all ICU-acquired infections thus necessitating rapid diagnostic interventions. Another critical factor is the increasing use of invasive medical devices such as central venous catheters and ventilators in hospitalized patients which elevate the risk of pathogen entry into the bloodstream. Additionally, growing regulatory emphasis on antimicrobial stewardship has led to higher adoption rates of microbial identification and susceptibility testing thereby reinforcing the demand for BSI diagnostics in regional healthcare facilities.

The MRSA segment is projected to witness the fastest CAGR of 16.9% from 2026 to 2034 which is fueled by escalating antibiotic resistance and increased surveillance for drug-resistant pathogens in healthcare settings.One of the primary drivers is the widespread prevalence of MRSA infections in hospitals in surgical and ICU departments. MRSA accounts for nearly 50.03% of S. aureus isolates in Asia thereby contributing significantly to prolonged hospitalization and treatment complexity. In Japan, the Ministry of Health has mandated routine nasal screening for patients undergoing major surgeries leading to heightened diagnostic activity. Similarly, in Australia, increased funding under the Antimicrobial Resistance Strategy has enabled widespread implementation of rapid MRSA tests in public hospitals. Moreover, the integration of genomic typing methods to track MRSA outbreaks has further boosted the demand for advanced diagnostic tools. The volume of MRSA-specific diagnostic tests in the Asia Pacific region will more than double by 2027 thus emphasizing its status as the fastest-growing indication in the market.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific hospital acquired disease testing market and accounted for 25.76% of total market share in 2025. Due to its vast population, expanding healthcare infrastructure and rising prevalence of nosocomial infections. The country's large hospital network, coupled with an increasing number of ICU beds and surgical procedures has amplified the need for accurate and timely diagnostics to manage healthcare-associated infections (HAIs). Government initiatives such as the “Healthy China 2030” strategy have emphasized infection prevention and control thereby leading to stricter HAI reporting requirements. The Chinese Center for Disease Control and Prevention reports a consistent rise in multidrug-resistant organisms including MRSA and CRE which are driving demand for rapid and molecular diagnostics.

India was positioned second in holding the dominant share of the Asia Pacific hospital acquired disease testing market and is driven by high HAI incidence, increasing hospitalization rates and growing awareness about antimicrobial resistance. HAIs affect nearly 10.82% of hospitalized patients with bloodstream infections and surgical site infections being the most common. The lack of standardized infection control measures in many smaller hospitals has further compounded the problem thereby prompting both public and private stakeholders to invest in better diagnostic capabilities. The Ayushman Bharat scheme has improved access to secondary-level care which indirectly boost referrals for microbiological testing.

Japan’s hospital acquired disease testing market is likely to have significant growth opportunities during the forecast period and is supported by its well-developed healthcare system, aging population and high healthcare expenditure. The country experiences a disproportionately high rate of hospitalizations and long-term care admissions thus increasing the risk of HAIs. The Japanese Ministry of Health mandates strict infection control protocols in hospitals which include routine screening for MRSA and other resistant pathogens. Moreover, Japan's regulatory environment facilitates the swift approval of novel diagnostic technologies.

Australia’s hospital acquired disease testing market growth is likely to have fastest growth opportunities in the next coming years and bolstered by its stringent infection control policies, high healthcare spending and early adoption of digital diagnostics. The country’s well-established patient safety framework mandates regular HAI monitoring thus ensuring a consistent demand for diagnostic testing.Over 200,000 HAIs occur annually with bloodstream infections and surgical site infections accounting for the majority. The commission’s National Hand Hygiene Initiative and mandatory HAI reporting standards have spurred hospitals to integrate real-time pathogen identification tools into routine workflows. Australia’s telehealth evolution has enabled remote diagnostics which allows rural hospitals to access centralized microbiology labs.

South Korea’s hospital acquired disease testing market is likely to grow with healthy cagr in the next coming years and is driven by its strong focus on digital health, government-backed infection control initiatives and advanced hospital infrastructure. The country has been proactive in integrating technology into HAI surveillance along with leveraging AI and big data analytics to enhance infection tracking and response. MRSA and ventilator-associated pneumonia remain among the top causes of HAIs in tertiary hospitals. South Korea has adopted automated diagnostic platforms and rapid molecular assays thus reducing turnaround time for HAI detection.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific hospital acquired disease testing market is intensifying as multinational diagnostics firms and domestic players vie for market share through technological advancements and strategic deployments. Global leaders such as BioMérieux, Becton Dickinson and Thermo Fisher Scientific maintain a strong presence by leveraging their established brand reputation, extensive product portfolios and robust distribution networks. These firms are increasingly tailoring their offerings to meet the unique infection control challenges prevalent across diverse healthcare settings in the region. Meanwhile, emerging local manufacturers are gaining traction by offering cost-effective diagnostic solutions and improving access to essential testing in underpenetrated markets. The competitive landscape is further shaped by rising demand for rapid diagnostics, increasing regulatory scrutiny around antimicrobial use and the need for streamlined data integration. Companies are differentiating themselves through innovation, scalability and enhanced customer support, thereby fostering a dynamic and evolving marketplace.

KEY MARKET PLAYERS

Key players in the Asia Pacific hospital acquired disease testing market are Abbott Laboratories, F. Hoffmann-La Roche Ltd., Becton, Dickinson and Company (BD), bioMérieux SA, Cepheid, Siemens Healthineers, Hologic Inc., NG Biotech, Daiichi Sankyo Co., Ltd., and AstraZeneca.

TOP PLAYERS IN THE MARKET

- BioMérieux is a leading player in the Asia Pacific hospital acquired disease testing market and is known for its comprehensive portfolio of microbiology diagnostic solutions. The company offers advanced systems for pathogen detection, antimicrobial susceptibility testing and molecular diagnostics tailored to healthcare-associated infections (HAIs). BioMérieux has established strong partnerships with hospitals and research institutions to enhance infection control practices. Its commitment to innovation and localized service support has enabled widespread adoption of rapid diagnostic technologies thereby contributing significantly to global standards in HAI management.

- BD plays a pivotal role in the Asia Pacific hospital acquired disease testing landscape through its cutting-edge diagnostic instruments and blood culture systems designed for early detection of HAIs. The company’s focus on automation and integration into laboratory workflows supports faster diagnosis and improved patient outcomes. BD actively collaborates with public health agencies and private hospitals across the region to strengthen infection surveillance programs. Its strategic investments in training and technical support have further reinforced its position as a key provider of hospital infection diagnostics globally.

- Thermo Fisher Scientific contributes significantly to the Asia Pacific hospital acquired disease testing market by offering a wide range of diagnostic tools including PCR-based assays, microbial identification systems and antibiotic resistance detection platforms. The company supports healthcare providers in the region through scalable solutions that integrate seamlessly with hospital information systems. Thermo Fisher actively participates in regional health initiatives aimed at combating multidrug-resistant organisms. Its emphasis on R&D and digital diagnostics aligns with evolving clinical needs thereby making it a major force in shaping the future of HAI testing worldwide.

TOP STRATEGIES USED BY KEY PLAYERS

Enhancing product portfolios through continuous innovation and technology integration is one of the primary strategies employed by key players in the Asia Pacific hospital acquired disease testing market. Companies are focusing on developing rapid, accurate and automated diagnostic platforms that reduce turnaround times and improve clinical decision-making for healthcare-associated infections (HAIs).

Another critical approach is expanding distribution networks and forming strategic alliances with local healthcare providers. Companies ensure wider accessibility to their diagnostic solutions while adapting to regional regulatory and epidemiological requirements by partnering with hospitals, reference labs and government agencies.

There is a growing emphasis on developing integrated infection control ecosystems which combine diagnostics with data analytics and surveillance tools. This strategy enables real-time tracking of HAIs, supports antimicrobial stewardship and enhances infection prevention measures hence positioning companies as comprehensive solution providers in the fight against nosocomial diseases.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, BioMérieux partnered with a leading Japanese university hospital to co-develop next-generation diagnostic panels specifically targeting drug-resistant pathogens commonly found in Asian healthcare settings.

- In May 2025, Becton Dickinson launched a new regional innovation center in Singapore focused on expanding its portfolio of rapid diagnostics for hospital-acquired infections.

- In August 2025, Thermo Fisher Scientific introduced a cloud-connected pathogen detection system tailored for hospital laboratories in India and Indonesia.

- In October 2025, Siemens Healthineers expanded its partnership with multiple South Korean hospitals to integrate AI-powered infection surveillance tools into existing laboratory workflows.

- In December 2025, Sysmex Corporation entered into a strategic agreement with an Australian health tech firm to deploy automated diagnostics for bloodstream infections in public hospitals.

MARKET SEGMENTATION

This research report on the Asia Pacific hospital-acquired disease testing market has been segmented and sub-segmented based on the following categories.

By Indication

- UTI (Urinary Tract Infection)

- SSI (Surgical Site Infection)

- Pneumonia

- Bloodstream Infections

- MRSA (Methicillin-Resistant Staphylococcus Aureus)

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is the Asia Pacific Hospital-Acquired Disease Testing Market?

The Asia Pacific Hospital-Acquired Disease Testing Market comprises diagnostic tests and technologies used to detect infections acquired by patients during hospital stays, helping healthcare providers improve patient safety and infection control.

2. What factors are driving the growth of the Asia Pacific Hospital-Acquired Disease Testing Market?

The market is driven by the rising prevalence of hospital-acquired infections (HAIs), increasing healthcare expenditure, growing awareness of infection prevention, and expanding adoption of rapid diagnostic technologies.

3. What are hospital-acquired diseases?

Hospital-acquired diseases, also known as hospital-acquired infections (HAIs) or nosocomial infections, are infections that develop during or after a patient's hospital stay and were not present at the time of admission.

4. Which testing methods are commonly used for hospital-acquired diseases?

Common testing methods include molecular diagnostics, polymerase chain reaction (PCR), immunoassays, microbial culture tests, rapid antigen tests, and next-generation sequencing (NGS).

5. Which pathogens are commonly detected through hospital-acquired disease testing?

Testing commonly targets pathogens such as Methicillin-resistant Staphylococcus aureus (MRSA), Clostridioides difficile, Escherichia coli (E. coli), Klebsiella pneumoniae, Pseudomonas aeruginosa, and Vancomycin-resistant Enterococci (VRE).

6. Which end users are the primary customers in this market?

The primary end users include hospitals, diagnostic laboratories, specialty clinics, academic research institutes, and public health organizations.

7. Which country holds a significant share of the Asia Pacific Hospital-Acquired Disease Testing Market?

China holds a significant market share due to its large healthcare infrastructure, increasing hospital admissions, growing investments in diagnostic technologies, and rising focus on infection control.

8. Which country is expected to witness the fastest market growth?

India is expected to register rapid growth owing to expanding healthcare facilities, increasing awareness of hospital-acquired infections, improving diagnostic capabilities, and supportive government healthcare initiatives.

9. How are molecular diagnostics influencing the market?

Molecular diagnostic technologies provide faster, highly accurate detection of pathogens, enabling timely treatment decisions, improved infection surveillance, and better antimicrobial stewardship in healthcare settings.

10. What is the future outlook for the Asia Pacific Hospital-Acquired Disease Testing Market?

The market is expected to experience strong growth over the coming years, driven by increasing investments in healthcare infrastructure, rising adoption of rapid molecular diagnostics, expanding infection surveillance programs, and growing emphasis on patient safety and antimicrobial resistance management.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com