Asia Pacific Household Vacuum Cleaners Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Product (Canister, Central, Robotic, Drum, Upright, Wet & Dry), Distribution, Power Source, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2025 to 2033

Asia Pacific Household Vacuum Cleaners Market Size

Asia Pacific Household Vacuum Cleaners market size was valued at USD 1.71 billion in 2024, and the market size is expected to reach USD 4.65 billion by 2033 from USD 1.92 billion in 2025. The market's promising CAGR for the predicted period is 11.72%.

The Asia Pacific household vacuum cleaners market refers to the sale and distribution of residential cleaning appliances designed for dust and debris removal in homes, apartments, and small commercial spaces. The market encompasses a wide range of products including upright, canister, stick, handheld, robotic, and smart vacuum cleaners. According to the International Labour Organization, the growing participation of women in the workforce in countries like India and China has led to an increased reliance on automated home appliances to manage household chores efficiently.

Additionally, in Australia, the Australian Institute of Health and Welfare reports that rising concerns around allergens and indoor pollutants have prompted more consumers to invest in high-efficiency vacuum cleaners equipped with HEPA filters. As per the Korea Electronics Association, the adoption of AI-integrated and IoT-enabled vacuum cleaners is also gaining momentum, particularly among younger, tech-savvy consumers.

MARKET DRIVERS

Rising Urbanization and Changing Lifestyles

One of the primary drivers of the Asia Pacific household vacuum cleaners market is the rapid pace of urbanization and evolving consumer lifestyles. As more people migrate to cities and adopt modern living standards, there is a growing emphasis on cleanliness, efficiency, and convenience in household maintenance. In India, as reported by the Ministry of Housing and Urban Affairs, the expansion of middle-class housing developments has led to a surge in demand for compact and lightweight vacuum cleaners suitable for smaller living spaces. Moreover, in Southeast Asian countries such as Thailand and Vietnam, the rise of dual-income households has contributed to greater adoption of time-saving cleaning appliances.

Increasing Awareness of Indoor Air Quality and Allergen Control

Another significant driver fueling the growth of the Asia Pacific household vacuum cleaners market is the heightened awareness regarding indoor air quality and allergen management. Consumers are increasingly recognizing the link between poor indoor air conditions and health issues such as asthma, allergies, and respiratory infections. According to the World Health Organization, air pollution-related illnesses have become a major public health concern in densely populated cities across the region.

Furthermore, in Australia, the Asthma Foundation recommends regular use of high-efficiency vacuum cleaners to minimize dust mite exposure and improve respiratory health. As per the Singapore Green Building Masterplan, more than 40% of new residential developments now include provisions for improved indoor air quality, which is encouraging homeowners to invest in vacuum cleaners with superior suction and filtration capabilities, thus reinforcing market expansion across the Asia Pacific.

MARKET RESTRAINTS

High Cost of Premium and Smart Vacuum Cleaner Models

A key restraint affecting the Asia Pacific household vacuum cleaners market is the relatively high cost of premium and smart vacuum cleaner models, which limits adoption among price-sensitive consumers. While advanced models featuring AI integration, app control, and autonomous navigation offer enhanced functionality, they often come with price tags that are significantly higher than traditional vacuum cleaners. According to Deloitte, in emerging economies such as Indonesia and the Philippines, less than 15% of households can afford robotic or cordless vacuum cleaners due to budget constraints. Moreover, according to PwC, even in developed markets like Australia and Japan, economic downturns and fluctuating exchange rates have caused some consumers to delay purchases of premium vacuum cleaner models.

Lack of After-Sales Service Infrastructure in Rural Areas

Another major restraint impacting the Asia Pacific household vacuum cleaners market is the limited availability of after-sales service infrastructure in rural and semi-urban regions. While urban centers benefit from well-established repair networks and spare parts availability, many consumers in remote areas face difficulties in obtaining timely maintenance and technical support. According to Frost & Sullivan, over 70% of vacuum cleaner users in rural India report delays in servicing, discouraging repeat purchases.

MARKET OPPORTUNITIES

Growth of E-commerce and Direct-to-Consumer Sales Channels

An emerging opportunity in the Asia Pacific household vacuum cleaners market is the rapid expansion of e-commerce platforms and direct-to-consumer sales channels. Online retail has transformed the way consumers purchase home appliances, offering greater accessibility, competitive pricing, and a wider selection of models. In China, as per the China E-Commerce Research Center, major platforms such as Tmall and JD.com accounted for over 60% of all vacuum cleaner sales in 2023, with exclusive online launches becoming a common strategy for brands to reach mass audiences. Additionally, as per Frost & Sullivan, several international vacuum cleaner brands have established localized e-commerce partnerships to bypass traditional distribution hurdles and directly engage with consumers. This shift toward online retail presents a substantial growth avenue for manufacturers seeking to expand their reach across diverse consumer segments in the Asia Pacific.

Growing Demand for Cordless and Robotic Vacuum Cleaners

Another promising opportunity in the Asia Pacific household vacuum cleaners market is the rising consumer preference for cordless and robotic vacuum cleaners. These models offer greater mobility, ease of use, and smart automation, aligning with the evolving expectations of tech-savvy and convenience-driven consumers.

In Australia, the Australian Retailers Association notes that over 25% of vacuum cleaner purchases in 2023 were for cordless models, driven by urban professionals and multi-family households seeking lightweight and versatile cleaning solutions. Additionally, as per the China Household Electrical Appliance Association, domestic brands such as Ecovacs and Roborock have gained significant traction by offering affordable yet feature-rich robotic vacuum cleaners.

MARKET CHALLENGES

Intense Market Competition and Price Pressure

One of the foremost challenges facing the Asia Pacific household vacuum cleaners market is the intense competition among both global and regional players, which is resulting in significant price pressure and margin erosion. Numerous manufacturers compete not only on product innovation but also on aggressive pricing strategies, making it difficult for newer entrants to establish a foothold. According to McKinsey Global Institute, over 150 brands are actively selling vacuum cleaners in China alone, leading to commoditization and frequent promotional discounts that dilute profitability.

Moreover, as per PwC, retailers and online marketplaces exert considerable influence over pricing and visibility, further complicating the ability of manufacturers to maintain consistent margins. These competitive pressures make it increasingly challenging for companies to sustain long-term profitability while continuing to innovate and meet evolving consumer demands.

Rapid Technological Obsolescence and Consumer Skepticism

Another critical challenge confronting the Asia Pacific household vacuum cleaners market is the rapid pace of technological obsolescence, which leads to consumer skepticism and hesitation toward high-end models. In South Korea, as reported by the Korea Consumer Agency, nearly 40% of surveyed consumers expressed concerns about the longevity and future compatibility of smart vacuum cleaners. Similarly, in Australia, the Australian Competition and Consumer Commission found that returns and dissatisfaction rates for high-tech vacuum cleaners increased by 15% in 2023 compared to conventional models. Additionally, as per Frost & Sullivan, in India and Indonesia, many consumers remain skeptical about the actual performance benefits of premium vacuum cleaners, often viewing them as unnecessary luxury items rather than essential home appliances. This perception gap hampers the adoption of advanced models, despite growing digital awareness and marketing efforts aimed at educating consumers on long-term value and efficiency gains.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 11.72% |

| Segments Covered | By Product, Distribution, Power Source, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Bissell Inc., Electrolux, Dyson Limited, Eureka Forbes, Groupe SEB, Haier Group, Koninklijke Philips N.V., Miele, and Stanley Black & Decker, Inc, and others |

SEGMENTAL ANALYSIS

By Product Insights

The upright vacuum cleaner segment dominated the Asia Pacific household vacuum cleaners market, accounting for 32.3% of share in 2024. According to the China Household Electrical Appliance Association, over 45% of vacuum cleaner sales in China in 2023 were upright models, particularly among middle-income families with larger homes. Additionally, in Australia, the Australian Institute of Health and Welfare reports that nearly 38% of homeowners prefer upright models for deep cleaning carpets and pet hair removal. The combination of durability, user-friendliness, and cost-effectiveness continues to reinforce the dominance of upright vacuum cleaners in the regional market.

The robotic vacuum cleaner segment is swiftly emerging with the Asia Pacific household vacuum cleaners market with a CAGR of 18.6% from 2025 to 2033. In South Korea, the Korea Electronics Association notes that nearly 40% of newly launched vacuum cleaners in 2023 featured autonomous navigation and app-based controls, indicating strong consumer interest. Moreover, as per the Japan Consumer Electronics Association, robotic vacuum cleaner adoption in urban households has increased significantly, particularly among dual-income families seeking time-saving cleaning solutions.

By Distribution Channel Insights

The offline segment was the largest and held 54.3% of the Asia Pacific household vacuum cleaners market share in 2024. According to the India Retail Forum, over 60% of vacuum cleaner purchases in Tier-2 and Tier-3 cities occur through offline retail stores, where customers can physically assess product performance before buying. In Indonesia, according to the Indonesian Chamber of Commerce, traditional electronics retailers and appliance showrooms remain the primary sales points for mid-range and premium vacuum cleaners.

Additionally, as per the Japan Retail Association, major home appliance chains such as Yamada Denki and Bic Camera play a crucial role in influencing purchasing decisions through expert consultations and bundled offers.

The online distribution channels segment is likely to exhibit a CAGR of 22.4% in the next coming years. This expansion is fueled by the rapid rise of e-commerce platforms, digital payment adoption, and growing consumer preference for convenience-driven shopping experiences. According to Statista, online sales of vacuum cleaners in the Asia Pacific grew by 24% in 2023 compared to the previous year, with China and India witnessing the highest growth rates. In China, as per the China E-Commerce Research Center, Tmall and JD.com accounted for over 60% of all vacuum cleaner transactions, offering exclusive deals and instant delivery options. Similarly, in South Korea, the Korea Internet & Security Agency reports that online vacuum cleaner sales surged by 35% in 2023, driven by influencer marketing and social commerce trends.

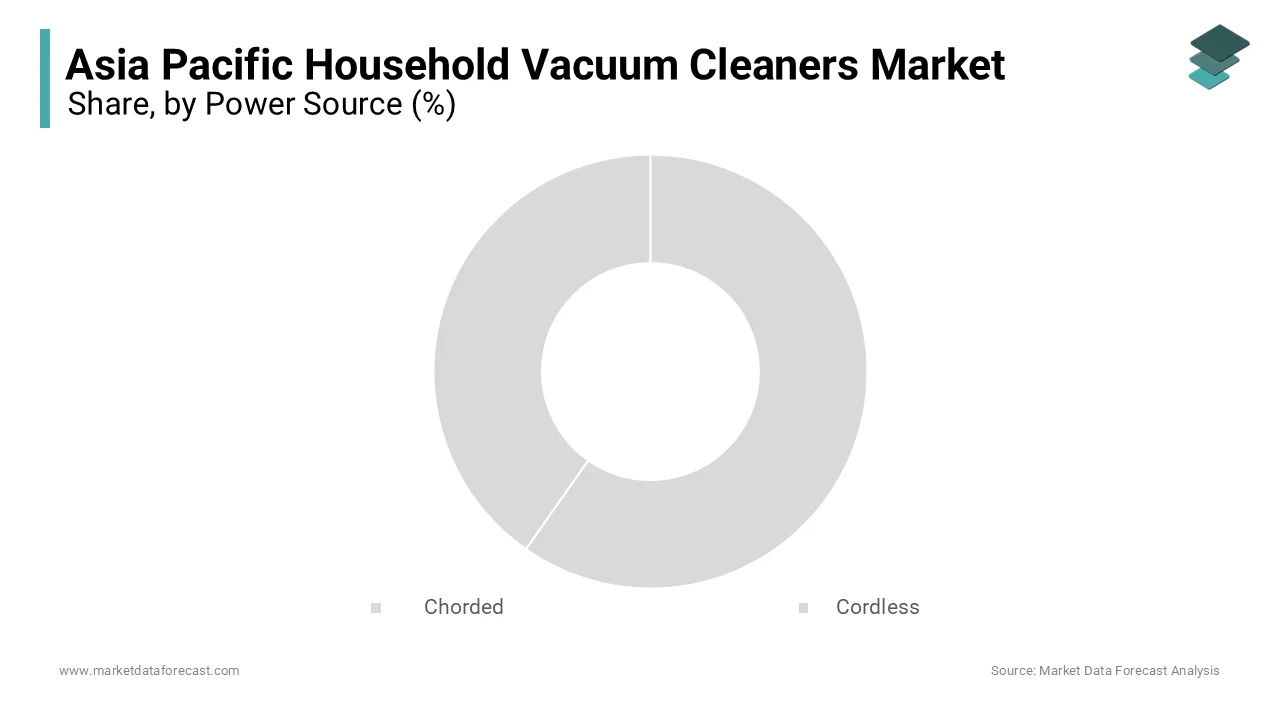

By Power Source Insights

The corded vacuum cleaners segment was accounted in holding 58.3% in 2024 with their affordability, consistent power supply, and suitability for deep cleaning applications, which is making them a popular choice among budget-conscious consumers. According to the China Household Electrical Appliance Association, over 50% of vacuum cleaner buyers in China in 2023 opted for corded variants due to their reliability and lower price points. Additionally, as per the Japan Electrical Manufacturers' Association, corded models continue to be widely used in commercial settings such as hotels and offices, where long-duration cleaning tasks require sustained suction power.

The cordless vacuum cleaners segment is likely to grow with a CAGR of 19.3% in the next coming years with the increasing consumer preference for lightweight, portable, and convenient cleaning solutions in urban apartments and multi-story homes. Furthermore, as per the Singapore Green Building Masterplan, residential developers are increasingly recommending cordless vacuum cleaners for space-efficient living environments. The cordless models are gaining traction across diverse consumer segments in the Asia Pacific with ongoing improvements in battery life, suction efficiency, and smart features.

REGIONAL ANALYSIS

China was the largest in the Asia Pacific household vacuum cleaners market with 34.3% of total share in 2024 with its massive consumer base, rapid urbanization, and expanding middle-class population that drives demand for modern home appliances. According to the National Bureau of Statistics of China, urban household penetration of vacuum cleaners exceeded 70% in 2023, with higher adoption rates in first- and second-tier cities.

India was ranked second with 17.1% of the Asia Pacific household vacuum cleaners market share in 2024 owing to the rising disposable incomes, urbanization, and evolving consumer lifestyles that prioritize cleanliness and hygiene. According to the Ministry of Housing and Urban Affairs, the Smart Cities Mission has spurred demand for modern home appliances, including vacuum cleaners, as part of broader efforts to enhance urban living standards.

In recent years, as noted by the Confederation of Indian Industry, there has been a notable increase in vacuum cleaner adoption among middle-class and upper-middle-class households. Additionally, the rise of dual-income households and greater awareness of allergen control has led to increased demand for HEPA-filter-equipped models.

Japan household vacuum cleaners market growth is lucratively growing with a strong presence due to its early adoption of high-efficiency vacuum cleaners, deep integration into daily household routines, and emphasis on indoor air quality.

According to the Japan Electrical Manufacturers' Association, nearly 80% of Japanese households own at least one vacuum cleaner, with many opting for advanced models featuring HEPA filters and energy-efficient motors. Additionally, as per the Ministry of Economy, Trade and Industry, government-led initiatives promoting healthy indoor environments have encouraged the adoption of vacuum cleaners equipped with allergen-trapping filtration systems.

South Korea household vacuum cleaners market is steadily growing with early adoption of smart home technologies, high internet penetration, and increasing consumer reliance on AI-enabled appliances for household maintenance. According to the Korea Consumer Electronics Association, over 35% of new vacuum cleaner models introduced in 2023 featured AI-powered navigation, voice control, and self-cleaning capabilities. Additionally, as per the Korea Internet & Security Agency, online sales of vacuum cleaners grew by 32% in 2023, driven by influencer marketing and live-streamed product demonstrations.

Australia household vacuum cleaners market growth is likely to grow with growing concerns around indoor air quality, allergy management, and the increasing prevalence of pets in households. According to the Australian Institute of Health and Welfare, nearly 20% of households now include at least one person suffering from allergies or asthma, prompting demand for vacuum cleaners with HEPA filtration systems. Additionally, according to the Property Council of Australia, real estate developers are increasingly incorporating vacuum cleaner recommendations as part of wellness-focused housing designs.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Bissell Inc., Electrolux, Dyson Limited, Eureka Forbes, Groupe SEB, Haier Group, Koninklijke Philips N.V., Miele, and Stanley Black & Decker, Inc. are the key players in the Asia Pacific household vacuum cleaners market.

The competition in the Asia Pacific household vacuum cleaners market is intense, characterized by the coexistence of global giants and rapidly growing regional brands vying for consumer attention through technological advancements and pricing strategies. The market is highly fragmented, with numerous players competing not only on product functionality but also on affordability, ease of use, and after-sales service efficiency. While established international brands like Dyson, Samsung, and Panasonic dominate premium segments with cutting-edge innovations, domestic manufacturers in China, India, and Southeast Asia are aggressively capturing mid- to entry-level markets with cost-effective alternatives.

Consumer demand is increasingly shifting toward smart and cordless models, prompting companies to invest heavily in battery technology, app-based controls, and autonomous navigation features. E-commerce has further intensified the competition by enabling direct-to-consumer sales and rapid market penetration. At the same time, rising health consciousness and allergy awareness are driving interest in HEPA-filter-equipped models, reinforcing the need for differentiated product offerings. To stay ahead, market participants are focusing on localized manufacturing, digital engagement, and after-sales service optimization by ensuring sustained relevance in a fast-evolving landscape.

TOP PLAYERS IN THE MARKET

Dyson Limited

Dyson is a dominant force in the Asia Pacific household vacuum cleaners market, known for its high-performance cordless models that combine advanced engineering with sleek design. The company has significantly influenced consumer preferences by introducing digital motors, HEPA filtration systems, and robotic variants tailored to urban living. In the Asia Pacific region, Dyson’s focus on innovation and premium branding has positioned it as a leader among aspirational buyers seeking superior cleaning performance.

Ecovacs Robotics Co., Ltd.

Ecovacs plays a pivotal role in shaping the regional market, particularly in the robotic vacuum cleaner segment. As a China-based manufacturer, the company has leveraged AI and smart home integration to expand its reach across Southeast Asia, Japan, and Australia. Through continuous R&D investment and strategic partnerships with e-commerce platforms, Ecovacs has become synonymous with affordable yet feature-rich robotic cleaning solutions, which is making it a preferred brand for tech-savvy consumers.

Panasonic Corporation

Panasonic remains a key player in the Asia Pacific market due to its strong regional presence and long-standing reputation for reliability and energy-efficient appliances. The company offers a broad range of vacuum cleaners, including upright, canister, and stick models designed to meet diverse consumer needs. With deep integration into local supply chains and a commitment to sustainable product development, Panasonic continues to reinforce its competitive edge across both traditional and modern retail channels.

TOP STRATEGIES USED BY KEY PLAYERS

One of the primary strategies adopted by leading players in the Asia Pacific household vacuum cleaners market is product innovation and differentiation , where companies continuously develop new features such as enhanced suction power, lightweight designs, and smart connectivity to cater to evolving consumer expectations. Another crucial approach is strategic collaborations and digital marketing , with brands leveraging social commerce, influencer endorsements, and online demonstrations to drive awareness and engagement, particularly in emerging markets. Additionally, localized distribution expansion and after-sales service improvement are widely pursued, allowing firms to strengthen customer trust, ensure timely maintenance support, and gain a competitive advantage in price-sensitive and rural regions.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Dyson launched its latest V17 Detect model in Singapore and Australia, featuring enhanced laser dust detection and improved battery life. This launch was aimed at strengthening Dyson’s foothold in the premium cordless vacuum cleaner segment across the region.

- In July 2023, Ecovacs introduced an AI-powered robotic vacuum cleaner equipped with real-time mapping and voice command compatibility in China and South Korea. This initiative was intended to enhance user experience and accelerate adoption among younger, tech-oriented consumers.

- In November 2023, Panasonic expanded its manufacturing facility in Malaysia to increase production capacity for compact upright and canister models, targeting growing demand in ASEAN countries. This move was designed to reduce costs and improve regional supply chain efficiency.

- In March 2024, SharkNinja entered into a strategic partnership with Flipkart in India to exclusively launch a series of budget-friendly vacuum cleaners tailored for Indian households. This collaboration aimed to boost market penetration in Tier-2 and Tier-3 cities.

- In August 2023, Xiaomi unveiled a new line of budget robotic vacuum cleaners under its Mi Home ecosystem in Thailand and Indonesia. The launch focused on expanding Xiaomi’s influence in the smart home sector and attracting first-time buyers looking for affordable automation.

MARKET SEGMENTATION

This research report on the Asia Pacific household vacuum cleaners market has been segmented and sub-segmented based on the following categories.

By Product

- Canister

- Central

- Drum

- Robotic

- Upright

- Wet & Dry

- Others

By Distribution Channel

- Online

- Offline

By Power Source

- Chorded

- Cordless

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What are the key opportunities in the Asia Pacific household vacuum cleaners market?

The rising urban population, increased focus on home hygiene, and growing adoption of smart, cordless, and robotic vacuum cleaners offer strong growth opportunities.

2. What trends are driving the Asia Pacific vacuum cleaner market?

Major trends include the surge in demand for energy-efficient and compact designs, increasing integration of AI and IoT, and rising preference for robotic vacuum cleaners.

3. What challenges does the Asia Pacific vacuum cleaner market face?

Challenges include high product costs, limited consumer awareness in rural areas, and maintenance concerns for advanced models like robotic vacuums.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com