Asia Pacific imaging Agents Market Size, Share, Growth, Trends, And Forecast Research Report, Segmented By Product, Imaging Modality, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore and Rest of APAC), Industry Analysis From (2025 to 2033)

Asia Pacific Imaging Agents Market Summary

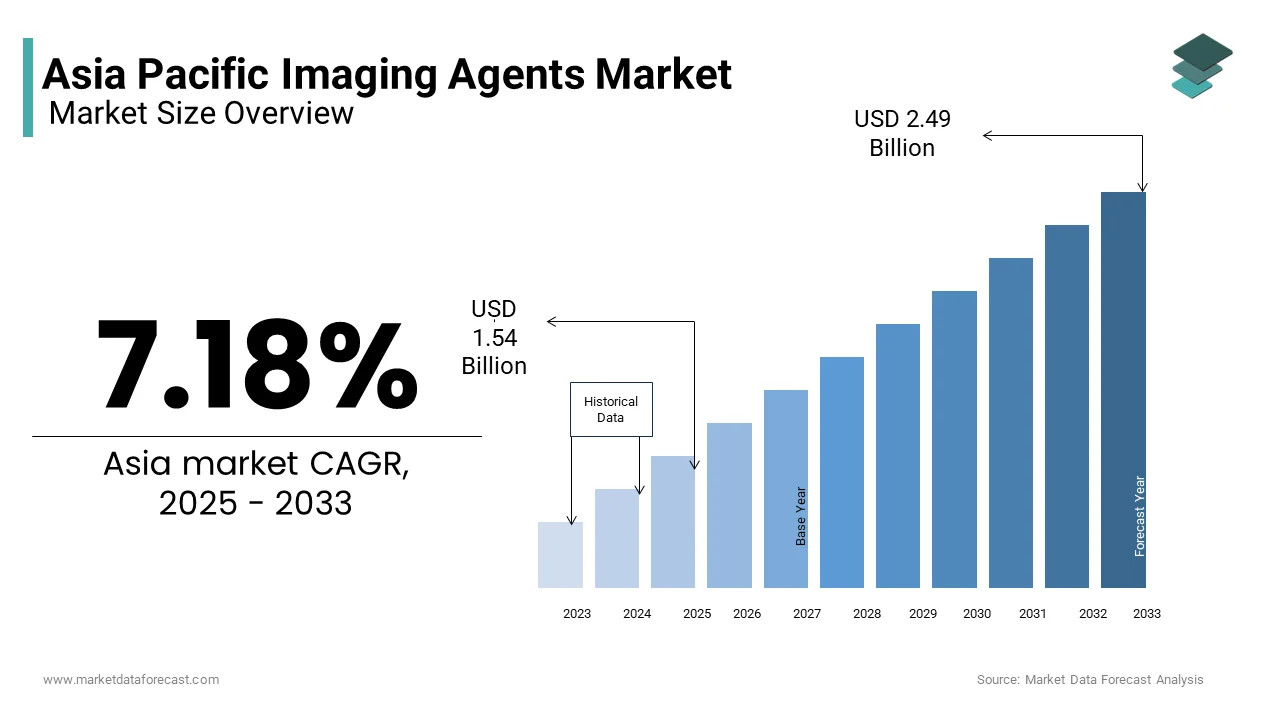

The Asia Pacific imaging agents market was valued at USD 1.43 billion in 2024 and is anticipated to USD 1.54 billion in 2025 to USD 2.49 billion by 2033, growing at a CAGR of 7.18% during the forecast period from 2025 to 2033.

Key Market Trends & Insights

- China was the top performer of the Asia Pacific Market in 2024.

- Japan was positioned second in the Asia Pacific market in 2024.

- India is likely to grow with new opportunities in the Asia Pacific market in 2024.

- Based on Product, the iodinated contrast media segment held 58.2% market in 2024.

- Based on Imaging Modality, the X-ray and computed tomography segment led the market in 2024

Market Size & Forecast

2024 Market Size: USD 1.43 Billion

2033 projected Market Size: USD 2.49 Billion

CAGR (2025 to 2033): 7.18%

China: Largest Market in 2024

Japan: Strongest Growth Region

Asia Pacific Imaging Agents Market Size

The Asia Pacific imaging agents market was valued at USD 1.43 billion in 2024 and is anticipated to USD 1.54 billion in 2025 to USD 2.49 billion by 2033, growing at a CAGR of 7.18% during the forecast period from 2025 to 2033.

The imaging agents are designed to enhance the contrast and clarity of internal anatomical structures during diagnostic imaging procedures such as magnetic resonance imaging (MRI), computed tomography (CT), ultrasound, and nuclear medicine. Their clinical utility is in oncology, cardiology, and neurology, where early and precise diagnosis significantly influences patient outcomes. The integration of imaging agents into routine diagnostic workflows has been accelerated by the rising incidence of chronic diseases and the expansion of advanced imaging infrastructure across the region. This epidemiological shift has intensified the demand for high-resolution imaging to enable early intervention. Additionally, the number of imaging-capable hospitals in Southeast Asia has increased by 38% since 2018, as documented by the Asian Pacific Society of Radiology, reflecting a systemic upgrade in diagnostic capacity.

MARKET DRIVERS

Rising Incidence of Chronic Diseases Requiring Advanced Diagnostic Imaging

The escalating prevalence of chronic diseases across the Asia Pacific region is a primary factor for the growth of the Asia Pacific imaging agents market. According to the World Health Organization, non-communicable diseases such as cancer, cardiovascular disorders, and neurological conditions accounted for 65% of total deaths in the region in 2023, with cancer alone responsible for over 8 million fatalities annually. Early and accurate diagnosis improves survival rates, and contrast-enhanced imaging has become a standard component in disease staging and treatment planning. In China, the National Cancer Center reported that over 4.8 million new cancer cases were diagnosed in 2023, necessitating millions of contrast-enhanced CT and MRI scans for tumor localization and metastasis assessment. Similarly, in India, the All India Institute of Medical Sciences documented a 30% increase in contrast MRI usage for brain and spinal tumors between 2020 and 2023, driven by improved access to imaging facilities in tier-2 and tier-3 cities. In Japan, where the aging population faces a high burden of cerebrovascular diseases, gadolinium-based agents are routinely used in MRI to detect early ischemic changes, with over 2.3 million contrast-enhanced neuroimaging procedures performed annually as per the Japanese Society of Radiological Technology. The Australian Institute of Health and Welfare noted that 78% of all cardiac MRI scans in the country involve contrast agents to assess myocardial viability.

Expansion of Advanced Imaging Infrastructure and Healthcare Modernization

The rapid modernization of healthcare systems across the Asia Pacific region in emerging economies has led to a substantial increase in the deployment of advanced diagnostic imaging equipment, directly boosting demand for imaging agents. Governments and private healthcare providers are investing heavily in upgrading medical facilities with state-of-the-art MRI, CT, and PET-CT scanners to improve diagnostic accuracy and reduce patient referral delays. Similarly, Indonesia’s National Health Insurance agency (BPJS Kesehatan) has approved reimbursement for contrast-enhanced imaging in oncology and cardiology, leading to a 40% rise in agent utilization between 2021 and 2023. In Vietnam, the number of MRI-capable hospitals increased from 89 to 157 between 2020 and 2023, according to the Ministry of Health, creating new demand for gadolinium-based contrast media.

MARKET RESTRAINTS

Safety Concerns and Regulatory Scrutiny Over Contrast Agent Toxicity

Persistent safety concerns surrounding certain imaging agents, particularly gadolinium-based contrast media (GBCAs), are impeding their widespread adoption in several Asia Pacific countries. Nephrogenic systemic fibrosis (NSF), a rare but severe condition linked to gadolinium retention in patients with renal impairment, has led to heightened regulatory caution. As per the Pharmaceuticals and Medical Devices Agency of Japan, over 120 cases of gadolinium deposition in brain tissues were reported between 2017 and 2022, prompting the agency to issue revised guidelines restricting the use of linear GBCAs in high-risk populations. In Australia, the Therapeutic Goods Administration suspended the registration of two linear agents in 2021 due to bioaccumulation risks. Similarly, China’s National Medical Products Administration has mandated stricter pre-scan renal function assessments before administering GBCAs, increasing procedural complexity and reducing utilization in primary care settings. In India, a 2023 survey by the Indian Radiological and Imaging Association found that 68% of radiologists limit contrast use in elderly patients due to safety apprehensions. Additionally, iodinated CT agents are associated with contrast-induced nephropathy, particularly in diabetic patients, who constitute over 77 million individuals in the region as per the International Diabetes Federation. These safety issues not only affect clinical decision-making but also increase liability concerns for healthcare providers.

High Cost and Limited Reimbursement in Emerging Economies

The high cost of advanced imaging agents and inadequate reimbursement frameworks in many Asia Pacific countries significantly limit their accessibility, particularly in low- and middle-income healthcare systems. In Indonesia, BPJS Kesehatan covers only 40% of contrast agent costs for CT and MRI, leading to low adoption rates outside major urban centers. India’s National Health Authority includes contrast MRI in its Ayushman Bharat scheme, but procurement delays and hospital-level pricing disparities result in inconsistent availability. As per a 2023 study published by the Public Health Foundation of India, only 32% of rural diagnostic centers offer contrast imaging due to cost and supply chain constraints. Even in more developed markets like Malaysia, public hospitals face budgetary limitations that restrict the frequency of contrast agent procurement. The absence of bulk tendering mechanisms and reliance on imported agents further inflate prices. While generic versions are emerging, regulatory approval timelines remain lengthy.

MARKET OPPORTUNITIES

Development of Targeted and Theranostic Imaging Agents

The emergence of targeted and theranostic imaging agents is creating new opportunities for the growth of the Asia Pacific imaging agents market. In oncology, prostate-specific membrane antigen (PSMA)-targeted PET tracers such as gallium-68 PSMA-11 are being used in Japan, South Korea, and Australia to detect metastatic prostate cancer with unprecedented accuracy. According to the Asia Oceania Federation of Nuclear Medicine and Biology, over 120 hospitals in the region have adopted PSMA-PET imaging since 2020, with diagnostic accuracy exceeding 90% in biochemical recurrence cases. In cardiovascular imaging, novel agents targeting amyloid plaques are improving the diagnosis of cardiac amyloidosis, a condition increasingly recognized in aging populations. The National Cerebral and Cardiovascular Center in Japan has integrated florbetapir-based PET scans into routine dementia workups, enhancing early Alzheimer’s detection.

Integration of Imaging Agents in Minimally Invasive and Image-Guided Interventions

The growing adoption of minimally invasive procedures and image-guided interventions is greatly influencing the growth of the Asia Pacific imaging agents market. In interventional radiology, contrast agents are essential for visualizing vascular anatomy during embolization, ablation, and stent placement. In China, the number of transcatheter arterial chemoembolization (TACE) procedures for liver cancer increased by 28% annually between 2020 and 2023, as reported by the Chinese Society of Interventional Radiology, with each procedure requiring multiple doses of iodinated contrast. In Australia, the Royal Australasian College of Surgeons has endorsed the use of fluorescence-guided surgery with indocyanine green, a near-infrared imaging agent, in oncological procedures, with adoption increasing by 45% since 2021. Additionally, ultrasound contrast agents are being used in targeted drug delivery systems, where microbubbles enhance localized therapy through sonoporation.

MARKET CHALLENGES

Supply Chain Vulnerability for Radioisotope-Based Imaging Agents

The production and distribution of radioisotope-based imaging agents is likely to hinder the growth of the Asia Pacific imaging agents market. Technetium-99m, the most widely used diagnostic isotope in SPECT imaging, has a half-life of only six hours, requiring daily delivery from centralized production facilities. As per the International Atomic Energy Agency, the region depends on reactors in Australia, Canada, and Europe for molybdenum-99 (Mo-99), the parent isotope of Tc-99m, creating logistical bottlenecks. In 2022, a scheduled shutdown at Australia’s OPAL reactor disrupted supply to Indonesia, Malaysia, and the Philippines for over 10 days, affecting thousands of cardiac and bone scans, as reported by the ASEAN Working Group on Radiopharmaceuticals. Similarly, Japan’s reliance on imported Mo-99 was exposed during the 2021 transport delays caused by global shipping disruptions.

Skilled Workforce Shortage in Radiology and Nuclear Medicine

A shortage of trained professionals in radiology and nuclear medicine will also degrade the growth of the Asia Pacific imaging agents market. According to the Asian Oceanian Society of Radiology, the region faces a deficit of over 150,000 radiologists and technologists, with some countries averaging fewer than one radiologist per 100,000 people. In Indonesia, there are only 2,300 certified radiologists for a population of 270 million, as reported by the Indonesian College of Radiology, leading to delayed interpretations and underuse of contrast-enhanced studies. Similarly, in the Philippines, the Department of Health estimates that 60% of existing MRI and CT units operate below capacity due to a lack of qualified operators. Nuclear medicine faces even greater challenges—India has fewer than 500 board-certified nuclear medicine physicians, despite having over 350 PET-CT centers. The complexity of administering and interpreting imaging agents, particularly in molecular and hybrid imaging, requires specialized training that is not uniformly available. In Vietnam, only three universities offer postgraduate programs in radiological technology, producing fewer than 150 graduates annually.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.18% |

| Segments Covered | By Product, Imaging Modality, Country |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of APAC |

| Market Leaders Profiled | Bayer AG, GE Healthcare, Bracco Imaging SpA, Guerbet Group, Lantheus Medical Imaging, Daiichi Sankyo Co., Ltd., Curium Pharma, Telix Pharmaceuticals Ltd., Cardinal Health Inc., Advanced Accelerator Applications (Novartis), Blue Earth Diagnostics, Jubilant Radiopharma, Eckert & Ziegler AG, Y-mAbs Therapeutics, Theragnostics Ltd., Spago Nanomedical AB, Miltenyi Biotec GmbH, SOFIE Biosciences, Iofina plc, NanoMab Technology Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The iodinated contrast media segment held 58.2% of the Asia Pacific imaging agents market share in 202,4, owing to the widespread use of computed tomography (CT) scans across diagnostic centers and hospitals. The increasing prevalence of chronic diseases such as cardiovascular disorders and cancer has significantly elevated the demand for CT imaging, which relies heavily on iodinated contrast agents for enhanced visualization. The World Health Organization estimates that non-communicable diseases account for over 75% of all deaths in the Western Pacific and South-East Asia regions, reinforcing the need for advanced diagnostic imaging. Additionally, the International Atomic Energy Agency reports that CT utilization in low- and middle-income Asian countries has grown by more than 10% annually over the past decade, further amplifying demand. Technological advancements, such as dual-energy CT, which improves tissue characterization, are increasing diagnostic accuracy and driving repeat usage. The availability of cost-effective generic contrast agents in countries like India and China is also expanding access.

The nanoparticle and emerging imaging agents segment is projected to grow with a CAGR of 12.4% from 2025 to 20,33, owing to the rapid advancements in nanotechnology and targeted molecular imaging, particularly in oncology and neurology. Institutions like the National University of Singapore and the RIKEN Center for Advanced Photonics in Japan are pioneering research in iron oxide and quantum dot-based contrast agents by enabling early tumor detection with higher specificity. Additionally, regulatory support is emerging, with China’s National Medical Products Administration fast-tracking approvals for novel agents under its breakthrough therapy designation.

By Imaging Modality Insights

The X-ray and computed tomography (CT) segments accounted in holding 52.3% of the Asia Pacific imaging agents market share in 2024, with the modality’s accessibility, speed, and cost-effectiveness in diagnosing acute and chronic conditions. In countries like India and Indonesia, where healthcare infrastructure is expanding rapidly, mobile and portable X-ray units are being deployed in rural clinics, increasing scan volumes. Cardiovascular diseases remain the leading cause of death, responsible for 60% of all fatalities in China, as reported by the Chinese Center for Disease Control and Prevention, necessitating frequent use of CT angiography. Moreover, trauma care systems in urban centers like Tokyo and Seoul rely heavily on emergency CT for rapid assessment. Public health campaigns, such as China’s National Lung Cancer Screening Program, which targets 50 million high-risk individuals by 2030, are institutionalizing CT-based diagnostics.

The Magnetic resonance imaging (MRI) segment is lucratively growing with an expected CAGR of 10.8% from 2025 to 2033, owing to the rising demand for non-ionizing, high-resolution imaging in neurology, musculoskeletal, and oncology applications. MRI is the gold standard for early detection of neurodegenerative changes. Technological innovations such as 7 Tesla MRI systems, now operational in research hospitals in Singapore and Shanghai, are pushing the boundaries of functional and molecular imaging. Furthermore, the development of safer, macrocyclic gadolinium-based agents has alleviated concerns over nephrogenic systemic fibrosis, restoring clinician confidence.

COUNTRY ANALYSIS

China

China was the top performer of the Asia Pacific imaging agents market by capturing 32.3% the share in 2024. As the region’s largest healthcare market, China’s dominance is anchored in its massive population, rising disease burden, and aggressive healthcare modernization. The government’s Healthy China 2030 initiative has allocated CNY 15 trillion ($2.1 trillion) to upgrade medical infrastructure, including the installation of over 100,000 new imaging devices by 2025. Public hospitals now account for over 90% of contrast-enhanced CT and MRI procedures, and the National Medical Products Administration has fast-tracked approvals for imported and domestic contrast agents. As per the National Cancer Center, 4.82 million new cancer cases occur annually, with lung, liver, and gastric cancers predominant.

Japan

Japan was positioned second in the Asia Pacific imaging agents market with 18.2% of the share in 2024. Japan’s population is the world’s most aged: 29.1% were 65 or older in 2023, according to Japan’s Ministry of Health, Labour and Welfare, which is leading to a high prevalence of age-related conditions like stroke, osteoporosis, and cancer. Japan operates one of the densest imaging infrastructures globally, with 6,800 CT scanners and 4,200 MRI units as of 2022, translating to 54 CT and 33 MRI units per 100,000 people, far exceeding the global average, according to OECD Health Statistics. Universal health coverage ensures near-total access to imaging services, with over 80% of MRI scans using contrast agents, as reported by the Japanese College of Radiology.

IndiaThe

Indian imaging agents market is likely to grow with new opportunities in the coming years. The Indian government’s Ayushman Bharat scheme, the world’s largest health insurance program, provides coverage to 500 million beneficiaries, which is significantly increasing access to imaging services. The number of contrast-enhanced CT scans in India grew by 18% year-on-year in 2022, as reported by the Indian Radiological and Imaging Association. Cardiovascular diseases account for 28% of all deaths, per the Indian Council of Medical Research, necessitating frequent imaging. Private diagnostic chains like Agilus Diagnostics and Metropolis operate over 4,000 collection centers, many equipped with CT and MRI, driving contrast agent usage.

South Korea

South Korea's imaging agents market is likely to grow with the technologically advanced, high-utilization healthcare system. The country excels in diagnostic imaging adoption, supported by universal health coverage, high medical density, and strong government backing for innovation. South Korea performs over 15 million imaging procedures annually, with CT and MRI utilization rates among the highest globally, according to the Health Insurance Review & Assessment Service (HIRA). The country has 45 CT and 30 MRI units per 100,000 people, per OECD data, enabling widespread access. Seoul National University Hospital and Asan Medical Center are global leaders in contrast-enhanced interventional radiology and oncologic imaging. Domestic firms like Taejoon Pharma and Dongkook Pharmaceutical supply a significant portion of iodinated and gadolinium agents. Regulatory reforms by the Ministry of Food and Drug Safety have shortened approval timelines, accelerating market entry.

Australia

Australia's imaging agents market is expected to experience steady growth opportunities in the coming years. The country performs over 8 million medical imaging procedures annually, with Medicare covering 85–100% of costs, ensuring broad access, as reported by the Australian Institute of Health and Welfare. Australia has 112 MRI units per million population, the highest in Asia Pacific, and 45 CT units per million, per OECD Health Statistics, enabling high scan throughput. The government’s Genomics Health Futures Mission, funded with AUD 500 million, integrates imaging with molecular diagnostics, boosting demand for advanced agents. Regulatory rigor through the Therapeutic Goods Administration ensures safety and efficacy, fostering clinician trust.

KEY MARKET PLAYERS

Bayer AG, GE Healthcare, Bracco Imaging SpA, Guerbet Group, Lantheus Medical Imaging, Daiichi Sankyo Co., Ltd., Curium Pharma, Telix Pharmaceuticals Ltd., Cardinal Health Inc., Advanced Accelerator Applications (Novartis), Blue Earth Diagnostics, Jubilant Radiopharma, Eckert & Ziegler AG, Y-mAbs Therapeutics, Theragnostics Ltd., Spago Nanomedical AB, Miltenyi Biotec GmbH, SOFIE Biosciences, Iofina plc, NanoMab Technology Ltd. are the market players that are dominating the Asia-Pacific imaging Agents market.

Top Players in the Market

Bayer AG

Bayer is a leading force in the Asia Pacific imaging agents market, which is renowned for its extensive portfolio of contrast media, including the widely used iodinated agent Ultravist and the MRI contrast agent Gadavist. The company has deep-rooted partnerships with major hospitals and diagnostic chains across China, India, and Japan, enabling widespread product adoption. Bayer has intensified its focus on regulatory approvals in emerging markets, recently securing fast-track clearance for Gadavist in South Korea for expanded neurological indications. It has also invested in localized manufacturing support and clinical training programs for radiologists in collaboration with academic institutions in Australia and Singapore. In 2023, Bayer launched a digital hub in Shanghai to accelerate clinical data collection and support real-world evidence generation. Its strong R&D pipeline includes next-generation liver-specific MRI agents.

GE HealthCare

GE HealthCare plays a pivotal role in the Asia Pacific imaging agents market by integrating contrast solutions with its advanced imaging hardware platforms, particularly in CT and MRI. The company’s Omnispect line of iodinated contrast media is optimized for use with its Revolution CT scanners, ensuring seamless workflow in hospitals across Japan, Australia, and India. GE HealthCare has strengthened its presence through localized production and distribution agreements in Southeast Asia, including a 2023 partnership with Thailand’s BDMS to supply contrast agents across its 50+ hospital network. The company launched the “Precision Care Initiative” in 2024, offering bundled imagin/u]’ok5 y[]7oi8u7/;b .,k 78;k67]k6g systems and contrast protocols to private healthcare providers in Indonesia and Vietnam. It has also collaborated with Australia’s CSIRO to develop low-osmolar contrast agents tailored for renal-impaired patients. GE HealthCare’s recent integration of AI-powered dose optimization tools in its platforms reduces contrast usage while maintaining image quality, improving safety and efficiency.

Guerbet

Guerbet is a specialized global leader in contrast media and injection systems, with a strong footprint in the Asia Pacific region in MRI and CT contrast agents. The company’s Dotarem (gadolinium-based) and Xenetix (iodinated) are widely adopted in Japan, China, and Australia due to their proven safety profiles and regulatory compliance. Guerbet has expanded its regional influence through strategic collaborations with local distributors and radiology societies to promote best practices in contrast administration. In 2023, it launched a dedicated Asia Pacific Innovation Center in Singapore, focusing on clinical research and training for advanced imaging protocols. The center supports trials on new agents for liver and prostate imaging in partnership with Singapore General Hospital. Guerbet also introduced the OptiVantage injector system in Japan and South Korea by enhancing precision in contrast delivery. Its partnership with Japanese AI firm Preferred Networks integrates injection data with imaging analytics for personalized dosing.

Top Strategies Used By Key Market Participants

Key players in the Asia Pacific imaging agents market are deploying multifaceted strategies to consolidate their positions and capture emerging opportunities. A dominant approach is vertical integration, where companies combine contrast agents with imaging hardware and software—GE HealthCare and Siemens Healthineers lead this trend by bundling contrast protocols with CT and MRI systems. Strategic partnerships with local healthcare providers and governments are widespread, enabling market access and regulatory navigation, as seen in Bayer’s collaborations with public hospitals in China. Localization is another strategy firms are establishing regional manufacturing, R&D centers, and distribution hubs in India, Singapore, and Malaysia to reduce costs and improve supply chain resilience. Guerbet’s Innovation Center in Singapore exemplifies this shift. Companies are also investing heavily in digital health integration, incorporating AI-driven dose optimization and teleradiology platforms to enhance contrast utilization efficiency. Regulatory acceleration is pursued through fast-track submissions in high-growth markets like Indonesia and Vietnam. Furthermore, player differentiation is achieved via clinical education programs, training radiologists on safe contrast use and advanced protocols. Mergers and acquisitions are less common but emerging, with firms acquiring AI or software startups to enhance smart imaging ecosystems.

COMPETITION OVERVIEW

The competition in the Asia Pacific imaging agents market is intense and evolving, shaped by a mix of global pharmaceutical giants, regional specialists, and rising domestic manufacturers. Established players like Bayer, GE HealthCare, and Guerbet dominate through technological innovation, extensive portfolios, and integrated imaging solutions. Their strength lies in brand recognition, regulatory expertise, and deep collaborations with healthcare systems across Japan, Australia, and South Korea. However, they face growing pressure from local companies in India and China, such as Wandong Medical and Jiangsu Hengrui, which offer cost-effective alternatives and benefit from government support for self-reliance in medical supplies.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Bayer launched a clinical training academy in Shanghai, China, to educate radiologists on advanced contrast protocols and safety by enhancing adoption of its MRI and CT agents across East Asia.

- In March 2023, GE HealthCare partnered with Bangkok Dusit Medical Services in Thailand to supply integrated imaging systems and contrast media across its 52-hospital network by expanding access in Southeast Asia.

- In August 2023, Guerbet inaugurated its Asia Pacific Innovation Center in Singapore, focusing on clinical research, AI integration, and training for next-generation contrast agents and injection systems.

- In November 2023, Siemens Healthineers introduced the Acuson Redwood ultrasound platform in Japan and Australia, which features optimized microbubble contrast imaging for liver and tumor assessments.

- In April 2024, Fujifilm received PMDA approval in Japan for a new liver-specific gadolinium-based contrast agent by expanding its portfolio and strengthening its presence in precision MRI diagnostics.

MARKET SEGMENTATION

This research report on the Asia Pacific imaging agents market is segmented and sub-segmented into the following categories.

By Product Type

- Iodinated Contrast Media

- Gadolinium-based Contrast Media

- Microbubble Ultrasound Contrast

- Barium-based Contrast Media

- Nanoparticle & Other Emerging Agents

By Imaging Modality

- X-ray / CT

- Magnetic Resonance Imaging (MRI)

- Ultrasound

- Nuclear Imaging (PET / SPECT)

- Others

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC

Frequently Asked Questions

What is the current market size of the Asia Pacific imaging agents market?

As of 2024, the Asia Pacific imaging agents market is estimated at USD 1.43 billion, driven by rising diagnostic imaging procedures and healthcare modernization across key economies.

What is the projected market value by 2033?

The market is anticipated to reach approximately USD 2.49 billion by 2033, reflecting strong growth in medical diagnostics and hospital infrastructure development.

What is the expected CAGR during the forecast period (2025–2033)?

The market is forecasted to grow at a CAGR of 7.18% from 2025 to 2033, supported by increasing disease burden and technological adoption in radiology.

What are imaging agents, and how are they used?

Imaging agents (or contrast agents) are substances used in medical imaging—such as MRI, CT, ultrasound, and nuclear imaging—to enhance the visibility of internal body structures, improving diagnostic accuracy.

Which imaging modalities dominate the use of contrast agents in the region?

Computed Tomography (CT) leads in usage due to widespread availability and fast scanning, followed by Magnetic Resonance Imaging (MRI) and nuclear medicine (PET/SPECT).

What are the main types of imaging agents in the market?

The market includes iodinated agents (CT), gadolinium-based agents (MRI), microbubble agents (ultrasound), and radiopharmaceuticals (nuclear imaging).

Which countries are the major contributors to market growth?

China, Japan, India, South Korea, and Australia are key markets, with China and India showing the fastest growth due to expanding healthcare access and rising imaging volumes.

What factors are driving demand for imaging agents in Asia Pacific?

Key drivers include rising prevalence of chronic diseases (cancer, cardiovascular, neurological), growing geriatric population, increasing healthcare spending, and expansion of diagnostic imaging centers.

How is government healthcare policy influencing the market?

In countries like India and Indonesia, government initiatives to improve diagnostic infrastructure and insurance coverage are increasing access to imaging services and, by extension, contrast agents.

Are there concerns about the safety of imaging agents?

Yes. Issues such as nephrogenic systemic fibrosis (linked to certain gadolinium agents) and allergic reactions have led to stricter usage guidelines and a push for safer, low-risk formulations.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com