Asia Pacific Insomnia Market Size, Share, Growth, Trends, and Forecast Report – Segmented By Distribution Channel (Hospital, Retail, and Others), Therapy Type, and Region (India, China, Japan, South Korea, Australia & New Zealand, Thailand) - Industry Analysis from 2026 to 2034

Market Size, 2025

$195 MnMarket Estimate, 2026

$211 MnMarket Forecast, 2034

$395 MnCAGR, 2026–2034

8.14%Executive Summary: Asia Pacific Insomnia Market

- Market Scope: Comprehensive regional Asia-Pacific insomnia market analysis covering distribution channels, therapy types, country-level leadership frameworks, and clinical prevalence metrics.

- Market Valuation: Valued at USD 195.43 million (2025 base year), estimated at USD 211.34 million (2026), and projected to reach USD 395.25 million by 2034, registering a strong CAGR of 8.14% (2026–2034).

- Primary Growth Drivers: High prevalence of sleep disorders, rising stress and lifestyle factors, and growing adoption of digital therapeutics. Key clinical and demographic highlights include >30.94% of adults across China, India, and Australia reporting clinically significant insomnia symptoms (nearly one in four adults affected overall), >60 million people in Asia-Pacific suffering from depression, 38.98% of Chinese adults reporting chronic insomnia, 27.71% of Japanese adults affected, and 30.95% of young South Koreans exhibiting insomnia linked to smartphone use. Additionally, >150,000 Australians accessed online insomnia portals in 2023, and regional digital therapeutic investments have risen 55.06% since 2022.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Distribution Channel | Retail Distribution (dominated with 48.08% of the market in 2025) | “Others” & Digital/Telemedicine Platforms (projected at fastest CAGR of 12.9%) |

| By Therapy Type | Pharmacological Therapies (led with a 63.9% share in 2025) | Non-Pharmacological Therapies & Digital CBT-I (forecasted at fastest CAGR of 14.2%) |

| By Therapeutic Intervention | Prescription Sleep Aids, Sedatives, & Traditional Clinical Care | AI-Powered Sleep Apps, Telemedicine, & Personalized Therapeutics |

| By Country / Region | China (led regional market with a 25.06% share in 2025) | Advanced Digital Healthcare & Sleep Technology Hubs (e.g., Australia & South Korea) |

Major Market Players & Market Structure

Market Structure: Highly competitive Asia-Pacific pharmaceutical and digital health landscape featuring major global drug manufacturers and health-tech enterprises competing intensely on next-generation pharmacotherapies, digital cognitive behavioral therapy for insomnia (CBT-I), AI-powered sleep applications, telemedicine delivery, and personalized treatment frameworks.

Key Companies: Currax Pharmaceuticals, Eisai, Merck Group, Pfizer, Vanda Pharmaceuticals, Cadila Healthcare, Sanofi, Viatris, Takeda Pharmaceutical, and Purdue Pharma.

Asia Pacific Insomnia Market Size

Asia Pacific Insomnia market size was valued at USD 195.43 million in 2025, and the market size is expected to reach USD 395.25 million by 2034 from USD 211.34 million in 2026. The market's promising CAGR for the predicted period is 8.14%.

The insomnia market growth is driven by the high prevalence of this sleep disorder which is characterized by difficulty in initiating or maintaining sleep. This condition often results in significant daytime impairment and a reduced quality of life thus fueling demand for effective treatments and management solutions. The Asia Pacific insomnia market encompasses a wide range of therapeutic interventions including prescription medications along with over-the-counter sleep aids, digital therapeutics, cognitive behavioral therapy for insomnia (CBT-I) and lifestyle management solutions. These offerings are increasingly being adopted across both public and private healthcare sectors as awareness about sleep health continues to evolve. In the Asia Pacific region, the burden of insomnia has risen sharply due to changing lifestyle patterns, increased work-related stress, urbanization and an aging population. More than 30.94% of adults in countries like China, India and Australia report clinically significant insomnia symptoms. Insomnia affects nearly one in four adults with a rising trend observed among younger populations due to excessive screen time and irregular sleep schedules. Governments and healthcare organizations across the region have begun emphasizing the integration of sleep medicine into primary care systems. In Singapore, the Ministry of Health has launched national campaigns promoting sleep hygiene while in South Korea, telemedicine platforms offering remote CBT-I sessions have gained traction. The Asia Pacific insomnia market is witnessing a shift toward multidisciplinary treatment approaches that combine pharmacological and non-pharmacological interventions and is driven by growing recognition of the economic and health impacts of untreated insomnia.

MARKET DRIVERS

Rising Prevalence of Stress and Mental Health Disorders

Stress and mental health disorders are playing a pivotal role in propelling the growth of the Asia Pacific insomnia market. Acceleration of urbanization and intensifying professional demands are contributing to rising levels of chronic stress, anxiety and depression among the working-age population all of which are strongly associated with disrupted sleep patterns. Over 60 million people in the Asia Pacific region suffer from depression which is a key contributor to insomnia. Over 25.62% of the country’s adult population experiences work-related stress with sleep disturbances often being an early manifestation. In China, nearly 38.17% of respondents reported persistent insomnia symptoms linked to psychological distress particularly in high-pressure industries such as finance and technology. Individuals diagnosed with anxiety disorders are twice as likely to develop chronic insomnia compared to the general population.

Increasing Awareness and Healthcare Infrastructure Development

Growing awareness of sleep disorders coupled with the development of healthcare infrastructure across the Asia Pacific region is a significant driver fueling the insomnia market. Enhanced capabilities in diagnosing and effectively treating insomnia are leading to increased demand for therapeutic solutions and sleep health services. Public health initiatives, media campaigns and digital outreach programs have played a crucial role in educating patients and clinicians alike about the importance of identifying and managing insomnia rather than dismissing it as a transient issue.In Singapore government-backed campaigns have led to a 40.83% increase in the number of individuals seeking professional help for sleep problems. In India, the launch of dedicated sleep clinics in major cities such as Mumbai, Delhi and Bangalore has improved access to diagnostic polysomnography and structured insomnia therapy programs. The number of certified sleep specialists in the country increased by nearly 25.67% between 2020 and 2025 thereby reflecting a broader institutional commitment to sleep health.Similarly, in Australia, the inclusion of insomnia screening tools in primary care settings has resulted in earlier diagnosis and intervention. The adoption of online cognitive behavioral therapy for insomnia (CBT-I) has surged which is facilitated by the expansion of digital health platforms. These developments indicate a structural shift toward recognizing insomnia as a treatable medical condition thereby creating a conducive environment for market expansion.

MARKET RESTRAINTS

Cultural Stigma and Underreporting of Sleep Disorders

The prevailing cultural stigma associated with sleep disorders and mental health conditions is one of the most significant obstacles hindering the growth of the Asia Pacific insomnia market . Insomnia is often perceived as a personal weakness or a minor inconvenience rather than a serious medical concern. This misconception leads to widespread underreporting and delayed diagnosis thus limiting the reach of evidence-based treatments. Fewer than 20.19% of individuals suffering from chronic insomnia seek professional medical help in countries like Indonesia, Thailand and the Philippines. In Japan, societal expectations around endurance and productivity discourage individuals from acknowledging sleep difficulties while contributing to high rates of undiagnosed cases. In rural areas of India where traditional healing practices remain dominant yet many patients rely on home remedies instead of consulting sleep specialists. Additionally, misconceptions about pharmaceutical interventions such as concerns about dependence on sleep medications which further deter patients from adhering to prescribed therapies. This reluctance results in suboptimal treatment outcomes and reduces the overall demand for insomnia-related products and services

Limited Access to Specialized Sleep Clinics and Trained Professionals

Access to specialized sleep clinics and trained professionals remains limited across much of the Asia Pacific region is acting as a major restraint on market growth. Insomnia diagnosis and treatment often require multidisciplinary expertise involving neurology, psychiatry and respiratory medicine in areas where clinician shortages persist. There is less than one sleep specialist per million population in several Southeast Asian countries including Vietnam, Laos and Papua New Guinea. In India, despite having a vast healthcare network only 12 states have fully equipped sleep disorder centers thereby leaving large sections of the population without access to standardized insomnia diagnostics. Fewer than 10.18% of medical colleges offer formal training in sleep medicine thus exacerbating the shortage of qualified practitioners. In China, urban hospitals have established sleep units but there is a stark disparity in service availability between Tier I and Tier III cities. Nearly 70.58% of individuals in rural provinces never receive a formal insomnia diagnosis due to lack of local resources.

MARKET OPPORTUNITIES

Expansion of Digital Therapeutics and Telehealth Platforms

The rapid proliferation of digital therapeutics and telehealth platforms presents a transformative opportunity for the Asia Pacific insomnia market. Digital cognitive behavioral therapy for insomnia (CBT-I) is emerging as a scalable and cost-effective alternative to traditional face-to-face consultations with increasing smartphone penetration, internet accessibility and consumer acceptance of virtual health services. Several countries in the region have already embraced this shift. In Australia, government-supported telehealth services now include digital CBT-I modules thereby enabling remote patient engagement and monitoring. Over 150,000 individuals accessed online insomnia therapy portals in 2023 alone thus demonstrating strong user adoption. Similarly, in South Korea, the Ministry of Health has integrated AI-powered sleep coaching apps within its national digital health initiative which allows real-time feedback and behavioral tracking.In India, startups such as Mindhouse and Qeepsake have introduced mobile-based meditation and guided sleep programs tailored to local demographics while reaching millions of users who may not otherwise engage with conventional insomnia treatments. In Japan, partnerships between tech firms and academic institutions have led to the development of wearable-integrated insomnia management systems that monitor sleep patterns and deliver personalized recommendations.

Integration of Traditional Medicine and Lifestyle Interventions

Integration of traditional medicine and lifestyle-based interventions into mainstream insomnia management strategies presents another promising avenue for growth in the Asia Pacific insomnia market. Countries such as China, India and Thailand have long-standing holistic health traditions such as Ayurveda, Traditional Chinese Medicine (TCM) and Thai herbal therapies that emphasize natural approaches to sleep improvement. Over 60.84% of individuals in China use some form of TCM for sleep-related issues ranging from acupuncture to customized herbal formulations. Adaptogenic herbs like ashwagandha and jatamansi can significantly improve sleep onset and duration when used alongside behavioral therapy. The Indian Ministry of AYUSH has actively supported research into these interventions thereby encouraging their inclusion in national insomnia guidelines. Moreover, wellness tourism and integrative health resorts in countries like Thailand and Bali have started offering insomnia-specific retreats combining yoga, mindfulness, dietary counseling and circadian rhythm regulation. Private healthcare providers are also incorporating these modalities into comprehensive insomnia care packages.

MARKET CHALLENGES

High Cost and Limited Insurance Coverage for Advanced Treatments

High cost of advanced treatment options combined with limited insurance coverage for insomnia-related care remains as one of the foremost challenges impeding the progress of the Asia Pacific insomnia market. While pharmacological therapies, cognitive behavioral therapy and digital health solutions have demonstrated efficacy their affordability remains a barrier for a significant portion of the population in middle- and low-income countries. Insomnia medications such as newer-generation hypnotics and selective serotonin reuptake inhibitors (SSRIs) are often excluded from national health insurance schemes in countries like Indonesia, the Philippines and Bangladesh. In India, despite the rollout of the Ayushman Bharat scheme the outpatient mental health services including insomnia treatment are largely not covered thereby forcing patients to pay out-of-pocket. Nearly 65.47% of patients cited financial constraints as a reason for discontinuing insomnia therapy. Similarly, in Australia and Japan, hospital-based sleep disorder treatments are partially reimbursed whereas coverage for digital CBT-I platforms and wearable sleep monitoring devices remains inconsistent. Financial barriers will continue to limit the scalability of insomnia treatment solutions until comprehensive coverage frameworks are put in place.

Regulatory Heterogeneity and Approval Delays for Innovative Therapies

Regulatory disparities across Asia Pacific countries pose a significant challenge for manufacturers and developers of insomnia treatments which contribute to delays in product launches and market access. The Asia Pacific region features diverse regulatory agencies with varying requirements for drug registration, clinical trial phases and post-marketing surveillance unlike the relatively unified approval pathways seen in the United States and European Union. The average approval timeline for new insomnia medications varies widely ranging from 12 months in Australia to over 24 months in China and Vietnam. In Thailand and Malaysia, regulatory bodies often require additional localized clinical data before approving foreign-developed drugs thus increasing development costs and slowing commercialization efforts. In Japan, while the Pharmaceuticals and Medical Devices Agency (PMDA) offers expedited review for select mental health treatments and submission dossiers must still align with Japan-specific Good Clinical Practice (GCP) standards that complicate multinational trials. These inconsistencies not only delay patient access but also hinder innovation by discouraging smaller biotech firms from entering the regional market. As the insomnia landscape evolves with new biological targets and digital therapeutics thereby harmonizing regulatory frameworks will be essential to accelerate the availability of novel treatments across the Asia Pacific.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.14% |

| Segments Covered | By Distribution Channel, Therapy Type, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, and the Rest of Asia-Pacific |

| Market Leaders Profiled | Currax Pharmaceuticals LLC (Currax Holdings USA LLC), Eisai Co., Ltd., Merck Group, Pfizer, Inc., Vanda Pharmaceuticals, Inc., Cadila Healthcare Ltd. (Zydus Cadila), Sanofi S.A., Viatris, Inc., Takeda Pharmaceutical Company Limited, and Purdue Pharma L.P, and others |

SEGMENTAL ANALYSIS

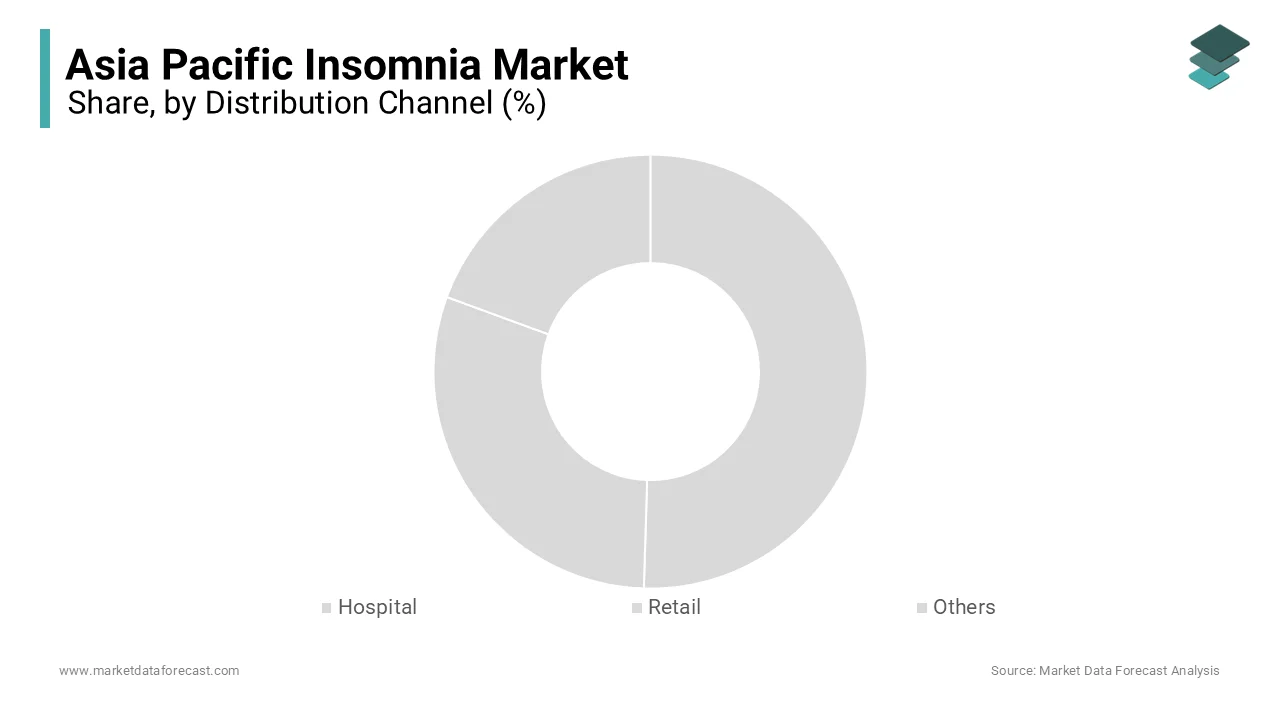

By Distribution Channel Insights

The retail segment dominated the Asia Pacific insomnia market by capturing 48.08% of total market share in 2025. This segment includes over-the-counter (OTC) sleep aids, herbal supplements and non-prescription melatonin formulations that are readily accessible in pharmacies, drugstores and online health platforms. A key driver behind this segment’s growth is the high consumer preference for self-managed treatment options without requiring formal medical consultation. In Australia, sales of natural sleep remedies have increased by 25.95% since 2021 thus reflecting a growing reliance on retail-based solutions. Additionally, rising awareness and aggressive marketing by manufacturers contribute to sustained demand in the retail space. In China, local brands such as Focustheory and Zhongcheng have expanded their presence through e-commerce channels thereby reaching millions of consumers across urban and rural areas.

The "Others" segment is predicted to witness the highest CAGR of 12.9% between 2026 to 2034 and is supported by the rising adoption of digital therapeutics, direct-to-consumer telemedicine platforms, wellness apps and corporate wellness programs. This growth is driven by the increasing adoption of digital health solutions for insomnia management especially among younger and tech-savvy populations. One major factor fueling this expansion is the rise of mobile-based cognitive behavioral therapy for insomnia (CBT-I) applications. Over 200,000 users accessed FDA-approved insomnia apps like Sleepio and SHUTi in 2023 alone thereby demonstrating strong engagement with non-traditional treatment modalities. In South Korea, the Ministry of Health launched a national digital sleep health initiative integrating AI-driven sleep tracking into public health services which accelerate accessibility. Similarly, workplace wellness programs in Japan now include sleep monitoring devices and virtual coaching sessions as part of employee mental health benefits. As per Frost & Sullivan, the number of digital insomnia interventions available across the Asia Pacific region has more than doubled since 2021 thereby signaling significant momentum in this emerging distribution category.

By Therapy Type Insights

The pharmacological therapies segment was the largest segment in the Asia Pacific insomnia market by capturing 63.9% of total market share in 2025. This includes prescription medications such as benzodiazepines, non-benzodiazepine hypnotics (Z-drugs), orexin receptor antagonists and off-label antidepressants used for managing both acute and chronic insomnia. A primary driver of this segment’s dominance is the immediate symptomatic relief offered by pharmacological treatments particularly in cases of severe or persistent insomnia. In Japan, prescription rates for Z-drugs such as zolpidem and zaleplon have remained consistently high with over 2 million prescriptions dispensed annually where sleep disorders are often associated with occupational stress. Moreover, regulatory approvals and physician familiarity with established insomnia drugs facilitate their continued use. In Australia, the Therapeutic Goods Administration has approved several next-generation hypnotics including lemborexant and daridorexant thus expanding treatment options. Additionally, in India, clinicians still prescribe medication as initial therapy due to its rapid onset and perceived efficacy despite rising awareness of non-pharmacological alternatives thereby reinforcing the stronghold of pharmacological treatments in the regional insomnia landscape.

The non-pharmacological segment is anticipated to witness a fastest CAGR of 14.2% from 2026 to 2034 and is fueled by increasing concerns about dependency risks associated with sleep medications and a growing preference for holistic, long-term solutions. This category encompasses cognitive behavioral therapy for insomnia (CBT-I), digital therapeutics, mindfulness techniques, lifestyle modifications and complementary therapies such as acupuncture and meditation. One of the key drivers is the rising integration of CBT-I into mainstream healthcare systems. In Australia, government-backed digital health portals now offer subsidized access to online CBT-I platforms while making evidence-based therapy more widely available. Another growth catalyst is the surge in wellness-focused lifestyles among urban professionals. Thailand and Bali have seen a 20.25% annual increase with insomnia-specific retreats gaining popularity. In India, yoga-based sleep interventions have been adopted by corporate organizations as part of employee well-being programs thereby enhancing scalability. Investments in insomnia-focused digital therapeutics across the Asia Pacific region have grown by 55.06% since 2022 thereby emphasizing the transformative trajectory of the non-pharmacological segment.

REGIONAL ANALYSIS

China was the top performer in the Asia Pacific insomnia market with 25.06% of global share in 2025. China's market growth is driven by its vast population base, rapid urbanization and rising prevalence of work-related stress. The country's expanding middle class and increasing disposable incomes have led to greater spending on sleep health products and consulting services. Over 38.98% of adults report chronic insomnia symptoms with the highest incidence among professionals in technology, finance and healthcare sectors. In response, the National Healthcare Security Administration has introduced policies to improve insurance coverage for mental health conditions including insomnia diagnostics and treatment. China remains a central force shaping the trajectory of the Asia Pacific insomnia market with robust government support and rising consumer demand.

India was positioned second in holding the dominant share of the Asia Pacific insomnia market in 2025 owing to its rapidly evolving healthcare landscape marked by increasing awareness, lifestyle changes and a growing burden of sleep disorders. Urbanization as well as shift work culture and rising mental health concerns have contributed to higher insomnia prevalence among working-age populations. More than one in four adults experience clinically significant insomnia symptoms with a majority seeking pharmacological intervention as initial treatment. The Ministry of Health and Family Welfare has recently updated its mental health policy to emphasize early diagnosis and structured treatment pathways for insomnia thereby encouraging integration with primary care services.

Japan’s insomnia market growth is driven by its aging demographic structure along with high healthcare expenditure and well-established mental health infrastructure. The country faces a disproportionately high burden of insomnia due to excessive work hours, cultural expectations and an aging population increasingly prone to sleep disturbances. Nearly 27.71% of Japanese adults suffer from chronic insomnia with many relying on prescribed hypnotic medications. The Ministry of Health, Labour and Welfare has implemented initiatives promoting healthier work-life balance including mandatory sleep disorder screening for employees in high-stress industries.

Australia’s insomnia market is likely to grow with a healthy CAGR in the next coming years and is distinguished by its progressive healthcare policies, high adoption of digital therapeutics and growing emphasis on sleep medicine as a specialty. The country’s well-developed mental health framework supports early diagnosis and multidisciplinary treatment strategies for insomnia. Over 1.4 million people suffer from chronic insomnia with increasing numbers seeking non-pharmacological alternatives such as cognitive behavioral therapy and digital sleep coaching. The Department of Health has integrated sleep disorder screening into general practitioner training programs thereby improving frontline identification and referral rates.

South Korea’s insomnia market is likely to have significant growth opportunities during the forecast period and is driven by technological innovation, digital health integration and a highly developed healthcare system. The country has embraced sleep medicine as a priority area in addressing insomnia linked to academic and professional pressures. Nearly 30.95% of young adults exhibit insomnia symptoms associated with excessive smartphone use and irregular sleep schedules. In response, the Ministry of Health and Welfare has introduced digital insomnia clinics offering AI-assisted diagnostics and remote therapy via mobile applications. Academic institutions like Seoul National University Hospital are conducting extensive research on neuroimaging and biomarker-based insomnia diagnostics.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Currax Pharmaceuticals LLC (Currax Holdings USA LLC), Eisai Co., Ltd., Merck Group, Pfizer, Inc., Vanda Pharmaceuticals, Inc., Cadila Healthcare Ltd. (Zydus Cadila), Sanofi S.A., Viatris, Inc., Takeda Pharmaceutical Company Limited, and Purdue Pharma L.P are the key players in the Asia Pacific insomnia market.

The competition in the Asia Pacific insomnia market is intensifying as multinational pharmaceutical giants and emerging domestic players vie for dominance through differentiated treatment modalities and strategic innovations. Established firms such as Takeda, Eisai and Johnson & Johnson maintain a strong foothold due to their advanced drug portfolios, robust R&D capabilities and well-established distribution networks. These companies are increasingly focusing on next-generation therapies that offer improved safety profiles and reduced dependency risks compared to conventional hypnotic medications. At the same time, new entrants particularly in the digital therapeutics space are disrupting the market landscape by offering cost-effective, scalable solutions tailored to younger and tech-savvy consumers. Startups specializing in AI-driven sleep coaching and mobile-based CBT-I platforms are gaining traction in urban centers where mental health awareness is rising. Additionally, increasing regulatory support for sleep disorder management coupled with rising consumer preference for personalized treatment options is reshaping competitive dynamics. As stakeholders navigate evolving treatment paradigms and shifting patient expectations while differentiation through innovation, localization and multidisciplinary care models has become crucial for sustained market dominance.

TOP PLAYERS IN THE MARKET

Takeda Pharmaceutical Company (Japan)

Takeda is a leading force in the Asia Pacific insomnia market and is known for its innovative sleep disorder therapies and deep-rooted presence across the region. The company’s portfolio includes next-generation insomnia medications that target orexin receptors while offering safer alternatives to traditional hypnotics. Takeda actively collaborates with regulatory bodies and academic institutions to promote evidence-based insomnia treatment guidelines thereby reinforcing its influence in shaping clinical practices. Its strong research pipeline continues to explore novel biological pathways for chronic insomnia and contributes significantly to global advancements in sleep medicine.

Eisai Co., Ltd. (Japan)

Eisai plays a pivotal role in the Asia Pacific insomnia market through its development of targeted pharmacotherapies and its commitment to improving patient outcomes. The company has been instrumental in introducing orexin receptor antagonists that provide improved safety profiles and long-term efficacy. Eisai supports public health initiatives focused on sleep hygiene education and early diagnosis of insomnia disorders. Eisai continues to drive awareness and adoption of comprehensive insomnia management strategies that extend beyond medication alone.

Johnson & Johnson (United States)

Johnson & Johnson contributes significantly to the Asia Pacific insomnia market by delivering integrated treatment approaches that combine pharmacological and digital interventions. The company's focus on mental health innovation has led to investments in digital therapeutics and cognitive behavioral therapy platforms tailored for insomnia. J&J enhances access to holistic sleep solutions and supports the shift toward multimodal treatment strategies across diverse patient populations in the Asia Pacific region.

TOP STRATEGIES USED BY KEY PLAYERS

Expanding digital health offerings such as AI-powered sleep therapy apps and teleconsultation platforms is one of the primary strategies employed by key players in the Asia Pacific insomnia market.Companies are increasingly investing in scalable digital cognitive behavioral therapy (CBT-I) solutions to address growing consumer demand for non-pharmacological treatment options.

Another critical approach is strengthening regional partnerships with local healthcare providers and government agencies. Companies enhance product accessibility and improve patient outreach as well as ensure better integration of insomnia treatments into mainstream care pathways by aligning with national health programs and hospital networks.

There is a strong emphasis on developing culturally relevant treatment protocols and localized marketing campaigns. Recognizing the diversity in sleep patterns, lifestyle habits as well as cultural attitudes toward insomnia these firms are tailoring their messaging and therapeutic approaches to resonate more effectively with different Asian populations thereby increasing acceptance and adherence to treatment regimens across the region.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Takeda Pharmaceutical launched a dedicated insomnia research center in Tokyo aimed at accelerating the development of novel therapies targeting neurochemical imbalances associated with chronic sleep disturbances.

- In May 2025, Eisai Co., Ltd. partnered with a leading South Korean telemedicine platform to integrate its insomnia management protocols into digital health consultations thereby enabling remote monitoring and personalized treatment adjustments.

- In August 2025, Johnson & Johnson entered into a joint venture with an Indian wellness startup to develop localized insomnia solutions combining behavioral therapy, Ayurvedic insights and wearable sleep tracking technology.

- In October 2025, Otsuka Pharmaceutical expanded its insomnia-focused clinical trial network across Southeast Asia thereby initiating studies in Thailand, Vietnam and Malaysia to gather region-specific efficacy data.

- In December 2025, Sumitomo Dainippon Pharma acquired a Singapore-based sleep diagnostics firm to enhance its capability in precision insomnia treatment planning.

MARKET SEGMENTATION

This research report on the Asia Pacific insomnia market has been segmented and sub-segmented based on the following categories.

By Distribution Channel

- Hospital

- Retail

- Others

By Therapy Type

- Pharmacological

- Non-Pharmacological

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What are the key growth opportunities in the Asia Pacific insomnia market?

Rising stress levels, increasing awareness of mental health, and greater access to sleep disorder treatments are driving growth in the insomnia market across the Asia Pacific region.

2. What trends are shaping the Asia Pacific insomnia market?

Trends include growing adoption of cognitive behavioral therapy for insomnia (CBT-I), increased use of digital sleep-tracking tools, and the development of novel sleep aids with fewer side effects.

3. What challenges does the Asia Pacific insomnia market face?

Major challenges include social stigma around mental health treatment, underdiagnosis of sleep disorders, and side effects associated with long-term use of sedative medications.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com