- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Asia Pacific Interventional Cardiology Market Size

The Asia Pacific interventional cardiology market was worth USD 1.79 billion in 2025. The Asia Pacific market is expected to reach USD 3.54 billion by 2034 from USD 1.93 billion in 2026, rising at a CAGR of 7.87% from 2026 to 2034.

The Asia Pacific interventional cardiology market is driven by a broad range of medical devices and technologies used for minimally invasive diagnosis and treatment of cardiovascular diseases. This includes percutaneous coronary interventions, structural heart disease corrections and peripheral vascular procedures. The region has witnessed a paradigm shift in cardiovascular care due to rising adoption of advanced catheterization techniques, growing patient awareness and increasing healthcare investments. Cardiovascular diseases account for over 30.91% of total mortalities across Asia Pacific countries with India and China contributing significantly to this burden. Nearly 54.4 million people in India suffer from cardiovascular diseases which underlines the critical need for interventional solutions. Similarly, Japan’s aging population has led to a surge in demand for minimally invasive cardiac procedures and is supported by government initiatives aimed at strengthening tertiary healthcare infrastructure. Australia, reports a consistent rise in hospitalizations related to coronary artery disease. Technological advancements such as fractional flow reserve-guided stenting, bioresorbable scaffolds and robotic-assisted systems have further catalyzed the growth trajectory.

MARKET DRIVERS

Rising Prevalence of Coronary Artery Disease Across Urban Populations

The soaring prevalence of coronary artery disease (CAD) in urban centers is one of the primary drivers of the Asia Pacific interventional cardiology market and is fueled by sedentary lifestyles along with unhealthy diets and rising tobacco consumption. Nearly 213 million adults in the Asia Pacific region were living with diabetes in 2021 which is a key comorbid condition that exacerbates CAD progression. In China alone there are 11 million individuals suffering from stable angina which is a common manifestation of CAD necessitating interventional management. Similarly, in Singapore, ischemic heart disease accounted for nearly 27.63% of all deaths in 2022 thus reflecting a significant strain on public health systems. These alarming figures are prompting increased adoption of percutaneous coronary interventions (PCIs) especially in Tier-1 cities where access to specialized care is improving. Moreover, Japan exhibits one of the highest rates of aging populations globally with over 29.18% of its citizens aged above 65 years. Elderly patients often present with complex coronary pathologies thereby making them prime candidates for interventional cardiology procedures. Consequently, the confluence of demographic shifts, lifestyle changes and chronic disease burdens is amplifying regional demand for advanced interventional therapies.

Expansion of Healthcare Infrastructure and Medical Tourism Hubs

Expansion of healthcare infrastructure and medical tourism hubs in emerging economies like Thailand, India and Malaysia is another pivotal driver of the Asia Pacific interventional cardiology market while positioning these countries as preferred destinations for advanced cardiovascular treatments. India attracted over 6.2 million international medical tourists in 2023 in which many seeking cost-effective yet high-quality cardiac interventions unavailable or prohibitively expensive in their home countries. This growth is supported by substantial government investments in healthcare facilities. For instance, Indonesia's Ministry of Health allocated USD 2.1 billion in 2023 toward upgrading cardiovascular care units across major hospitals. In addition, private healthcare providers such as Fortis Healthcare in India and Bumrungrad International Hospital in Thailand have expanded their cardiac intervention divisions by acquiring state-of-the-art angiography systems and hiring skilled interventional cardiologists. The region is witnessing a steady influx of both domestic and international patients with improved insurance coverage, telemedicine integration and cross-border collaboration in medical device procurement thereby reinforcing the scalability of interventional cardiology services.

MARKET RESTRAINTS

High Cost of Advanced Interventional Devices and Procedures

The high cost of advanced interventional devices and procedures is a significant restraint impeding the growth of the Asia Pacific interventional cardiology market. Technologies such as drug-eluting stents, intravascular ultrasound systems and fractional flow reserve measurement tools remain largely inaccessible to low-income populations due to financial constraints. Nearly 40.93% of the population in Southeast Asia lacks adequate health insurance coverage thereby limiting their ability to afford elective or emergency interventional cardiology treatments. In Vietnam, the average cost of a single coronary stent implantation can exceed USD 5,000 which is well beyond the annual income of most households. In the Philippines, the Philippine Health Insurance Corporation (PhilHealth) covers only a fraction of interventional costs thus leaving patients to bear the remainder out-of-pocket. Japan, while equipped with some of the world’s most sophisticated cardiovascular care centers faces challenges related to the reimbursement of novel interventional technologies. The Ministry of Health, Labour and Welfare reported that new-generation bioresorbable vascular scaffolds are not widely reimbursed and discourage clinicians from adopting them despite their clinical benefits. Such economic barriers continue to restrict market penetration across diverse consumer segments within the Asia Pacific region.

Regulatory Complexity and Delayed Product Approvals

Another major constraint impacting the Asia Pacific interventional cardiology market is the prolonged and complex regulatory approval process for innovative medical devices. Countries such as China and South Korea impose stringent clinical evaluation requirements which often cause delays in product commercialization. The average time for approving a new interventional cardiology device exceeds 24 months compared to around 12 months in the United States or European Union. This extended timeline hampers the timely introduction of cutting-edge technologies such as robotic-assisted catheter systems and artificial intelligence-integrated diagnostic platforms. In South Korea, the Ministry of Food and Drug Safety mandates multi-phase clinical trials even for devices already approved in other jurisdictions which complicates global manufacturers' entry strategies. Nearly 30.74% of foreign medtech firms delay their market launch in South Korea due to regulatory hurdles. India, despite recent reforms in its medical device approval framework still experiences bottlenecks. Nearly 18.17% of interventional cardiology device applications face rejection in initial assessments due to incomplete compliance documentation.

MARKET OPPORTUNITIES

Growing Adoption of Telehealth and Remote Monitoring in Cardiac Care

The Asia Pacific interventional cardiology market is presented with a significant opportunity through the expanding use of telehealth and remote monitoring systems in postprocedural cardiac care. Digital health adoption has become integral in managing follow-up care for patients who are undergoing interventions such as angioplasty and stent placements. Australia has been at the forefront of integrating remote monitoring into mainstream cardiac rehabilitation programs. Similarly, in Japan, where home-based healthcare is increasingly favored companies like Terumo and Medtronic have launched wearable cardiac monitors that enable real-time data transmission to physicians. In India, Apollo Hospitals launched an AI-driven cardiac analytics platform in 2023 that supports remote diagnostics and procedural planning. This innovation allows interventional cardiologists to assess vessel blockages without requiring frequent in-person visits. The convergence of telemedicine and interventional cardiology is unlocking new avenues for scalable and cost-effective patient engagement models across the Asia Pacific.

Increasing Public-Private Partnerships in Cardiovascular Research and Development

Increasing public-private partnerships in cardiovascular research and development present a compelling opportunity to shape the Asia Pacific interventional cardiology market by advancing innovation and accelerating the introduction of cutting-edge medical devices. Governments across the region are actively collaborating with multinational corporations and academic institutions to enhance local R&D capacities. PPPs in health sciences across Asia Pacific grew by 22.86% annually between 2020 and 2023. China serves as a prime example with the Shanghai Municipal Government partnering with Siemens Healthineers in 2023 to establish an interventional cardiology innovation center focused on developing AI-assisted angiographic imaging systems. Similarly, in South Korea, the Ministry of Science and ICT collaborated with Samsung Medison to advance portable echocardiography devices tailored for rural and underserved communities.India’s Department of Biotechnology has also engaged in multiple joint ventures including one with Abbott Laboratories to co-develop affordable coronary stents adapted for the genetic predispositions of native populations. The Indian Council of Medical Research reported that such partnerships have reduced the development cycle of indigenous interventional devices by up to 30.81%. These collaborative efforts not only accelerate technological advancements but also improve accessibility while positioning the Asia Pacific region as a strategic hub for next-generation cardiovascular innovations.

MARKET CHALLENGES

Shortage of Trained Interventional Cardiologists and Technicians

Shortage of trained interventional cardiologists and catheterization lab technicians is one of the foremost challenges hindering the growth of the Asia Pacific interventional cardiology market. Despite rising demand for minimally invasive cardiac procedures there remains a stark disparity between patient load and available expertise. In several Southeast Asian nations, the number of interventional cardiologists per million population is less than five while compared to over 20 in developed Western markets. In Indonesia, only 460 certified interventional cardiologists serve a population exceeding 275 million thereby leading to long wait times and limited procedural capacity. Similarly, in the Philippines, fewer than 150 specialists are actively performing coronary interventions nationwide. This scarcity constrains the efficient delivery of time-sensitive procedures such as primary angioplasty for acute myocardial infarction. Japan faces a declining pool of young professionals entering interventional cardiology due to demanding workloads and radiation exposure concerns despite its advanced healthcare infrastructure.

Disparities in Access to Interventional Facilities Between Urban and Rural Areas

Uneven distribution of interventional cardiology infrastructure between urban and rural regions is a critical challenge facing the Asia Pacific interventional cardiology market. Metropolitan centers are equipped with state-of-the-art catheterization labs while rural areas often lack basic diagnostic and interventional capabilities. Over 60.88% of the population in countries like India, Bangladesh and Papua New Guinea resides in rural zones with limited access to specialized cardiac care. In India, less than 5.7% of rural districts have operational cath labs thereby forcing patients to travel hundreds of kilometers for treatment. This geographic disparity contributes to delayed interventions and higher mortality rates. Nearly 58.19% of acute myocardial infarction patients in rural India do not receive reperfusion therapy within the recommended 120-minute window. Similarly, in Indonesia, the Ministry of Health revealed that only 12 out of 34 provinces have at least one dedicated interventional cardiology unit. Even in Australia, where healthcare access is generally robust the Royal Flying Doctor Service reported that remote communities face an average delay of 4 hours in reaching facilities capable of performing PCI. These infrastructural imbalances pose a formidable challenge to achieving equitable cardiovascular outcomes across the Asia Pacific region.

SEGMENTAL ANALYSIS

By Device Type Insights

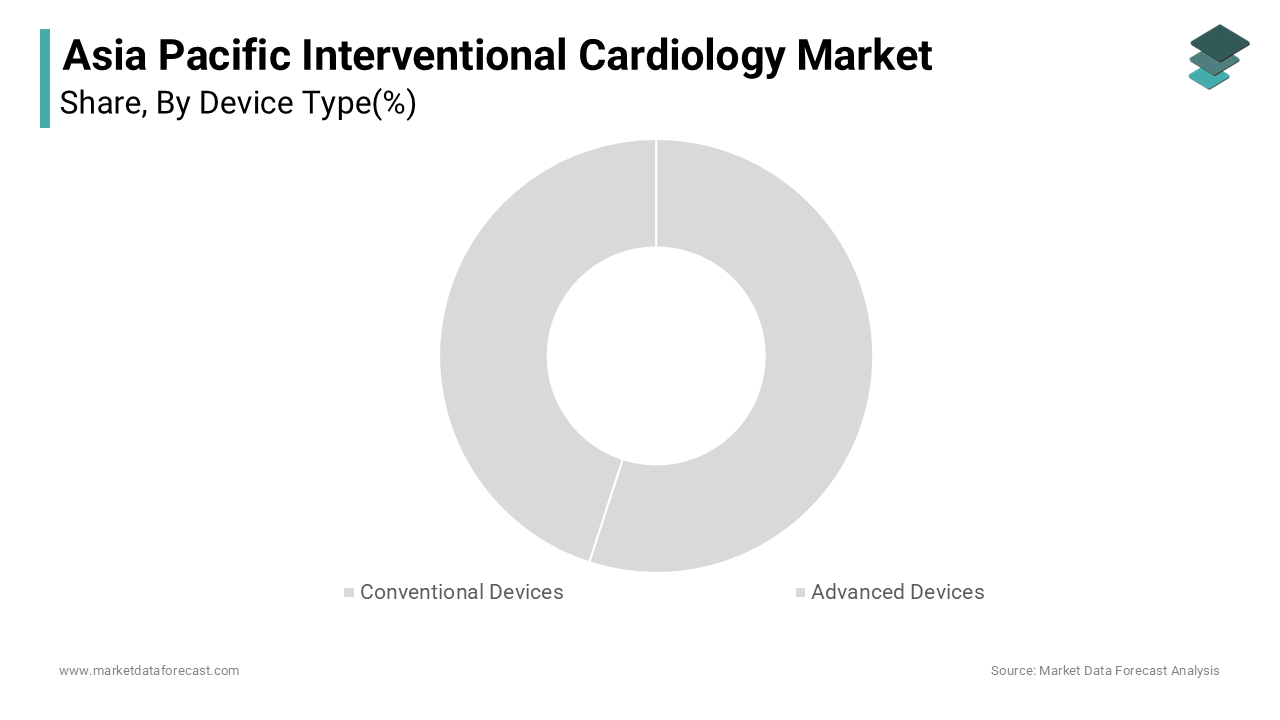

The conventional device segment held the leading share of 58.67% of the total Asia Pacific interventional cardiology market share in 2024. The affordability and widespread adoption of traditional tools such as bare-metal stents, balloon catheters and basic angioplasty systems primarily drives this dominance. Public hospitals in India and Indonesia continue to rely on conventional devices due to budgetary constraints and lack of reimbursement coverage for advanced alternatives. Additionally, in rural areas of China and the Philippines where healthcare spending per capita remains low at USD 450 and USD 610 respectively which cost-effectiveness becomes a crucial decision factor. Coronary interventions in lower-tier cities utilize conventional devices thereby reflecting their entrenched position in resource-limited settings. The vast patient pool suffering from coronary artery disease across the region further fuels demand. In Vietnam alone, over 3 million patients were diagnosed with ischemic heart disease in 2023 most of whom received treatment via conventional interventional methods.

The advanced device segment is predicted to witness a highest CAGR of 12.4% between 2025 and 2033. This growth is predominantly fueled by the increasing integration of innovative technologies such as bioresorbable vascular scaffolds (BVS), fractional flow reserve (FFR)-guided interventions and robotic-assisted catheterization systems. In Japan, which leads the region in technological adoption over 40.9% of PCI procedures conducted in 2023 utilized FFR-based diagnostics. South Korea has witnessed a surge in the use of intravascular ultrasound (IVUS) during complex interventions with a 20.09% year-on-year increase in IVUS-guided procedures. Australia is embracing next-generation solutions where more than 25.13% of cardiac centers now offer robotic-assisted PCI using platforms like CorPath GRX. Coupled with rising health insurance penetration and government-backed innovation funds this shift toward high-precision and minimally invasive tools is underpinning the rapid expansion of the advanced device category across the Asia Pacific region.

By End User Insights

The hospitals segment was the largest end-user segment and held 63.9% of the Asia Pacific interventional cardiology market share in 2024 with the comprehensive infrastructure available in hospital settings including dedicated cath labs, multi-disciplinary teams and access to emergency care units all of which are essential for performing complex cardiovascular interventions. Over 80.17% of coronary interventions in developing economies such as India and Indonesia are conducted within hospital environments which is primarily due to the availability of critical care support and regulatory compliance requirements. In Australia, public and private hospitals accounted for more than 90.7% of PCI procedures in 2023 emphasizing their central role in delivering interventional cardiology services. Furthermore, hospitals benefit from higher investment inflows where India’s Ministry of Health allocated more than USD 1.2 billion in 2023 towards upgrading hospital-based cardiac care units. These combined factors reinforce the continued supremacy of hospitals as the leading end-user segment across the Asia Pacific region.

The cardiac catheterization laboratories segment is on the rise and is expected to be the fastest-growing end-user segment in the global market by witnessing a CAGR of 13.1% between 2025 to 2033. This accelerated growth is attributed to the increasing establishment of standalone cath labs equipped with advanced imaging and interventional capabilities outside of traditional hospital settings. In South Korea, over 30.12% of elective PCI procedures are now performed in specialized cath labs rather than general hospital wards. These facilities offer faster turnaround times, reduced waiting periods and lower operational costs while making them attractive to both providers and patients. Moreover, in Malaysia, private healthcare operators have invested heavily in setting up modular cath labs in secondary cities where hospital infrastructure is limited. Cath labs are emerging as a pivotal growth engine in the Asia Pacific interventional cardiology market with favorable policy support and growing consumer preference for streamlined cardiac care.

REGIONAL ANALYSIS

China outperformed other regions in the Asia Pacific interventional cardiology market in 2024 by accounting for 22.96% of the global market share. As one of the most rapidly aging countries globally with over 280 million people aged 60 or above. More than 1.2 million PCI procedures were performed nationwide in 2023 marking a 14.5% annual increase compared to the previous year. Government initiatives such as the Healthy China 2030 blueprint have prioritized cardiovascular disease management resulting in improved access to interventional therapies across urban and semi-urban regions. Local stent brands now account for over 70.65% of market usage in China thus enhancing affordability and procedure accessibility.

Japan was positioned second in holding the dominant share of the Asia Pacific interventional cardiology market in 2024. More than 29.17% of Japan's population was aged 65 or older in 2023 resulting in a heightened incidence of chronic cardiovascular conditions. The Japanese Circulation Society reported that over 450,000 coronary interventions were conducted in 2022 emphasizing the country’s robust procedural volume. Japan’s universal health insurance system ensures broad coverage of interventional procedures thereby enabling timely access even in remote regions.

India’s interventional cardiology market is likely to have significant growth opportunities during forecast period. A combination of rising cardiovascular disease burden, increasing healthcare expenditure and expanding medical tourism has propelled market growth. Cardiovascular diseases contributed to nearly 28.13% of all deaths in India in 2023 with coronary artery disease being the leading cause. Over 60 million people suffer from some form of cardiovascular illness while creating a substantial demand for interventional procedures. In response, India’s Ministry of Health launched the National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases and Stroke (NPCDCS) by allocating more than USD 300 million to strengthen early diagnosis and treatment. An estimated 4.5 million international patients visited India in 2023 with a notable percentage opting for coronary interventions.

Australia’s interventional cardiology market growth is likely to have fastest growth opportunities in the coming years. The country benefits from a well-established healthcare infrastructure, high physician-to-patient ratios and favorable reimbursement policies that facilitate widespread access to advanced cardiac treatments. Ischemic heart disease remains the second leading cause of death in the country with over 55,000 hospitalizations related to coronary interventions in 2024. The Department of Health also noted a significant uptick in the adoption of minimally invasive technologies including drug-eluting stents and fractional flow reserve (FFR)-guided procedures.

South Korea’s interventional cardiology market growth is driven by its swift adoption of medical technologies, rapidly aging population and a robust national health insurance system. Nearly 17.05% of the population is aged above 65 years thus contributing to a high prevalence of coronary artery disease. The Korean Society of Cardiology reported that PCI procedures surpassed 200,000 in 2023 while demonstrating a steady upward trend over the last decade. Technological advancements play a crucial role in this growth trajectory with institutions like Seoul National University Hospital deploying AI-powered diagnostic platforms and intravascular ultrasound systems for enhanced procedural accuracy.

COMPETITIVE LANDSCAPE

The competition in the Asia Pacific interventional cardiology market is intense and marked by the presence of established global players alongside rapidly growing domestic manufacturers. Multinational corporations dominate due to their strong R&D pipelines, broad product portfolios and well-established distribution networks. However, local firms are gaining traction by offering cost-effective alternatives that cater to the affordability constraints of emerging economies. This dynamic creates a dual-market structure where premium innovation competes with value-driven accessibility. Moreover, the market sees continuous product differentiation strategies with companies focusing on developing technologically advanced devices that improve procedural efficiency and patient outcomes. Companies are also engaging in strategic mergers, acquisitions and joint ventures to consolidate their market presence and gain access to new geographies. In parallel, regulatory reforms and government support for indigenous manufacturing are reshaping the competitive environment thereby giving domestic players an opportunity to challenge global leaders. Additionally, increasing collaboration between industry participants and healthcare institutions is fueling innovation and improving clinical adoption. The battle for market dominance is intensifying thereby prompting companies to adopt multifaceted approaches to sustain growth and relevance.

KEY MARKET PLAYERS

Some of the key market players in the Asia Pacific interventional cardiology market inlcude

- Abbott Laboratories

- Medtronic PLC

- Boston Scientific Corporation

- Terumo Corporation

- B. Braun Melsungen AG

- Cardinal Health (Cordis)

- BIOTRONIK SE & Co. KG

- Biosensors International Group, Ltd.

- MicroPort Scientific Corporation

- Meril Life Sciences

- OrbusNeich

- Opto Circuits

- Vascular Concepts

Top Players in the Asia Pacific Interventional Cardiology Market

One of the leading players in the Asia Pacific interventional cardiology market is Medtronic plc. The company has a strong presence across major markets including Japan, China and Australia while offering a broad portfolio of interventional cardiology devices such as stents, catheters and intravascular imaging systems. Medtronic’s commitment to innovation and strategic collaborations with regional healthcare providers enables it to maintain a dominant position. Its investment in localized R&D and partnerships with academic institutions supports the development of tailored solutions for diverse patient populations across the region.

Another key player is Terumo Corporation, a Japanese multinational medical device manufacturer that plays a pivotal role in shaping the interventional cardiology landscape in Asia. Terumo is particularly strong in vascular access and interventional solutions with a focus on high-quality guidewires, catheters and embolic protection devices. The company's deep understanding of local clinical practices and its extensive distribution network across emerging markets like India and Southeast Asia give it a competitive edge. Terumo also emphasizes continuous product refinement and clinician engagement to improve procedural outcomes.

Boston Scientific Corporation is another global leader with significant influence in the Asia Pacific interventional cardiology market. Boston Scientific offers a comprehensive range of coronary and structural heart intervention products. The company has been actively expanding its footprint through direct investments, joint ventures and training programs aimed at enhancing physician adoption. Its strategic focus on digital health integration and next-generation interventional tools positions it strongly in both developed and developing markets within the Asia Pacific region.

Top Strategies Used by Key Market Participants

Key players in the Asia Pacific interventional cardiology market are increasingly adopting strategic partnerships and collaborations to enhance their technological capabilities and expand their regional footprints. These alliances often involve joint research initiatives with academic institutions as well as co-development agreements with local manufacturers or exclusive distribution arrangements to penetrate untapped markets. Such partnerships enable companies to align with evolving regulatory landscapes and better address region-specific clinical needs.

Another prevalent strategy is localized product development and manufacturing where global firms adapt their offerings to meet the unique requirements of various Asian healthcare systems. This includes modifications in device design, cost-optimization strategies and simplified user interfaces tailored for different levels of clinical expertise. Establishing regional production facilities not only reduces supply chain complexities but also supports pricing competitiveness thereby making advanced interventional solutions more accessible.

Lastly, capacity-building and physician training initiatives have become critical to sustaining long-term growth. Leading companies are investing heavily in hands-on training centers, simulation-based education and digital learning platforms to upskill interventional cardiologists. These efforts drive greater adoption of proprietary technologies while strengthening brand loyalty among key decision-makers in the region.

RECENT MARKET DEVELOPMENTS

- In February 2024, Medtronic launched a dedicated innovation center in Shanghai focused on accelerating the development of interventional cardiology devices tailored for Asian anatomies.

- In May 2024, Terumo Corporation expanded its manufacturing facility in Singapore to increase production capacity for cardiovascular catheters and guidewires.

- Also in June 2024, Boston Scientific partnered with a leading Indian hospital chain to establish regional training institutes for interventional cardiologists.

- In September 2024, Abbott Laboratories introduced a new line of drug-eluting stents in South Korea following regulatory approval.

- In November 2024, Siemens Healthineers collaborated with Chinese tech firm Huawei to integrate AI into diagnostic imaging solutions used during cardiac interventions.

MARKET SEGMENTATION

This research report on the Asia Pacific interventional cardiology market is segmented and sub-segmented into the following categories.

By Device Type

- Conventional Devices

- Advanced Devices

By End User

- Hospitals

- Cardiac Catheterization Laboratories (Cath Labs)

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of APAC